Beautiful!

Soon to be drafted by the military. Did you know U.S. Navy enlists dolphins as “serious military assets?”

https://twitter.com/AMAZlNGNATURE/status/1038419050341101569

Love Mo Cheeks. What a great guy.

Congrats, my brother, making it to the Hall.

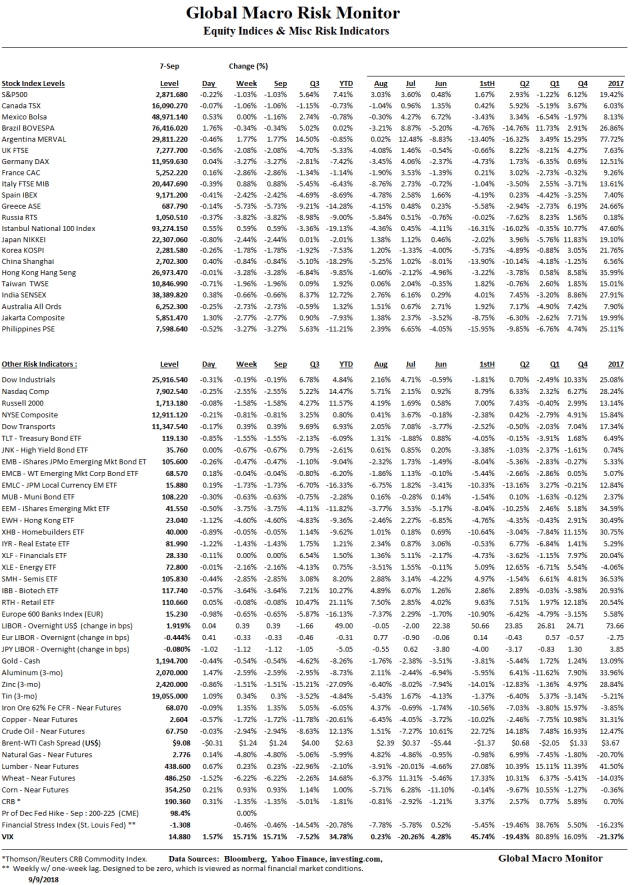

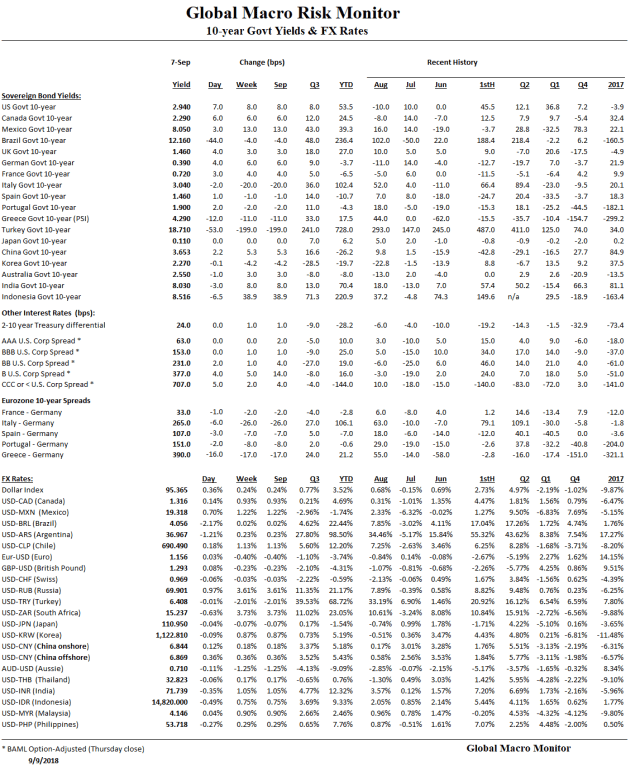

The BLS out with the employment report this morning,

Total nonfarm payroll employment increased by 201,000 in August, and the unemployment rate was unchanged at 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, health care, wholesale trade, transportation and warehousing, and mining. – BLS

Historically average employment growth coupled with an acceleration in average hourly earnings.

