Is that it? Is the sell-off over, new highs on the short-tem horizon?

Nobody knows. The recovery is a process and unfolds one step tick at a time.

In our last Week In Review post, we noted,

Only three times since 1950 has intraday volatility jumped so high as measured by a modified version of the Average True Range: 1) September 1955 after an extraordinarily period of calm the S&P500 tanked on September 26th when markets opened after President Eisenhower’s heart attack on the 8th hole of Cherry Hills Country Club over the weekend. The market quickly recovered; 2) January 1962 when the “Kennedy slide” began to accelerate, and 3) the October 1987 stock market crash. – Global Macro Monitor, February 11

Given the historic vol shock we just experienced, we thought we would take a look at how the bear market of 1987 and 1962 unfolded after their volatility spikes.

We dismiss the 1955 Eisenhower heart attack shock as it was short-lived and did not result in a bear market.

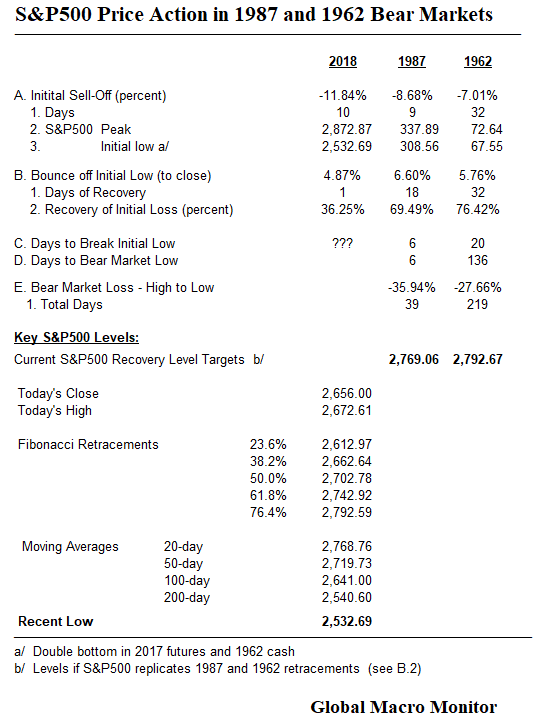

The table juxtaposes the 1987 and 1962 bear markets with the current S&P500.

The recent sell-off is several hundred basis points greater than that of the first wave of both the 1987 and 1962 bear markets, 11.84 versus 8.68 percent in 1987 and 1962’s 7.01 percent. The first leg of the bear took nine days in 1987 and 32 days in 1962 versus ten days in this recent period.

Note the first leg down of the 1962 bear also ended with a double bottom as did the current S&P500 futures.

First Bounce

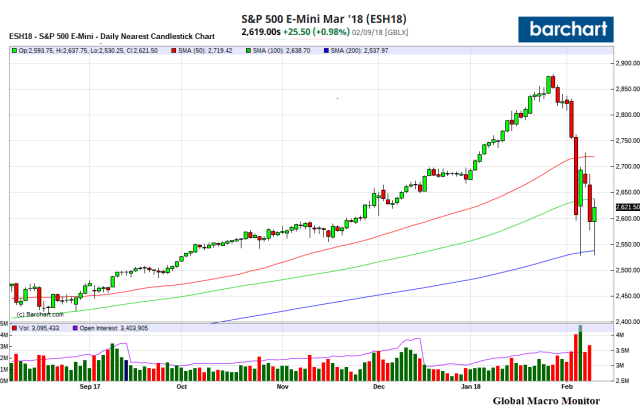

The S&P500 has thus far rebounded 4.87 percent off its Friday low, recovering 36.23 percent of its losses from the peak. It compares to the initial bounce of 6.60 percent, and a 69.49 percent recovery in 1987, which lasted 18 days; and 5.76 percent in 1962, which recovered 76.42 percent of its peak to first low loss in 32 days.

Next Leg Down

The data are still unfolding for the current S&P500.

