Click on table to enlarge and for better resolution

Click on table to enlarge and for better resolution

The May Crude Oil futures contract has regained its 200-day moving average in overnight trading. Significant.

Crude is lifting on the back of a bigger than expected draw as measured by the API. Specs have also reduced their net long positions after last month’s big plunge in oil prices. Let’s see if the API data are confirmed by the EIA tomorrow.

The question is looking at the chart is this a move back to the $52-55 trading a range? Or the build of the right shoulder of an H&S pattern? Or neither? Tell us and we will buy a yacht together.

We received some interesting pushback on our recent post, Is the U.S. Government Bankrupt? Not Even Close.

The purpose of the post was to remind readers to not ignore the left side of a government’s balance sheet — assets — and only focus on its liabilities. We quoted President Trump on how he is kicking around ideas about selling some of the federal government’s assets to reduce the national debt.

Readers wrote in — some nasty, probably because we didn’t affirm their doom and gloom views — saying this was not politically feasible and would never happen. We agree on the difficulty of such a policy being implemented. It is not easy for a sovereign, due to domestic politics and even legal issues, to sell assets to pay off its creditors.

Much of our career focused on sovereign debt and working on and working out such issues.

Debt-for-Equity Swaps

During the 1980’s LDC debt crisis, however, there were mechanisms set up to allow the creditors of a sovereign borrowing to swap their debt holdings for equity in, say, a state-owned company. There were many cases of these debt-for-equity swaps. They were not perfect solutions and without problems, but they did exist.

Even now, in Greece, for example, the country’s external creditors always insist on the government pursuing the privatization of state assets with programs negotiated directly into the country’s bailout packages. Greece usually misses the targets and drags its feet on implementation. Imagine, if you will, the domestic political blowback to a government of, say, selling off the Parthenon to pay back German and EU creditors. Yikes!

Sovereign Risk and Debt Crises

But that post is history. We really want to focus on the concept of sovereign risk and debt crises in this post. Why is it that sometimes highly indebted countries experience runs on their currency or can’t roll over their debt? These are complicated issues and should be analyzed case-by-case. But, for this post, we will speak in wide-reaching generalities.

Local Currency vs Foreign Currency

First, it is important to distinguish the difference of a local currency or foreign currency debt problem. As long as the government has an independent central bank, the local currency debt problem can be monetized, which, if happens during a rollover crisis, usually results in hyperinflation and the collapse of the exchange rate. See Bulgaria in the mid-1990’s.

Rarely does a reserve country experience rollover risk, especially since the introduction of mass quantitative easing (QE). We were moving close in the Eurozone in 2011, however, as European financial system was on the brink. Super Mario to the rescue.

We do think that the next major global financial crisis, which a major stock market correction/bear market is not, will be a major industrialized country entering into a period of high rollover risk. That is when we must worry the House of Debt comes tumbling down.

Monetize or Default?

Many now believe that a sovereign borrower with an independent central bank can’t default on its local currency obligations. That the markets will never question its ability to pay.

We disagree, however, as Russia did and defaulted on local currency debt in 1998. In this sort of crisis, where a country falls into the trap where it can’t roll its maturing debt, it comes down to a political decision and who is going to take the pain.

Monetize the debt and the resulting hyperinflation hurts the local population. Default and restructuring the local currency debt hurts the country’s creditors. In Russia’s case, many of the creditors were foreigners, such as hedge funds. Enter the political calculus. Note Russia also devalued the rubble simultaneously with the decision to default, which further hurt its local currency creditors.

Foreign Currency Debt

Most of the recent debt crises — 1980’s LDC Debt, Mexico Peso Crisis (a little more complicated), and the 1997 Asian Financial Crisis – involved transfer risk. This occurs when the debt is denominated in foreign hard currency and the central bank runs out of FX reserves or they fall below a critical level. Even though local currency is available for payment, there are not enough hard currency reserves to convert the local currency thus debt service is disrupted.

Major Reasons for Sudden Stops

Why is it a country gets itself into a debt crisis as the market cuts them off from financing resulting in the sudden stop of capital flows?

We are going to speak into generic terms that can apply to both local and foreign currency debt crises and briefly focus on four major flaws in the structure of the global financial system that contribute to sudden stops and debt crises.

Upshot. Other than Venezuela (Puerto Rico doesn’t count) and some upcoming noise over raising the debt ceiling in the U.S. there doesn’t seem to be much risk of a major sovereign debtor getting into trouble in the near-term, though some smaller countries are defaulting on their external debt. QE and the threat of QE have changed much in the discipline.

Maybe a credit crisis and accelerated capital flight in China could morph into a crisis, but we are too far from that and have not looked at it closely enough.

A geopolitical event could trigger a sovereign crisis somewhere in the world.

An unexpected political event could trigger a crisis.

A sudden loss of confidence in the Japanese bond market, where the debt ratios are off the charts? The Bank of Japan owns almost half of the JGBS outstanding. And will buy more. In our opinion, there is a greater risk of a currency crisis in Japan than a bond market crisis, but we could be wrong.

