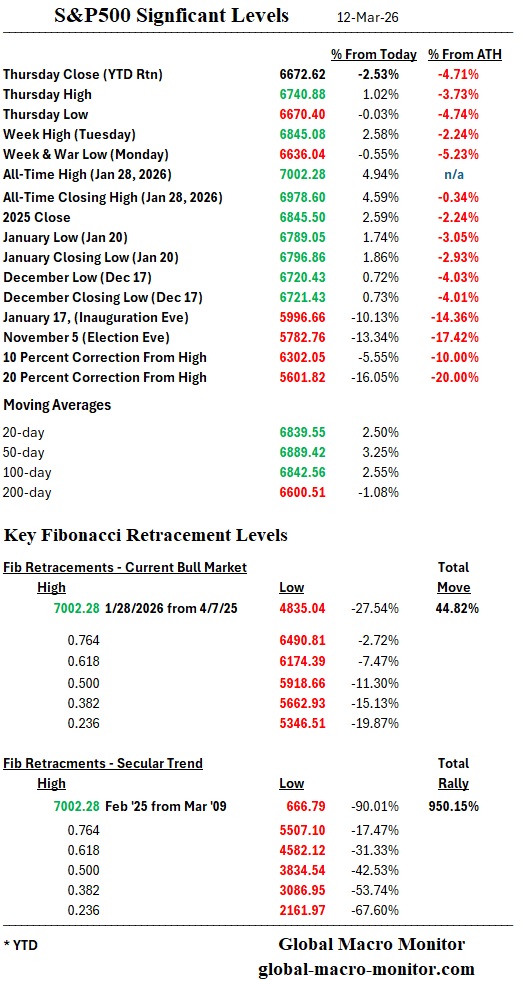

As we approach the Ides of March, the S&P 500 is performing a high-wire act that should give even the most seasoned bull a case of vertigo. Currently sitting at 6,672, the index is a mere 4.7% below its recent all-time high of nearly 7,002. On the surface, the resilience is remarkable. Beneath the hood, however, the engine is smoking, the tires are bald, and the road ahead is washed out.

The disconnect between headline price action and the escalating “polycrisis,” from a hot war in the Middle East and $100 per bbl crude oil to the brewing private equity crisis, suggests that the market isn’t climbing a wall of worry; it’s ignoring the floor falling out from under it.

