Six counties in the SF Bay Area ordered residents to “shelter in place.”

Six counties in the SF Bay Area ordered residents to “shelter in place.”

Still waiting for the dawn, the sun is coming up

The sun is coming up on the ocean

This love is like a drop in the ocean

This love is like a drop in the ocean

Yahweh, Yahweh

Always pain before a child is born

Yahweh, tell me now

Why the dark before the dawn? – U2

Yes, it’s dark out there and, likely will get darker, but its always darkest before the dawn.

We will get through this, folks. At least, most of us will.

Take The O’Shaughnessy Challenge

Tired of the Doom & Gloom? Take the O’Shaughnessy Challange.

We are honored that the Wall Street legend, Jimmy O‘ follows our site.

As a young trader on the Street, I was weaned on his classic book, What Works On Wall Street. If you haven’t read it, run, don’t walk to buy it.

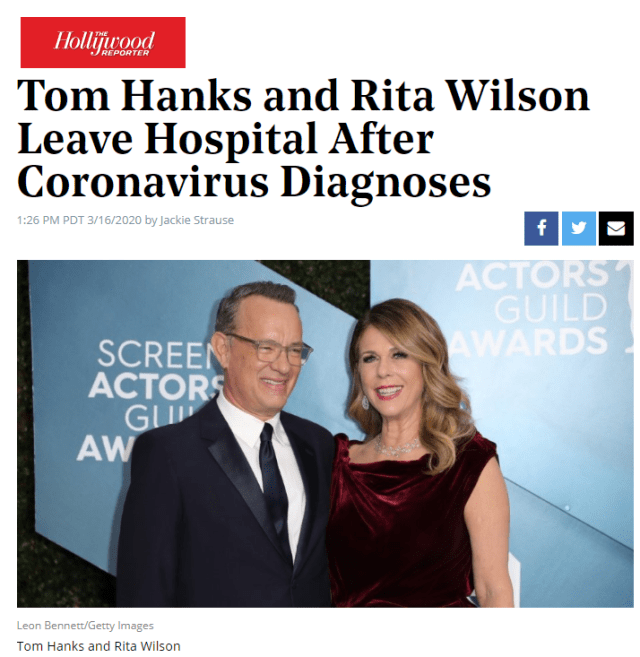

Jim retweeted a news story that we sent out earlier that Tom Hanks and, his wife Rita Wilson had been released from the hospital, and challenged his followers commit to disseminate some confirmed good news.

The Hollywood pair remain under quarantine in a rented home in Australia.

Tom Hanks and Rita Wilson, who have tested positive for the coronavirus (COVID-19), have left the hospital and are now continuing to self-isolate at a rented home in Australia.

Hanks’ rep confirmed to The Hollywood Reporter on Monday that the pair remain under quarantine in the home. — Hollywood Reporter

That is pretty damn good news, in our book. Hanks and Wilson are both 63-years-old, which puts them in the higher risk cohort group.

We’re not claiming it is going to turn the stock and bond market, but it could be the first big crack in the doom that has descended upon the world. As one of my Twitter bros tweeted,

The Woody lives!

We. Are. Not. All. Gonna. Die

Now, go take the O’Shaughnessy Challenge, find some good news to tweet or share with somebody, or in our comments. You will feel much better.

We Take The Challenge

Here is our first, short and sweet.

The snow is falling softly on CK‘s Montana ranch. What a great person and friend she is.

Can’t confirm that’s her ranch but pretty sure it’s even better.

In our March 7th post, Stages Of A Pandemic: Denial, Panic, Fear, and Rationality, we suspected the country was about to move from denial to panic over the coronavirus pandemic. It sure did and infected the global markets in a big way leading to today’s massive monetary package from the Fed.

Clearly, Jay Powell has more information than most of us as they saw the markets seizing up and had to act. Hopefully, they won’t be bailing out the bad actors and will allow the necessary debt restructurings and some equity holders to be wiped out to prevent the zombification of the economy. It won’t be the end of the world.

Trouble In Treasury Land

Last Sunday we posted this,

Can the U.S. government finance its $1.2 trillion plus annual deficits with an entire yield curve at less than 1 percent?

We seriously doubt it and the Fed is going to have to step-up big time with QE, non-QE, or let’s just call it for what it is, monetization. – GMM

During last week, bond/note auctions began to sputter, Treasury yields on the long-end spiked, and bid-offer spreads blew out.

