We are adding to our gold futures trade right here, right now at 1289 with a 1360ish target. Trailing stop at 1252.00. Decent risk-reward, in our opinion. The path of least resistance is now up with 5.5 percent upside to 2.9 percent downside.

We are adding to our gold futures trade right here, right now at 1289 with a 1360ish target. Trailing stop at 1252.00. Decent risk-reward, in our opinion. The path of least resistance is now up with 5.5 percent upside to 2.9 percent downside.

The market has spoken.

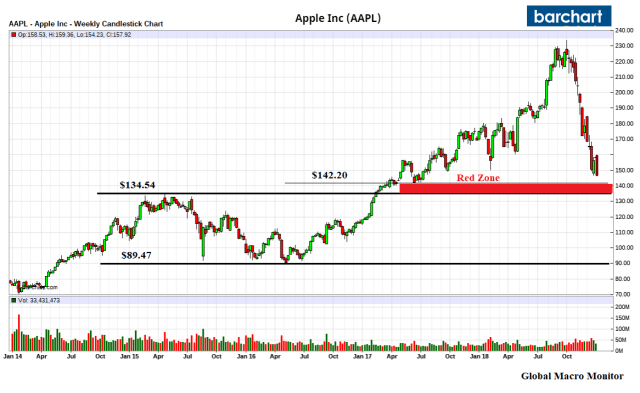

Apple stock has taken out the Christmas Eve low at $146.59 in tonight’s after-hours trading. Tough to gauge the true conviction until tomorrow’s open.

Nevertheless, the Apple bulls, which includes Mr. Buffett, need to move into prevent defense here and take an Alamo-like stand to gallantly defend the red zone at $134.54 to $142.20. A break of the goal line at $134.54 opens up some big downside.

Don’t count out the hammer to really come down on Jay Powell and the Fed now. He is due to speak on Friday.

Apple truly dropped the ball by depending on financial engineering and inflation — i.e., buybacks and increasing revenues by raising iPhone prices — to increase its stock price. Investors are now paying the price.

Steve Jobs must be rolling over in his grave with Tim’s cave to Uncle Carl. Mr. Cook is now left to defend Apple’s purchase of the stock, some at much higher prices, while Uncle Carl is probably lounging on a beach somewhere in the Carribean.

We love the company and the product but not the stock quite yet.

Stay tuned.

Apple just released this extraordinary guide down in a letter to investors from Tim Cook.

We are now watching for the stock’s reaction. We suspect it could be ugly or the stock may have priced most of this. We have and have had our priors but we don’t guess and will let the market tell us.

“We suspect if unit sales do not increase this holiday season, the stock could be in trouble.” – GMM, November 1, 2018

Target Apple

“What more efficient way to take the U.S stock market down than to hit its largest stock by threatening market access to the Chinese consumer? Apple’s market cap is over $800 billion, the world’s largest, and such a scenario would certainly take the overall market down.” – GMM, August 7, 2017

Apple made a huge mistake by announcing it would stop reporting iPhone unit sales. Trying to hide bad news never works. Transparency trumps all.

January 2, 2019

To Apple investors:

Today we are revising our guidance for Apple’s fiscal 2019 first quarter, which ended on December 29. We now expect the following:

We expect the number of shares used in computing diluted EPS to be approximately 4.77 billion.

Based on these estimates, our revenue will be lower than our original guidance for the quarter, with other items remaining broadly in line with our guidance.

While it will be a number of weeks before we complete and report our final results, we wanted to get some preliminary information to you now. Our final results may differ somewhat from these preliminary estimates.

When we discussed our Q1 guidance with you about 60 days ago, we knew the first quarter would be impacted by both macroeconomic and Apple-specific factors. Based on our best estimates of how these would play out, we predicted that we would report slight revenue growth year-over-year for the quarter. As you may recall, we discussed four factors:

First, we knew the different timing of our iPhone launches would affect our year-over-year compares. Our top models, iPhone XS and iPhone XS Max, shipped in Q4’18—placing the channel fill and early sales in that quarter, whereas last year iPhone X shipped in Q1’18, placing the channel fill and early sales in the December quarter. We knew this would create a difficult compare for Q1’19, and this played out broadly in line with our expectations.