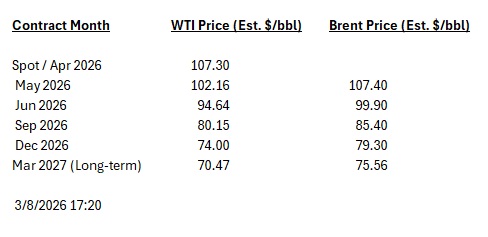

The Oil Shock: A 50% Surge into the Inflationary Fire

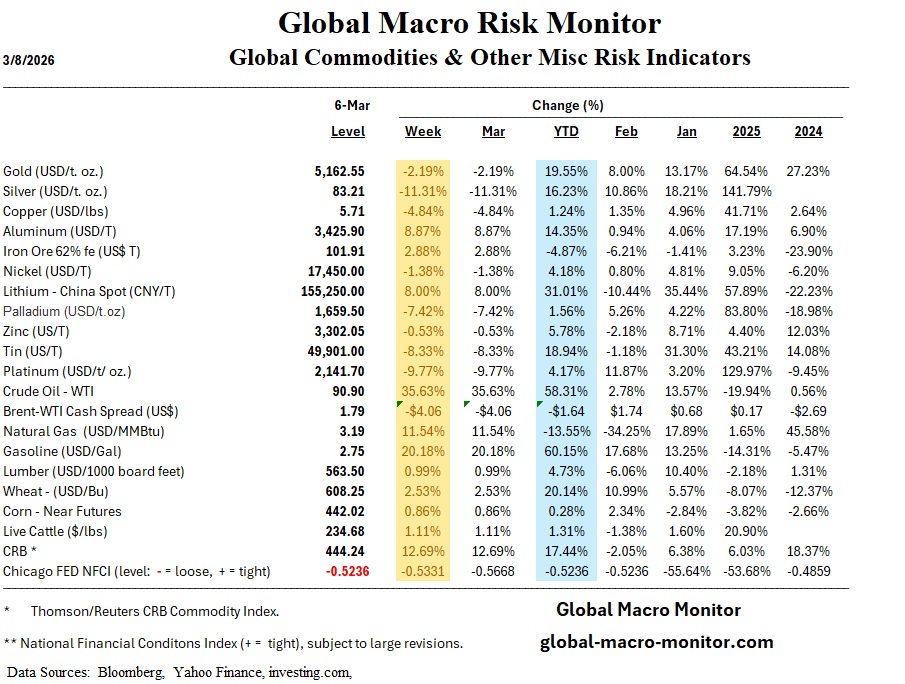

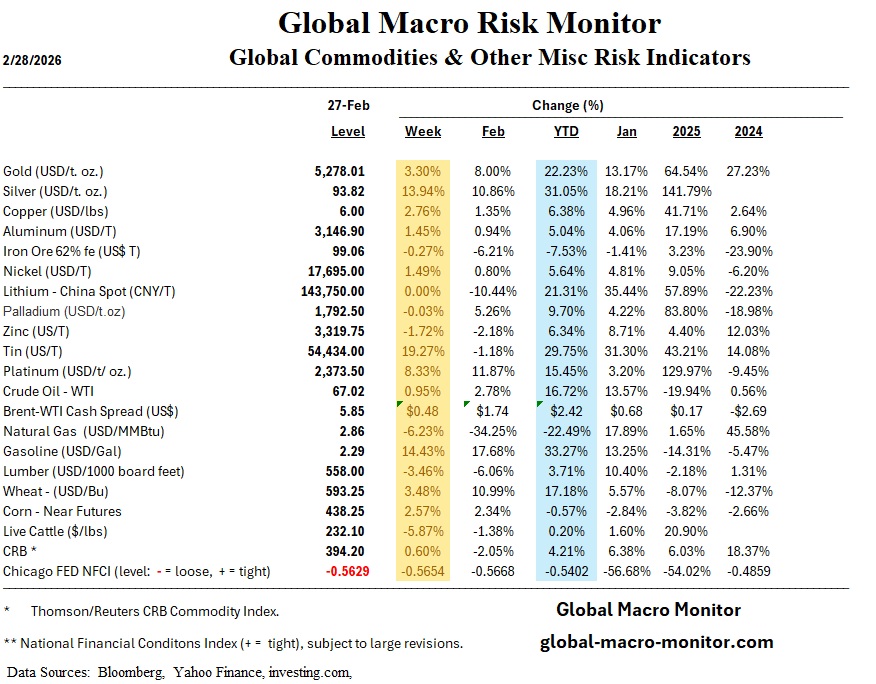

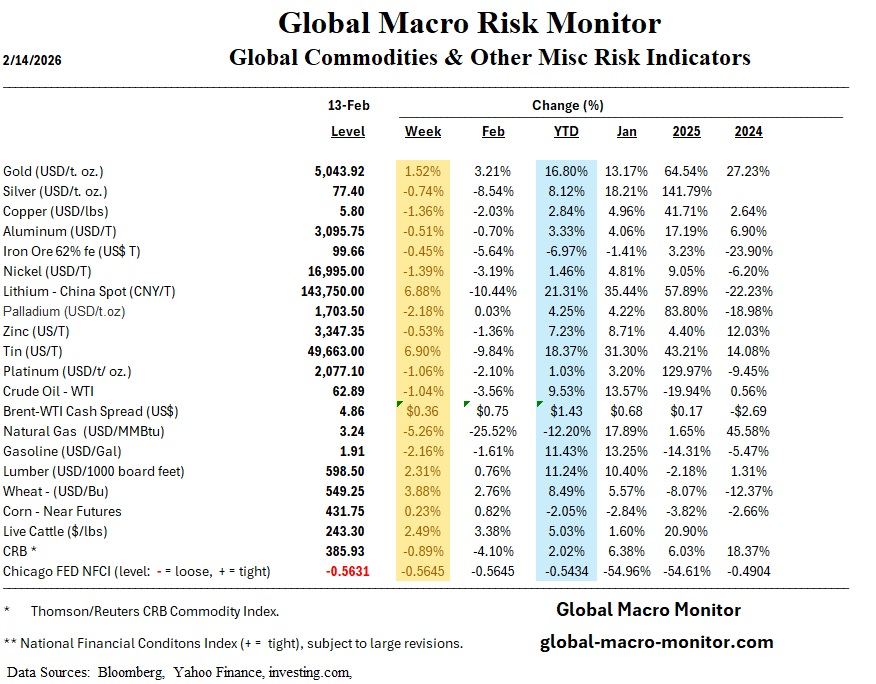

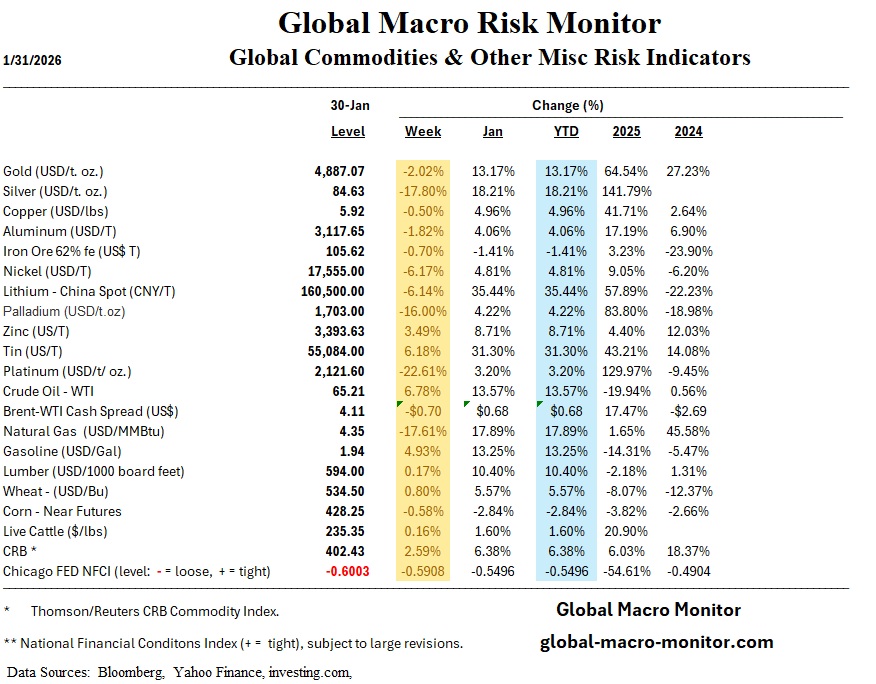

The most immediate threat to the global “soft landing” narrative is the black gold currently fueling a regional conflagration. Since the onset of the war with Iran earlier this year, crude oil prices have surged nearly 50%, with Brent crude breaching the $115 per barrel mark.

For the American consumer, the impact is visceral. We aren’t just talking about $4.50 at the pump; we are talking about a systemic jolt to the logistics and agricultural sectors.

- Logistics Lag: Diesel prices have jumped 28% since the start of the conflict, directly raising the cost of every item delivered by a truck or ship.

- The Strait Crisis: With the Strait of Hormuz effectively a contested zone, 20% of global oil and LNG supply is under threat.

