It is 94 days and 10 hours until the November 6th midterm election, which will determine the fate of the Trump presidency. All things are now political, including, and, most notable, today’s nonfarm payrolls report.

We did an in-depth analysis of what is happening in the labor market in our May post, Deconstructing The U.S. Jobs Market.

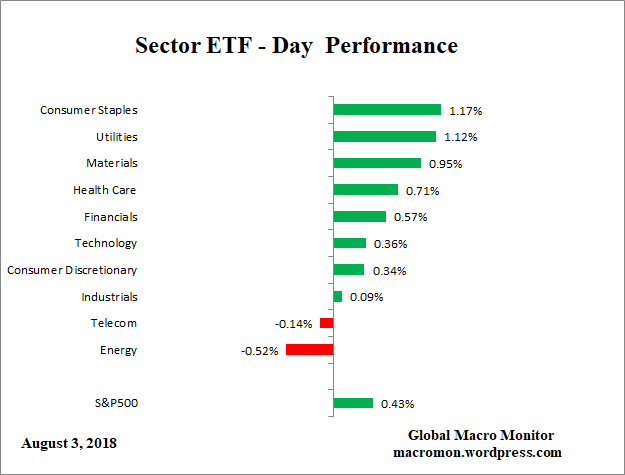

July Employment Report

Nonfarm payrolls came in less than expected, increasing by 157k in July with the unemployment rate moving down slightly to 3.9 percent. Payroll jobs extended their streak of 94 consecutive months of positive growth, which began in October 2010.

The average monthly change in payroll employment during the streak has been an increase of 200k jobs per month. July’s number thus underperformed the average but prior months were revised up, increasing the 3-month moving average to 224k. There is too much noise in the data to make inferences from one month of data.

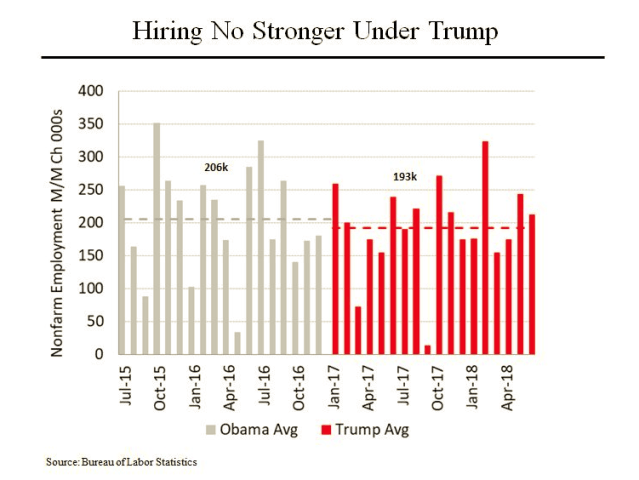

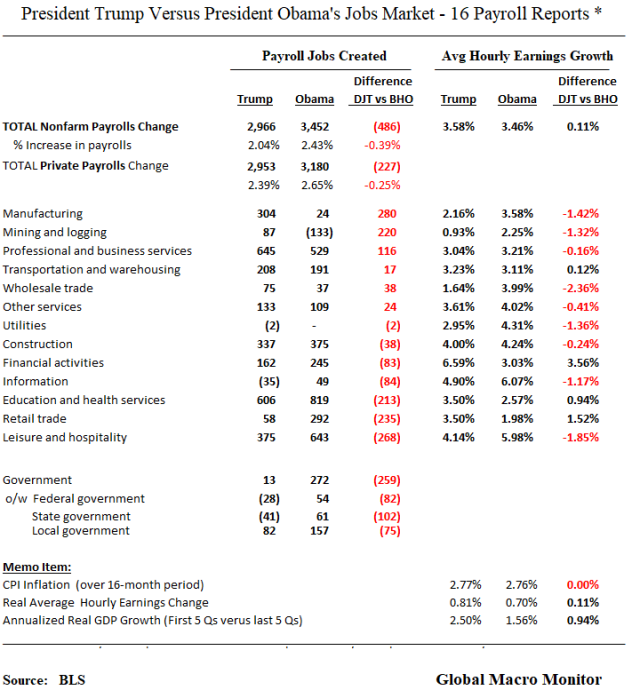

The Trump v. Obama Jobs Machine

As we move closer to the November election, a big debate is coming on the economy, especially over jobs. The economy is in good shape, but the growth is not trickling down to most of the labor force.

