The Mooch says Republican Senators “hate Trump’s guts” and will turn on him.

Watch this space. It’s been in rampopotamus mode over the past week.

The Mooch says Republican Senators “hate Trump’s guts” and will turn on him.

Watch this space. It’s been in rampopotamus mode over the past week.

Reposting a piece from a few years back to provide some market perspective on today’s news. There are a confluence of events, not just political instability, of why we believe stocks are headed lower, including valuations and the shifting of geopolitical and economic tectonic plates.

We’ve analyzed the behavior of the S&P500 during the Watergate impeachment hearings and the Clinton impeachment. If you’re shorting risk markets solely based on speculation that President Trump may be impeached, maybe you should think again.

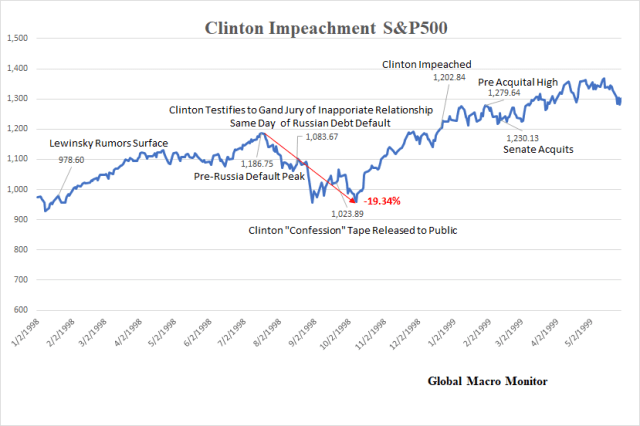

Let’s first look at the Clinton impeachment S&P500. The market never seemed to take the Clinton impeachment seriously and was never a threat to the stock market.

Then we’ll analyze the more complicated Watergate scandal, which many consider the main culprit of the 1973/74 bear market, a 50 percent decline in S&P500 from January 11, 1973 to October 3, 1974.

Finally, we will take a look at Trumpgate and introduce you to our newest political Six Sigma political thriller.

Clinton Impeachment

The rumors of the Clinton-Lewinsky affair broke January 19, 1998, on the Drudge Report, which was a market holiday. Recall U.S. stocks were in a rip-roaring bull market and massive bubble that saw the Dow rise 253 percent during the Clinton administration, second only to Calvin Coolidge’s roaring twenties bull market (see here for Presidential Stock Returns). The NASDAQ, home of the infamous dot.coms, rose a multiple of the Dow.

The table below shows the timeline of various key events and the S&P500 returns.

Even after the news broke and the “blood was in the water” — recall the media frenzy, probably crazier than now because it involved sex — U.S. stocks continued to march higher. The S&P500 rose another 21.27 percent until its peak pre-Russia debt default high of 1,186.75 on July 17th.

Summer of 1998 – Russian Debt Default

Ironically, Russia announced its debt default the same day President Clinton testified to the grand jury he had an “inappropriate relationship” with Ms. Lewinsky on August 17th. The global markets fell apart and what was a garden variety correction in the S&P500 sharply accelerated.

The Brazian stock market fell 16 percent on September 10th. The Fed was forced to cut interest rates several times in just 7 weeks. Systemic risk was rising rapidly as Long-Term Capital Management (LTCM) ultimately failed and was bailed out by a consortium of financial institutions in late September.

The total decline in S&P500 during this period was 19.34 percent finally bottoming on August 31, many months before the global economic crisis ended.

Was the financial crisis of 1998 the result of the fear of Clinton being impeached? Hardly, or should we be blunter – NFW!

Remember, the U.S. had the “Committee to Save the World.”

The 1998 financial crisis was mainly the result of Russia’s debt default and the subsequent huge global margin call. Hedge funds were big in Russian debt that had defaulted forcing them to sell many of their assets, say, even their Safeway bonds. As credit spreads significantly widened in almost every credit instrument, the extremely levered LTCM with all its Nobel laureates tanked.

Even if you believe the march toward impeachment was a contributing factor in the ’98 financial crisis, it wasn’t, or it needed a sufficient condition, and was not even a necessary condition, in our opinion. We will admit there is a possibility the Clinton administration was distracted by the scandal and may not have allowed or wanted Russia to default.

We lost a lot of money betting Russia was “too nuclear to fail” even as we were in the euro bonds the Russians continued to pay. At one point, these bonds with 9 plus percent coupons fell into the teens with current yields of over 60 percent. There were no buyers in sight. If only we held on, but couldn’t as we were too levered.

