“Here it comes. Oh my goodness. In your life have you seen anything like that?” — Vern Lundquist, 2005 Masters

“Here it comes. Oh my goodness. In your life have you seen anything like that?” — Vern Lundquist, 2005 Masters

BFTP: Blast From The Past

Answer to yesterday’s Masters quiz question:

Anthony Kim posted 11 birdies in the second round of the 2009 Masters.

German WWII POWs

Here’s some more 19th hole fodder to impress your buddies and something I bet you didn’t know about Augusta:

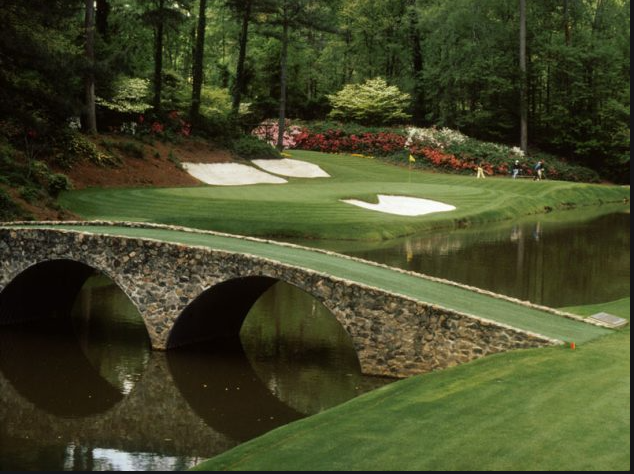

German POWs from nearby Camp Gordon built the bridge over Rae’s Creek next to the 13th tee box during WWII. They were part of Rommel’s Panzer division in North Africa responsible for building bridges to enable tanks to cross rivers.

While Augusta National is famed for its almost unnaturally beautiful flora, as it turns out some rather interesting fauna once called the course home as well: 200 heads of cattle and more than 1,400 turkeys. From 1943 until late 1944, Augusta National was closed for play and transformed into a farm of sorts to help support the war effort. Some of the turkeys were given to club members during Christmas (meat rations were in effect) while the rest were sold to local residents to help fund the club. And the cows? Well, they acted as natural lawnmowers but also inflicted quite a bit of damage to Augusta National, devouring many of the course’s famed plants and shrubs.

To help repair cattle-related damage and revive Augusta National for its reopening, 42 German prisoners of war from nearby Camp Gordon were shuttled back and forth to work on the course.

Writes John Strege in “When War Played Through: Golf During World War II:”

“The POWs had been with the engineering crew serving Rommel, the Desert Fox, in North Africa, part of the Panzer division responsible for building bridges that enabled German tanks to cross rivers. It was a useful skill for the renovation work to be done at Augusta National. The Germans were asked to erect a bridge over Rae’s Creek adjacent to the tee box at the thirteenth hole.”

The Masters resumed at Augusta National — now free of German prisoners and barnyard animals — in 1946. And interestingly enough, the Supreme Commander of the Allied Forces in Europe during World War II, Dwight D. Eisenhower, later became a member of Augusta National. Two Augusta National landmarks bearing Eisenhower’s name still stand today: the Eisenhower Tree (a loblolly pine at the 17th hole that the former president and avid golfer repeatedly struck with golf balls and requested be cut down; photo above) and the Eisenhower Cabin (built in the 1950s according to Secret Service security guidelines by the club for the former president’s visits).