A rapid rise in inflation could trigger a sovereign crisis if bonds are allowed to price it in and we enter into a feedback loop of higher deficits, due to higher interest payments, and higher interest rates due to higher deficits. Keep it in mind, but currently not on radar.

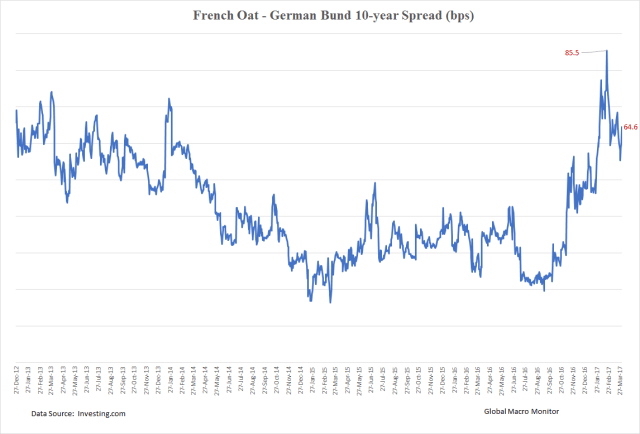

President Marine Le Pen? Bingo!

Existential crisis in Europe would trigger a massive blowout of credit spreads and sovereign CDS. Low probability, but high impact event.

We would be buying any panic unless polling changes dramatically, which now puts Macron up around 30 points in the second round. The polls in Brexit and the Trump victories were much closer if not spot on in the last few days. A 30 point lead is a yuuuge and unlikely poling mistake. Buying panic is easier said than done, however, as the changing polls would be why the panic would ensue.

A lot of French voters are still undecided and upset. Who knows what they will do in the privacy of the polling both. Launch the “Molotov” cocktail as the Americans did? Stay tuned.

The spread widened by about 5 bps this past week. Macron still holds a slight lead in first round polling over Le Pen. France’s Polling Commission of false reports by Russian news agencies,

France’s polling watchdog has issued a warning over what it says is a misleading Russian news report claiming that François Fillon, the scandal-struck conservative candidate, has regained the lead in the presidential race.

The Polling Commission criticised a French-language report by Sputnik, a state-run Russian news agency, for presenting a social media survey by Brand Analytics, a Moscow-based online research firm, as a “poll” showing Mr Fillon as the front runner.

In fact, French opinion polls, which are strictly supervised by the authorities, show Mr Macron leading on about 26 per cent, with Marine Le Pen, the Front National leader, one point behind. – Telegraph

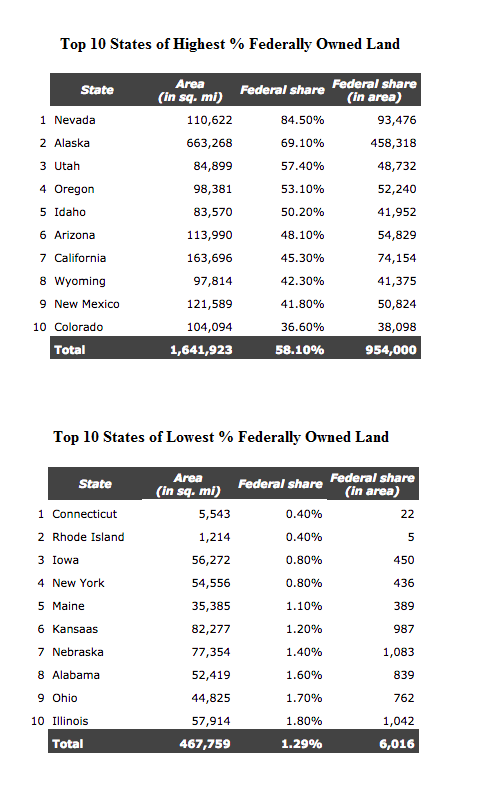

Click on table to enlarge and for better resolution

Nice follow-up quote from our last post on federal land holdings and assets. U.S. government praying for a land bubble? Just yanking your Markov chain.

At the peak of the real estate bubble in the late 1980s, the 1.32 square mile of Imperial Palace grounds in the center of Tokyo was said to be worth more than all the real estate in California. – CNBC

(QOTD = Quote of the Day)

We often hear the meme “the U.S. is the next Greece.” “The government is insolvent.” Complete nonsense.

We tend to focus too much on the right side of the government’s balance sheet and not the left side — the federal government’s assets. This is not to downplay the seriousness of the debt issues – current, future, and off-balance sheet obligations – and the need for a long-term viable debt solution.

Just take a look at the chart and tables below, however, which we snagged from the Big Think, of how much land the federal government owns, especially in the west. Almost half of the land in California and more than 80 percent of Nevada. Stunning.

Then there are the mineral rights. Time magazine cites an International for Energy Research report that the U.S. government owns,

Oil and gas resources on and offshore worth $128 trillion

That is several multiples of the current national debt.