The economy, as measured by real GDP growth, is significantly stronger in the first 18 months of the Trump administration than the last 18 months of President Obama’s term. However, job creation is oddly lagging, and real wage growth is lower under Trump than Obama.

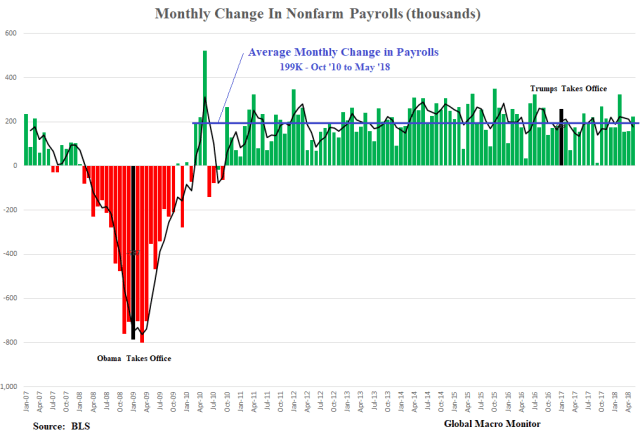

Monthly Job Increases

The chart illustrates the monthly change in nonfarm payrolls in President Trump’s first 18 months has averaged 190k versus President Obama’s 206k in his last 18 months in office.

There are three more employment reports before the midterm elections, and nonfarm payrolls will have to increase by an average of 350k per month for Trump’s job machine to exceed Obama’s 213k monthly increase in his last 21 months in office. That just ain’t gonna happen, folks.

Employment Growth By Sector

The table breaks down the job changes by sector.

Not Your Mother’s Manufacturing Jobs

President Trump deserves credit for reviving manufacturing employment, but these are not the traditional manufacturing jobs of historical folklore. For example, employment in the auto and light truck manufacturing sector continues to decline, 9k jobs lost since President Trump took office. This may be one of the factors why he is polling so poorly in Michigan and the midwest states.

Moreover, even after the implementation of tariffs, employment in the primary metals manufacturing sector, which includes the celebrated steel mills has only increased by 14k since January 2017.

It also seems odd wage growth is much slower in manufacturing and mining under Trump. It may be due to the fact there is so much slack in these sectors.

Food And Booze Manufacturing Jobs

Conversely, employment in food manufacturing and brewpubs (producing craft beer), wineries, and distilleries is booming, and account for more than 20 percent of the manufacturing jobs created during the current administration. What the hard hats would probably label “snowflake” manufacturing are what economists call nondurable goods.

Upshot

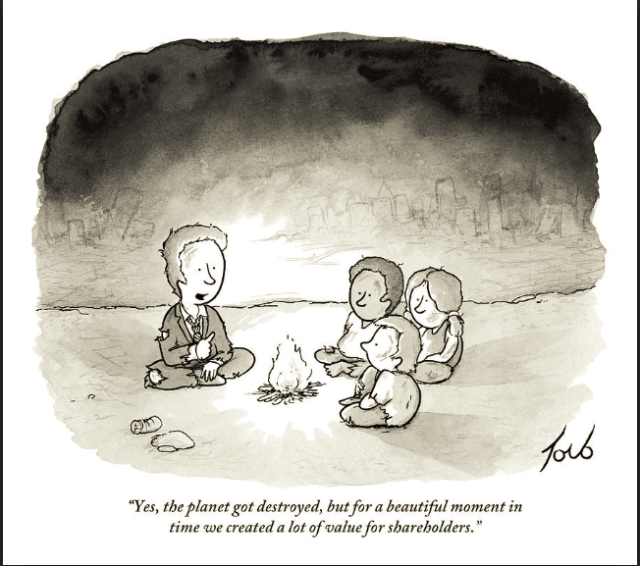

The economy continues to hum along, but most the gains appear to be accruing to capital rather than labor. We do sense a political outrage building over the tax cuts being used mainly for stock buybacks and not new hiring or wage increases.

Here is a rant from a recent piece from none other than Forbes Magazine, the bastion of capitalist Wall Street,

The decades-long diversion of business income to shareholders has resulted in a soaring stock market but also stagnating incomes for most of the population. If this gargantuan transfer of assets to the existing owners of shares is allowed to continue, nothing less than a global political or financial cataclysm—or both—is in the offing. The good news is that remedial action may be on the way.