Later, we will make the argument that Watergate may have been the necessary condition of the 1973/74 bear market, but the OPEC embargo was the sufficient condition.

Impeachment and Acquittal

By the time President Clinton was impeached in the House of Representatives on December 19th, the S&P500 was up 23 percent since the Lewinsky rumors first surfaced. The Senate acquitted President Clinton on February 12, 1999, and with S&P500 up 26 percent since the start of the scandal, “the long national nightmare” of the bankrupt impeachment short sellers was over.

The S&P500 continued higher for another year, finally bursting on March 24, 2000, up 56 percent from the day of discovery of the Clinton-Lewinsky affair.

What we did learn in 1998 was that stock market bubbles don’t pop easily. That is until they do.

Watergate Scandal

The analysis of Watergate on the stock market is a little more difficult to unpack as it involved the conflation of three major “rock your world” events:

1) A nasty bear market that took the S&P500 down almost 50 percent from January 1973 to October 1974;

2) A potential constitutional crisis (never the case during the Clinton impeachment) as it was uncertain if the White House would turn over “the tapes“. President Nixon fired the Special Prosecutor who was charged to oversee the federal criminal investigation in Watergate;

3) And we think, most important, was the first OPEC oil embargo that shook the global economy on October 16, 1973

The break-in of the Democratic National Committee headquarters in the Watergate apartment complex took place in the summer of 1972. It took several months before it hit the front pages as national news and became a Presidential scandal. Bob Woodward and Carl Bernstein, now household names, were urban beat reporters rendered to the back pages of the Washington Post when they were assigned to the Watergate story.

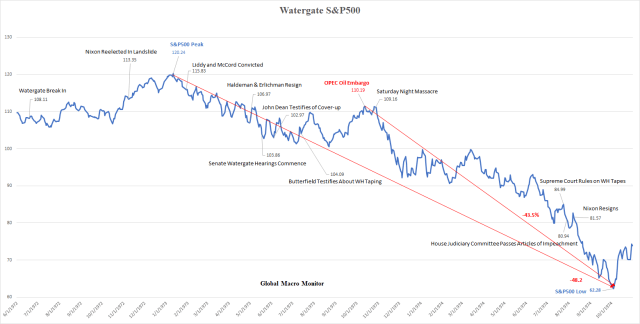

The S&P500 was in rally mode going into the 1972 landslide reelection of Richard Nixon. The index peaked on January 11, 1973, at 120.24 and would not regain that level until more than 7 years later. From the day of the Watergate break-in until the January peak, the S&P500 rose 11.22 percent.

Liddy and McCord Convictions

On January 30, 1973, two members of President Nixon’s re-election committee were convicted for the Watergate break-in.

“…two former officials of President Nixon’s re-election committee, G. Gordon Liddy and James W. McCord, Jr. were convicted yesterday of conspiracy, burglary and bugging the Democratic Party’s Watergate headquarters.”

– Washington Post, January 31, 1973

Game on, Watergate.

Short-term Bottom

The S&P500 continued to decline through the summer until making a short-term low on August 22nd at 100.53, down 16 percent from the January high. It then rallied 11 percent for two months peaking on October 26th.

At this point, the S&P500 was only down 7.4 percent even after the John Dean testimony to Congress and the Saturday Night Massacre and the OPEC oil embargo, of which both occurred just a week before. Similarly ironic, the OPEC oil embargo and the Saturday Night Massacre occurred in the same week as did the Clinton confession to the grand jury and Russian debt default happened on the same day.

.

The double shock of OPEC, raising the price of oil by 70 percent with further cuts in production to follow, coupled with the Saturday Night Massacre, raising the specter of a constitutional crisis in the U.S., sent the global economy and markets into a tailspin.

As the chart illustrates, these two events marked the end of the short-term rally. The S&P500 proceeded to fall another 43.5 percent through the resignation of President Nixon on August 8, 1974, until it bottomed on October 3, 1974.

From its January 1973 high until the resignation of President Nixon in August 1974, the S&P500 fell 32 percent.

OPEC or Watergate?

So we ask you, folks, what was the main cause of the 1973/74 bear market and 50 percent decline of S&P500? Watergate or OPEC?

Structural Economic Damage of OPEC

Nobody knows for certain, but we maintain speculate that if the global economy had not suffered the structural damage from the OPEC shock, the Watergate scandal would have been just noise and the S&P500 would’ve probably not even entered a bear market and suffered only a normal correction. That is unless Nixon sent tanks out onto Pennsylvania Avenue.