Second, we knew the strong US dollar would create foreign exchange headwinds and forecasted this would reduce our revenue growth by about 200 basis points as compared to the previous year. This also played out broadly in line with our expectations.

Third, we knew we had an unprecedented number of new products to ramp during the quarter and predicted that supply constraints would gate our sales of certain products during Q1. Again, this also played out broadly in line with our expectations. Sales of Apple Watch Series 4 and iPad Pro were constrained much or all of the quarter. AirPods and MacBook Air were also constrained.

Fourth, we expected economic weakness in some emerging markets. This turned out to have a significantly greater impact than we had projected.

In addition, these and other factors resulted in fewer iPhone upgrades than we had anticipated.

These last two points have led us to reduce our revenue guidance. I’d like to go a bit deeper on both.

Emerging Market Challenges

While we anticipated some challenges in key emerging markets, we did not foresee the magnitude of the economic deceleration, particularly in Greater China. In fact, most of our revenue shortfall to our guidance, and over 100 percent of our year-over-year worldwide revenue decline, occurred in Greater China across iPhone, Mac and iPad.

China’s economy began to slow in the second half of 2018. The government-reported GDP growth during the September quarter was the second lowest in the last 25 years. We believe the economic environment in China has been further impacted by rising trade tensions with the United States. As the climate of mounting uncertainty weighed on financial markets, the effects appeared to reach consumers as well, with traffic to our retail stores and our channel partners in China declining as the quarter progressed. And market data has shown that the contraction in Greater China’s smartphone market has been particularly sharp.

Despite these challenges, we believe that our business in China has a bright future. The iOS developer community in China is among the most innovative, creative and vibrant in the world. Our products enjoy a strong following among customers, with a very high level of engagement and satisfaction. Our results in China include a new record for Services revenue, and our installed base of devices grew over the last year. We are proud to participate in the Chinese marketplace.

iPhone

Lower than anticipated iPhone revenue, primarily in Greater China, accounts for all of our revenue shortfall to our guidance and for much more than our entire year-over-year revenue decline. In fact, categories outside of iPhone (Services, Mac, iPad, Wearables/Home/Accessories) combined to grow almost 19 percent year-over-year.

While Greater China and other emerging markets accounted for the vast majority of the year-over-year iPhone revenue decline, in some developed markets, iPhone upgrades also were not as strong as we thought they would be. While macroeconomic challenges in some markets were a key contributor to this trend, we believe there are other factors broadly impacting our iPhone performance, including consumers adapting to a world with fewer carrier subsidies, US dollar strength-related price increases, and some customers taking advantage of significantly reduced pricing for iPhone battery replacements.

Many Positive Results in the December Quarter

While it’s disappointing to revise our guidance, our performance in many areas showed remarkable strength in spite of these challenges.

Our installed base of active devices hit a new all-time high—growing by more than 100 million units in 12 months. There are more Apple devices being used than ever before, and it’s a testament to the ongoing loyalty, satisfaction and engagement of our customers.

Also, as I mentioned earlier, revenue outside of our iPhone business grew by almost 19 percent year-over-year, including all-time record revenue from Services, Wearables and Mac. Our non-iPhone businesses have less exposure to emerging markets, and the vast majority of Services revenue is related to the size of the installed base, not current period sales.

Services generated over $10.8 billion in revenue during the quarter, growing to a new quarterly record in every geographic segment, and we are on track to achieve our goal of doubling the size of this business from 2016 to 2020.

Wearables grew by almost 50 percent year-over-year, as Apple Watch and AirPods were wildly popular among holiday shoppers; launches of MacBook Air and Mac mini powered the Mac to year-over-year revenue growth and the launch of the new iPad Pro drove iPad to year-over-year double-digit revenue growth.

