Italy calmer as market turns it focus on trade wars.

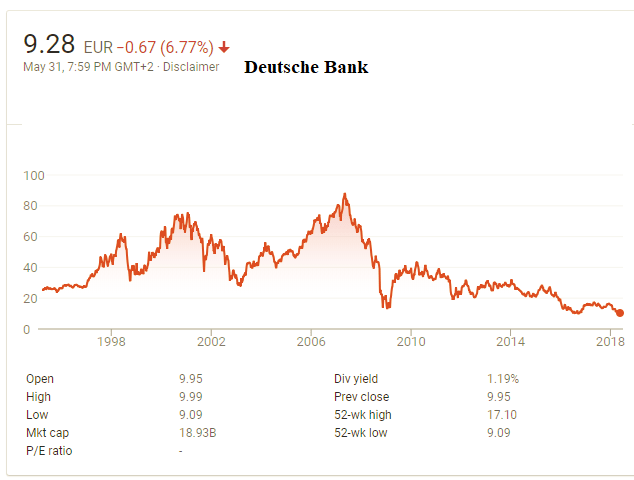

Deutsche Bank making all-time lows as it was hammered again due to its U.S. business put on problem bank list. DB is now getting the market’s attention but still doesn’t fully realize the potential problem. Remember, we were there first.

Stunning! Even God has to worry about being displaced by technology.

Just kidding. Please, no Tower of Babel hate mail from the faithful.

Scientists at Newcastle University have 3D printed the world’s first human corneas. By creating a special bio-ink using stem cells mixed together with alginate and collagen, they were able to print the cornea using a simple low-cost 3D bio-printer. It’s hoped, after further testing, that this new technique could be used to help combat the world-wide shortage of corneas for the 15 million people requiring a transplant.

Italy’s president has attempted to broker an eleventh-hour deal between the country’s two largest populist parties to avoid another destabilising national election, helping Italian assets recover from a sell-off that rattled investors worldwide.

Sergio Mattarella, who triggered this week’s crisis by blocking the appointment of a Eurosceptic finance minister proposed by the two parties last Sunday, held informal meetings with leaders of the anti-establishment Five Star Movement and the far-right League on Wednesday evening. FT

Political noise will be elevated in Italy through the summer, and investors and traders should excogitate a strategy and execute it. Discount the day-to-day noise.

Italy’s auctioned 5 and 10-year bonds today,

Italy successfully sold five- and 10-year debt at an auction, bringing some relief to jittery markets following this week’s meltdown in the nation’s bonds amid a political crisis.

…Both auctions were oversubscribed by investors, buoyed by large reinvestment flows from a bond maturing later this week. Still, the pricing of the longer-dated note showed signs of the pessimism that has battered the market this week. – Bloomberg

Check out today’s auction results versus Monday here and here. Note today’s 10-year auction 1.48 bid-to-cover relative to 2.23 in Monday’s auction.

The two major factors to watch are: 1) the polls and to whether Italian voters solidify their support for the euro currency, or harden their positions against it, and 2) if 5-Star and Lega move forward to form a government, who will be the finance minister in the new government?

Increasing fear among Italians of an ITALEXIT as the markets punish the country is the hope bet of many in the EU. Even the majority of the Greeks, during the height of their debt crisis, didn’t contemplate leaving the euro.

“My concerns and expectations are that the coming weeks will show that developments in markets, government bonds and Italy’s economy could be so drastically impacted that they serve as a signal to voters not to vote for populists on the right and left.” – Guenther Oettinger, a German EU commissioner