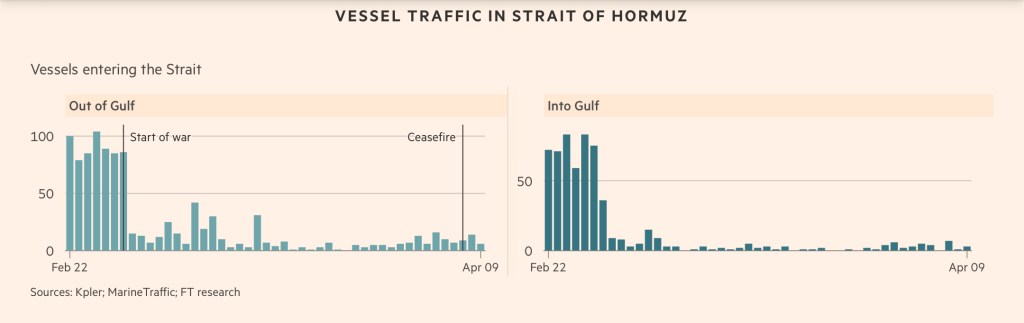

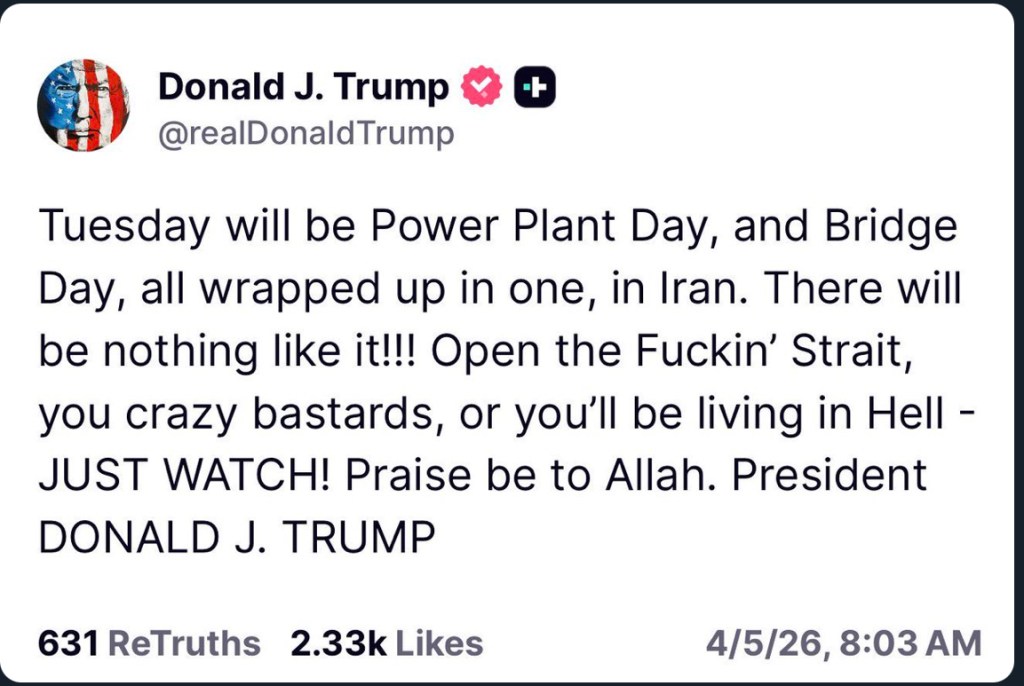

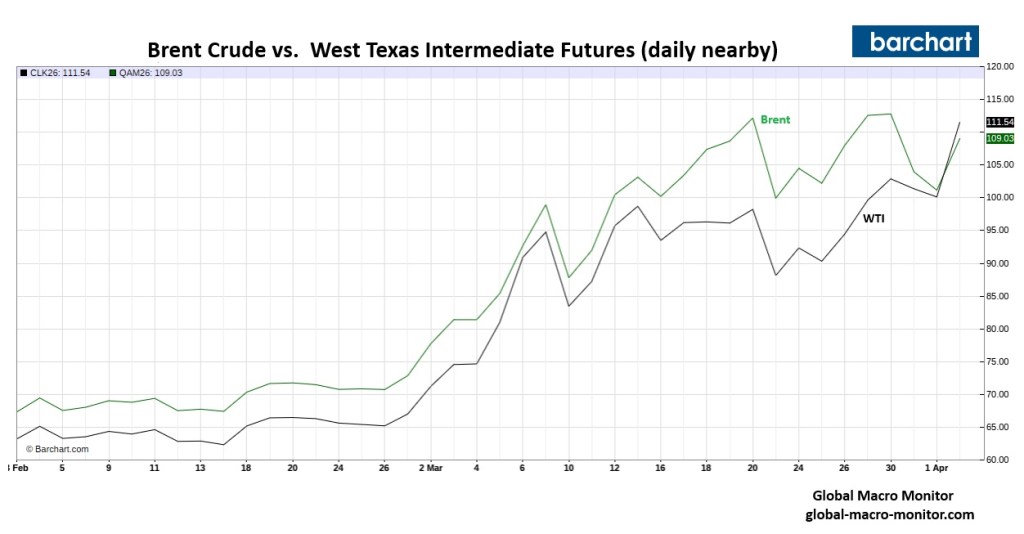

The oil market just delivered one of those “stop what you’re doing” moments: U.S. benchmark WTI trading at a premium to Brent. That’s not just unusual, it’s a signal flare for acute market dislocation.