Nevertheless, job growth was impressive given the tightening constraint on labor supply, which is starting to show up in higher nominal wage growth.

Ideally, wages grow based on productivity gains and not supply shortages, which are inflationary in nature. The real average hourly earnings growth was pretty much about flat, although relative earnings in some sectors, such as construction, are accelerating. We expect inflation to accelerate x/ a major financial shock.

Political Implications

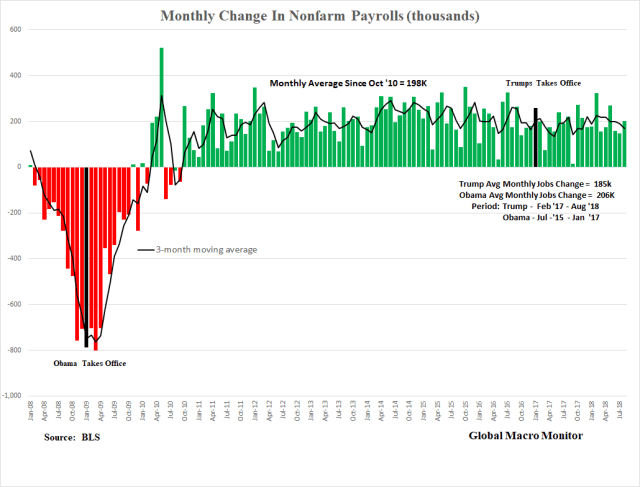

We have been tracking the Trump labor market relative to the Obama labor market for several months now. Though the economy is now growing at almost double the rate than during President Obama’s last six quarters in office, the gains are not being equitably distributed to labor. The size of the surplus labor pool is also shrinking, forcing potential employers to begin to raise wages and pass it on to consumers, creating generalized inflation, or, if possible, choose to automate.

The chart above and following table illustrate our point.

During the last 19 months of the Obama administration, the monthly change in nonfarm payrolls averaged 208k, totaling 3.96 million, versus 185k per month, or 3.58 million, during the first 19 payroll reports of the Trump Administration. There are three more employment reports before midterms and monthly nonfarm payroll gains will have to average 392k in order for the Trump jobs market to catch the Obama job increases, and that just ain’t gonna happen folks.

The latest 3-mo moving average of monthly job gains is now running at 168k versus 204k when President Obama’s left office at the end of January 2017.

The labor market is supply constrained and continued strong economic growth is going to translate into wage inflation, which will be passed on in general price increases.

The Trump administration deserves kudos for reviving manufacturing employment, but, surprisingly, wage growth in that sector is much lower under Trump. We suspect this has to do with relatively greater slack in the manufacturing labor market.

Retailgeddon

Also note the zero job growth in the retail since Trump took office. The new rust belt.

This could result in some political pressure on Republicans during the midterms as retail trade is the fourth largest employment sector among private employers. Also note that in many of the red states, WalMart is the largest private employer.

The retail subsector — warehouse clubs and supercenters — the category where WalMart lives, has experienced negative job growth under President Trump, losing 25k (last data point is July) jobs since January 2017. We suspect automation forced by competition from Amazon as the main jobs destoryer.

The retail average hourly earnings have grown at a compounded annual rate of 2.92 percent under President Trump.

Earnings Growth

The overall nominal average hourly earnings growth rate is running about 46 bps higher under Trump, but the relative purchasing power is offset by higher inflation. Real wages are slightly higher under Obama than Trump.

Nevertheless, we think the economic impact on the midterm vote is asymmetric from now until the election. That is only negative shocks will impact the vote on the margin.

