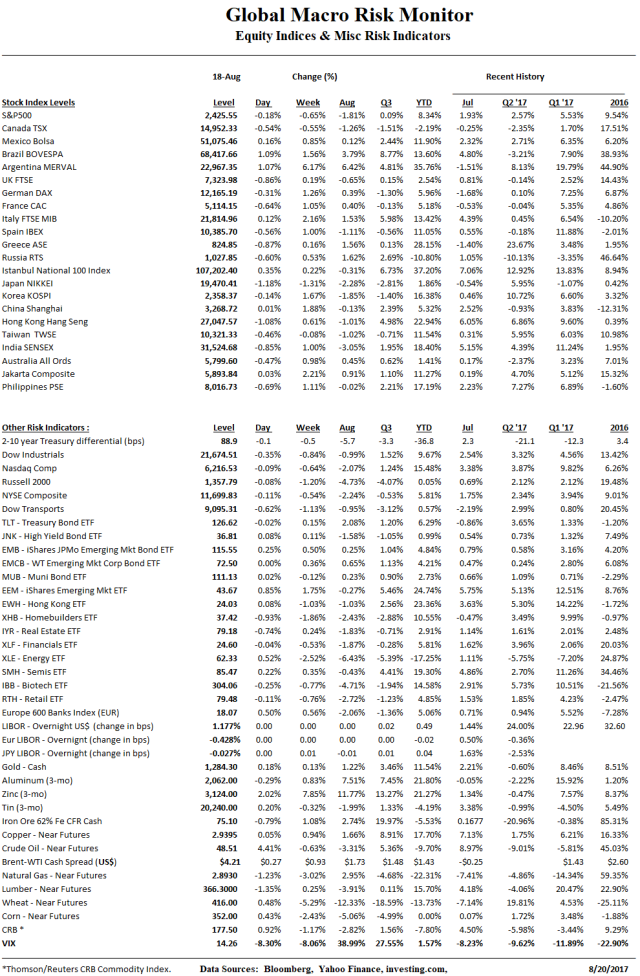

Click on table to enlarge and for better resolution

Click on table to enlarge and for better resolution

Click on table to enlarge and for better resolution

On August 1st we warned in our post, Watch This Space – Industrials v Transports, to monitor the Dow Industrials-Transports divergence:

Not as relevant as it used to be, but something to keep on your radar. Transports approaching 200-day moving average at 9,117.59 [corrected on Aug. 19] and diverging from Industrials..

– GMM

We also posted this chart:

Let’s Revisit The Analysis

The Trannies peaked on July 14th; are down 6.85 percent from that high; have closed two consecutive days through its 200-day moving average for the first time since July 2016; though only currently about 1 percent below the 200-day.

The Dow Industrials index peaked on August 8th and is down just 2.28 percent from the high. The S&P500 has already aready pierced its 50-day, the Dow remains a little over 50 points above its 50-day moving average.

During Historic Low Volatility

What is surprising is that the Transports and Industrials parted ways during the calmest three-week period in S&P500’s history.

Here’s to another record for 2017, as the past 15 trading days have officially marked the calmest stretch in the history of the S&P 500 Index. Per Ryan Detrick, Senior Market Strategist, “As amazing as this is to say, the S&P 500 hasn’t closed more than 30 basis points up or down for a record 15 consecutive days. Even in the face of heightening geopolitical tensions, we are in the midst of the calmest three-week period in history.” – LPL Research, August 10, 2017

North Korea

Markets are always complacent and ignore event risk during bubblicous and extremely loose financial conditions, until they don’t.

We also noted the ripping South Korean stock market and currency in our July 24th post, No Worries In The South Korean Markets, even as the missiles were flying one after another all throughout the year just 35 miles to north of Seoul.

We have been writing a lot these days about how crude oil is not pricing any geopolitical risk of a very messy Middle East. See here and here.

That’s nothing, however, compared to the performance of the South Korean stock market and currency, year-to-date, given the geopolitical risk of the many North Korean missile tests fired off in the first seven months of 2017 (see timeline below). The KOSPI stock index is up 21 percent and the currency has strengthened a little over 7 1/2 percent against the dollar.