Flying Blind

The only thing we are certain is that all of us, including the policymakers, are flying blind. Much like a pilot trying to navigate an aircraft in a thick fog lacking credible flight instruments, which have been distorted by years of monetary and government intervention to prop up asset markets. Most of the old trusted economic signals from financial markets are long gone.

What is fairly clear from the past week, at least to us, is that markets do not and will not finance the now expected $2-3 trillion annual USG budget deficit at the sub-1 percent fake interest rates and that the Fed will be forced to monetize much or maybe most of the shortfall.

To hear calls that Treasury should issue $5 trillion in 10-year bonds or refinance its debt with negative interest rates is probably the most absurd thing we have ever heard in our long journey in the financial markets. WTF?

Yes, there are $10-20 trillion of fixed-income instruments marked at negative yields but don’t make the mistake of thinking that trillions of dollars trade at those levels or that trillions of dollars were bought at negative yields by market and price-sensitive players.

Yields are set by the marginal buyer. And we suggest you get to know the marginal buyer of duration at close to zero yields — the momentum crowd, including the algos with zero context, haven flows, stock short-sellers using bonds as a proxy, and the ultimate take-out sucker, the central banks.

Though there are holders of bonds at these yields, we suspect governments cannot issue large down here without the central bank taking down a big portion of the issues, either directly or indirectly. We believe the events of last week and the Fed’s action today confirmed it.

Running a pro-cyclical fiscal policy and boosting eficit spending over the past few years is going to prove to be a huge mistake.

Let’s move on.

The Coronavirus

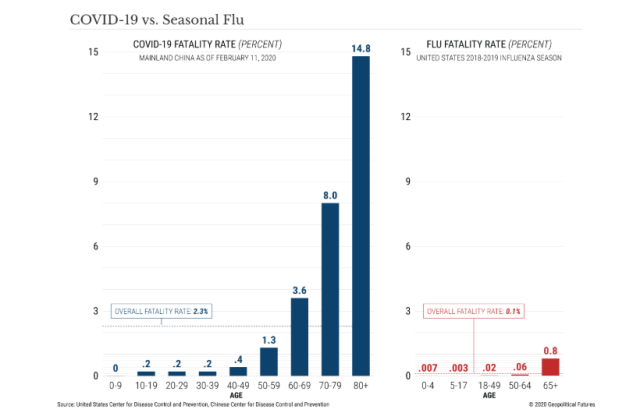

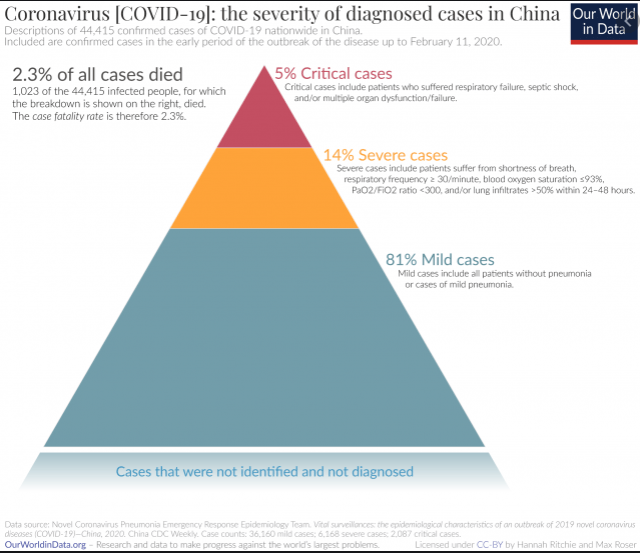

The following charts bring some perspective. That is, though COVID-19 is much more fatal and “not just the flu” we are not all going to die.

In fact, most of us who get infected won’t even require hospitalization.

The problem is the law of large numbers.

So many of us are going to be infected, even though a small proportion will need hospitalization, our healthcare system will be overwhelmed and fail.

That is why governments are locking down whole cities and governments.