What Happened (and Why It Matters)

OilPrice.com highlights a rare inversion where WTI surged above Brent, flipping a long-standing global pricing hierarchy. Traditionally, Brent commands a premium given its role as the seaborne global benchmark. When that relationship breaks, something is fundamentally wrong in the plumbing of the oil market.

The driver? Immediate supply scarcity, localized, acute, and geopolitical.

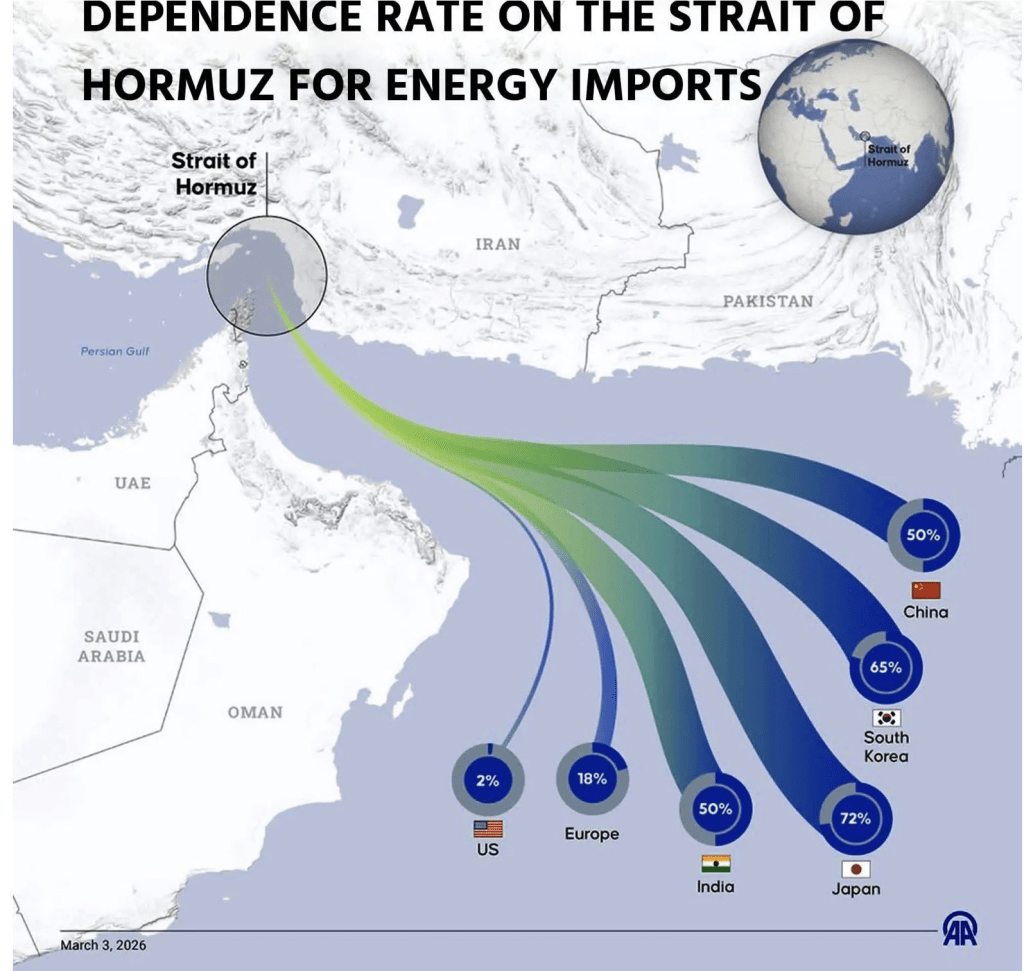

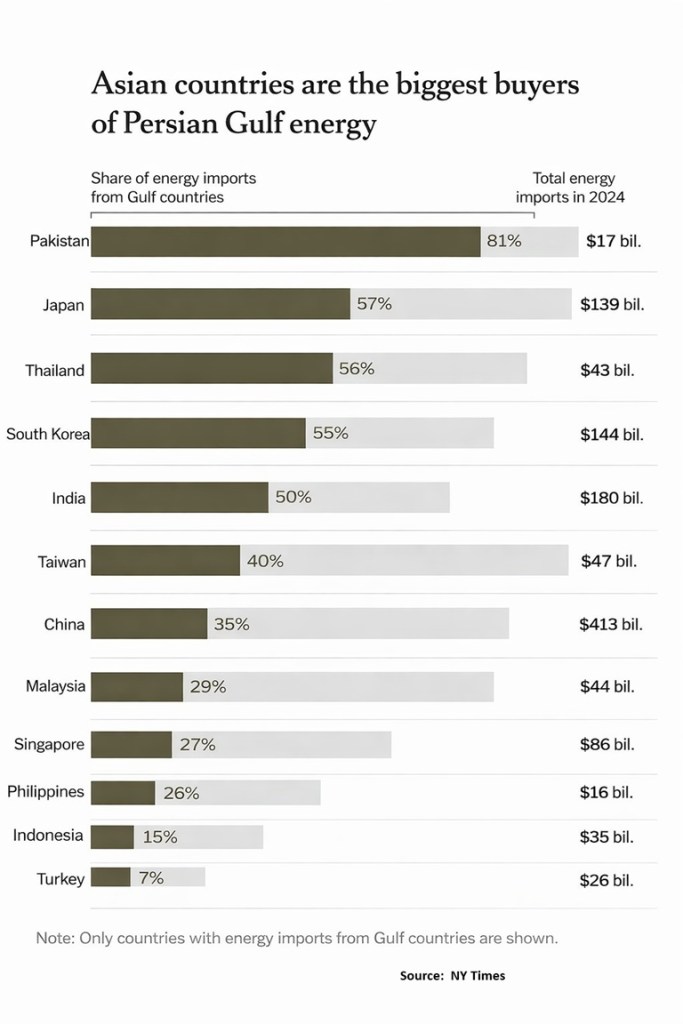

Recent developments—particularly escalating tensions involving Iran and disruptions to the Strait of Hormuz—have choked off a meaningful portion of globally traded crude. Markets are now pricing availability, not just fundamentals.

WTI’s premium is less about U.S. oil being “better” and more about it being accessible. Domestic barrels, sitting in Cushing or flowing through U.S. infrastructure, suddenly look like the cleanest shirt in a very dirty laundry basket.

Microstructure > Macro (For Now)

A key nuance emphasized in the article—and corroborated by broader market commentary—is that this inversion is partly technical:

In a market gripped by backwardation, front-month barrels command a premium. Traders are paying up for immediacy.

But don’t dismiss this as just calendar spread noise. The magnitude of the move signals something deeper:

The market is pricing physical scarcity today, not theoretical abundance tomorrow.

The Bigger Picture: A Supply Shock, Not a Demand Story

