Must view, folks.

Must view, folks.

A new Stanford University and World Bank survey (December 2024, 4,278 U.S. adults) reveals just how transformative generative AI has become in everyday work. Researchers compared the average time to complete 18 common tasks with and without AI tools, and the results are striking: across the board, AI reduced task times by at least 60%.

The biggest gains appeared in troubleshooting, where AI cut the average time by 76%. Technical fields also benefited heavily—programming and technology design were completed dramatically faster, while analytical challenges such as critical thinking and mathematics saw sharp efficiency boosts.

On the creative side, writing tasks dropped from 80 minutes without AI to just 25 minutes with it—the lowest completion time across all categories. Even work typically seen as “human-centered,” like judgment, personnel management, and instructing, showed at least 65% productivity improvements.

The message is clear: generative AI isn’t only about speeding up coding or content creation. It’s reshaping how we approach both technical and interpersonal tasks, freeing time for higher-order thinking and strategy. As organizations continue integrating these tools, the productivity frontier is shifting—and the future of work is arriving faster than most expected.

When Sam speaks, you’d better listen. “Kernel of truth” equals ambiguity of value in our book.

BTW, you heard it here first in last night’s post. Caveat emptor, Comrades.

…market observers are increasingly uneasy about stretched valuations. Equity prices have surged on the back of lower risk premiums and abundant liquidity, but profit growth has not always kept pace. This creates a situation analogous to driving a vehicle with a low fuel tank: while the road ahead may appear clear, no one knows exactly when and where the car will run out of gas or err…charge. – GMM

Nothing is more fun than “picking up nickels in front of a steamroller,” right?.

Must view video, folks. May be the most important 4 1/2 minutes of your life!

“AI is most likely both a bubble and eventually going to be the most important technology of the 21st century.”

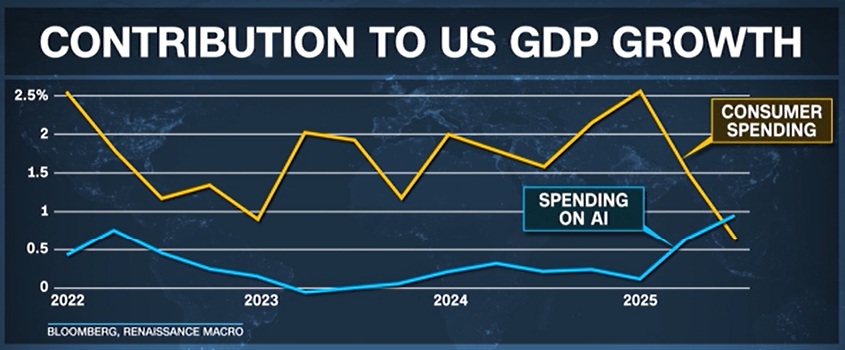

The biggest hyper scalers…the big tech companies, like Meta and Microsoft are spending hundreds of billions of dollars, maybe up to $400 billion this year, on the infrastructure to build Artificial Intelligence…Last quarter, spending on Artificial Intelligence added more to GDP than total consumer spending…That statistic is completely crazy, consumer spending is 70 percent of the economy. — Dereck Thompson

