It’s that time again.

No, not the now annual October fires in California (helluva a Chinese hoax, btw) we’re running from but the S&P moving into the selling zone.

We are reposting a piece we published on the very day the market peaked in July right around here. The S&P came close to making a new high today, within 1/2 point and couldn’t even end at its closing high of 3025.86. Close, but no cigar, and sometimes a cigar is not just a cigar. Thank you, Sigmund.

We maintain this is good place to sell and set up shorts again. We will sell all day long up until 3125, at which point, we will cut and be forced to capitulate that “this time may be different.” The market should be able to look through another meaningless Potemkin trade deal with China, which leaves the world worse off than when negotiations began but it’s hard to bank should of. Arghh, we are obstinate but not stupid.

Stock valuations are at record highs and the markets are so, so gummed up and distorted by government intervention, mainly from the Fed — the ultimate socialism, in our book — that policymakers and market analysts have lost their compass and can’t tell true north from south, east from west or front from back. The cheerleaders were out in full force with their pom-poms this week, by the way. Our experience is that when it feels the hardest to sell, it’s time to sell.

Tight Liquidity

Nobody can seem to figure out this “liquidity problem” in the repo market and why banks with excess reserves are not arbing the Fed funds and repo rate.

The shadow puppets that we see dancing on the wall of the cave are based on our first principles.

1) Interest rate distortions. If prices are not allowed to move to their equilibrium levels, quantities will do the work. Go back and read some of our rent control analogies on how the repression of interest rates will lead to excess demand for liquidity, which can only be filled by haven flows or monetization, ie., the central banks. Ditto for a fixed exchange rate regimes, which come under pressure and central banks have sell their hard currency reserves to maintain the peg. Witness the now in the repo market.

2) Larger budget deficits and structural changes in Treasury financing. The structural changes in the Treasury market and pro-cyclical deficits are wreaking havoc on liquidity and crowding out funding in other markets. See here.

Few understand that the U.S. G used to fund up to 50 percent of its annual budget shortfalls with the social security surplus (off-budget), limiting financing pressure from the government in the financial markets. No mas, comrades.

Social Security is now running monthly deficits, which will continue to get worse until the political geniuses in Washington fix it. The Treasury will have to increase its reliance on the market not only to fund the ballooning on-budget deficits but now an off-budget deficit (Social Security plus USPS).

Look for additional posts on this subject in the next few posts if our power stays on, which is increasingly unlikely. We have crunched some impressive and compelling data.

Finally, check out the twisted logic of the markets.

Rick Reily is one smart dude and the real brain at Black Rock. He, in essence, states in the following tweet that last October, interest rates were too high but now they are too low yet the market still needs liquidity from the Fed. Do you have a feeling we all are all just winging it? Grasping at straws?

In a well-functioning economy, interest rates would rise, reducing the demand for funding from, say, zombie companies and/or drive them out business and forcing the public sector to tighten budgets, for example, increasing real savings and therefore no need for the central bank to make up the shortfall.

Interest rates can’t rise, however, because it’s not a well-functioning economy. There is too much debt, too many market distortions, and the economy is too dependent on asset bubbles, which would burst like water balloons if rates were to rise. Just like the Q4 2018 U.S. stock market.

Enter The Selling Zone

We have entered the selling zone — S&P 3025-3100 — to execute the Get Shorty trade. This also provides an excellent opportunity for long-term investors to start cutting back on risk if they have not already been doing so.

You know our view. Rarely should LT investors reduce risk in a significant manner, maybe just three to four times during their working lives, but this is one of those times, we believe.

Structural Headwinds

The tectonic plates of the global international economic order are breaking apart and moving in the wrong direction and valuations are at historic extremes.

Not to mention the absurdity that “billions upon billions” of fixed-income securities seem to enter the negative interest rate Twilight Zone on a daily basis.

Moreover, the Fed is about to take the unprecedented action of cutting rates next week with stocks at historical highs and inflation marching higher. That signals, at least to us, a Fed gone political and that policymakers have created a beast they cannot tame.

We expect the summer Friday afternoon ramp into the close, which will be an opportunity to start letting some go or setting some up. It’s hard to sell strength but much more enjoyable than selling into weakness and into a big hole.

