“We are in the throes of a burgeoning financial bubble. If I had a choice between holding a U.S. Treasury bond or a hot burning coal in my hand, I would choose the coal.” – Paul Tudor Jones

(QOTD = Quote of the Day)

“We are in the throes of a burgeoning financial bubble. If I had a choice between holding a U.S. Treasury bond or a hot burning coal in my hand, I would choose the coal.” – Paul Tudor Jones

(QOTD = Quote of the Day)

Nice bounce.

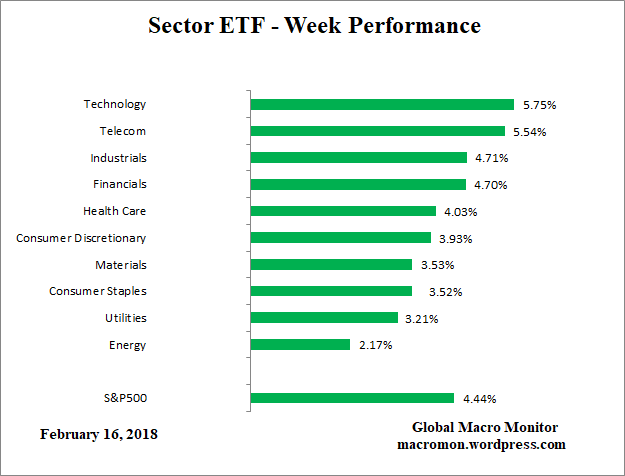

The S&P500 is up 7.88 percent off the low and has recovered 58.65 percent of its loss. It looks like the pivot is the .618 Fibonacci retracement level, which it traded through but could not hold as the market sold off into Friday’s close.

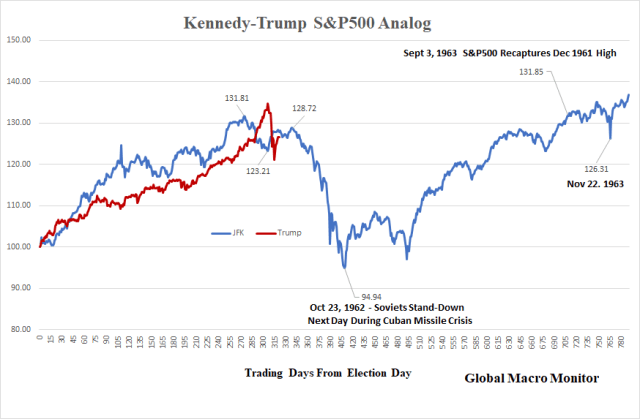

We are still following the Kennedy-Trump analog and won’t trash it until the S&P500 closes firmly above the 2,800 level.