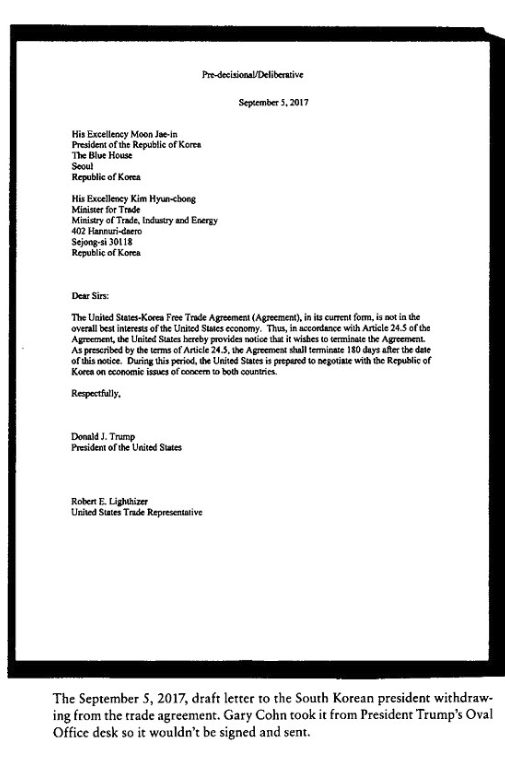

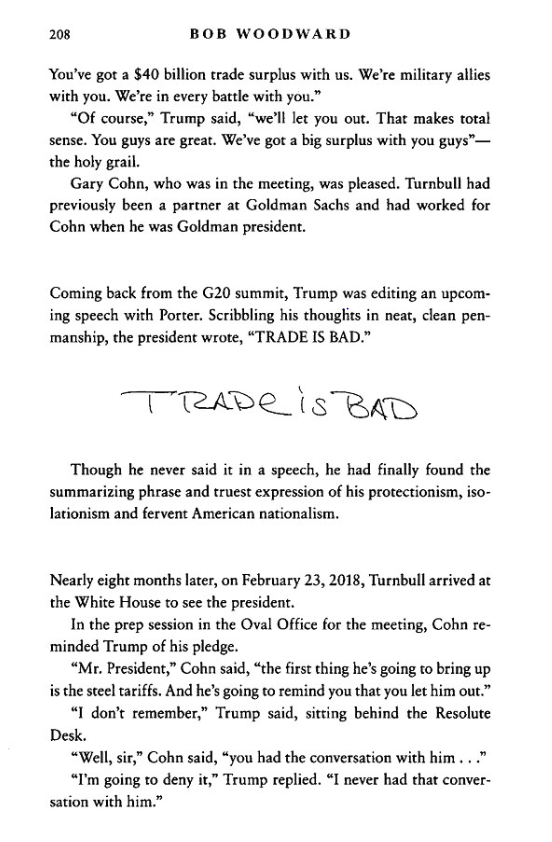

Yesterday’s NY Times guest Op/Ed confirmed our suspicions about President Trump,

Furthermore, we don’t believe President Trump is a free trader at heart but more of a protectionist and neo-mercantilist. There is no “Art of the Deal” – see his waffling on immigration – and no method to the administration ’s madness to negotiating anything, for that matter, but only driven by impulse and myopia. — Global Macro Monitor, June 24, 2018

Anyone who works with him knows he is not moored to any discernible first principles that guide his decision making….President Trump’s impulses are generally anti-trade and anti-democratic. – Anonymous, NY Times, September 5, 2018

Today it’s solidified,

The market has been in complete denial on this issue dismissing the trade war rhetoric as “Art of the Deal” nonsense. We suspect the market is in for a nasty reckoning when they have their epiphany. Stay tuned.

(updated Sept. 7, 2:22 eastern)

Source: Daily Mail

Beast Mode In September?

Can’t tell you how many recommendations we read at the end of August about how the S&P500 would continue its Beast Mode rally into September. After all that it was it does during midterm election years, no?

It may still yet but not so fast, comrades.

August And September Gains Rank High

We looked at the sum of the monthly gains for August and September and found that the 2018 performance ranked in the 84th percentile of late summer rallies over the past 70 years. How does the S&P perform in September after such gains?

What Now For September?

Glad you asked.

Realizing that the past is not always prologue, empirical probabilities suggest there is only a 36 percent probability of making money on the long side in S&P500 in September given such large gains registered during August and September.

The table above illustrates that only during 11 years since 1950 has the S&P outperformed this year’s return for July and August.

Interestingly, 45 percent of those annual observations were during midterm election years; significant given midterms only occur 25 percent of the time.

