Do the markets price risk anymore? That it is always inevitable when the world is awash with central bank based liquidity is not a surprise.

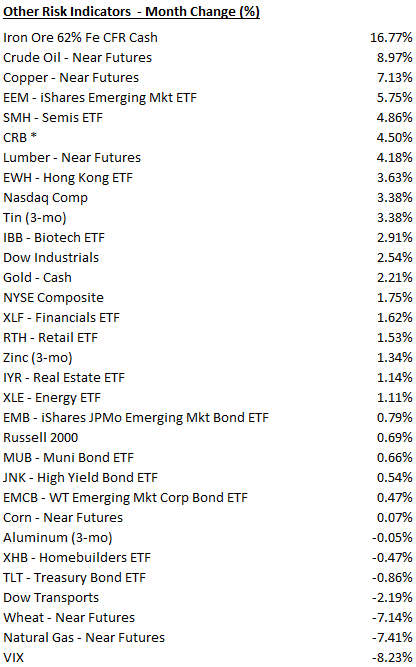

We do see the VIX creeping back over 10 after trading with 8 handle for its only second time in history last Wednesday.

Just as with about everything else, with the exception of crude, which now seems to be pricing in some geopolitical risk, very few markets are pricing for potential political or geopolitical shocks.

See our post, No Worries In South Korean Markets, with their currency and stock market ripping higher this year all while missilies fly up north. The KOSPI did fall almost 2 percent on Friday, however.

Non-worries over a budget debacle are quite understandable, however, since the conflict always seems to work itself out, especially now we have one party rule.

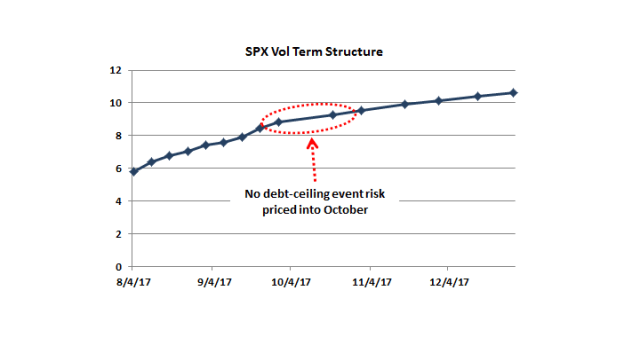

Here is Credit Suisse,

There is “no event risk” currently priced in options that allow investors to hedge against or speculate over potential volatility on the S&P 500, the main US equities barometer, according to Mandy Xu, derivatives strategist at Credit Suisse.

…The tranquility in equities presents something of a juxtaposition to fixed income, where jitters have risen in a portion of the US Treasuries market. – FT

We are expecting several stock negative forces to converge in October, which, we believe, will generate a market sell-off as stocks continue to march higher the rest of the summer adding to their already overextended valuations.

1) seasonality; 2) the Fed balance sheet should, or could be shrinking ; 3) China’s Party Congress may have concluded, removing the country’s implicit policy put, and thus increasing the risk of a China policy or economic shock; 4) the new U.S. Federal government fiscal year begins October 1 and if the Trump administration has not passed any significant economic legislation, the markets may begin to throw in the towel; 5) there will be more clarity on ECB tapering; 6) even more elevated asset prices as the risk markets grind higher through the rest of summer as we suspect, setting up for a potential blow-off by the end of September; 7) nervousness over the debt ceiling; and, finally, 8) by then, the souffle now being baked and puffed up by the markets should barely be able to withstand the slamming of the oven door. – GMM

Stay tuned.