Global markets staged an impressive rebound this week, fueled by growing optimism that trade tensions between the United States and China may soon ease and that some bilateral trade deals are imminent. Investors eagerly latched onto comments from U.S. Treasury Secretary Scott Bessent and President Trump suggesting that tariff levels were unsustainable and that some dialogue, formal or informal, might be underway. This generated a powerful relief rally, with the S&P 500 and Nasdaq surging approximately 4.6 percent and 6.7 percent, respectively. However, despite the ebullient market response, no formal negotiations or agreements have been reached, and the underlying political dynamics remain deeply adversarial.

Hope v Reality

The reality is that while hopes of de-escalation buoy markets, the U.S.-China standoff is mired in political ego. President Trump appears reluctant to make the first move toward a deal, wary of appearing weak ahead of the 2026 elections. Conversely, President Xi Jinping, emboldened by China’s relative economic stabilization and newly announced stimulus plans, is taking a patient, strategic approach. With no official meetings scheduled, the current atmosphere reflects more wishful thinking than tangible progress.

Therein lies the core risk: investors may be underestimating the political barriers to resolution. Trump’s current position is precarious. Without a trade breakthrough, the U.S. could soon face visible consequences—empty store shelves, rising consumer prices, and a dent in consumer confidence—as tariff impacts cascade through supply chains beginning next month. If economic pain intensifies, Trump may be forced into a humiliating climbdown to avoid severe electoral damage.

Bulls Back In Charge

Nevertheless, the S&P500 bulls captured a key level on Friday, the .5 Fibonacci retracement at 5491, putting the bulls in charge for now. Shorts are foolish to fight this market, especially knowing it is very likely that some large traders/investors have access to material non-public information and are trading on it, which is an absolute f$%king disgrace.

Watch Your Time Horizons

We believe that medium to long-term optimism may be mispriced. There is a prevailing belief that resolving trade tensions would automatically unlock a fresh wave of global growth. Yet this is misleading. Even if tariffs were significantly reduced from current levels, the global economy will still face the structural headwind that tariffs will be much higher than they were at the beginning of the year, reducing world trade and therefore global growth.

Imagine, for example, if Macy’s doubled its prices, then announced a 25% off weekend sale. Are customers really better off than before the price hikes? Of course not. Yet that’s exactly how the market seems to be reacting to the latest headlines. Sure, 25% off sounds better than a 100% increase—but seriously, Mr. Market? Tariffs will remain much higher than they were before this entire mess began.

Moreover, the uncertainty generated by the tariff wars has already inflicted lasting damage on investment confidence. The idea that a quick deal would fully reverse these scars is naïve.

A Zero Tariff Deal?

One significant development this week was the soft proposal, or more like an idea thrown out by German Finance Minister Jörg Kukies, for a comprehensive zero-tariff agreement between the U.S. and Europe. Kukies eloquently argued, “The easiest way to ensure balance and fairness is for everyone to go to zero. Then we have free trade, efficiency, and economies of scale. We can think about standardization, mutual market access, and many other things”.

From a pure economic perspective, this is sound logic. True free trade would enhance productivity, lower costs, and strengthen growth on both sides of the Atlantic.

However, President Trump does not align with free trade orthodoxy. His administration’s goal is not greater global economic efficiency; it is to reshore manufacturing and generate tariff revenues to finance prior tax cuts. These objectives fundamentally conflict with a zero-tariff deal. Accepting such an agreement would dismantle the entire strategic rationale, if there is one at all, behind the tariff regime. Thus, despite Germany’s overtures, it is highly unlikely that Trump would agree to zero tariffs—unless political and economic pressures render his position untenable.

Looking ahead, while the recent rally in equities has been impressive, there are clear limits to upside potential unless there is a definitive resolution on trade. The markets are functioning on hope rather than substance. Earnings risks are rising, though Q1 is shaping up to be better than expected, economic indicators are softening, and monetary policymakers, including the Fed and ECB, are increasingly hamstrung by uncertainty.

If trade tensions linger—and especially if tariffs continue to feed into inflation and constrain growth—the global economy could be pushed into a downturn in the coming quarters. The durability of the current market rally is, therefore, suspect. As real economic impacts begin to materialize, the cheerful narrative driving markets today may give way to renewed volatility and risk aversion.