We also expect to set all-time revenue records in several developed countries, including the United States, Canada, Germany, Italy, Spain, the Netherlands and Korea. And, while we saw challenges in some emerging markets, others set records, including Mexico, Poland, Malaysia and Vietnam.

Finally, we also expect to report a new all-time record for Apple’s earnings per share.

Looking Ahead

Our profitability and cash flow generation are strong, and we expect to exit the quarter with approximately $130 billion in net cash. As we have stated before, we plan to become net-cash neutral over time.

As we exit a challenging quarter, we are as confident as ever in the fundamental strength of our business. We manage Apple for the long term, and Apple has always used periods of adversity to re-examine our approach, to take advantage of our culture of flexibility, adaptability and creativity, and to emerge better as a result.

Most importantly, we are confident and excited about our pipeline of future products and services. Apple innovates like no other company on earth, and we are not taking our foot off the gas.

We can’t change macroeconomic conditions, but we are undertaking and accelerating other initiatives to improve our results. One such initiative is making it simple to trade in a phone in our stores, finance the purchase over time, and get help transferring data from the current to the new phone. This is not only great for the environment, it is great for the customer, as their existing phone acts as a subsidy for their new phone, and it is great for developers, as it can help grow our installed base.

This is one of a number of steps we are taking to respond. We can make these adjustments because Apple’s strength is in our resilience, the talent and creativity of our team, and the deeply held passion for the work we do every day.

Expectations are high for Apple because they should be. We are committed to exceeding those expectations every day.

That has always been the Apple way, and it always will be.

Tim

Q: What to you is a logical macro trade at this stage of the cycle? – Bloomberg

A: Logical doesn’t mean profitable – Stan Druckenmiller, 32.33 minutes

(QOTD = Quote of the Day)

Buying the euro with an 80 cent handle was such a no-brainer at the beginning of the millennium. Here? A much tougher call.

We do think the euro, in its current form, will not last.

We suspect the first step, especially if the ginormous German current account surplus does not begin to decline soon, will be a move to a two-speed dual currency. One for the northern (core) countries, such as Germany; and one for the south (periphery), for Italy and Greece, for example.

A two-speed euro, involving two distinct but related currencies, keeps the entire euro project together and gives the EU donkey the carrot of moving forward while at the same time deploying the stick of promised economic reform. It is important to understand that the perpetual forward motion idea lies at the heart of the EU. As long as the project seems to be moving forward slowly towards the nirvana of more integration when the time is right, Europe is progressing…

So peripheral countries need a change in the value of the currencies we trade in to make our companies more competitive and thus more likely to export. In tandem, we need to make imports more expensive so we don’t buy too many of them. The weaker exchange rate achieves this. Devaluations work. And to anyone who doubts that devaluations work in small European countries, just examine the lasting competitive gains garnered by Finland and Sweden after their 1992 devaluations.

Without currency change, we can’t keep up with the Germans. Up till now, we borrowed to achieve a lifestyle and a level of economic activity. Now none of us can pay this money back. – OECD Observer

Tough map to getting there, however, and will have to be a sprung on the market as a surprise otherwise queue the financial panic. The new incoming ECB President (likely to be Finnish) and Eurozone leaders best begin to start thinking about it.

Hat Tip: Holger

The fiscal stimulus and trade concessions cometh?

The Caixin/Markit Manufacturing Purchasing Managers’ Index (PMI) for December, released on Wednesday, fell to 49.7 from 50.2 in November, marking the first contraction since May 2017.

Economists polled by Reuters had forecast only a marginal dip from November to 50.1, just above the neutral 50-mark dividing expansion from contraction on a monthly basis.

New orders — an indicator of future activity — fell for the first time in two and a half years, with companies reporting subdued demand despite some price discounting. New export orders shrank for the ninth month in a row.