Oh, by the way, Korea also impeached and removed their president earlier this year, had a presidential election, and has also been put on a currency manipulation monitoring list by the US Treasury.

…Is this the definition of “climbing a wall of worries”, complacency, or just a bullet proof bull market? We vote for capital flows seeking emerging markets.

– GMM, July 24, 2017

Ironically, the South Korean Kospi stock index peaked on the date of our post and proceeded to decline around 6 percent before recovering a few hundred basis points in the last week as worries over the nuclear crisis subsided, at least temporarily. The dollar has gained about 2 1/2 percent against the Korean won since July 24th.

Joint Military Exercise This Week

The markets will be watching North Korea with a keen eye this week as the U.S. and South Korea begin their annual war games on Monday, which included 25,000 American and 50,000 South Korean soldiers last year. The NY Times reports very provocative posters have gone up in North Korea over the past week.

“What is typical in these posters is the image of an undaunted, fierce North Korea that is not fazed by the moves by the United States or the United Nations,” Koen de Ceuster, an expert on North Korea at Leiden University in the Netherlands, told Reuters.

…Countries use various signaling techniques in times of crisis, experts in geopolitics say, including diplomacy, back-channel talks and public messaging. The North is clearly sending a message with these posters.

…For now, the war of words has been muted. But a potential inflection point looms. On Monday, American and South Korean troops will begin annual large-scale war games — the first since the North test-fired missiles that might be able to reach the United States mainland. – NY Times, August 19

The North Korean crisis seems even more uncertain now and much riskier after Steve Bannon’s comments last week, which may embolden Kim Jong-un to challenge President Trump’s ““fire and fury” threats.

There’s no military solution here; they got us.”

“Until somebody solves the part of the equation that shows me that 10 million people in Seoul don’t die in the first 30 minutes from conventional weapons, I don’t know what you’re talking about,” Mr. Bannon said in a phone call with Robert Kuttner, The American Prospect’s co-editor. – NY Times, August 17

The New York Post reports today,

There’s media speculation that the allies might try to keep this year’s drills low-key by not dispatching long-range bombers and other U.S. strategic assets to the region. But that possibility worries some, who say it would send the wrong message to both North Korea and the South, where there are fears that the North’s advancing nuclear capabilities may eventually undermine a decades-long alliance with the United States.

“If anything, the joint exercises must be strengthened,” Cheon Seongwhun, who served as a national security adviser to former conservative South Korean President Park Geun-hye, said in an interview.

…It’s almost certain that this year’s drills will trigger some kind of reaction from North Korea. The question is how strong it will be. – NY Post, August 19

Stunning to think, at least to us, with such ubiquitous event risk on the horizon that global markets were so calm over the past few months. Until they weren’t.

Conclusion

We’re not taking any victory laps here. We, along with everyone else, have no idea what the future holds. The market could crash next week or rip to new all-time highs.

The Trannies could rebound big, the North Koreans could remain calm during the joint military exercise (doubt it), and President Trump could name Gary Cohn to replace Janet Yellen as the Fed Chairman, not inconceivable if markets continue to decline. Or not.

The major stock indices are only 2-3 percent off their highs. Nothing.

The one big lesson we’ve learned this year, however, is the best short-term bet is to usually take the opposite side of how the majority of the fast money is positioned. We don’t have that information, however.

Increasing Event Risk

But, the markets are looking increasingly vulnerable to event risk, of which we see many through October: 1) seasonality; 2) the Fed balance sheet should, or could start shrinking; 3) China’s Party Congress may have concluded, removing the country’s implicit policy put, and thus increasing the risk of a China policy or economic shock; 4) the new U.S. Federal government fiscal year begins October 1 and if the Trump administration has not passed any significant economic legislation, the markets may begin to throw in the towel; 5) there will be more clarity on ECB tapering; 6) potentially even more elevated asset prices if the risk markets recover and grind to new highs through the rest of summer; 7) nervousness over the debt ceiling; 8) more political instability; and 9) North Korea.