Let’s be clear. A massive extraction of resources for shareholders is not the way capitalism used to work. What’s now happening would have been illegal only a few decades ago. The principal mechanism enabling this massive shift of resources—an estimated $1 trillion in 2018 alone—is a practice known as share buybacks: firms purchase their own shares so as to increase the value of each individual share and so enrich the existing owners of shares.

When conducted on a large scale in the open market, share buybacks used to be considered illegal as they constituted obvious stock price manipulation. But they were effectively legalized in 1982 by a hard-to-understand SEC regulation: rule 10b-18. As a result, executives of public corporations, rather than creating fresh value and new customers through entrepreneurship and innovation, began extracting value for shareholders (and themselves) by buying back their own shares. The emphasis on generating immediate returns to boost the current stock price in due course created a short-term focus in public corporations at the expense of innovation, long-term shareholder value, and the dynamism of the entire economy. – Forbes, July 8, 2018

October Surprise?

President Trump and the Republicans are getting minimal political traction from the strong economy for the above reasons and headed for a major political facial in the midterm elections.

We fully expect an October surprise, probably in the form of some Potemkin Village-esque trade deal with China, much like the Korean trade deal farce, for example.

It will be too little, too late, and certainly won’t change the women’s vote.

Contemplate this. My old Congressman from Greenwich Village, Jerry Nadler, current ranking member, as the new chairman of the House Judiciary Committee in the next Congress. Subpoena power galore. The president’s worst nightmare.

The next Congress is sure to be full of political fireworks and massive uncertainty. Not priced.

Source: New Yorker

Tell us it ain’t so, Forbes, the bastion of capitalism and Wall Street. Using such words as “global political or financial cataclysm” to warn us about the consequences of stock buybacks? Double Yikes!

The decades-long diversion of business income to shareholders has resulted in a soaring stock market but also stagnating incomes for most of the population. If this gargantuan transfer of assets to the existing owners of shares is allowed to continue, nothing less than a global political or financial cataclysm—or both—is in the offing. The good news is that remedial action may be on the way.

Let’s be clear. A massive extraction of resources for shareholders is not the way capitalism used to work. What’s now happening would have been illegal only a few decades ago. The principal mechanism enabling this massive shift of resources—an estimated $1 trillion in 2018 alone—is a practice known as share buybacks: firms purchase their own shares so as to increase the value of each individual share and so enrich the existing owners of shares.

– Forbes, July 8, 2018

1012

Apple’s market cap hit 1012 dollars today.

Impressive but no pom-poms here at Global Macro Monitor. We would be more impressed if Apple’s main businesses were doing better and the company was more focused on electrical engineering rather than financial engineering.

Don’t get us long, I mean wrong, we were The Dallas Cowboy Cheerleaders for Apple’s stock pre-2015. Check the record.