Though the S&P500 bottomed less than two months after President Nixon resigned, it didn’t regain its January 1973 high until July 17, 1980. The stagnation of the 1970’s brought on by the structural damage to and the massive realignment of the global economy of the OPEC shocks definitely took a major long-term toll on the financial markets.

Yom Kippur War

An argument can be made that Watergate distracted and weakened the Nixon administration, which emboldened the Arab nations that attacked Israel during the Yom Kippur War in early October 1973. The Nixon Administration responded with Operation Nickel Grass, a strategic airlift to deliver weapons and supplies to Israel.

This was after the Soviet Union began sending arms to Syria and Egypt. The Arab nations of OPEC, in retaliation to Operation Nickel Grass, raised the posted price of oil on October 16. The actions of the Soviets and OPEC may have been the result that they and the world perceived the U.S. weak due to a domestic political scandal. Pure supposition on our part.

So, Watergate, a necessary condition to the 1973/74 bear market? Maybe.

What About Trumpgate?

So far no hard facts and no smoking gun, at least that is publicly known, no John Dean testimony, no tapes.

But potentially more complicated. The underlying allegations are much more serious than covering up of a third rate political burglary and lying about, well, you know. Also, a much wider net that could consist of many things, including improper business transactions that took place prior to taking office.

Lots of incompetence, strange and suspicious behavior from the administration, combined with speculation, rumors, coincidences, and what appears to be circumstantial evidence of some sort of a coverup, and the punditry in a feeding frenzy desperately trying to connect the dots. Once again, a total media circus.

Oh yes, and the appointment of the highly and widely respected Special Counsel, Robert Mueller, to “oversee the previously-confirmed FBI investigation of Russian government efforts to influence the 2016 presidential election and related matters.”

Though the appointment of Mueller illustrates just how serious the matter is, and is becoming, it should be seen as a positive by both those who suspect President Trump is guilty of something as it takes the specter of a constitutional crisis off the table. And for those who believe the President has done nothing wrong, the appointment of the Special Counsel should vindicate him. All other things being equal, the Mueller appointment should be a positive for the markets.

Unless President Trump fires the Special Counsel.

Furthermore, doesn’t it seem like President Trump is making a special effort to go out of his way just to troll his political opponents?

Conclusion

Granted the initial conditions of these three cases differ greatly. Valuations, liquidity conditions, and the structure of the global economy all have changed dramatically. But as illustrated in our analysis, it is usually not a great idea to short stocks based solely on an impeachment trade. In fact, we tend to agree with what Professor Jeremy Siegal of the Wharton School said yesterday on CNBC,

“If Donald Trump resigned tomorrow I think the Dow would go up 1,000 points,” – Jeremy Siegel, May 17, 2017

The corollary is that the Republican pro-economic growth agenda is then accelerated as the political distraction, incompetence and protectionist bias of the current administration are removed. And that the policies are passed before the 2018 election, which the Republicans are becoming increasingly vulnerable to losing both houses of Congress.

The downside scenario is that the investigation lingers, the bad news keeps dripping out, nothing gets done, the Democrats take the House in 2018 and introduce impeachment hearings. That may be the most likely scenario and stocks won’t like it, especially given their high valuations.

Our sense, the Republicans may believe this scenario and double up their efforts to unify and get something done quickly — that is going to the “two-minute offense” — as the clock runs out. Stock positive.

One Big Caveat

Noted in our analysis are the two big “coincidences” of bad things concurrently occurring at tipping points during the two impeachment proceedings. The Russian default on the same day President Clinton confessed to the grand jury and the OPEC oil embargo during the same week of Watergate’s Saturday Night Massacre. Coincidences?

Bad things tend to happen in the world when the U.S. administration is distracted and looks weakened by political scandal. And, believe us, there is a legion of bad things out there just waiting to happen, all of which are stock market negative.

And then there is “wag the dog“.

The 6 Sigma Event: President Pelosi in 2019

Finally, you know we like to think outside the box here at the Global Macro Monitor and live in the fat tails.

Contemplate this 6 sigma scenario:

Bad news for Trump continues to leak out and staffers and acquaintances are indicted all through the rest of 2017 and 2018. The Democrats take the House and Senate in a landslide in November 2018.

Impeachment charges are brought both against President Trump and Vice President Pence, say, as a co-conspirator on obstruction of justice charges in the firing of James Comey.

It’s 2019 and the Dems control the House and the Senate with comfortable majorities.