Indicators

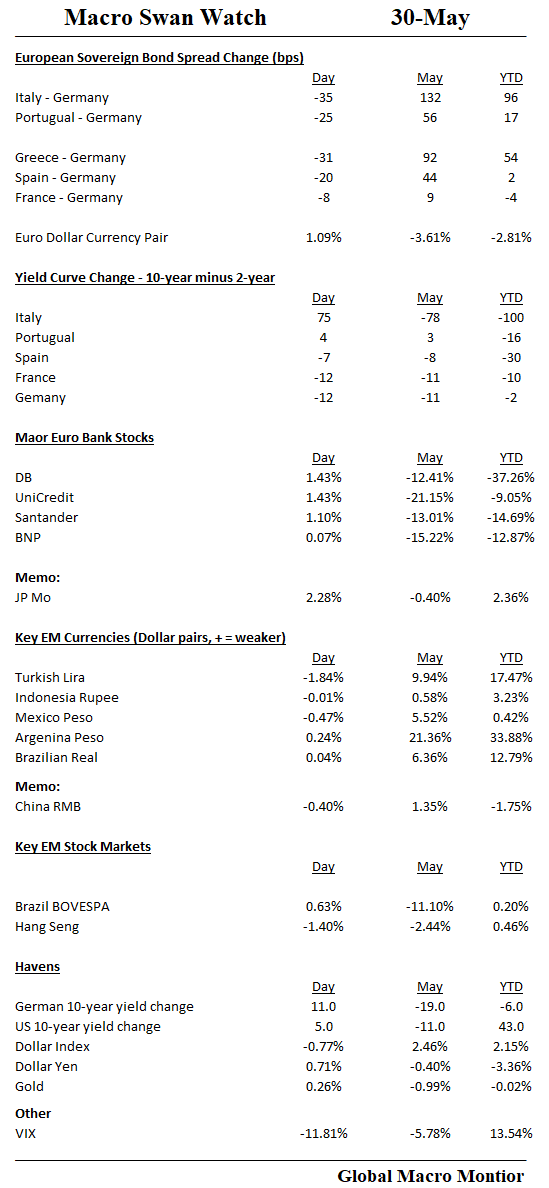

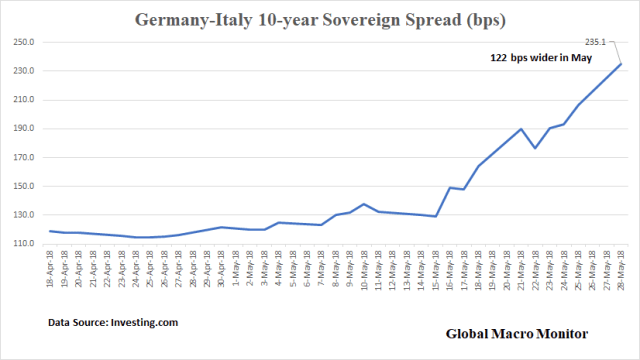

Big snap back in Italian sovereign spread and sharp yield curve steepening. Looks like big short cover in 2-years. Euro banks did not recover as much.

EM mixed. Dip buying algos and traders rewarded in U.S. equities.

We have been warning over the past few weeks that the macro swans have been gathering. See here,here, and here.

Swan Watch

The Global Macro Monitor defines “macro swan” as any global macroeconomic or financial event with the capacity to spill over into world markets causing risk aversion and lower asset prices. Today, they attacked.

We don’t know how long this is going to last but it will almost certainly last longer than the cheerleaders suggest. We will continue to monitor the market signals and will try and post a our swan watch table (see below) on a daily basis until the coast is clear. It is a work in progress and will change over time.

Euro and EM Swans

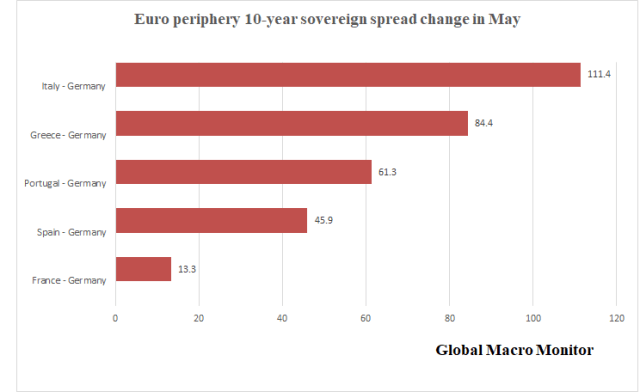

The big swans we are currently focusing on are the Italian-led bond market crash in the Euro periphery and the exchange rate and bond volatility in a few of the large emerging markets.

While gathering the data what stands out the most is the massive and rapid curve flattening in Italy relative to the other periphery countries. Curve inversion is signal of potential credit problems and worries of default. Not seeing that in the other periphery countries yet.

Deutsche Bank

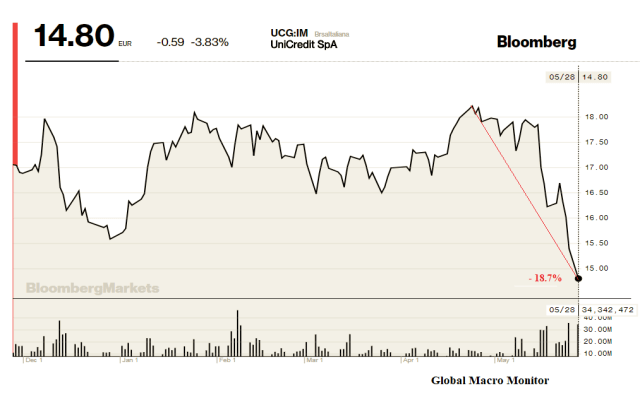

Deutsche Bank, another macro swan, was hammered today with the stock closing in the single digits at €9.82. The bank’s market cap of €20.3 billion now supports a €1.48 trillion balance sheet. That’s a market cap to asset ratio of 1.38 percent. Something may be rotten in the state of Denmark Deutsche’s balance sheet.