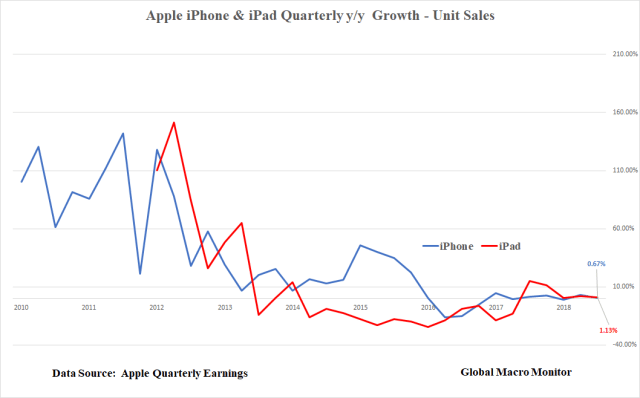

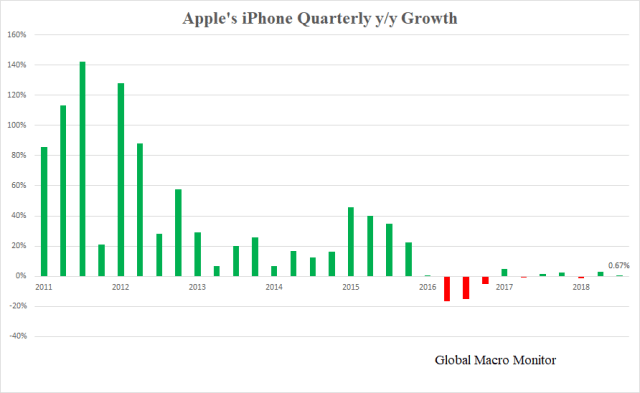

Just the data, ma’am

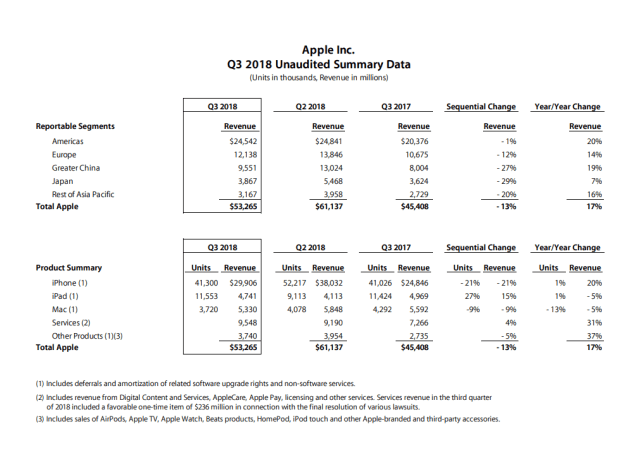

The table below illustrates that almost all of Apple’s revenue growth was driven by inflation, that is the price increase for iPhones. Unit sales growth for the company’s three major products – iPhone, iPad, and Mac – were either flatish year over year or negative. This has been the case now for several years.

If Apple were not able to significantly raise iPhone prices (mainly through the upgrade to the X) and only grow revenues by the device’s unit sales growth of 0.67 percent, Apple’s total revenues would have been about one third of what was posted, or 6.7 percent versus 17.3 percent.

One thousand dollar smart phones are not a sustainable proposition, in our opinion, folks. China, or somebody, somewhere, will, or already is producing a quality equivalent smart phone for $250.

Are iPhones Peacock Feathers?

Yes, yes, and yes, still not a Porsche. We get it.

Our sense, however, millennials, and the youngers, are not as into conspicuous consumption as the self-absorbed boomers are.

An iPhone is not peacock feathers, folks, at least we don’t think so.

Does owning an Apple iPhone really signal superior genes to the opposite sex?

Make sure to click on the peacock feathers link to understand what the hell we are talking about!

An Omen Of Coming Inflation?

Furthermore, Apple’s inflation driven earnings may be an omen of a larger inflation coming to the overall economy.

Of course, the iPhone X was a much better quality phone and will almost certainly be hedonically adjusted by the BLS so it won’t show up in the CPI.

Ridiculous. Real wages and purchasing power decline as consumers purchase higher priced items, regardless if the camera phone has a better resolution.

But, hey, if Apple can charge $1,000 for a phone why not ________ for any item. Fill in the blank for your company and seller or supplier of choice.

Great Products, But What Have You Done For Us Lately?

We love Apple products, have loved the stock in the past, and have a double digit number of Apple devices in our household.

We will like the stock much more when they are driven more by electrical engineering (product innovation) rather than financial engineering (stock buybacks).

The New Supply-Side Economics of Asset Markets

Finally, the limiting supply (shifting supply curve left) induced surge in Apple price shares due to buybacks is endemic of today’s asset markets, in general. Most notable in risk-free bonds — restricting supply through QE, which distorts the risk-free interest rate, of which all assets are priced; though this is slowly changing; housing with all cash investors and private equity — now the largest holder of single family homes, and gouging renters; and equities through the massive buyback programs.

Moreover, there is feedback loop buying bias induced by the move to passive investing.

The “Steel Bubble”

These are a few of the major factors why these overvalued asset markets are so much harder to pop than the asset bubbles of Christmas past. See our posts on the “steel bubble.”

Apple, The Stock

Toppy. Selling the hype and waiting for the “new, new thang.” If they build it, I will come.

Overall market action bullish. No sellers, until they sell. Today’s action is a signal that no-liquidity August has arrived. Go to the beach!

Stay tuned.