The House impeaches the President and Vice President. The Senate convicts both.

Who is next in line to assume the Presidency? The Speaker of the House, Nancy Pelosi?

The probability? Six sigma or about 2 * 10^-9 or two in a billion. Most likely, even much, much lower.

Hey, but good stuff for a political thriller or fodder for the House of Cards, no?

Wow! Just heard a so-called “banking expert” say that the Fed was reducing reserves on their balance sheet during quantitative tightening (QT), which has led to the current chaos in the overnight repo market. Not entirely true.

Asymmetric Libalibity Balance Sheet Accounting

During QE the Fed purchased assets in the secondary markets, primarily Treasury notes and bonds, and mortgage-backed securities (MBS), by increasing their liabilities in the form of bank reserves. During QT, on a monthly basis, the Fed did not reinvest some or all of the maturing securities purchased during QE up to a certain monthly cap. The U.S. Treasury, for example, would have to pay down the debt by reducing their cash balance at the Fed.

Rather than reducing reserves on the liability side, the Fed would reduce their liabilities by the reduction of the Treasury cash balance equivalent to the maturing securities. We are not certain, but suspect, when MBS rolled off, reserves were reduced. The Fed is a bit less transparent when it comes to their MBS portfolio, at least that is our perspective and could be due to the complications of prepayment risk.

Nevertheless, we believe QT worked more through a high powered fiscal channel as the maturing Treasuries sucked liquidity out of the market through maturing debt and not a direct reduction in bank reserves on the Fed balance sheet. As a consequence, the Treasury had to issue more securities in the market to replenish their cash balances, an effective checking account, at the Fed. Crowding out on steroids.

Still, at the end of the day, excess reserves in the monetary system have tracked the reduction in Federal Reserve assets fairly closely but certainly not a rho =1, perfect correlation. There is the rub.

Monetary Policy Is Complex And Complicated

As an undergraduate political science student (double major in econ), I read somewhere that President Kennedy had much trouble understanding the difference between monetary and fiscal policy. In fact, to prevent from conflating the two in public, he wrote cheat notes with a pen on each fist before his press conferences. I am still searching for the source of that factoid.

Even former Chairman Alan Greenspan admitted monetary policy is a black box,

There is, regrettably, no simple model of the American economy that can effectively explain the levels of output, employment, and inflation. In principle, there may be some unbelievably complex set of equations that does that. But we have not been able to find them, and do not believe anyone else has either.

Consequently, we are led, of necessity, to employ ad hoc partial models and intensive informative analysis to aid in evaluating economic developments and implementing policy. There is no alternative to this, though we continuously seek to enhance our knowledge to match the ever-growing complexity of the world economy. – Alan Greenspan, Decemeber 1996

The Pragmatic Capitalism blog has the best perspective on the complexity of today’s monetary system, in our opinion,

The monetary system is too complex and too dynamic for you to understand it all. So it’s better to understand enough that you can be competent, but not so much that you become a danger to yourself. – Cullen Roche

So, nobody knows with absolute certainty what the hell is going on in the repo and money markets.

Are bank reserves too low? Are markets starting too convulse because debt is too high? Is there a temporary mismatch in cash flows of different financial entities? Is the problem a temporary blip or more systemic? All of the above? None of the above?

Wish we could say, but we don’t know.

Nevertheless, as Goethe once stated,

By seeking and blundering, we learn.

Look At Deficit Financing

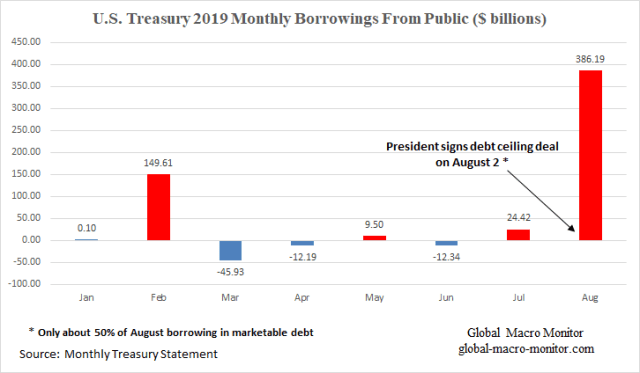

We do have our suspicions that the money market turmoil has something to do with what is happening with the huge increase in the budget deficit, which in the first 11 months of fiscal (Oct-Sep) 2019 is close to $1.1 trillion dollars. That’s larger than the combined GDPs of Austria, Ireland, and the Czech Republic. In addition, how the deficit has been financed during the budget ceiling negotiations we believe is also impacting market liquidity.