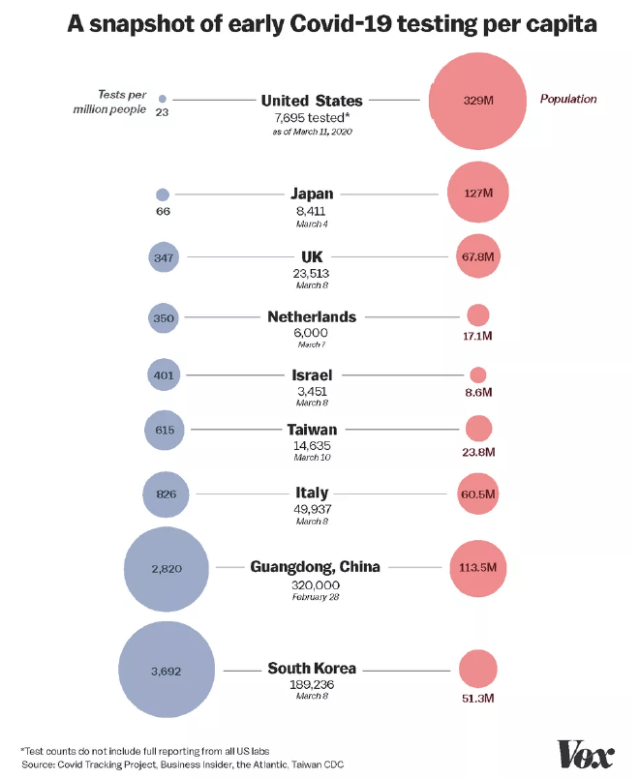

Learn from Asia.

Test, trace, isolate and inform are keys to epidemic control – Bloomberg

Godspeed, brothers, and sisters.

Not Just The Flu

80 Percent Of Cases Should Be Mild

Are You Outraged Yet?

China’s industrial output fell more than expected as the coronavirus shutdown factories, across the nation. Industrial output fell13.5% in January and February from a year earlier, versus a median estimate for a 3% contraction. Retail sales fell 20.5% in the period, compared to a projected 4% fall. Fixed-asset investment dropped 24.5%, versus a forecast 2% decline. The unemployment rate jumped to 6.2%, the highest on record.

Gross domestic product is headed for a year-on-year contraction in the first quarter, its first since comparable data begins in 1989. Source: Bloomberg

Source: Shane Oliver @ShaneOliverAMP

This is about as close as we will get to a pure lab experiment measuring the efficacy nonpharmaceutical interventions (NPIs) intended to reduce infectious contacts, folks.

The 1918 influenza pandemic resulted an estimated 500,000–675,000 deaths in the U.S. and 50–100 million deaths worldwide.

The intensity of the 1918 pandemic, whether assessed as total excess deaths, the rate of increase in the epidemic curve, or peak death rates, varied widely among U.S. cities. Cities also varied widely in their choice and timing of implementation of NPIs designed to reduce disease spread. Many cities closed schools, churches, theaters, dance halls, or other public accommodations; made influenza a notifiable disease; banned funerals or other public gatherings; or introduced isolation of sick persons. In some cases, these NPIs were put in place in the first days of epidemic spread in a city, whereas in other cases, they were introduced late or not at all. — PNAS

Note how St. Louis flattened the death curve (not the infection curve) with aggressive action in banning public gatherings within a few days of the first cases being reported. Philly was complacent, however, downplaying the threat and lagging in its policy response by just a few weeks more than St. Louis. Two weeks!

The contrast of mortality outcomes between Philadelphia and St. Louis is particularly striking. The first cases of disease among civilians in Philadelphia were reported on September 17, 1918, but authorities downplayed their significance and allowed large public gatherings, notably a city-wide parade on September 28, 1918, to continue. School closures, bans on public gatherings, and other social distancing interventions were not implemented until October 3, when disease spread had already begun to overwhelm local medical and public health resources. In contrast, the first cases of disease among civilians in St. Louis were reported on October 5, and authorities moved rapidly to introduce a broad series of measures designed to promote social distancing, implementing these on October 7. The difference in response times between the two cities (≈14 days, when measured from the first reported cases) represents approximately three to five doubling times for an influenza epidemic. The costs of this delay appear to have been significant; by the time Philadelphia responded, it faced an epidemic considerably larger than the epidemic St. Louis faced. Philadelphia ultimately experienced a peak weekly excess pneumonia and influenza (P&I) death rate of 257/100,000 and a cumulative excess P&I death rate (CEPID) during the period September 8–December 28, 1918 (the study period) of 719/100,000. St. Louis, on the other hand, experienced a peak P&I death rate, while NPIs were in place, of 31/100,000 and had a CEPID during the study period of 347/100,000. Consistent with the predictions of modeling, the effect of the NPIs in St. Louis appear to have had a less-pronounced effect on CEPID than on peak death rates, and death rates were observed to climb after the NPIs were lifted in mid-November (7–9). — PNAS

Policy Failure

Here’s to hoping we are St. Louis and not Philadelphia but our late start, dithering, and horrendous leadership, including misinformation and mixed messaging disseminated by the Administration almost surely condemns the nation as a whole to the fate of The City of Brotherly Love during the fall of 1918.