Conversely, JP Morgan’s market cap of $360.6 billion supports a balance sheet of $2.61 trillion, a market cap to asset ratio of 13.8 percent. That is a healthy bank.

Keep it on the radar.

The Fed

Finally, lots of chatter today how the Fed will have to slow its interest rate hikes. Maybe, maybe not.

More important is what are they are going to do with their balance sheet?

That part of monetary tightening is on autopilot and won’t be adjusted unless the FOMC takes extraordinary action. We calculate SOMA account holdings on the balance sheet have been reduced by $107 billion since September 2017, including a $87 billion decline in Treasury notes and bonds and $24 billion in agencies.

Also, another $300 billion of balance sheet reduction is on the books from June to December, including a roll off of $180 billion in Treasury notes and bonds and $120 billion in agencies. Nobody knows the consequences of how such a sharp reduction in the monetary base will affect markets, but we may be seeing it in how some of the indicator species of tighter money, such as the emerging markets, are currently behaving.

Italy’s president, Sergio Mattarella, named Carlo Cottarelli, prime minister as the attempt to form a left-right populist coalition government fell apart after Mattarella’s veto of Eurosceptic economist, Paolo Savona as finance minister. An extraordinary development almost tantamount to the Queen of England prohibiting the U.K prime minister from appointing a chancellor of the exchequer.

Sergio Mattarella, Italy’s president, has tapped Carlo Cottarelli, a former senior IMF official, as caretaker prime minister after frustrating a bid by two populist parties to run the eurozone’s third-largest economy.

Mr Mattarella asked Mr Cottarelli to assemble a technocratic cabinet as Italian bonds and equities were hit by a sell-off in reaction to the rising political uncertainty and a mounting constitutional crisis.

Mr Cottarelli accepted the mandate and attempted to deliver a soothing message to markets, although he is widely considered unlikely to win a vote of confidence, which would trigger fresh elections by the autumn.

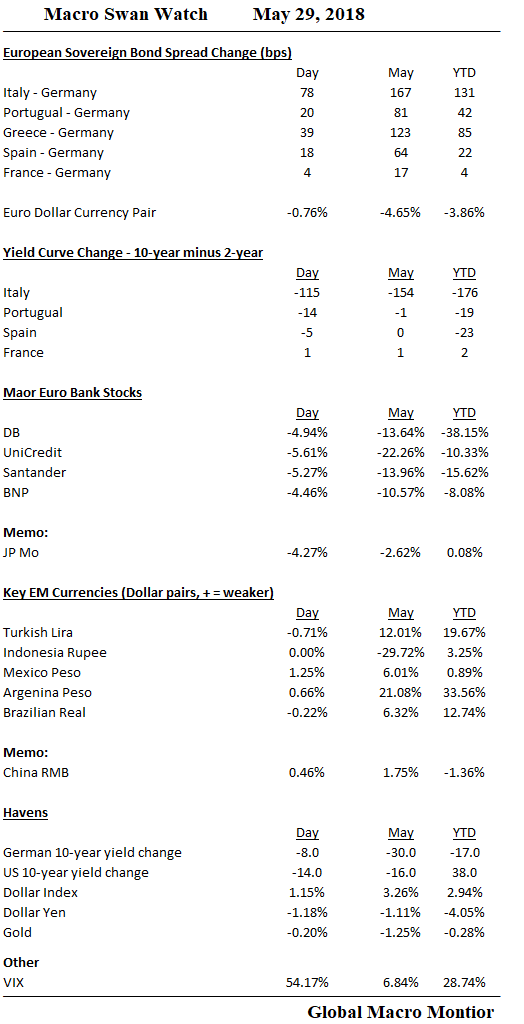

…But the message failed to register with investors amid the confrontation between the populists and the old political order. The country’s debt yields ratcheted up to levels not seen since the aftermath of the eurozone debt crisis as Italian government bonds came under heavy selling pressure.

The FTSE MIB index was also hit hard, led by bank stocks. In mid-afternoon trading in Milan, Italy’s main stock barometer was down 2.5 per cent, leaving the loss for the month of May at nearly 9 per cent and wiping out all against this calendar year. – FT, May 29

Upshot?