It’s tantamount to holding a beach ball underwater and then released when the President signed the debt ceiling deal at the beginning of August.

Add to that our distorted monetary system where interest rates are repressed and prices can’t clear the market but quantities will. Think, rent control.

A decade of extraordinary monetary policy experiments has left the system badly distorted. Thus the Fed is now like a pilot flying a plane with an engine that has been stealthily remodelled. Neither the passengers nor the pilot knows how the engine’s shifting cogs might affect the controls during a wave of turbulence, because there is little historical precedent. — FT, Sep 19th

Le Chatelier’s Principle (LCP)

It’s a classic case of Le Chatelier’s principle (LCP) in action. If one economic variable is repressed in a dynamic equilibrium system, such as prices or interest rates and not allowed to adjust to clear the market, another variable in the system will have to move to offset. The great economist, Paul Samuelson, did his Ph.D. dissertation on LCP.

Maybe that variable is cash liquidity?

It is clear to us, there is too much debt in the system to allow interest rates to move to their equilibrium levels in a steady-state normal world. We saw what happened in Q4 2018 to the stock market when the 10-year Treasury yield broke out higher, one year ago to almost this very day.

Because rates can’t move higher to a technical equilibrium level as the supply of debt increases, the larger budget deficits will have to be financed by either haven flows as other markets (stocks, e.g.) sell off, foreign inflows (stronger dollar), more indirect monetization in the form of some kind of QE or a derivative of POMO, OMO, a combination of all of the above, or whatever you want to call it.

It doesn’t seem there is much appetite to allow markets to fall to generate the haven flows nor for a stronger dollar. Ergo, the Fed will be forced to do the heavy lifting. If you been reading GMM over the years, you know which variable will offset the Fed activity. That is the end game.

Coming Soon

We are still working on the analysis but here is a sneak peek at some of the data.

Again, looking at the data in the table, we believe the Treasury is going to be issuing a lot more debt in the next few months to make up the months of nonborrowing from the public due to this year’s debt ceiling constraints, Similar to the first 8 months of last year (see table), which was a catch-up from the 2017 debt ceiling debacle.

As usual, we reserve the right to be wrong. Stay tuned.

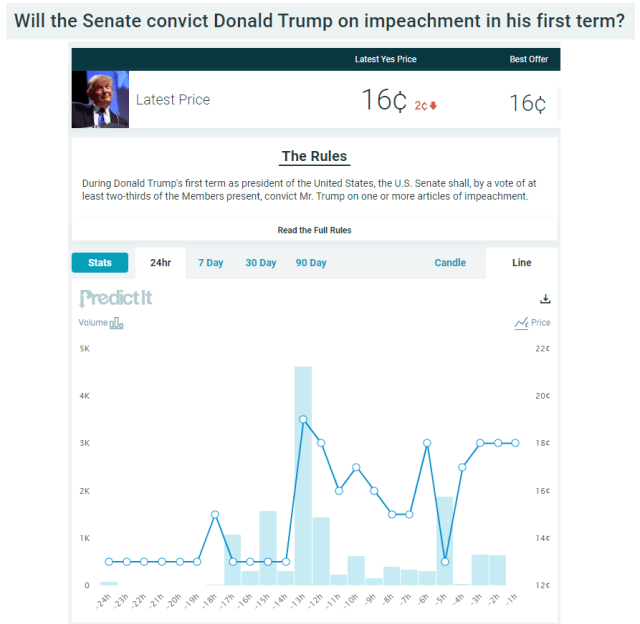

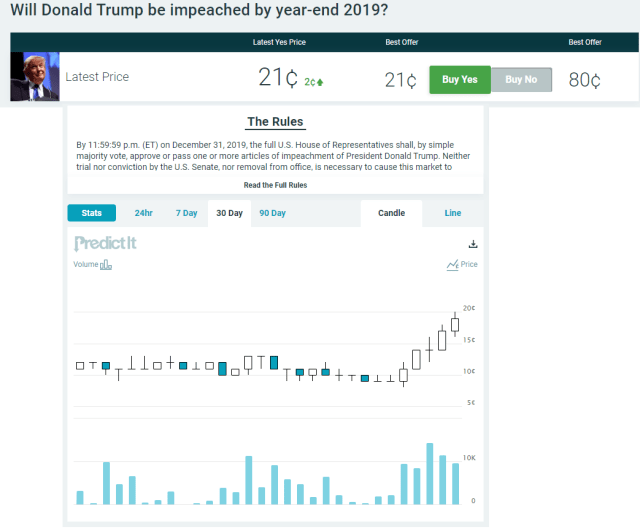

Since our post on the impeachment market about nine hours ago, the 2019 contract is up 81 percent, from 21 to 38, and 322 percent in the past week. Annualize that return!

