Selling 5 contracts at the open of the overnight session. Back to you with levels.

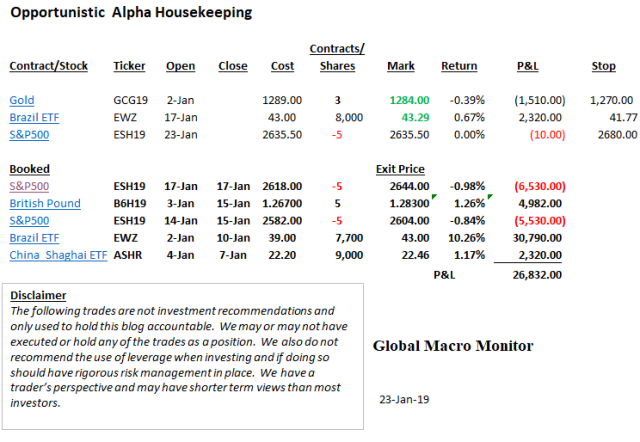

Update: Sold 5 March S&P e-minis at 2635.50. Stop at 2680.00.

Comment: Looks like good news on China deal is pushed out, less of a tape bomb risk and increasing probability that negotiations could go sideways. The admin loses cred everytime they trot out Kudlow to goose the market.

The temperature is heating between Trump and the Dems, which we are betting may spook the market. Could just be posturing ergo be careful of tape bombs in the form an olive branch after tomorrow Senate votes. Trump has backed himself into a corner a needs a way out as his polls numbers are dropping like a stone.

The Chinese are watching.

Staying flexible. Nervous there are too many bears roaming the market and some decent chip earnings. Intel big after close tomorrow.

Didn’t like selling in the hole, down 3 1/2 points below the fair-value close, but could get some ugly headlines overnight. Or, maybe not.

Brazil continues to trade well, gold doing nothing, and the British Pound got away from us.

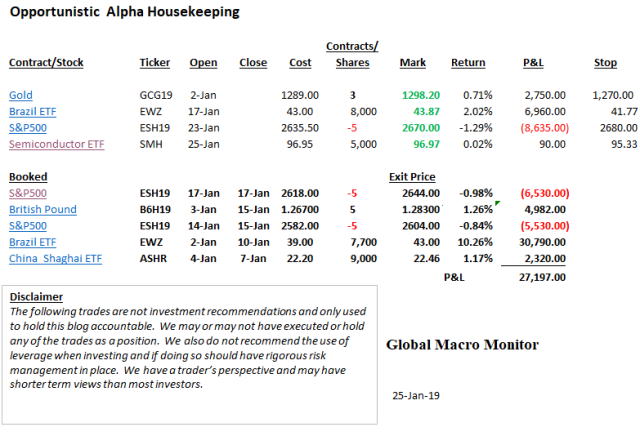

Hope you stayed long, now trading with a 1.31 handle, up over 3.5 percent from the original entry.

Do as we say, not as we do.