While production edged higher after two months of stagnation, factories cut jobs for the 62nd month in a row. – Reuters, Jan 1

Bloomberg is reporting tonight,

Chinese President Xi Jinping said Taiwan must be unified with the mainland to achieve his goal of completing the country’s rejuvenation.

“China must and will be united, which is an inevitable requirement for the historical rejuvenation of the Chinese nation in the new era,” Xi told a gathering in Beijing to mark the 40th anniversary of a landmark Beijing overture to Taipei after the U.S. and China established relations.

Xi also sent a warning to advocates of Taiwan’s independence, who include supporters of Taiwanese President Tsai Ing-wen. “It’s a legal fact that both sides of the straits belong to one China, and cannot be changed by anyone or any force,” Xi said. – Bloomberg, Jan 1

Whether this impacts the trade negotiations with the United States, who knows. But it can’t be positive.

John Bolton must be fuming. Remember, Xi, plays the long game while Trump plays for short-term wins.

We have advocated over the past year keeping the Taiwan Strait front and center on the geopolitical radar. See here and here.

Hat Tip: Greg McKenna

Here’s a nifty tune to start 2019. St. Bono looks like a baby…

Although it is one of U2’s most well-known tunes, many fans don’t realize that the song’s lyrics are actually about the Polish Solidarity movement. – IrishCentral

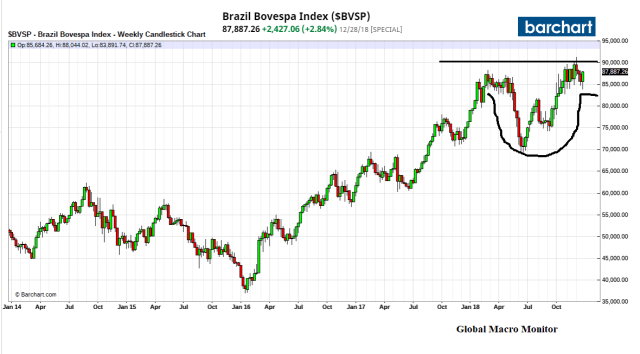

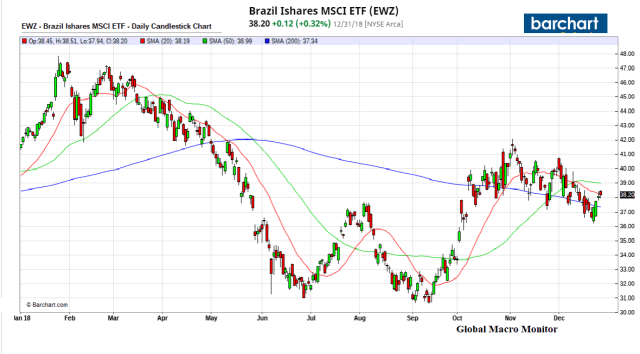

Bolso’s FinMin, Paulo Guedes and his team of “Chicago Boys” are very market-friendly and potentially transformative for the Brazilan economy. The question is does Bolsonaro have the political skills to see the reforms through?

The animal spirits of a new market-friendly government should boost the BOVESPA during the administration’s honeymoon. Brazil is our favorite stock market to start the year.

Probably the best way to play it is with the Country ETF, EWZ, with the buy trigger at break above the 50-day at $38.99, in our opinion. First upside target is $47.77. After the purchase, put in the first trailing stop at $36.20.

EWZ has been correcting after the almost 40 percent six-week runup into the election. The ETF could see a measured move to $47.77-$53.38 in a timeframe dependent on how global markets fare in January. Good risk reward with a potential 20-35 percent upside. Not a bad day at the office.

Caveat emptor: the medium-term political risk is elevated. Pension reform is a real political bitch, in all countries, and allegations of corruption continue to haunt even the Bolsonaro government. Moreover, Jair seems to have tied his future to President Trump, who is, at best, certain to have a rocky 2019.