…Alex Azar [Secretary of Health and Human Services], he did go to the president in January. He did push past resistance from the president’s political aides to warn the president the new coronavirus could be a major problem. There were aides around Trump – Kellyanne Conway had some skepticism at times that this was something that needed to be a presidential priority.

But at the same time, Secretary Azar has not always given the president the worst-case scenario of what could happen. My understanding is he did not push to do aggressive additional testing in recent weeks, and that’s partly because more testing might have led to more cases being discovered of coronavirus outbreak, and the president had made clear – the lower the numbers on coronavirus, the better for the president, the better for his potential reelection this fall. — NPR

Upshot

Trust the scientists. Though I believe in miracles, and we are going to need a big one, but never bank one.

As the death toll rises and the economic carnage increases, there is going to be holy hell to pay come the November election.

President Wilson And The 1918 Flu

Very eerie parallels of how President Woodrow Wilson handled the 1918 Flu. See here.

President Trump gave the market what it was looking for today with a laser focus on containing the coronavirus and enlisting the private sector in the battle. No focus on the stock market during the entire presser, which is, ironically, one of the reasons why stocks rallied so hard.

Good for him and good for all of us.

No Victory Laps, Please

Much too early to take a victory lap, however, as it is about to get much darker over the next month.

The following is ridiculous as much as it is absurd and reveals the mentality of the White House.

One bounce after a 27 percent crash in 17 trading days doesn’t make a bull market, folks.

Update March 14

https://twitter.com/northmantrader/status/1238803846333374464?s=21

Here Is The Reality

Gonna get very dark in the next month. Kristof is a true saint, in our book.

No bottom in stocks or the economy until the test kits are ubiquitous. We believe markets want an aggressive plan and action to treat the disease rather than focusing on the symptoms. Then markets will take care of themselves and find their appropriate levels.

WTF? Where Are The Test Kits?

True story. A family member receives a text on the way to work this morning that her boss has a fever of 102 degrees with a diagnosis that she “ticked all the boxes for COVID-19.” They couldn’t test her because they didn’t have the test kits and she was put in quarantine for two weeks.

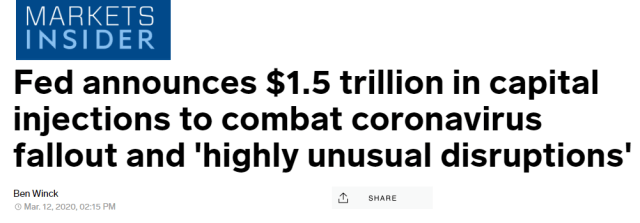

The Fed Steps Up

By the way, this is from our Sunday night post, What Every Market Player Should Now Be Contemplating,

Can the U.S. government finance its $1.2 trillion plus annual deficits with an entire yield curve at less than 1 percent?

We seriously doubt it and the Fed is going to have to step-up big time with QE, non-QE, or let’s just call it for what it is, monetization.

These yields are distorted and not true market rates, and now have become Airbnb rentals driven by haven flows, the MoMo crowd and ‘bots, and a proxy for stock shorts.

Long-term investors? Think rent control distortions. We will be closely monitoring the monthly auctions for real demand. – GMM, March 8th

No Trillion Dollar Issuance At “Fake Yields”

After two shitty bond auctions this week showing tepid demand, bid/offer spreads blowing out in Treasury securities, and the 10-year yield spiking from 0.39 percent to 0.85 percent, the Fed steps up big time today.

The Federal Reserve Bank of New York will start adding fresh capital to money markets on Thursday to pad against coronavirus risks and ease stresses on the Treasury-bill market.

The extraordinary funding measure first involves a $500 billion injection at 1:30 p.m. ET on Thursday, the bank said. The cash will be added to money markets through a three-month market repurchase agreement, or repo operation.