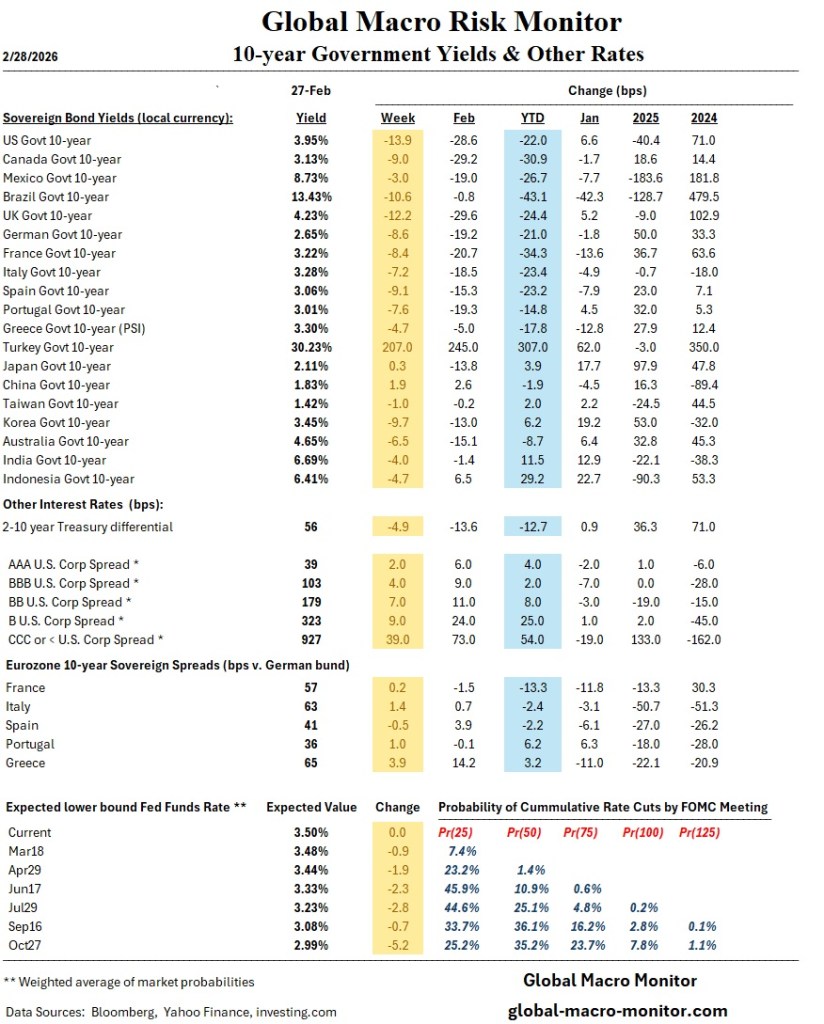

This isn’t just “transitory” noise. This is a supply-side shock that effectively acts as a global tax on growth while simultaneously pinning the Federal Reserve into a corner. If the Fed cannot cut rates because oil is driving a 3.7%–4.0% inflation spike, the “safety net” for equities effectively vanishes.

Private Equity and the AI Existential Threat

While the energy markets burn, the “smart money” in private equity (PE) is starting to sweat. Recent weeks have seen emerging cracks in the private credit sector, with high-profile funds reportedly gating or restricting withdrawals. This liquidity squeeze is the first sign that the high-rate environment is finally breaking the back for private credit. We can’t help but be reminded of the collapse of the Bear Sterns hedge funds in 2007, which were a precursor to the Great Financial Crisis.

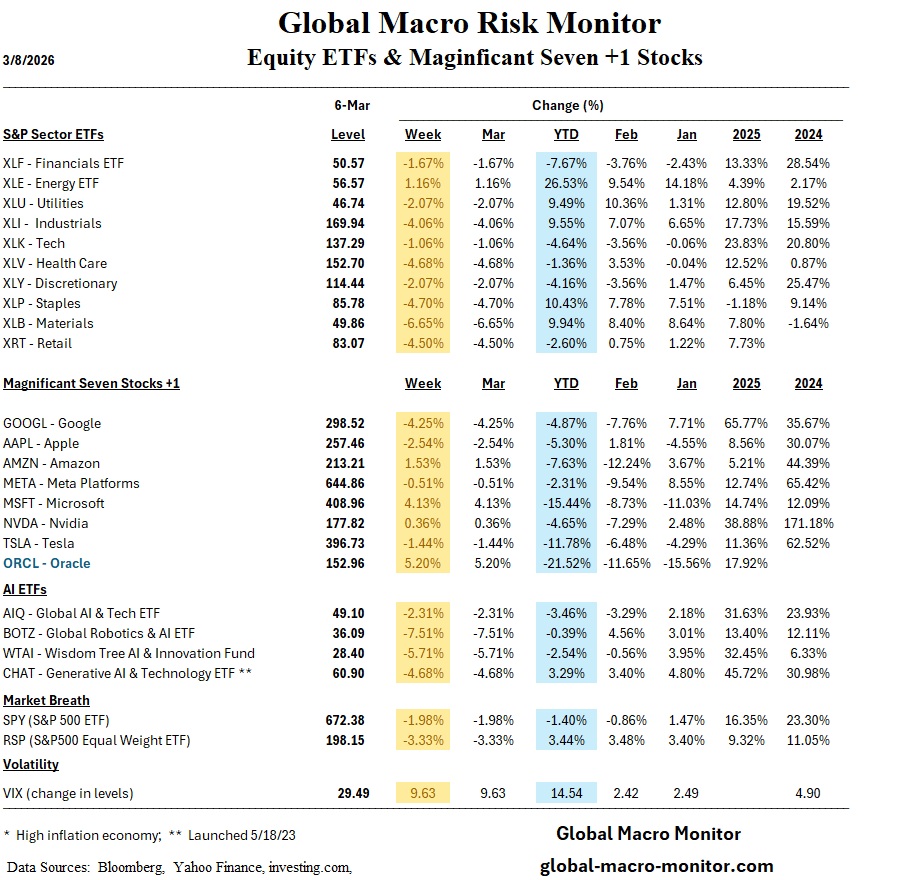

Compounding this is the shift in the AI narrative. In 2024 and 2025, AI was the ultimate “hopium” drug. Today, the discourse has turned a little dark. It does feel, at least to us, the markets are in a transition from AI euphoria to existential anxiety.