Let’s be clear—this is not 2008-style demand exuberance. This is a supply shock with geopolitical teeth:

In other words: this is a multi-node disruption across the global energy network.

The result? Oil prices have surged over 50% in a month, with WTI pushing into the $110+ range intraday.

Market Implications for Portfolio Managers

1. Inflation Is Back (and It’s Sticky)

Energy is once again the marginal driver of CPI. This isn’t transitory—it’s structural while geopolitical risk persists.

2. Term Structure Is the Trade

Backwardation is screaming tightness. Front-end crude, refined products, and crack spreads are where the action is.

3. U.S. Energy Assets Gain Strategic Premium

Domestic producers and midstream players are suddenly geopolitical hedges. The U.S. is becoming a relative safe haven in oil supply.

4. Tail Risks Are Fat and Getting Fatter

Options markets are now pricing scenarios north of $150 crude if disruptions persist.

The Global Macro Monitor Take

This isn’t just an oil rally, it’s a regime shift in pricing power.

When WTI trades above Brent, the market is telling you one thing loud and clear:

“I don’t care about benchmarks, I care about barrels I can actually get.”

In that world, liquidity fragments, correlations break, and macro models built on stable relationships start to wobble.

The playbook here isn’t about forecasting demand curves, it’s about mapping geopolitical risk onto physical supply chains.

Welcome to oil markets where geography Trumps economics.