The average return for the 11 years was -0.1 percent with a median of -0.3 percent. Five of the 11 years took place during midterm election years, with only one election resulting in a change in Congressional leadership, the 1994 Clinton lambasting.

Moreover, we suspect the coming change in the leadership in the House of Representatives will not be as market-friendly as the 1994 Republican rout and capture of both houses of Congress.

Initial Conditions and Conditional Probabilities

It is important to go deeper when you hear forecasts based on simple extrapolations or analogs. Is it priced? What are current valuations relative to history?

Deep state, deep fakes, deeper analysis.

Facebook (Sheryl Sandberg) and Twitter (Jack Dorsey) on Capitol Hill today taking pipe from the pols. Large cap tech getting spanked with both stocks down meaningful.

I am all in for either they [Facebook] step up and take responsibility for what they have built, or they are the new Philip Morris. It’s an appropriate product for adults, but they have no business selling to children. – Raj Goel, CNBC September 5th

Yes, as we have said in the past,

Dopamine is the new nicotine, folks. – GMM, July 25th

The social media giants need to get serious and aggressively address the issues at hand, such as tech addiction (even Apple here) and dealing with the nefarious mind benders and influencers, or the government is going to drop the hammer and sickle. Regulation is coming, folks.

It’s here folks. Just as we said back in early July.

Not a political statement, just trying to model reality.

Recall, on the eve of the election we did predict Trump would win the electoral college and HRC the popular vote. The call wasn’t driven by our politics but by analysis.

Look for the wave to crest and break in early November when women and millennials, in general, come to the polls in droves to express their revulsion for President Trump. No level of the S&P or GDP growth will matter.

If feels like something big is coming.

The liberal insurgency inside the Democratic Party has claimed another victory, with Boston city councilor Ayanna Pressley defeating veteran Rep. Michael E. Capuano (D-Mass.) on Tuesday with a message of generational change. – Wash Post

We are witnessing the synthesis of a sort of Hegelian dialectic with the rise of Trump as the preceding antithesis. If you read our post from Monday, we did say,

This will truly be the year of women flexing their political clout. – GMM

“There will be no refunds!”

The data are moving against them.

Still, 63 days and 16 hours are an eternity in politics. Much can happen between now and then but we suspect it won’t be positive.

Moreover, the economy won’t save them. Ask President Clinton about that.

Given the current political climate, extremely low polling for the incumbent president, it does look like a 1994 rout is in store for the party in power. In 1994, the Democrats lost both the House and Senate as Newt’s “Contract with America” was ushered in with the Republicans capturing 54 congressional seats, eight Senate seats, and ten governorships.

The 1994 political rout took place in spite of a strengthening economy, which was beginning to accelerate — Q2 1994 GDP growth came in at 5.5 percent, with the three-quarter moving average GDP growth the highest in 10 years. The S&P500 was up around 2 percent going into September 1994. – GMM, Sept 2

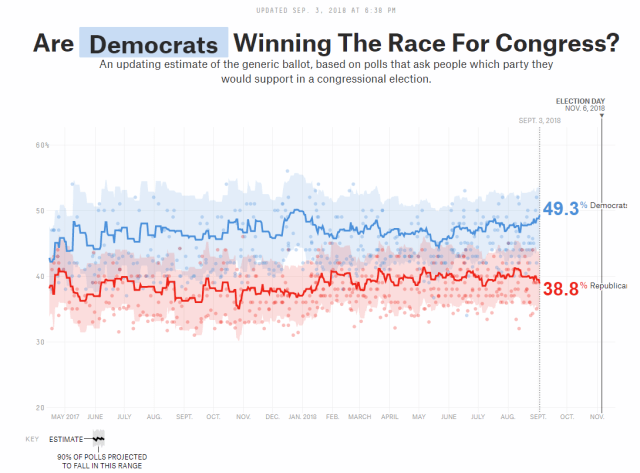

Flipping the Senate will be more difficult but a much higher probability than expected, in our opinion.

This will truly be the year of women flexing their political clout.

Not partisan or a political statement, just inferences from the polling data and our sense of the political climate.