The market is no longer pricing in just the efficiency gains of AI; it is beginning to price in the displacement of white-collar labor and the potential for a “hollowed-out” economy.

Major tech platforms that led the charge last year are now being sold off as investors realize that AI agents might not just help these companies, they might replace their entire business models.

Positioning vs. Logic: The 2026 Reality

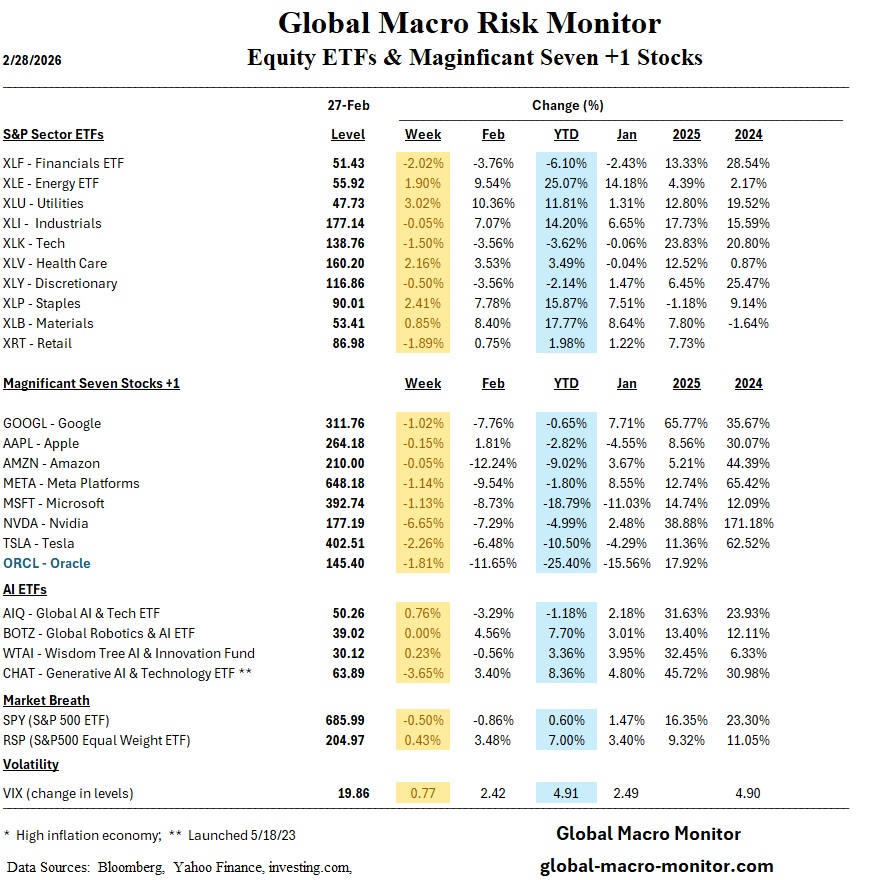

The February 27 Global Risk Monitor offered a sobering reminder that remains the definitive guide for our current moment:

“Markets do not trade in the short-term on logic; they trade on positioning, leverage, and emotion, often in that order.”