What We Are Watching Next Week

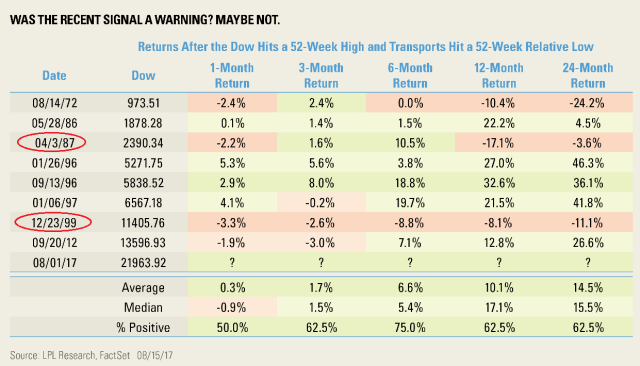

1) Dow Transports. Since the Trannies led the sell-off it is number one our list.

Per Ryan Detrick, Senior Market Strategist, “Going back in history, we have often seen the rare combo of a 52-week high in the Dow and a 52-week relative low in transports precede some tumultuous times. It took place ahead of the ‘73/’74 bear market, the ’87 crash, and the ’00 peak for starters, which makes the signal seen earlier this month something we aren’t taking lightly.”

Now here’s the good news: The track record of this rare signal is far from spotless. Per Ryan Detrick, “Although on the surface this sounds scary, looking at all the signals (to remove clusters, each instance must be at least three months apart to define a new signal) in which the Dow and Dow/transports spread hit new 52-week highs, the Dow has been up a median 17.1% over the following year. We’d still say the weakness in transports is a concern, but a bigger concern is that we’ve gone more than a year without a 5% correction, and there are multiple big events (think debt ceiling, tax reform, and infrastructure spending) out of Washington on the horizon that could trip up the market.” – LPL Research, August 16

2) North Korea. Will Kim Jong Un test President Trump? If he does, will President Trump back down? War is a low probability, but extermely high impact event. Not enough fear priced. We hope and pray for de-escalation.

3) Market Reaction to Carl Icahn Resignation. See here for Carl Icahn’s resignation letter to President Trump submitted around 5 PM eastern on Friday.

4) Jackson Hole Economic Symposium, “Fostering a Dynamic Global Economy.” Runs through August 24-26. Mario Draghi will be big.

Pressure is mounting on the world’s central bankers to give more clues about how they intend to exit huge stimulus packages unfurled to dig the global economy out of a hole after the financial crisis. After a decade of low-interest rates and bond buying, a process known as quantitative easing, the Jackson Hole summit could be a platform to convince markets they can safely wean the world off cheap money.

…The Fed chair, Janet Yellen, is the first leading figure to speak at the event on Friday, followed by Draghi later that day. – The Guardian, August 20

Finally, we recognize the global economy seems to be gaining some traction, global interest rates remain extremely repressed, the BoJ and ECB are still buying assets, the global financial system overfloweth with central bank money, investors like to make money and are forced to chase yield and returns, and the markets are chock-full of buy the dipper algos.

Ergo, no bear market until the above conditions change.

A Tower of Terror flash crash sometime around October to be bought? We increasingly think so. The option value of cash will increase significantly in the autumn.

“They won. Helped save the United States. I like winners”. Who could have said that?

I have learned that success is to be measured not so much by the position that one has reached in life as by the obstacles which he has had to overcome while trying to succeed. – Booker T. Washington

CARL C. ICAHN

767 Fifth Avenue

New York, NY 10153

The Honorable Donald J. Trump

President of the United States

The White House

1600 Pennsylvania Avenue, N.W.

Washington, DC 20500

Dear Mr. President:

This will confirm our conversation today in which we agreed that I would cease to act as special advisor to the President on issues relating to regulatory reform.

As I discussed with you, I’ve received a number of inquiries over the last month regarding the recent appointment of Neomi Rao as Administrator of the Office of Information and Regulatory Affairs (or “regulatory czar,” as the press has dubbed her) – specifically questions about whether there was any overlap between her formal position and my unofficial role. As I know you are aware, the answer to that question is an unequivocal no, for the simple reason that I had no duties whatsoever.

I never had a formal position with your administration nor a policymaking role. And contrary to the insinuations of a handful of your Democratic critics, I never had access to nonpublic information or profited from my position, nor do I believe that my role presented conflicts of interest. Indeed, out of an abundance of caution, the only issues I ever discussed with you were broad matters of policy affecting the refining industry. I never sought any special benefit for any company with which I have been involved, and have only expressed views that I believed would benefit the refining industry as a whole.