President Trump has even mentioned selling off the government assets to reduce debt. Marketwatch recently reported,

Which brings us to one of the president’s more intriguing ideas: why not sell off some of those rights and pay down part of the debt?

Candidate Trump sold this in his usual simplistic terms: I’m a real estate guy, I know how to make the deals. We pay down the debt while putting Americans back to work in the oil and gas industry. We become energy independent and screw the Middle East. What’s not to like? – Marketwatch

We did get some pushback on the feasibility of selling federal land and real assets as it is a very difficult political proposition. But that is not the point of this post. The markets implicitly understand the strength of U.S. G’s balance sheet, say, relative to Greece, for example.

What a great Ph.D. dissertation topic — measuring the U.S. government’s net worth by calculating the market value of all its assets.

Look no further than the latest Flow of Funds data from the Federal Reserve Board to get a snapshot of what’s happened in the U.S. economy during the new millennium.

Because “credit is the mother’s milk of the economy” let’s focus on debt growth by each sector.

…credit is the mother’s milk of growth; without credit the economy cannot flourish. And credit cannot flow freely without a well-functioning financial system. – Mark Zandi

Reagan Keynesian Recovery

But, first, take a look at the credit binge during the Reagan expansion of the 1980’s. Double digit debt growth from 1982, when the economy began to emerge from a deep recession to 1986. Almost all sectors experienced rapid credit growth during this period.

Not to downplay the supply-side structural reform under Reagan, which we always support, but it sure looks like his economy was a classic debt-fueled Keynesian expansion. The data are undeniable.

An Aside: IMF and World Bank

Comprehensive economic policy during an economic crisis, either hyperinflation or a depression/deep recession, for example, consists of both stabilization and structural reform.

Traditionally, in emerging markets, the International Monetary Fund (IMF) is charged with stabilizing a country during an economic crisis through various macroeconomic policies, both fiscal and monetary. The World Bank then moves in with structural adjustment and reform policies and financing to “fix” the economy.

At least, that was the case when we were there in the mid-1980’s. Note, we worked at the World Bank in the mid-1980’s on Chile’s first structural adjustment loans. Add that to our work on Poland and we are proud to say we helped reform two of the best performing emerging market economies over the last 30 years. Economic superstars!

That’s our epithet.

W Bush’s Economy

Starting in 2000 notice the rapid expansion of mortgage debt, double digit growth from 2000 to 2006. This fueled the housing bubble and the use of home equity to finance consumption. Home equity as an ATM stimulated aggregate demand. The housing/credit bubble was instrumental helping the economy emerge from and avert a very severe recession brought on by the crash of the stock market, which began in early 2000. One bubble replaced by another more onerous, dangerous and debilitating housing/credit bubble.

The Great Recession

Notice, the collapse in household debt growth in 2008. The deleveraging of the consumer and business sector, coupled with state and local governments, led to a severe downturn in domestic demand and resulted in the great recession.

The federal government did exactly would it should do during a deep recession through a debt-fueled fiscal expansion. Annual debt growth of the federal government exceeded or came close to 20 percent from 2008-2010. The alternative do-nothing policy was a Great, Great, Great Depression. We can’t emphasize enough the word Great.

Yes, but debt rose several trillion dollars under Obama? Yadda, yadda, yadda!

Don’t get us wrong, we are the first to say, or scream, that the country needs a long-term structural plan to deal with our national and private debt obligations. Economic stimulus should be temporary and used only during downturns. Simpson-Bowles, anyone?

We give an A plus to the Obama policymakers for averting a catastrophic global depression. There is no doubt, at least in our minds, if not for their and the Fed’s bold stabilization policies, all of us would be living under martial law and probably under a freeway eating bark. Counterfactuals can’t be proven, but this, we are pretty certain.

President Obama, not so good on structural reform, however. Could have been better and probably constrained by the “do-nothing, obstructionist Congress.”

Enter Trump

The markets have high hopes for the Trump Administration introducing and implementing vast structural reforms in the economy. The new president inherits a relatively strong economy and won’t be distracted and busy trying to stabilize a collapsing economy as President Obama was at the beginning of his Administration.

This should allow him to focus on the needed reforms to get the economy back to a higher growth trajectory, especially given he has a ruling majority in Congress. No excuses.

Here’s to hoping they are the right policies.

The Administration can start by jettisoning the disastrous Border Adjustment Tax (BAT) idea, which will severely hurt President Trump base voters through higher inflation and job layoffs in our WalMart nation, in order to finance tax cuts for higher income earnings. Economic and political nonsense, in our opinion.

We are rooting for you, Gary Cohn.

The FT’s Neil Hume speaks to Jeremy Weir, chief executive of Trafigura – one of the world’s biggest oil traders – about the outlook for the market and the price of oil.

► Subscribe to the Financial Times on YouTube: http://bit.ly/FTimeSubs