Click here to view the excellent video

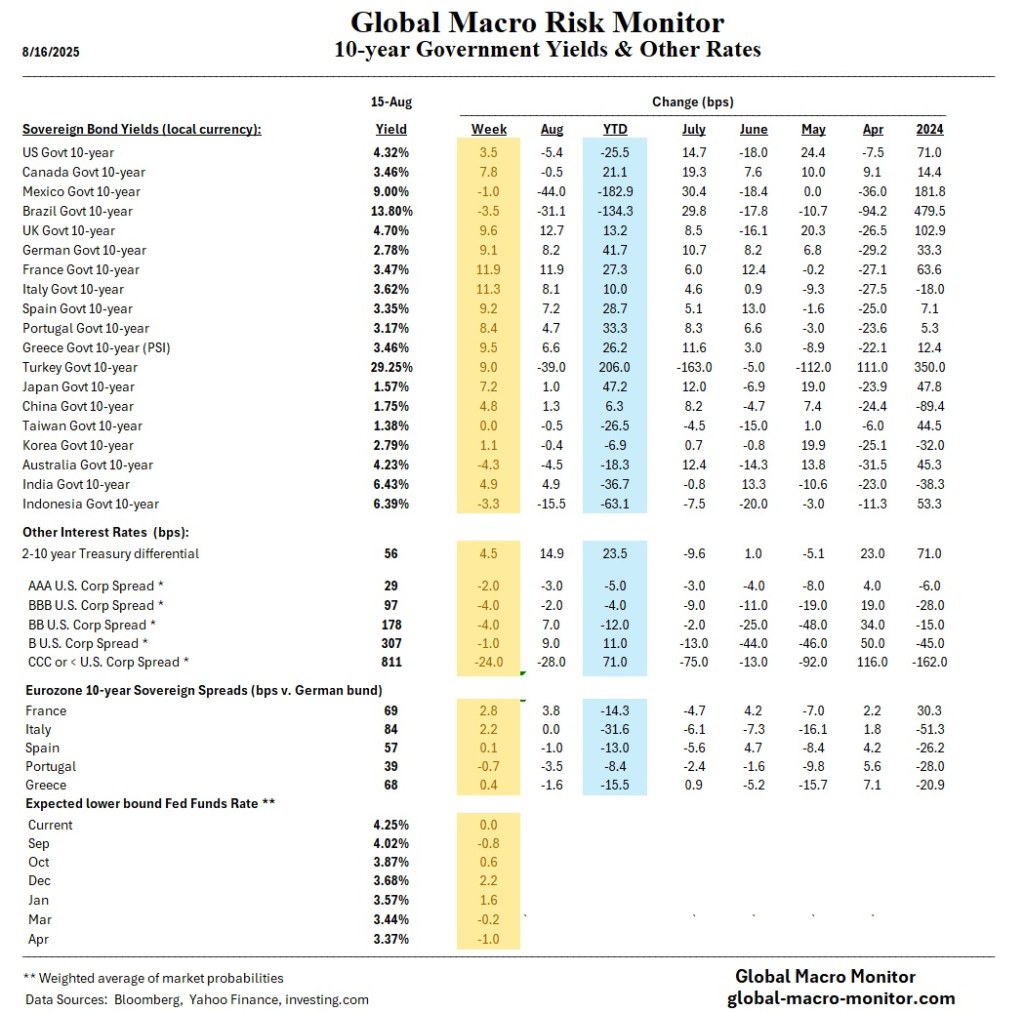

Investor appetite for risk continues to surge as U.S. corporate credit spreads tighten to levels not seen in nearly three decades. Investment-grade spreads have narrowed to just 88 basis points, the tightest since 1997, according to Bloomberg. A parallel trend is evident in emerging markets, where the spread on corporate bonds has fallen to just 200 basis points—a 20-year low. The abundance of liquidity and the absence of default concerns have driven demand for credit, thus suppressing required risk premiums.

This compression of credit spreads is also impacting the equity risk premium—the extra return investors demand for holding stocks over risk-free assets. As credit markets send signals of reduced financial stress, equities have become relatively more attractive. Lower discount rates are supporting higher equity valuations, with major indices such as the S&P 500 hitting new all-time highs. Investors are increasingly tolerating richer valuations in search of returns, a dynamic fueling continued stock market gains.

Regional Economic Insights

Europe is treading water economically, with inflation near target but growth continuing to stagnate. The ECB remains on watch as disinflationary forces persist. Japan, meanwhile, could see a modest rate hike in October, but with consumer demand soft and inflation subdued, policy normalization is expected to proceed slowly. Equity markets there have attracted some capital due to corporate reforms and yen weakness.

China’s economy remains under pressure, with weakening consumer confidence and ongoing stress in the housing market. While policymakers have introduced targeted easing, industrial production and retail sales data disappointed, reinforcing concerns over long-term structural headwinds.