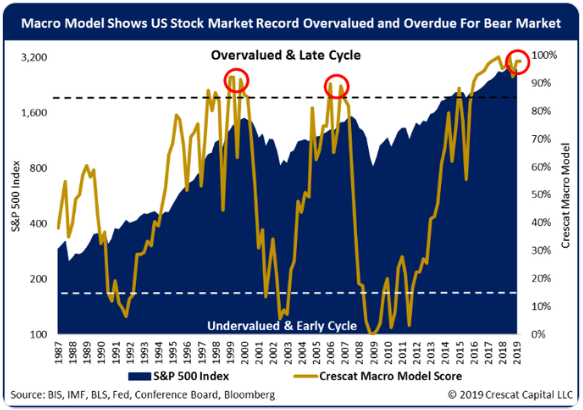

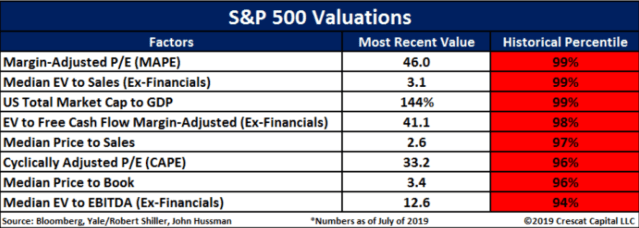

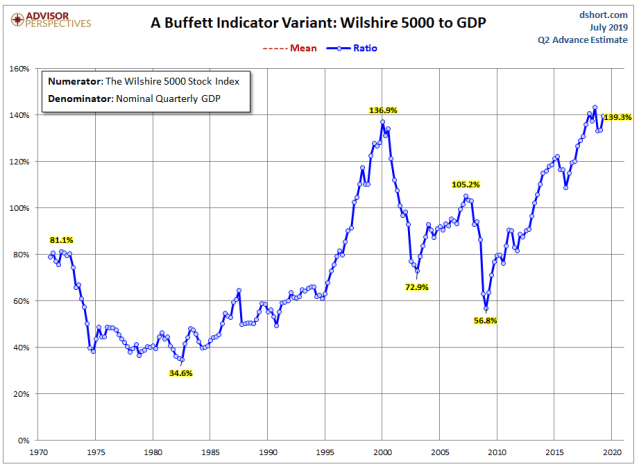

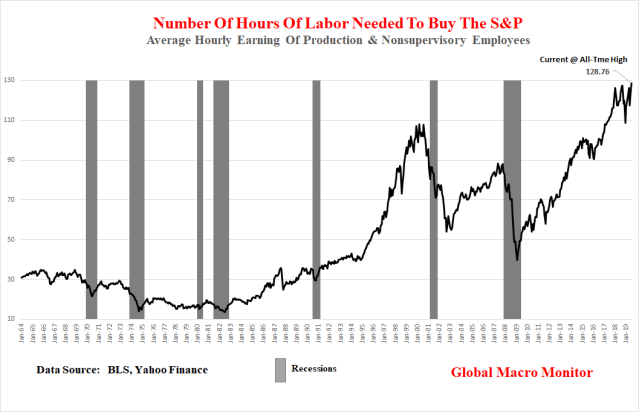

Stocks Out Of Runway

The charts below illustrate that history dictates that stocks have very little room to run to the upside from current levels. We could be wrong and ‘this time may be different.”

We seriously doubt it, however, but discipline always trumps conviction and that is why we have a hard stop at 3125 to cover. We will then wait to put them out at even more absurd valuations.

Long-term investors that do sell should have a Plan B to get reinvested if they are wrong.

Good luck, folks. See ya’ thirty-plus percent lower.

Micro Metrics

Hat Tip: Antonio Pérez Algás @apanalis

Hat Tip: Kevin C. Smith, CFA @crescatkevin

Macro Metrics

See disclaimer

Pingback: Enter The Selling Zone 2.0 | Zero Hedge

Pingback: Enter The Selling Zone 2.0 - StockExchange.international

Pingback: Enter The Selling Zone 2.0 – SYFX+

Pingback: Enter The Selling Zone 2.0 | ValuBit

Pingback: Enter The Selling Zone 2.0 – iftttwall

Pingback: Enter The Selling Zone 2.0 | Real Patriot News

Pingback: Enter The Selling Zone 2.0 – TradingCheatSheet

Pingback: Contra Corner » Enter The Selling Zone 2.0

Pingback: Enter The Selling Zone 2.0 | The Reclaimed Press

Pingback: Enter The Selling Zone 2.0 – aroundworld24.com

Pingback: Enter The Selling Zone 2.0 | AlltopCash.com

Pingback: Enter The Selling Zone 2.0 | Newzsentinel

Pingback: Enter The Selling Zone 2.0 – Forex news forex trade

Pingback: Enter The Selling Zone 2.0 | Verity Weekly

I’m a noob at investing and I hope you’re right that a downturn is coming. I’m 70% in cash now. Do any of your methods for determining that the market is overvalued take into account the historically low interest rates that affect the risk free rate for performing valuations? Also, Jamie Dimon said he could not arb the repo market spike because of liquidity requirements set by Fed. You don’t believe him?

Pingback: Enter The Selling Zone 2.0

Pingback: Discipline Trumps Conviction | Global Macro Monitor

Pingback: Buying Tops And Trump’s Race For Stock Market History | Global Macro Monitor