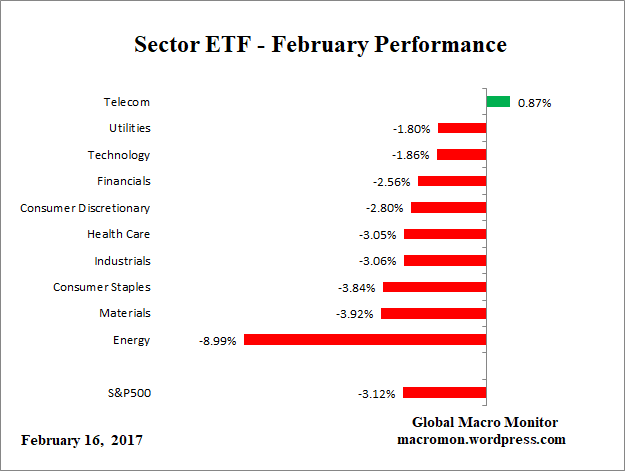

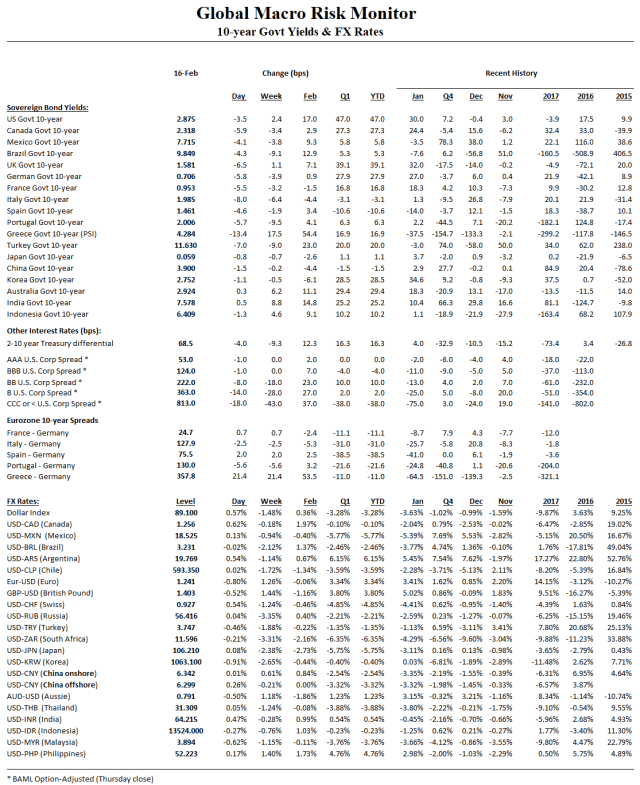

Interest rates seem to have stabilized and came back nicely in Germany, which provided some cover for equities to bounce. Credit spreads are wider in February.

The dollar continued on its weak path with the index making a new low on Friday before bouncing. Tread carefully if rates start moving higher and dollar lower.

Financial stress in the system is increasing, but note, the data is lagged by a week.

Copper and Zinc up big this week. Natural gas is, and will always be, the widow maker.

.

Efforts to reach a US immigration deal suffered a major setback as Senate failed to approve a bipartisan plan that would have granted legal status to unauthorised immigrants known as Dreamers

► Subscribe to FT.com here:http://bit.ly/2GakujT

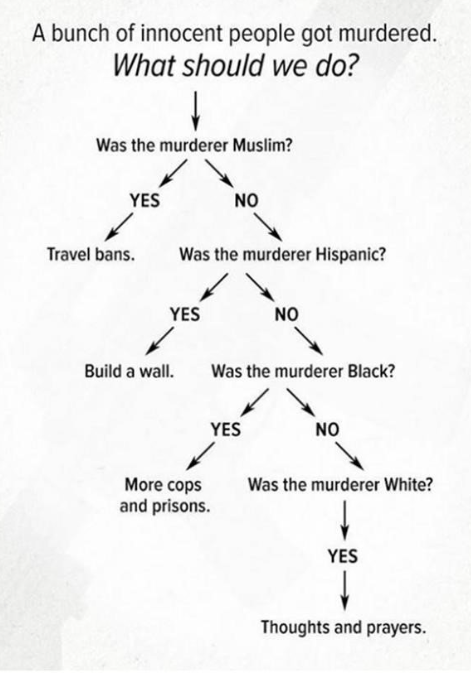

No political statement here but the following decision tree illustrates how algorithms can be biased. Note decision trees are a fundamental tool of artificial intelligence, algorithms and predictive analytics and their biases can destroy lives and even countries.

Hat Tip: @ianbremmer

Hat Tip: @ianbremmer

Algo Or Government Reaction Function

We hope the decision tree is not the algo or reaction function of the current U.S. government and the Congressional leadership, but to use Milton Friedman’s analogy of the pool player using but not understanding the laws of physics, they act as if it is.

To illustrate this, consider Milton Friedman’s famous exposition of the as if argument. He used the analogy of a snooker player who does not know the geometry of the shots they make but behaves in close approximation to how they would if they did make the appropriate calculations. We could, therefore, model the snooker player’s game by using such equations, even though this would not strictly describe the mechanics of the game. – Unlearning Economics

It is also one reason why we are bearish on the American Street and expect political and social instability to increase in the U.S. over the next few years. The politicos are stunningly tone deaf to the mood and needs of the vast majority of the American public. The “Swamp” is now at the elbow of exponential growth. Something is going to break.