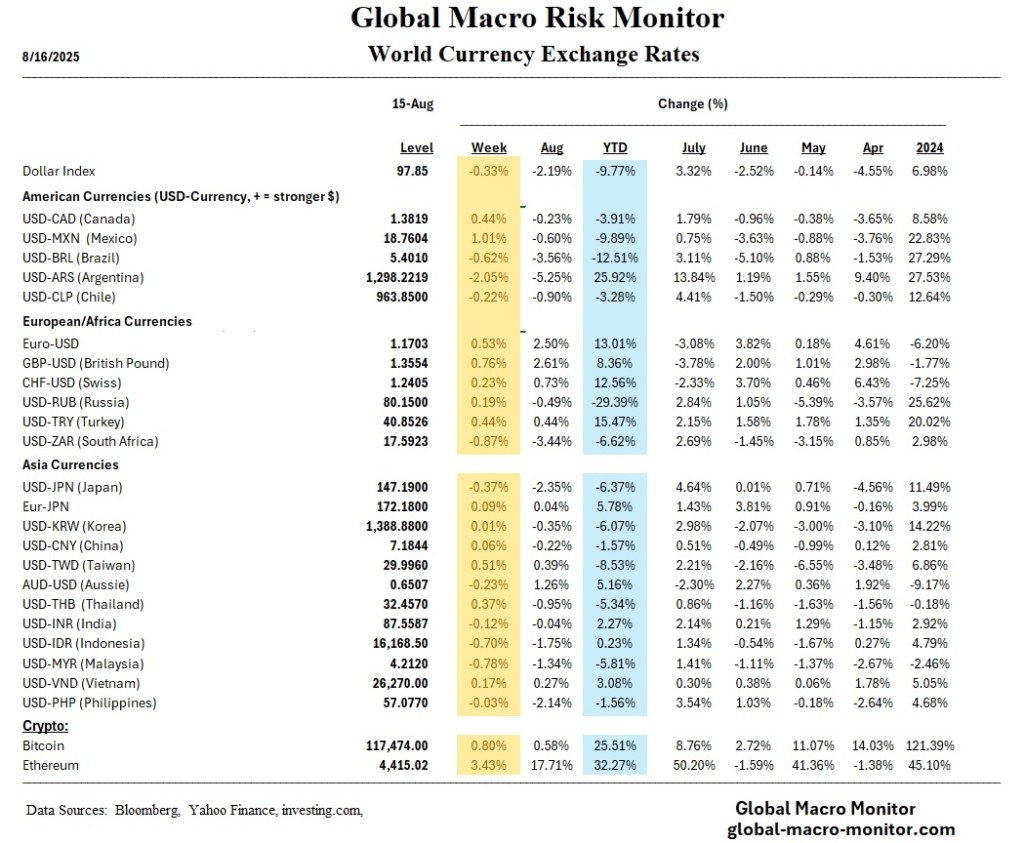

Mexico, in contrast, is one of the more robust emerging markets. Strong remittances, prudent fiscal policy, and positive terms of trade have attracted foreign capital inflows. The Mexican peso remains a top performer, buoyed by confidence in macroeconomic stability and nearshoring trends.

Inflation: CPI-PPI Divergence

U.S. inflation data delivered a mixed message last week. The Consumer Price Index (CPI) came in below expectations, reinforcing optimism about cooling inflation. In contrast, the Producer Price Index (PPI) rose more than anticipated, suggesting sticky wholesale input costs. This divergence has not derailed expectations for a Fed rate cut in September, but it does introduce uncertainty regarding the durability of disinflation trends.

Valuations and the “Low Fuel Tank” Risk

Despite the bullish backdrop, market observers are increasingly uneasy about stretched valuations. Equity prices have surged on the back of lower risk premiums and abundant liquidity, but profit growth has not always kept pace. This creates a situation analogous to driving a vehicle with a low fuel tank: while the road ahead may appear clear, no one knows exactly when and where the car will run out of gas or err…charge.

Markets can continue to climb for some time, supported by technical momentum and investor optimism. However, just like a car running on fumes, the current rally may face sudden exhaustion, whether triggered by an unexpected inflation shock, earnings miss, or geopolitical blow-up. Investors are advised to monitor underlying fundamentals closely, particularly as valuations rise to levels that price in very optimistic assumptions.

MARKETS

Key Themes

UNITED STATES

Economy

EUROZONE

Macro Conditions

UNITED KINGDOM

Labor and Growth Trends

JAPAN

Policy Outlook

CHINA

Growth and Structural Challenges

EMERGING MARKETS

Capital Markets

RISKS AND OUTLOOK

Valuation Warning

Cautionary Note: Market conditions resemble driving with a nearly empty gas tank where momentum can carry the rally further, but without a clear catalyst or refueling (e.g., earnings upgrades, growth acceleration), a stall could be sudden and sharp.