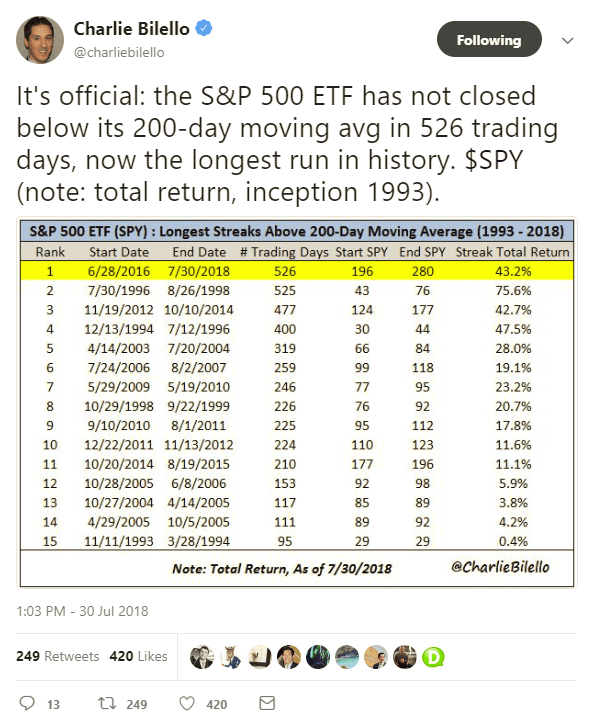

In case you missed Charlie B.’s excellent table from yesterday, which illustrates the S&P500 has not closed below its 200-day moving average in 526 days, here you go.

Stunning, especially given Joltin’ Joe’s hitting streak lasted 526 consecutive games. Coincidence? You decide.

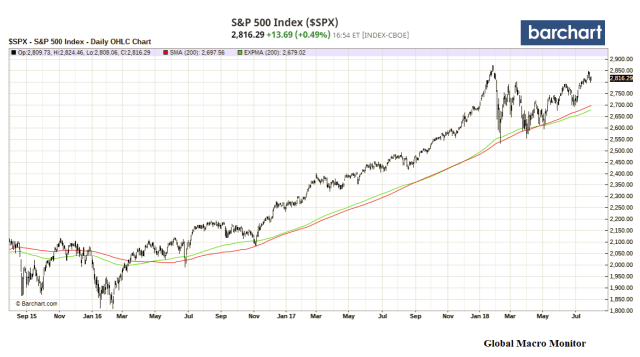

We do have the S&P500 closing below its 200-day April 2, 2018, however. Not the case for the exponential 200-day versus the simple 200-day, but moving to the exponential opens up earlier days for such a breach. The same holds for the SPY, the S&P500 ETF. We have the question into Charlie.

Even so, the simple 200-day has been the steel curtain of support for the stock market over the past two years. The classic moving average took a massive pounding late March to early May yet still held, which we noted in our, Stock Bull & Bear Traps Galore post in early May,

Relentless Pounding Of The 200-day Moving Average

A lower swing high, that is below 2.717, will almost seal the fate the bears will take out the 200-day sometime very soon. They have been relentlessly pounding the 200-day during this correction.

In bull markets, the 200-day may be tested maybe once or twice over a short period then bounce big and continue the uptrend. Not test it every third day as it seems to be doing recently.

Some believe what doesn’t kill you makes you stronger.

Personal character? Absolutely.

Technical support levels? We don’t think so.

Eventually, the front line will crack, even if it is the robots defending it. And, what if they decide to all retreat at the same time and go offer only, as they did in the flash crash?

When contemplating the constant hammering of the S&P500’s 200-day moving average, think the financial equivalent of Chairman Mao’s “human wave theory.”

“overwhelm the defenders by the sheer weight of numbers” – Wikipedia

-Global Macro Monitor, May 7

We concluded wrongly. Thank you ‘bots, algos, machines, drones or whatever the hell you want to call them.

We do expect the 200-day to be breached sometime before the year-end, however, with a higher probability of it happening in August or September. In case you’re wondering, the current S&P simple 200-day is at 2698, or about 4 ½ percent below today’s close.

Stay tuned.

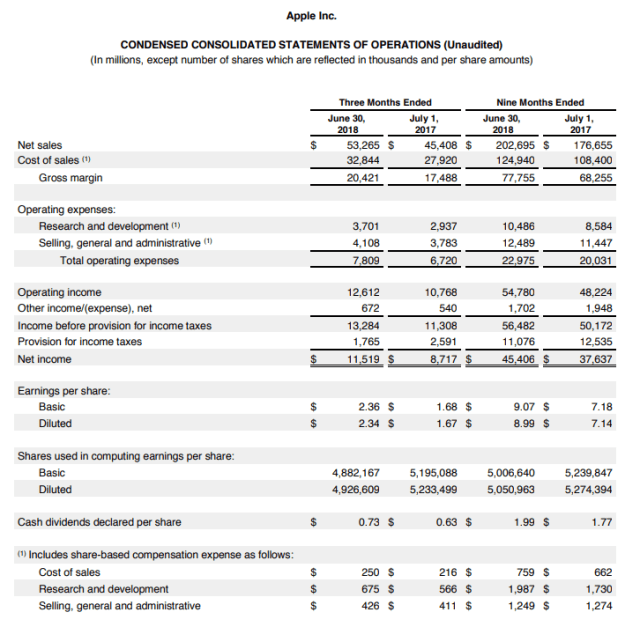

Apple out with earnings. Stock up about 3 percent in after hours.