We now fear the American Street more than the Arab Street.

Don’t Forget The Victims Of Florida School Shooting

Just look at the pictures and listen to stories of the kids and adults killed in the recent school shooting in Florida. Heartbreaking.

The reaction of the country, the victims’ families, and even the high school students that survived the shooting seems different this time.

Do you sense the rage building? Could this be the tipping point?

The Second Amendment

We are strict constructionists in reading the U.S. Constitution here at the Global Macro Monitor. Therefore we believe the second amendment allows for the right of every American to carry a Brown Bess, the most common musket used on both sides during the Revolutionary War, the timeframe when the Constitution was written. Nothing more.

Assault rifles, such as the AR-15? No f#*king way (NFW).

On The Side Of Reagan And Scalia

We side with both President Reagan and Justice Scalia on this one.

“I do not believe in taking away the right of the citizen for sporting, for hunting and so forth, or for home defense,” he said. “But I do believe that an AK-47, a machine gun, is not a sporting weapon or needed for defense of a home.” – President Reagan

“It may be objected that if weapons that are most useful in military service — M-16 rifles and the like — may be banned, then the Second Amendment right is completely detached from the prefatory clause. But as we have said, the conception of the militia at the time of the Second Amendment’s ratification was the body of all citizens capable of military service, who would bring the sorts of lawful weapons that they possessed at home to militia duty. It may well be true today that a militia, to be as effective as militias in the 18th century, would require sophisticated arms that are highly unusual in society at large. Indeed, it may be true that no amount of small arms could be useful against modern-day bombers and tanks. But the fact that modern developments have limited the degree of fit between the prefatory clause and the protected right cannot change our interpretation of the right.” – Justice Scalia

The time, though long past, has come.

Appendix

If you have time, make sure to watch this 12 minute video on the dangers of bias in algos and artificial intelligence. Well worth your time.

The first three of those words are attributed to the British Prime Minister, Benjamin Disraeli, and also sometimes associated with Mark Twain.

You know our skepticism of most government data, especially the BLS calculation of inflation in consumer goods and services. The data are so massaged by seasonal and hedonic adjustments, and even full-blown methodological revamps when the numbers do not fit the objectives of the government, they just don’t reflect reality.

Go back to 1982 when the BLS came up with the concept of “owner’s equivalent rent (OER),” a large component of how the price of shelter is calculated in the CPI. This was in response to the government believing rising housing prices were distorting the true cost of housing. Houses were then recategorized as capital goods. The data for OER are not hard, not real world data points that can be measured, such as egg prices.

A friend pointed out the following in today’s Wall Street Journal,

A monthly measure of what households pay for everything except gasoline and food rose a seasonally adjusted 0.349% in January—the strongest one-month increase since March 2005—driven by broad-based increases in costs like rent, clothing and medical services. – WSJ, February 15

We wonder out loud about the 0.349 percent print. Round it down, Charlie Brown!

Just another 0.001 percent and the BLS would have posted a core CPI monthly change of 0.4 instead of the 0.3 percent. The market response?

The headline number print of 0.5 percent was also very close to its rounding point. Going out three more decimals, the number was .5448 percent. Another 0.0012 percent, headline CPI prints at 0.6 percent.

Could they have?

Bureaucrats day trading (the data not securities) the monthly economic data? The word comes down from on high not to kill Goldilocks with RoundUp?

You decide.

File this one under all things rigged and don’t cry for me, Argentina!