Geopolitical and Policy Risks

Week Ahead: August 19–23, 2025

Economic Data Releases

United States

Euro Area

Japan

China

Central Bank Actions

U.S. Federal Reserve

European Central Bank (ECB)

Bank of Japan (BoJ)

Earnings Reports

U.S.

Europe

Asia

Key Themes to Watch

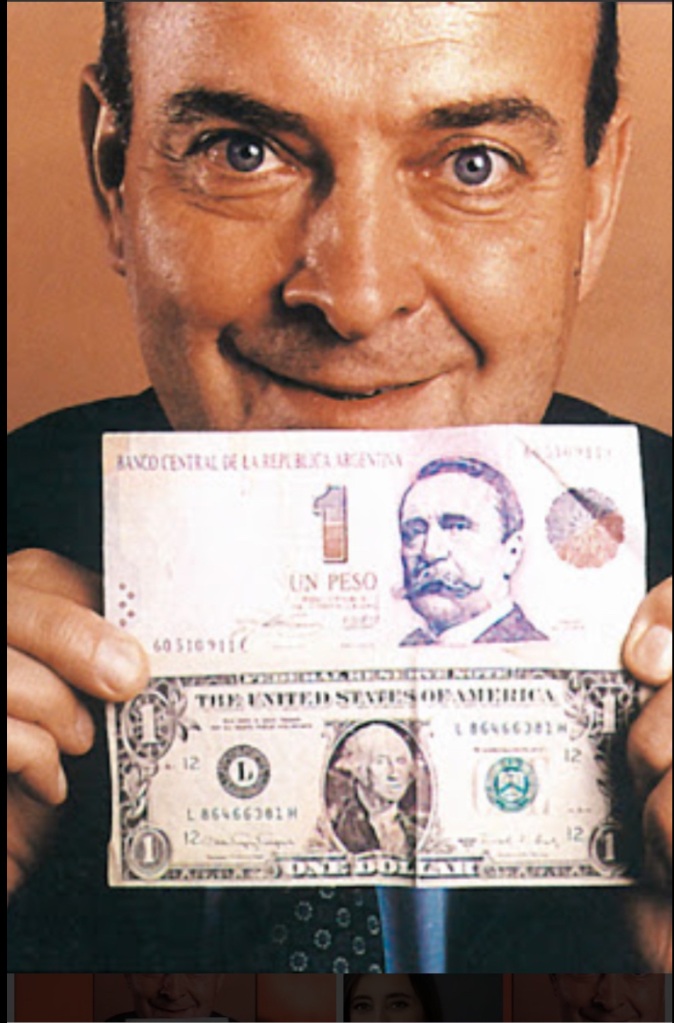

Today’s Drudge Report headline, with George Washington staring from a dollar bill under the headline “NATL DEBT $37 TRILLION” and accusations of falsified inflation data, encapsulates the growing perception that America’s fiscal and political trajectory is veering toward Banana Republic territory. As both a political analyst and an economist who worked in Argentina during its catastrophic hyperinflation of the late 1980s, I find the parallels increasingly unsettling.

Key Economic Indicators

The United States is experiencing a dangerous cocktail: record-high national debt; persistently large fiscal deficits; protectionist trade policies; official economic statistics under attack, and the risk of being manipulated by the government; creeping autocracy and authoritarianism; and equity markets at euphoric highs. The S&P 500’s surge masks a hollow core — real wage stagnation, eroded purchasing power, and an over-reliance on debt-financed consumption. The slow erosion of trust in official inflation data compounds the problem; when investors, households, and global creditors doubt government numbers, policy credibility collapses.