Revenues

We note: 1) the 17 percent overall revenue growth, still impressive given the size of the company; 2) looks like no blowback yet on trade with China, i.e., boycott of Apple products. Watch this space; 3) services growth comes in over 30 percent, and 4) all iPhone revenue growth all in the price increase, unit sales continue to flat line.

Upshot: The company is trying hard, and to some extent succeeding, to reinvent itself away from just an iPhone company. Nevertheless, iPhones still make up almost 60 percent of total revenues.

Stock

Where is stock going?

We don’t know but the glory growth days are over unless they can kickstart innovation. We are basically neutral on stock but don’t like the market in August. If big tech moves lower in August probably the best FAANG performer, however.

Bad policies lead to bad outcomes. – Jamie Dimon, July 30, 2018

(QOTD = Quote of the Day)

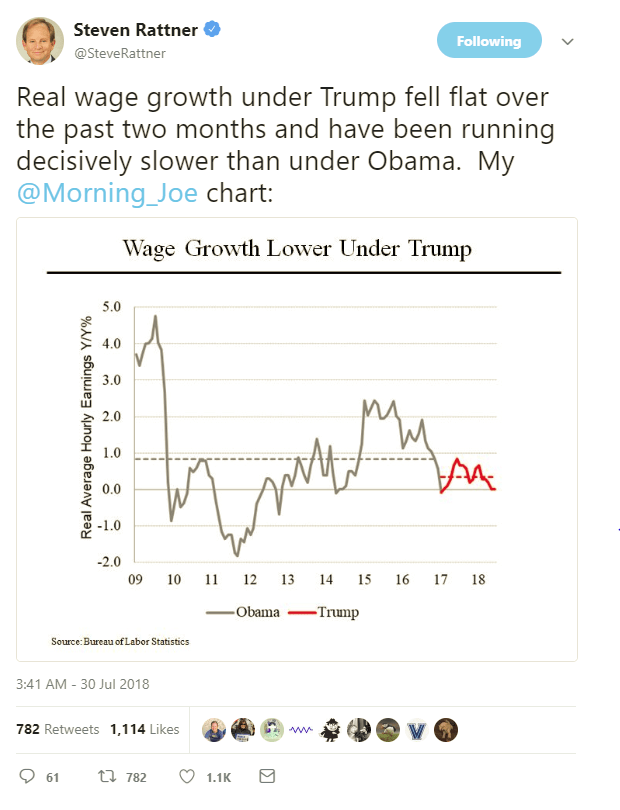

Steven Rattner, whom the UAW can thank for leading the auto bailout during the GFC, presented these graphs today on Morning Joe.

Does the analysis look a little familiar?

It should. We first presented it in our, Deconstructing The U.S. Jobs Market in May and, again, in our, Really How Was That Employment Report on June 4th in much greater detail.

We claim no monopoly on the facts or the truth as they are universal, and we are happy they are getting out there and we got them to you early. Stay tuned for more good stuff coming your way.

We did send Rattner our analysis in May.

Nevertheless, the above data, however presented, are probably the reason why Trump is getting no political kick from the economy and tax cuts. We are looking for a massive Lavender Wave in the November midterms. Certainly not priced.

This One Takes The Cake!

This one pissed us off, however. We first started presenting this chart in 2012.

They didn’t even have the courtesy change the chart title and gave no attribution.

We lift all the time but try to give attribution.

Afterall research is nothing more than formalized plagiarism, no. The raison d’etre of blogs are to narrow down all the data and research to what is important.

Again, no monopoly on facts or the truth. Maybe a little on the presentation style, however.

As they say, you know what is the best form of flattery.

Fareed’s interview with Yale professor, Laurie Santos, and teacher of Yale’s most popular class ever, the “happiness class” is a great follow up to our Facebook post from last week.

Yale professor Laurie Santos, who teaches a popular “happiness class,” tells Fareed how social media makes people less social and so can decrease wellbeing.

(Click here for interview)