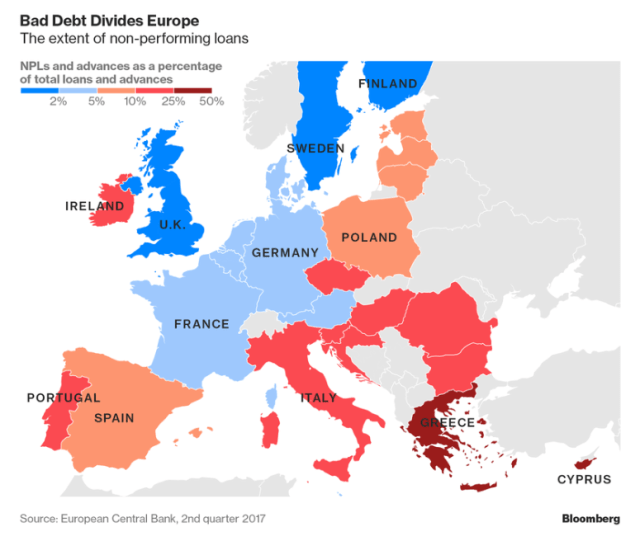

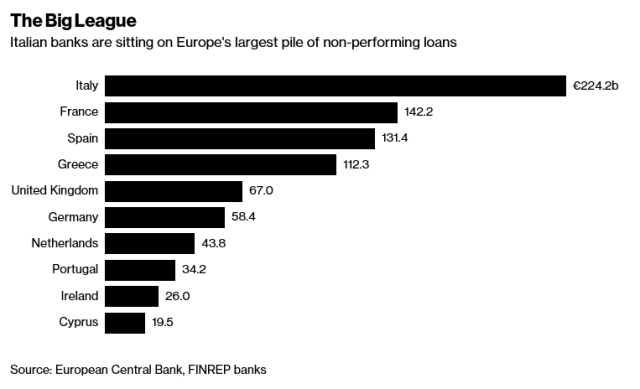

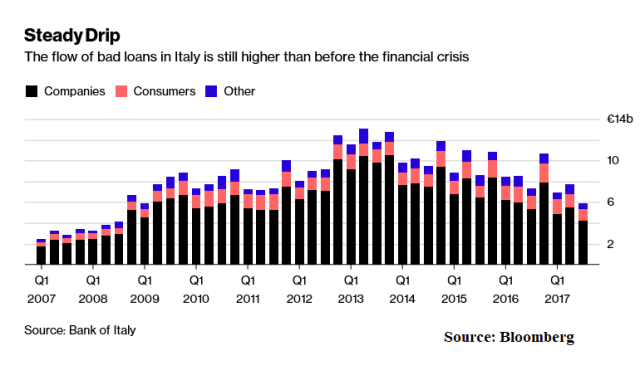

Looks like the new “Iron Curtain” in Europe is the non-performing loans (NPLs) in each country’s banking system. Greece and Italy stand out.

For European banks, it’s a headache that just won’t go away: the 944 billion euros ($1.17 trillion) of non-performing loans that’s weighing down their balance sheets.

Economists say the pile of past-due and delinquent debt makes it harder for banks to lend more money, hurting their earnings. European authorities are prodding lenders to sell or wind down non-performing credit, but they’re split on how to tackle the issue, and some investors are disappointed by the pace of progress. – Bloomberg

That was impressive.

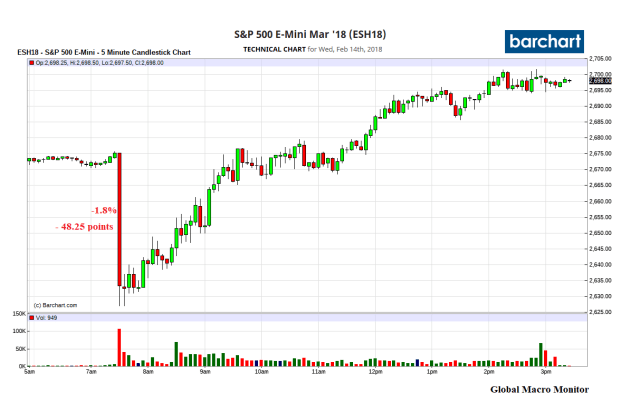

The hot CPI and weak retail sales data hits the tape at 8:30 eastern, S&P500 futures trade down 48.25 points or 1.8 percent in a Jackie Moon moment, bounces around for about 20 minutes, then takes off and trades up 2.8 percent from the low into the close. Even as the 10-year yield breaks and closes through the Maginot Line of 2.9 percent.