Summary

While the past week brought a welcome reprieve to markets and may continue, the fundamental dynamics have not changed. The U.S.-China standoff remains unresolved, driven as much by political pride as economic strategy. The German proposal for a zero-tariff regime, while admirable, is almost certainly dead on arrival in Washington. Thus, caution remains warranted. Investors should not be lulled into complacency by superficial signs of progress; instead, they must prepare for the possibility that the real economic fallout of tariff escalation is only just beginning.

Markets

U.S. Market Analysis

Markets Rebound Sharply:

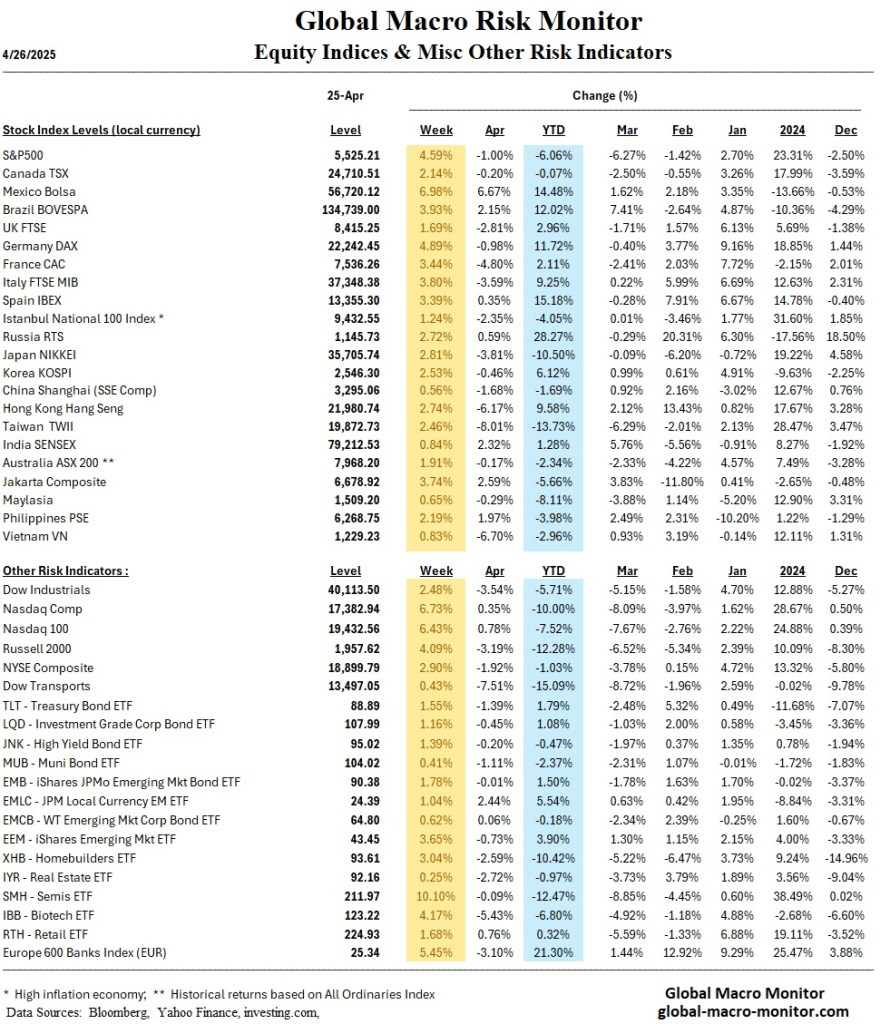

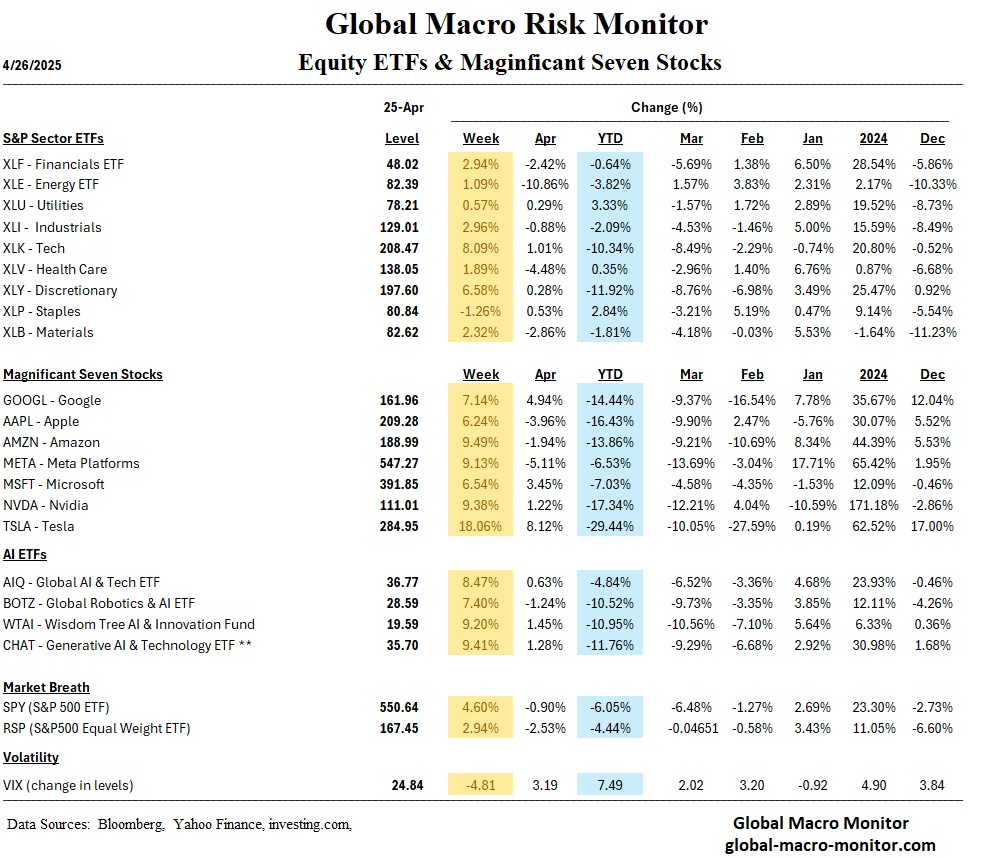

U.S. equities posted their strongest week since late 2023, buoyed by optimism over potential de-escalation in U.S.-China trade tensions. The S&P 500 rose 4.6%, the Nasdaq surged 6.7%, and the Dow gained 2.5%.

Small-Caps Lead Gains:

The Russell 2000 rose 4.1%, outpacing large caps for the second consecutive week, helped by strong tech earnings and expectations of a more dovish Fed.

Market Breadth Improves:

Participation broadened across sectors. The percentage of S&P 500 stocks above their 200-day moving average rose to 34.2%, up from 29.4%.

Bond Yields Ease:

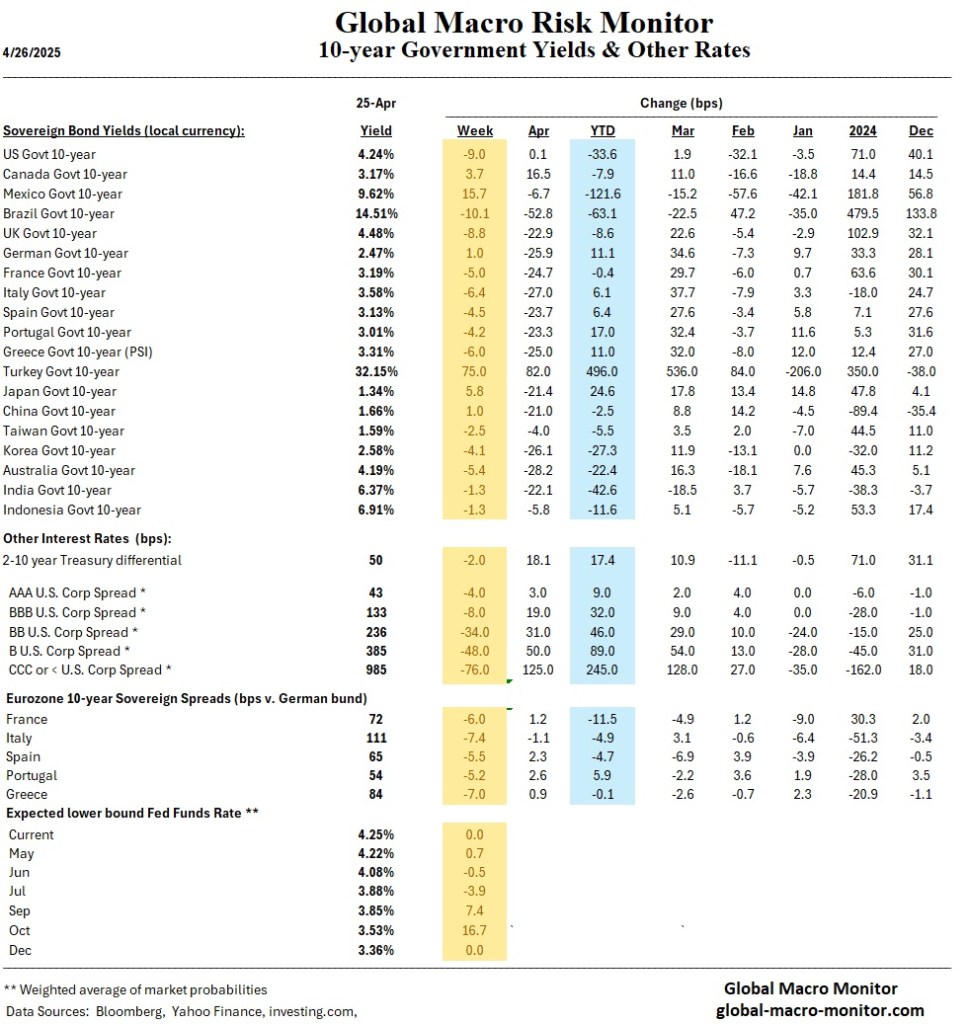

10-year Treasury yields fell 8 bps to 4.24% as safe-haven demand moderated and growth concerns lingered.

Bitcoin Rally Continues:

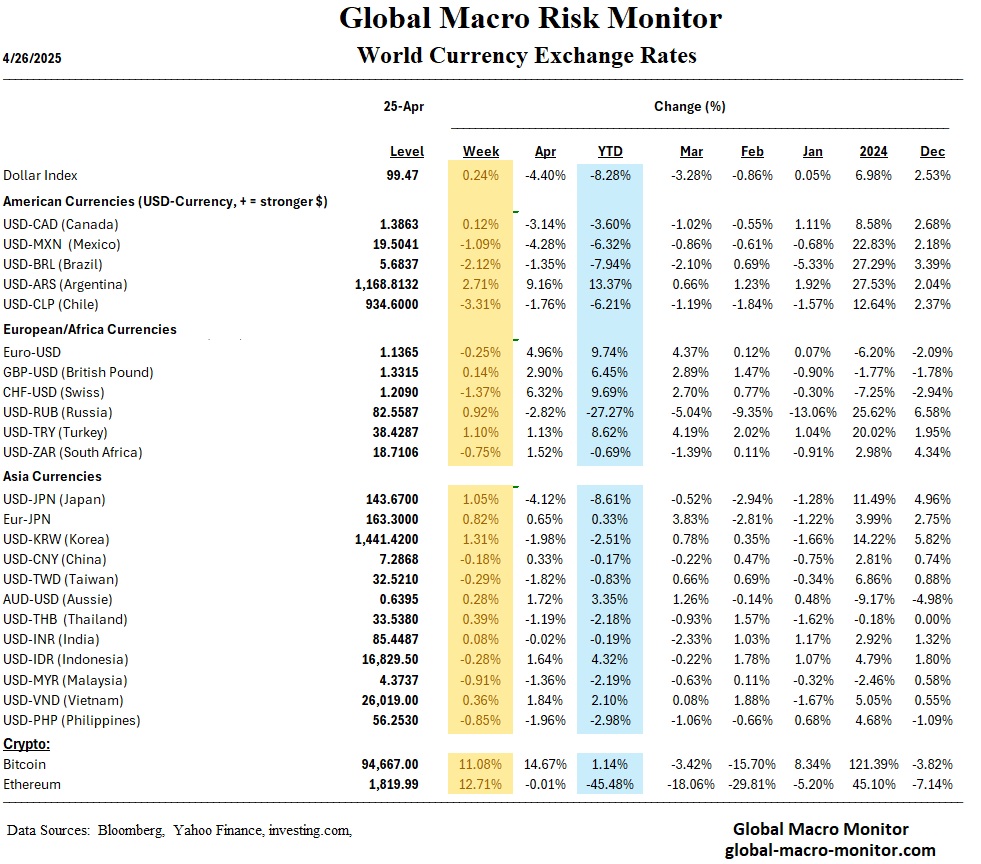

Bitcoin surged over 11%, rebounding toward the $100K mark, supported by optimism around broader risk appetite.

Credit Spreads Tighten:

Investment-grade credit spreads narrowed slightly, indicating improved investor risk sentiment amid hopes of trade stabilization.

Global Market Analysis

Europe:

STOXX Europe 600 gained 2.77%, led by Germany’s DAX (+4.89%) and France’s CAC 40 (+3.44%), following Trump’s softer tone on tariffs and improving earnings sentiment.

Asia:

- Japan:

Nikkei 225 advanced 2.8%. BoJ policymakers hinted at maintaining easy monetary policy amid tariff uncertainty. - China:

Shanghai Composite rose 0.56% as stimulus expectations bolstered sentiment despite continuing trade tensions.

Emerging Markets:

- Emerging Asia:

GDP downgrades for Singapore, Malaysia, and Korea weighed on sentiment, but policy stimulus measures are expected to cushion the slowdown. - Latin America:

Held up relatively well as supportive domestic factors offset external headwinds. - EEMEA:

Caution prevails amid capital flow risks, but no immediate crises are detected.

Economics

U.S. Economic Overview

Positive Earnings, But Slower Growth:

73% of reporting S&P 500 companies beat earnings expectations. However, S&P Global PMI data showed business activity slowing to a 16-month low, especially in services.

Tariff Inflation Risks Reemerge:

Prices charged for goods and services rose at the fastest pace in over a year, largely due to tariffs.

Consumer Sentiment Weakens:

University of Michigan’s Consumer Sentiment Index fell for the fourth consecutive month, highlighting persistent uncertainty around trade policy.

Fed Outlook Steady:

Markets maintain expectations for two Fed rate cuts in 2025. Longer-term rates fell this week amid rising concerns about Q2 growth.

Housing Market Softens:

Existing home sales plunged 5.9% in March to the lowest March level since 2009, weighed down by high mortgage rates.

Global Economic Overview

Eurozone:

Growth outlook dimmed as April PMI data pointed to weakening services and manufacturing. German GDP forecasts downgraded to zero growth for 2025.

China:

Despite better-than-expected Q1 GDP, new tariffs threaten future exports. Beijing’s Politburo announced preparations for emergency stimulus measures.

Japan:

Tokyo CPI inflation rose faster than expected, bolstering the case for a BoJ rate hike later this year, but tariff risks complicate the timeline.

Australia & Colombia:

Central banks kept rates steady; rate cuts still expected as global risks intensify.

India:

RBI expected to cut rates by 25 bps following softening inflation and weaker growth.

Mexico & Norway:

Key inflation data due next week will likely dictate the timing for further easing.

Week Ahead (April 28–May 2, 2025)

Key U.S. Events:

Economic Data:

- Tue (Apr 29): Advanced International Trade, Consumer Confidence

- Wed (Apr 30): ADP Jobs Report, Q1 GDP, Pending Home Sales

- Thu (May 1): ISM Manufacturing Index, Jobless Claims

- Fri (May 2): Nonfarm Payrolls, Unemployment Rate

Earnings:

- Mega-Cap Tech Reports: Microsoft, Meta (Wed); Apple, Amazon (Thu)

Key Global Events:

- China PMIs: Wednesday—will gauge early tariff impact.

- Eurozone GDP & CPI: Wednesday—critical for ECB policy outlook.

- Bank of Japan Meeting: Thursday—no change expected, but tariff commentary crucial.

- Tariff Developments: Any new trade announcements could cause sharp market moves.