More political uncertainty and bigger populist blowback. The markets are not buying the appointment of an IMF technocrat as it did during 2011 European debt crisis with Mario Monti, seeing through it an impetus for greater political blowback.

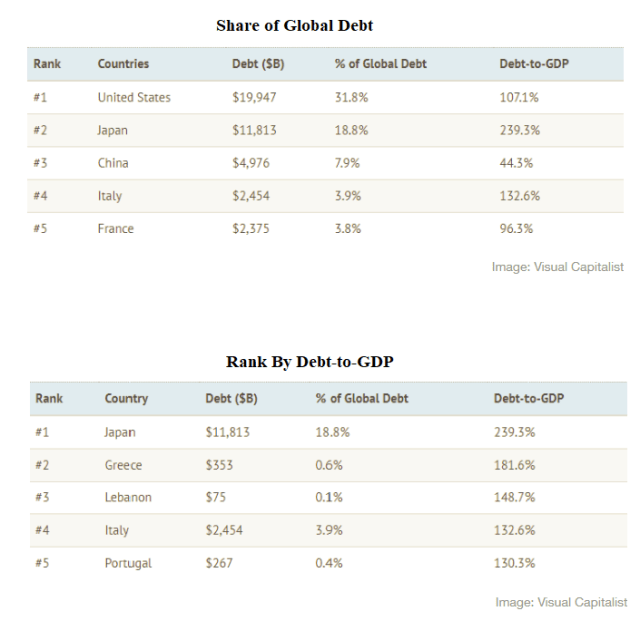

Italy is the 4th largest sovereign debtor government in the world. The risk of contagion to the rest of the world is more likely than not, in our opinion. It has already begun in Europe as sovereign spreads are starting to correlate. Today’s spread widening: Italy + 29 bps; Spain +12 bps; Portugal +19 bps;, and Greece +15 bps.

Bond Market Convexity Going To Do More Damage

A massive spread blowout today will also be more painful and do more damage than it did in 2011 due to how lower interest rates have affected the convexity of the bond market. That is given an increase in yields; bond prices are hit much harder. The New York Fed has written about the “convexity event risks” in the bond markets.

The pain will have to get much worse in Italy to put the fear of ITALEXIT into the country’s realpolitik.

That said, Italy was still able to auction debt today.

Italy placed the top planned amount of 1.75 billion euros ($2 billion) of a zero-coupon bond maturing in March 2020 at a gross 0.35 percent yield, up from a negative yield of minus 0.275 at the previous auction in late April…

…At Monday’s auction, Italy also placed a combined 1.25 billion euros of two inflation-linked bonds maturing in May 2022 and May 2028, meeting the top of its targeted issuance range.

The May 2022 BTPei bond fetched a gross negative yield of minus 0.05 percent. It had last been sold in February at minus 0.41 percent.

Italy paid 1.28 percent to place the May 2028 linker up from 0.47 percent when it last auctioned it a month ago.

The Treasury will sell six-month bills on Tuesday and up to 6 billion euros in bonds on Wednesday, including 5- and 10-year nominal bonds as well as a seven-year floating-rate one. – Reuters

We need to confirm on whether or how the ECB directly participates in bond auctions. The posted auction results are not as transparent as in the U.S. (see next link). Nevertheless, the Italian 10-year went off with a 2.23 bid-to-cover today.

There doesn’t seem like funding stress quite yet, but an Italian 2-year at 0.35 percent with a depreciating Euro is a juicy target for the bond market vigilantes who want to test Super Mario and whether eMac is ready to lead Europe

President Trump, The Populist

Furthermore, the Trump administration’s “save Europe” policy in the event of a crisis will likely be much different from the pro-EU Obama administration during the 2011 crisis. Philosophically, President Trump is closer to the populists than he is to Macron.

Italians bond yields should not be this low on a fundamental basis, yet they are, and it is the result of the Draghi put. We wrote the following in our May 9th post, Italy’s North-South Economic Divide,

The Italian 10-year government bond is 112 bps through the U.S. 10-year note yield, and the country doesn’t have an independent central bank! Moreover, the Germans are coming to town at the ECB very soon. How is that for pricing risk?

Moreover, the political dynamics in Germany are going to complicate another ECB bailout of Italy if one is needed.

Eckhard Rehberg, a member of Chancellor Angela Merkel’s Conservatives, didn’t mince words: “Italy is playing with fire and is endangering the euro zone.” – Handelsblatt Global