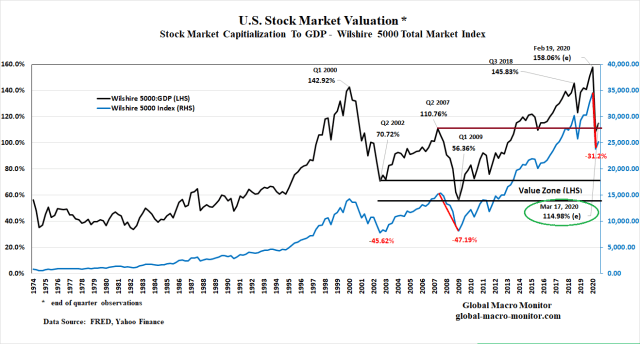

Based on the both historic price action of the two financial bubbles that have burst in the past twenty years and our favorite valuation metric — Market Capitalization-to-GDP or the Wilshire 5000 Index to Nominal GDP — stocks still have about 30-35 percent to fall before we believe the “bottom is near.”

Stock Market Valuation Is Still Higher Than Pre-GFC Peak

It is stunning that even after a 27 percent decline in the Wilshire 500, the U.S. stock market cap-to-GDP ratio is still above its pre-GFC (Great Financial Crisis) peak!

Where Is Value — A Market Cap-to-GDP of 77 Percent?

We don’t know, nor does anyone else, but a market cap-to-GDP of around 77 percent is in the neighborhood where stocks start to look cheap, in our opinion. Caveat emptor, however, markets almost always overshoot.

Assuming a -5.0 percent Q2 contraction in nominal GDP, which is generous, and the bottom comes at the end June, the 2020 bear market decline in the Wilshire 5000 (use it as proxy for other indices) from the Feb 19th closing high to a hypothetical June low would be between 50-55 percent, which is right in line of the recent bears.

Caveat Reader

We admit the above analysis could be very wrong and readers should take it simply for what it is, conjecture, along with every other analysis out there, by the way. We could be wrong on the levels or the time frame or both. Nobody. Knows. The. Future.

Use Valuation Metrics As A Gas Gauge

The valuation metric has worked for us, and we compare it to a gas gauge to inform us that the tank is running low or high — i.e, how much potential upside/downside there is in current prices — and not the exact spot where the market runs out of gas. Trying to top-tick the high is a mug’s game, ask Issac Newton.

The higher the black line moves above past highs, the harder and more painful the fall, or a meaner regression to the mean.

Write that down, folks.

The question is have stock valuations “reached a permanently high plateau” as the famous economist, Irving Fisher, stated just a few weeks before Black Thursday 1929?

Believe it, if you wish. After all, we now live in a culture and political environment where,

It’s not a lie if you believe it.

To that, we say hogwash. — GMM, Feb 17th (two days before peak S&P500)

Watch The Bond Market

Ugly price action in bonds.

Read our post from yesterday, Some Perspective, for our view on what is driving bonds. The upshot is bonds are mispriced given the deluge of supply that is coming. It is our, opinion that there are very few real long-term buyers of duration at sub-1 percent yields.

Watch this space, which is probably more important that the price action in stocks.

Shame on the stock pumpers.

Stay frosty, folks.