Nevertheless, I chose to end this arrangement (with your blessing) because I did not want partisan bickering about my role to in any way cloud your administration or Ms. Rao’s important work. While I do not know Ms. Rao and played no part in her appointment, I am confident based on what I’ve read of her accomplishments that she is the right person for this important job.

I sincerely regret that because of your extremely busy schedule, as well as my own, I have not had the opportunity to spend nearly as much time as I’d hoped on regulatory issues. I truly appreciate the confidence you have in me and sincerely hope that the limited insights I shared have been helpful to you. I love our country which has allowed me to achieve so much and I thank you for the informal opportunity you have given me to aid it.

Sincerely,

CARL C. ICAHN

Those who think Bannon leaving the White House creates greater domestic political stability maybe should rethink that proposition.

“Steve is now unchained,” said a source close to Bannon. “Fully unchained.”

“He’s going nuclear,” said another friend. “You have no idea. This is gonna be really fucking bad.”

…And last week he told people in a meeting that he would have 10 times more influence outside the White House than inside it.

– The Atlantic

.

We’re baaaccck!.

We warned in our last post before leaving on holiday, “Look for some large sigma event, which is always the case when we are off the desk.” How about a vol spike caused by worries over a nuclear exchange? Nuclear war!

The potential implosion of a presidency?

We think yesterday’s presidential presser has a relatively high probability of being a (or the) structured criticality event that we could look back to as the tipping point that leads to a very volatile autumn.

Structured criticality is a property of complex systems in which small events may trigger larger events due to subtle interdependencies between elements. This often gives rise to a form of stratified chaos where the general behavior of the system can be modeled on one scale while smaller- and larger-scale behaviors remain unpredictable.

For example:

Consider a pile of sand. If you drop one grain of sand on top of this pile every second, the pile will continue to grow in the shape of a cone. The general shape, size, and growth of this cone is fairly easy to model as a function of the rate at which new sand grains are added, the size and shape of the grains, and the number of grains in the pile.

The pile retains its shape because occasionally a new grain of sand will trigger an avalanche which causes some number of grains to slide down the side of the cone into new positions.

These avalanches are chaotic. It is nearly impossible to predict if the next grain of sand will cause an avalanche, where that avalanche will occur on the pile, how many grains of sand will be involved in the event, and so on. – Wikipedia

We love applying the conceptual framework of physics and dynamic systems models to economics and the markets, but think the obssession with the math has perverted the analysis and will someday lead to a doozy of a market meltdown when the algos collide and short circuit on a day to be named later.

In the hypothetical worlds of rational markets, where much of economic theory is set, perhaps. But real-world history tells a different story, of mathematical models masquerading as science and a public eager to buy them, mistaking elegant equations for empirical accuracy.

As an extreme example, take the extraordinary success of Evangeline Adams, a turn-of-the-20th-century astrologer whose clients included the president of Prudential Insurance, two presidents of the New York Stock Exchange, the steel magnate Charles M Schwab, and the banker J P Morgan. To understand why titans of finance would consult Adams about the market, it is essential to recall that astrology used to be a technical discipline, requiring reams of astronomical data and mastery of specialised mathematical formulas. ‘An astrologer’ is, in fact, the Oxford English Dictionary’s second definition of ‘mathematician’. For centuries, mapping stars was the job of mathematicians, a job motivated and funded by the widespread belief that star-maps were good guides to earthly affairs. The best astrology required the best astronomy, and the best astronomy was done by mathematicians – exactly the kind of person whose authority might appeal to bankers and financiers. – Aeon

Hat Tip: Jose Cerritelli

We have have repeatedly warned our readers of potential political instability and to watch “the American street.” See here and here.

Our sense is we are headed for some heated political instability in the United States.

How will it affect the markets?