Mr. Market is not priced for the coming political instability the prediction markets are now starting to price. Almost even money now for the first term impeachment contract.

Check out the prediction market on impeachment over at PredictIt.

Odds Have Moved From 11:1 To 4.8:1 Trump Will Now Impeached By Year-End

The contract that Trump will be impeached by the end of 2019 is up 133 percent in the last week, moving the odds from 11:1 to 4.8:1.

The contract for impeachment by the end of Trump’s first term is up 71.4 percent, moving odds from 4.8:1 to 2.8:1.

Of course, impeachment doesn’t mean removal but Leon Cooperman said on CNBC last week,

“Right now, the market is assuming Donald Trump is reelected.”

2.05 minutes in

Click here to view video

Please, no hate mail accusing us of partisanship. We are just conveying information that many of our readers are probably not aware of.

Put your money where your politics are and place your bets, folks. Mr. Market certainly isn’t pricing it. Maybe there is an arb here?

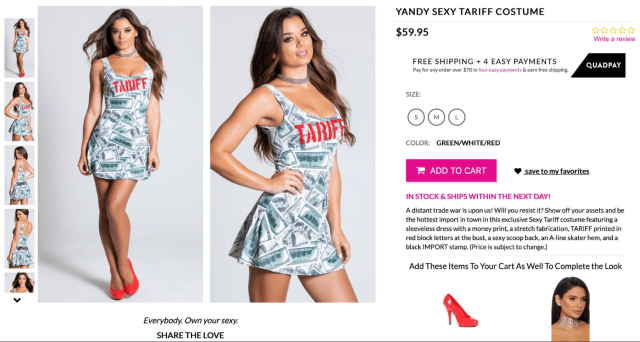

Probably not the roll back China was looking for?

Capitalism at its best or worst?

We have a few questions: 1) Does the Tariff Man get a royalty for the sale of each dress sold, and will that violate the Emoluments Clause of the U.S. Constitution, and 2) Are the dresses Made in China?

Just askin’.

Hat Tip: @scottlincicome

Once again, seeing lots of articles and talking heads mocking bubbles and the bears, which is usually a sign a big bubble is going to burst. The last time we saw this kind of taunting of the bears was three days before the bear market, which we think is on, began in January 2018.

Here’s what we wrote,

Finally, you also see the investing public openly mocking the bears during the later stages of a bull market. We see a lot of that these days. Just check your twitter feed. – GMM, January 23, 2018

Stress In Money Markets

Nobody really knows for certain what is causing the stress in the money markets, but our calculated guess is it is: 1) somehow related to the massive new issuance of Treasuries, which is sucking liquidity out of the markets, as prices are repressed and not allowed to clear –> think, a) rent control, where the excesses have to be cleared through quantities, and b) Le Chatelier’s principle, where, in a dynamic equilibrium, pressure on one variable has to be offset by movement in other variables; 2) primary dealers stuffed with Treasuries having to fund themselves, and 3) though there are still $1.4 trillion of excess reserves in the banking system, it is possible only a few banks hold the bulk and are hoarders. In other words, another top-heavy distribution problem, along with wealth and income, where the few own the much.

Whatever the case, the markets are so distorted now and becoming more so, especially by the false belief that central banks can even now fine-tune a Stradivarius violin. Haha!

We believe quantitative easing and the massive expansion of central bank balance sheets are the financial equivalent to excessive carbon emissions resulting in kind of a of global warming in the markets. Thus, traders and investors should expect more extreme weather market conditions.

Didn’t you see this coming?

To be fair to Adam, we took the headline a bit out of context to make our point. Please read his article here.

Discount The Street

During my days on Wall Street, it was stunning to watch how many would sell their souls and anything else to help them make their year-end bonus. I specifically remember a sales pitch by some bozo about how the Mexican Peso was going to become the next dollar, less than 12 months before it fricking blew! We laughed him out of the office.

This is one reason why Mr. Market is so cold-blooded, doesn’t correctly discount risk, and tends to have a one in every 10,000-year event (high sigma crash) almost every 10 years.

So, folks, when listening to the Street, bubble vision, the market talking heads, and even central bankers and policymakers, take heed the words of the great American author, Upton Sinclair.