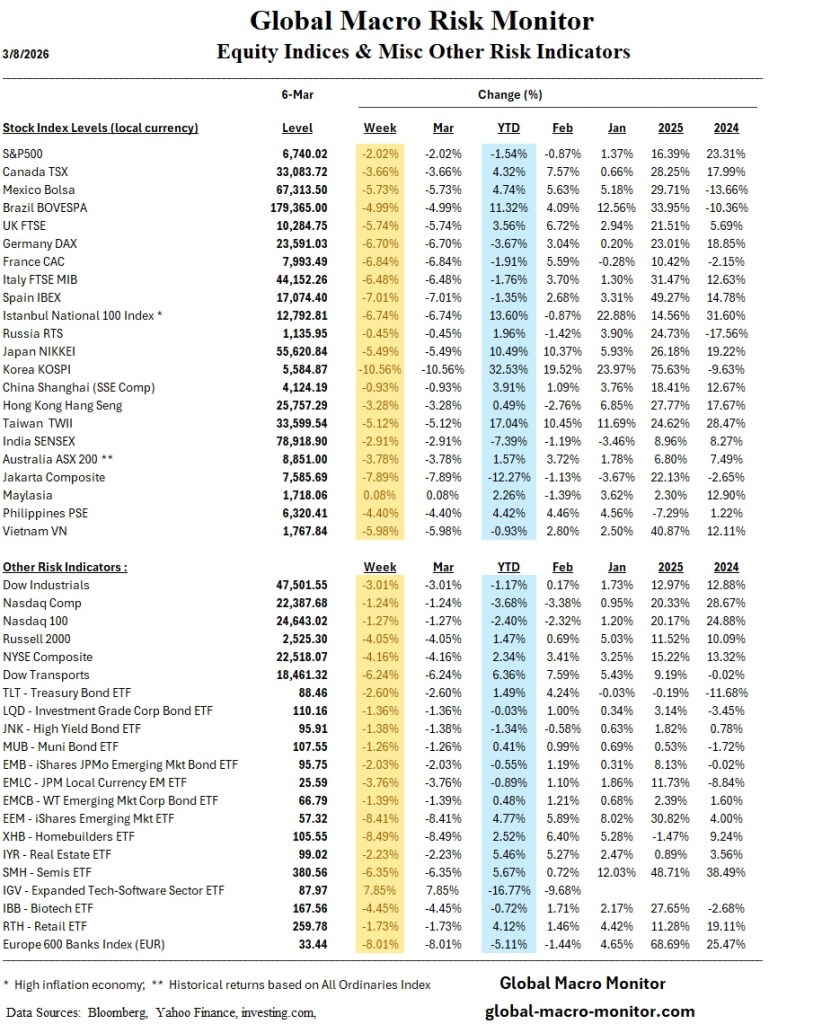

The U.S. market is trading “short,” not necessarily in terms of net-short positions, but in terms of conviction. We have seen a massive rotation out of the “Magnificent Seven” and into “boomer rocks” (gold) and defensive sectors like Utilities and Energy.

This is the hallmark of a market where the leverage is being unwound. When the logic (earnings growth, geopolitical stability) fails, the positioning (forced selling, margin calls) takes over. This morning’s “Three Black Crows” candlestick pattern on the hourly S&P futures chart suggests that every attempt to rally is being used as an exit door by institutional players.

The Path to 6600 (and Beyond)

Technical analysis is often dismissed until it becomes a self-fulfilling prophecy. My conviction remains high: a decline to the S&P 500’s 200-day moving average is not just a possibility; it is an inevitability.

The 200-DMA currently sits near 6,600, just a flubbled chip shot away. Historically, this level acts as the “line in the sand” between a healthy correction and a cyclical bear market.

- The Breach: If we break 6,600, we lose the structural bull-market support that has held since early 2024.

- The Target: A weekly close below this floor opens the trapdoor to the 6,100–6,200 range, a level last seen during the volatility of mid-2025.

The current market sentiment is fragile. With volatility indices (VIX) creeping back toward a 30 handle, there are no “downside shock absorbers” left.

Stay Frosty

The convergence of a 50% oil spike, a private equity liquidity crunch, and a fundamental reassessment of AI’s economic value has created a “perfect storm,” in our opinion. While the S&P 500 sits not that far off its highs, the foundation is crumbling.

The mantra for the coming quarter is simple: Stay frosty. Capital preservation should take precedence over chasing the “next leg up.” The market is telling us that the rules of engagement have changed; it’s time we start listening.

Today’s market also serves as a visceral reminder of Upton Sinclair’s famous warning:

‘It is difficult to get a man to understand something, when his salary depends on his not understanding it.’

As the financial media downplays the risks in oil and private credit, remember that their business model thrives on optimism, such as claiming the war and the energy spike are merely ‘transitory.’ We’ve heard that word before, and we know how that story ends. Don’t let their incentives cloud your judgment; the data are speaking a much different message.

As always, we reserve the right to be wrong, and often are, but the signals suggest it’s time to sit up straight and pay attention.

Stay frosty, folks.