Global markets are no longer simply trending lower, they are fracturing under policy uncertainty and headline-driven volatility. The U.S. market has suffered its fifth consecutive weekly decline in major U.S. indices, with the S&P 500 down ~7% YTD and the Nasdaq entering correction territory. Yet what stands out is not the direction, but the erratic path: sharp rallies repeatedly reversed by conflicting geopolitical signals.

Bond markets reinforce this instability. A global rout has pushed yields sharply higher (U.S. +50 bps, UK +70 bps, Italy +80 bps), while rate expectations have flipped from cuts to a non-trivial rate hikes. This is a classic late-cycle stress signal: tightening financial conditions colliding with weakening growth.

The VIX above 30 confirms that volatility is no longer episode, it is systemic.

Trump as Market Catalyst-in-Chief

Markets are now trading less on fundamentals and more on Trump’s signaling function. His pattern of announcing delays, pauses, or escalations in the Iran conflict has created a reflexive loop:

This is not random. His messaging appears intentionally calibrated to arrest market declines, particularly given his long-standing tendency to equate equity performance with political success.

However, this strategy is backfiring. Markets are now delivering a “blunt rebuke,” with investors increasingly doubting his ability to resolve the conflict . The result: policy communication is losing its marginal impact, requiring ever more dramatic interventions to stabilize sentiment.

Insider Trading Concerns: Structural Erosion of Trust

There is a far more troubling dynamic: systematic suspicious trading preceding major announcements.

Key examples include:

While direct culpability is unproven, the pattern is persistent and statistically improbable. More critically, institutional safeguards have weakened: enforcement actions have been reduced, and regulatory oversight diluted .

For markets, perception is reality. The implication is profound: price discovery is increasingly viewed as compromised.

Personal Trading Impact: A Case Study in Policy Risk

Last Monday provided a textbook example of this dysfunction.

Positioned short into what appeared to be a technically confirmed breakdown, I was caught offside by a Trump tweet signaling a delay in Iranian strikes. The market ripped 105 S&P points beyond my stop, resulting in a $4,000 loss.

This was not a failure of analysis—it was a failure of predictability.

The consequence has been behavioral:

Ironically, this caution led to missed profits later in the week, as the market resumed its downward trajectory. This is the hidden cost of policy-driven volatility: it suppresses risk-taking even when setups are correct.

War on Short Sellers: Liquidity Implications

Trump’s increasingly hostile rhetoric toward short sellers is another destabilizing force. By framing them as adversarial actors, policy risk is being selectively applied to one side of the market.

This has three implications:

Markets require shorts—not just for price discovery, but for buy-side support during declines (short covering). If this cohort withdraws, rallies become shallower and less durable.

The logical outcome:

Expect weak, at, best low-conviction rallies in the near term.

Regional Performance

United States

Europe

Asia

Emerging Markets & LatAm

Structural Outperformance (Prototype Insight)

Asia—particularly Korea and Taiwan—remains a structural outperformer, driven by AI capital flows and global manufacturing dominance . However, even these markets are not immune to global liquidity tightening.

Week Ahead: Fragility with Event-Driven Upside Risk

The market enters next week in a technically oversold but fundamentally unstable position.

Key Catalysts:

Base Case:

Tail Risk (Upside):

A credible ceasefire announcement could trigger a violent short-covering rally, given oversold conditions and elevated cash levels.

Bottom Line

Markets are no longer governed by traditional macro inputs—they are being distorted by political signaling, eroding institutional trust, and asymmetric policy risk.

In this environment, the correct strategy is not prediction—but survival and optionality.

Or put differently: This is no longer a trader’s market. It’s a headline battlefield.

The S&P 500 closed at the lower end of its multi-month trading range, a band that has effectively contained price action since September. That alone raises the obvious question: is this a breakdown, or just another shakeout within a range-bound market?

From a positioning standpoint, there’s a sense that short interest is crowded but cautious. The market doesn’t feel like it’s in a panic unwind phase yet, it feels tense, however. That distinction matters. True breakdowns tend to come from complacency, not from markets already leaning defensive.

Overnight futures appear to be pricing in a de-escalation scenario tied to Iran and U.S. pressure, specifically expectations around compliance with Trump’s short-term ultimatum related to the Strait of Hormuz.

That assumption looks fragile at best.

If anything, the market may be:

In other words, futures (as of 7 pm Eastern) are leaning optimistic into an uncertain geopolitical setup—a classic setup for volatility if reality diverges from expectations.