Historical Comparison: Argentina’s Warning

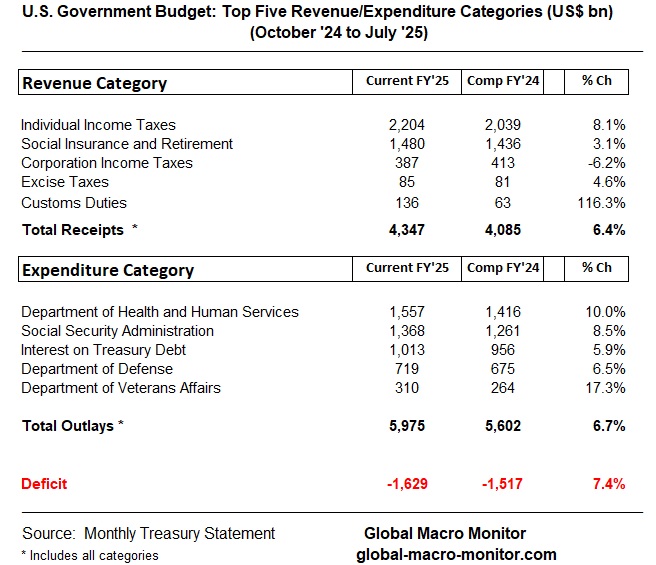

In Argentina, I watched the population sleepwalk into financial ruin, lulled by artificially low inflation figures, fiscal policy that relied too much on boosting revenues rather than controlling spending, the lack of an independent central bank, huge wealth and income inequalities, and massive capital flight. Though the U.S. and Argentina economies are vastly different, some similarities we see in the U.S. today are ominous. Once objective data is politicized, the ability to correct course without severe social pain vanishes. Moreover, the hoopla over tariff revenues as the fiscal savior is just that – hoopla. As the table illustrates below, customs duties only account for 3 percent (albeit growing) of the U.S. government budget receipts.

Future Outlook

If the U.S. continues this trajectory—i.e, rejecting credible statistics, pressuring companies to sideline dissenting economists, and relying on market highs to reassure the public—it risks a future where reality intrudes suddenly and brutally. We may awaken to an economy impaired not by external shocks, but by our own self-inflicted distortions. The lesson from Argentina is clear: complacency is not a cushion, it’s a trapdoor.

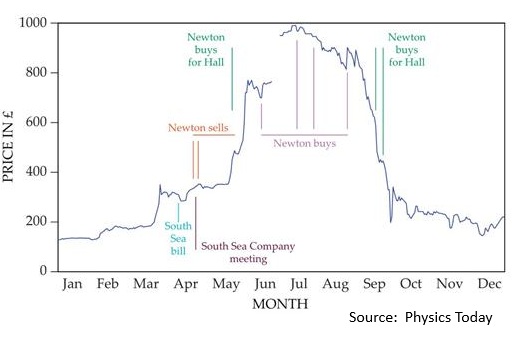

Gravity and the Lesson of Isaac Newton

Let us end with a story of how gravity was really discovered.

Isaac Newton, one of history’s greatest scientific minds, was not immune to the powerful pull of speculative mania. During the South Sea Bubble of 1720, Newton initially demonstrated prudence, selling his shares early for a healthy profit. But as prices soared and friends grew fabulously wealthy, he succumbed to what we now call FOMO—Fear of Missing Out—and re-entered the market near its peak. When the bubble burst, Newton suffered catastrophic losses, later lamenting that he could “calculate the motions of the heavenly bodies, but not the madness of men.”

His experience was a sobering demonstration of a truth he already understood in physics: what rises rapidly under its own momentum will inevitably be pulled back down by gravity. Today’s U.S. markets, now more speculative than at any time in history, mirror that same dangerous psychology. Algorithm-driven surges, meme stock frenzies, and short-term profit chasing have replaced long-term fundamentals, creating an economic environment where upward momentum feels unstoppable—until it isn’t.

Newton’s loss was more than financial; it was a recognition that the laws of nature apply to human behavior in markets as well as to falling apples. In a culture that prizes speed and quick gains over discipline, his hard-earned lesson is more relevant than ever: gravity is patient, and in markets, it always wins in the end.

Domingo Cavallo, Argentina Finance Minister (1991-96, 2001), touting the country’s convertibility of one peso = one dollar during its currency board regime. The currency board eventually collapsed in 2001 under the weight of massive capital flight. The peso now trades at 1,313.00 per/$US

Hat Tip: Craig B.

QOTD – Quote of the Day

Enlightened statesmen will not always be at the helm. – James Madison, Federalist Papers #10