Depends on trajectory of events, but unless inflation or interest rates spike providing competition for risk assets, don’t expect a bear market to start tomorrow. We have always lived our financial career by Bagehot’s dictum:

“John Bull can stand many things, but he cannot stand

2.0, [-1.5 or 1.25] percent” – Bagehot

We still maintain yield and return chasers will not retreat to their caves, with, the exception of short-term bouts, such as last week, unless policy rates move up another 100-200 basis points and the monetary bases in the G3 shrink by double digit percentage points though quantitative tightening (QT). That is how much liquidity (potential buying firepower) is still in the global system, in our opinion, folks.

What we are looking for?

We still have high conviction the risk markets will experience a swift, short, and steep sell-off in October – 5 to 10 percent – based on:

1) seasonality; 2) the Fed balance sheet should, or could be shrinking ; 3) China’s Party Congress may have concluded, removing the country’s implicit policy put, and thus increasing the risk of a China policy or economic shock; 4) the new U.S. Federal government fiscal year begins October 1 and if the Trump administration has not passed any significant economic legislation, the markets may begin to throw in the towel; 5) there will be more clarity on ECB tapering; 6) even more elevated asset prices as the risk markets grind higher through the rest of summer as we suspect, setting up for a potential blow-off by the end of September; 7) nervousness over the debt ceiling; and, finally, 8) by then, the markets should be sufficiently overbought, overvalued and very vulnerable to event risk. – GMM

Add to that possible key White House resignations.

What do you think the markets will do if Gary Cohn resigns?

That’s at least worth a 5 percent haircut off the S&P500, in our opinion, and a spike to 20 in the VIX, triggering another round of structured criticality.

The exodus of executives sparked talk that Gary Cohn, Trump’s top White House economic adviser and a key liaison to the U.S. business community, might resign in protest as well.

Cohn, who is Jewish, was upset by Trump’s remarks, though he is remaining with the administration for now, sources said. – Reuters, August 16, 2017

Cohn may also come to the conclusion that after the August Congressional recess he is wasting his time as he perceives that the Trump administration has lost all credibility on Capitol Hill and none of his policies has any chance of being implemented. If rumors begin to spread in mid-September, markets will begin to wobble, bigly.

If Chief of Staff, John Kelly, goes? Get shorty, big time.

The 1987 Analog

Since we know crash talk is surely coming, we’ve put together a two-year trading analog of the S&P500 from end of December 1985/2015 to December 1987 and August 16, 2017.

.

First, over the 20-month trading period, the 1987 S&P500 outperformed the current 2017 S&P500 by over 31 percent as of today’s close. Not much of an analog.

Second, the yield on the 2-year increased 287 bps (45 percent) from the beginning of 1987 to the eve of the crash with the 10-year up 252 (33 percent), peaking over 10 percent. The 2-year is up only 13 bps (11 percent) this year with the 10-year down 22 bps (-9 percent).

Third, the 1987 S&P500 peaked on August 25th and banged around until October 5th, where it was only down 2.6 percent from the peak. It then fell 13.6 percent from October 5th to Friday, October 16, the trading eve of the crash. On Black Monday, October 19, 1987, the S&P500 closed down 20.47 percent, almost double the 1929 crash.

Similarly, the 1929 stock market peaked on September 3, 1929 and fell sharply to close down 32 percent on the eve of Black Tuesday, October 29, 1929. That crash sliced 11.7 percent off Dow Jones Industrial in one day. In both cases, 1929 and 1987 the markets sent a loud signal and warning of an imminent crash as, a matter of fact, the markets were crashing before the big crash.

The major difference of the two markets is the Dow didn’t regain the September 3, 1929 peak until November 23, 1954, more than 25 years later. The 1987 S&P500 reclaimed its August 25, 1987 high on July 26, 1989, less than two years. Compliments of easy monetary policy and the circumvention of a great depression.

Upshot?

It’s probably time to buckle up. We expect volatility to begin to pick up; for the markets to start banging around until October; then experience a Tower of Terror sell-off sometime in October.

Though the sell-off may be the day the algos go rogue, there is no doubt, the full firepower of the PPT and the Fed will be put to work. Can they beat this new technology gone wild?

Gotta be quick on the draw as it could be over in the blink of an eye.

Could be wrong. After all, isn’t this astrology, folks?

See you in a week or two. Look for some large sigma event, which is always the case when we are off the desk. I will try to work off the “fat tails’ on holiday.

Have a great holiday, folks!