The cash S&P500 has now rallied 6.55 percent off its Friday low and recovered 48.78 percent of the high-to-low loss in this market move. A move through the 20-day moving average at around 2770 will force the bears and shorts to reconsider their market view.

Can’t believe we are sucked into commenting on short-term moves, which are noise and random at best, determined almost solely by how the fast money is positioned and leaning. But in the long-run there is always another short-run.

Nevertheless, today’s price action signals: 1) the market is “sold out” in the short-term; 2) there are few real sellers left in this leg, and 3) the fast money and machines were offside going into the CPI betting on an Armageddon number, which they kind of got but were not rewarded. Bond shorts faired much better.

The bullish and FOMO psychology hasn’t washed out yet and thus still makes us suspect the lows are not in. The market is still very expensive and you can throw out the widely touted “fairly valued” EPS, which are the result of financial engineering and stock buybacks.

We like the S&P500 Price to Sales ratio as a more objective valuation metric as even earnings can easily be manipulated and are creatures of corporate CFOs. We know that from our experience of working in a large money center bank.

Moreover, the dollar continues to weaken, when fundamentals favors strength, which is a major concern. Especially as interest rates rise.

Something is rotten and driving the capital flight.

Today was impressive, however. Chalk another one up for the bulls.

Next Levels

Today’s high on the cash S&P500 was 2702.1, just a little more than 50 bps below 2702.78, the 50 percent retracement and key Fibonacci level. The next level is 2726.67, last Wednesday’s high before the swan dive to 2532.69 on Friday morning.

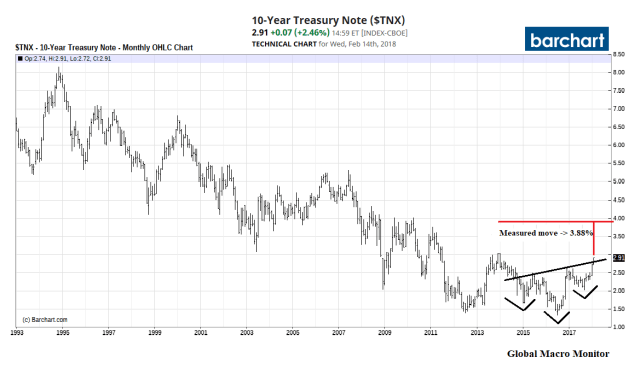

Where Are 10-Year Yields Headed?

Nobody knows and because of that uncertainty, we look to gurus or technical analysis to comfort us and ease the anxiety of not knowing the future.

We do know the long-term downtrend on yields has been broken and looking at the chart, a reverse head-and-shoulders bottom has formed. The neckline has been broken and a measured move will take the 10-year to around 4 percent.

Makes sense to us, fundamentally, as real interest rates are set to rise due to the supply and demand dynamics in the U.S. bond market and inflation is increasing. A two to three percent real rate plus inflation has always been a running assumption for the long-term equilibrium interest rate all throughout our research career.

Technical Analysis

Technical analysis is imperfect but a tool, and one way to light the uncertain and a foggy-lit path of future prices. We are not religious zealots and only half way sold on the utility of technical analysis but just throwing it out there for you.

We infer from the price action and lots of losses of the past several years that the machines use technical analysis to set bear and bull traps. It has rarely paid to place a bet when a key technical level breaks as the algos are programmed to generate a giant reversal and squeeze when they calculate and estimate the net position of traders is leaning the wrong way.

Whatever your view, however, three percent is the next big number for the 10-year note yield.

By the way, remind us not to comment on short-term market moves.

Wow, the robots are even coming for the political scientists.

Researchers used artificial intelligence to compare the manifestos of the German parties with the coalition agreement. And it showed that 70 percent of the content referred to the SPD manifesto and only 30 percent to that of the conservatives…

READ MORE: http://www.euronews.com/2018/02/13/german-coalition-agreement-ai-program-shows-bias