One-month and three-month repos for $500 billion each will be conducted on Friday and continue to be offered weekly through the calendar month, the bank added. – Market Insider

The term “capital” is a bit misleading, in our opinion.

Upshot

Marginal buyers, such as haven flows, momentum algos, and stock shorts using bonds as a proxy, who determine the price or bond yield on your screens, can set rates at zero or below. But that is not a price or yield where $1 trillion-plus of new securities can be issued or where the market can liquidate an enormous position.

Just think of the S&P500 level at the peak of 3393-ish. Marginal buyers drove the price there — irrationally in our view — and we all marked our positions and investments at that level but, in reality, it was not a level where all could liquidate.

Stay tuned as we are working on a more in-depth piece on this very important subject. We suspect all the distortions created by monetary policy and government intervention to prop up markets are coming home to roost at the worst time possible.

Marginal buyers set prices. Make sure you know who are the marginal buyers.

President Reagan On The ’87 Stock Market Crash

We are reposting this piece. History rhymes. The U.S. was in the midst of conflict with Iran during the 1987 crash as we are today.

The Fed tried to stem the selling today and who knows what would have happened if they didn’t step up.

Originally Posted on April 21, 2018

President Reagan certainly understood the nature of markets.

That is they do whatever they are going to do, sometimes without a fundamental rhyme or reason. Very different from the current occupant of the White House who seems to think every uptick in the S&P is all about him, and he is not afraid to take credit for the upside and tweet about it.

Before going to President Reagan’s comments about the October 19, 1987 stock market crash, we first review some data, which lends light on the 1987 crash.

The S&P500 had just completed a massive run from September 1985 before peaking on August 25, 1987, moving up almost 87 percent in less than two years. That qualifies as a bubble in our view.

Yuuuge Decline In Interest Rates

Much of the move was attributed to a sharp drop in interest rates.

The 10-year Treasury yield fell almost 350 bps in less than a year before making a local bottom in September 1986. Interest rates then began to move sharply higher, utterly roundtripping almost the entire move by the day of the crash.

The 10-year yield had risen 300 bps year-to-date on October 16th, closing back above 10 percent, increasing almost 150 bps just since the S&P peaked on August 25th.

The S&P500 was already down 16.33 percent from its high before crashing on October 19th. Markets rarely fall out of the sky and usually signal something big is coming by a sharp rise in volatility. Think of a Richter scale before a volcano blows.

This is why we take the early February volatility shock seriously and a signal of regime change, and give a much higher probability for a potential major price reversal than most in the market are anticipating.

Finally, the S&P500 fell 23.43 percent from the October 16th Friday close to the intraday low on Tuesday before a mysterious buyer stepped into to the Major Market Index futures contract at 12:38 p.m, setting the stage for one of the most powerful rallies in history.

We believe the 1987 stock market crash was an accident waiting to happen due mainly to a toxic cocktail of a severely overbought market and rising interest rates. All that was needed was a buyers strike coupled with some catalysts or reasons to bail and take profits. The same reasons may or may not have mattered if not for such a toxic cocktail.

Given the nature of the New Economy, we seriously doubt the government will allow such a similar short-term crash, say, 15-25 percent, to occur again. We now have no doubt the Fed will step up and announce they will do whatever it takes and become the buyer of last resort to keep the market from melting down in one or two days.

Why? Because it would be the end of the world and they surely know it.

The thought of the Fed directly purchasing stocks as the Bank of Japan now does contradicts everything Larry Kudlow’s dictum, “free market capitalism is the best path to prosperity” stands for.

Privatizing profits and socializing major Wall Street losses are now forever institutionalized especially given the structure of our asset driven global economy. The “Powell put” may now have a little lower strike price than many traders would like but it is absolutely still in place. No doubt about it.

Oy veh! Sorry deflationistas.

Iran Again

By the way, the U.S. was also in the midst of a conflict with Iran in October 1987.

President Reagan’s Comments

Now to President Reagan.

Asked after the close if the stock market crash was his fault, the President delivers the ultimate money quote, in our book:

Profound. We can learn from the Gipper to refrain from trying to explain or attribute daily stock market moves to certain factors. Any one of the catalysts we deem moved the market in a certain direction on a given day could have moved it 180 degrees the other way with a different set of technical conditions.

Reagan truly understood market noise.

Full Transcript Of October 19, 1987 Informal Exchange With The Press

Here is the full transcript with reporters that day, October 19, 1987.