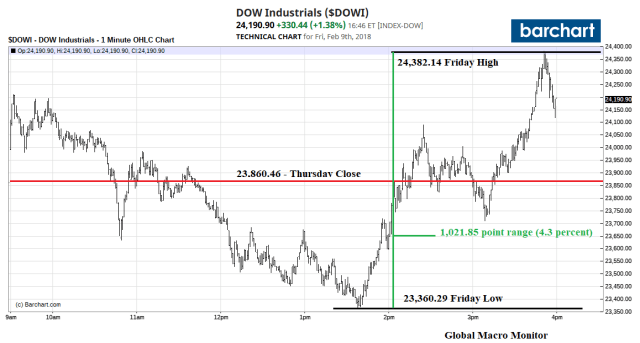

In 1987, it took six days to break the initial lows after making the swing high. The market then bounced 1.66 percent on October 13th, to close back above that low. It was the last hope and gasp of the bulls, however.

The S&P500 then rolled over hard and fell 2.95 percent, 2.34 percent, and 5.16 percent the next three days going into the eve of the crash.

The S&P500 closed down 20.47 percent on Black Monday and finally bottomed the next day.

The total loss of the 1987 bear market was 35.94 percent on S&P500 from its high to low, and lasted 39 days, 40 days and 40 nights of testing.

1962

The 1962 bear market unfolded much slower.

After the initial bounce, the S&P500 took 20 days to take out the initial low and bounced around that level for ten days then rolled over hard.

The 1962 bear market also experienced a flash crash on May 28th, falling 6.7 percent.

“The stock market careened downward yesterday,” reported The Wall Street Journal on May 29, 1962, “leaving traders shaken and exhausted.” The Dow Jones Industrial Average fell 5.7% that day, down 34.95, the second-largest point decline then on record.

“The drop took place on volume so heavy,” added the Journal, that the “ticker wasn’t able to finish reporting floor transactions until 5:59 p.m., two hours and 29 minutes after the market closed.”

…The crash of 1962 is a reminder that markets always have been messy and that investors’ morale always has been fragile. What’s more, the problems the regulators sought to solve nearly a half-century ago are still with us today. They probably will be tomorrow, too. — Jason Zweig, Wall St. Journal

The S&P500 took 136 days to bottom after breaking its initial low, beginning its rebound after the Soviets stood down during the Cuban Missile Crisis.

The 1962 bear market clipped 27.66 percent of the S&P500 and lasted 219 trading days.

Current S&P500 Target Levels

The table also shows the key levels for the current S&P500.

Most interesting are those levels which replicate the initial bounce of the 1987 bear, a 2,760.06 S&P500 and 1962, a level of 2,792. 67. The message here is not to get complacent or too lathered up as the market rallies hard off the recent low. It can go a lot further and is commonplace even in bear markets.

Noteworthy is that the S&P traded through the 38.2 fibo today but failed to close above it.

Bond Yields

We are also watching bond yields closely because their path is going to determine the direction of the stock market

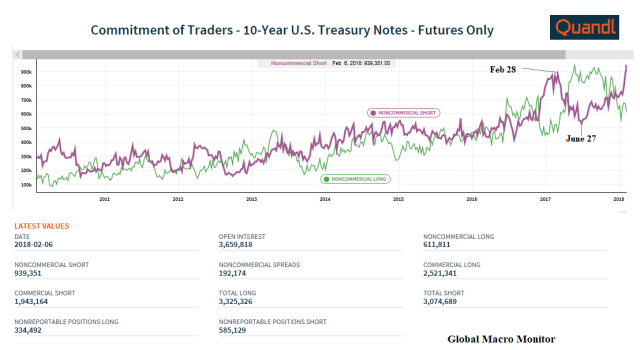

As the Quandl chart shows, the fast money crowd is significantly short 10-year note futures.

It is not always a prelude to an imminent short squeeze, however, as the 10-year note yield chart shows the fast money had pretty good timing as yields temporarily spiked at their maximum short positions.

They then had to scramble to cover their positions generating the massive squeezes.

We sense the market technicals are rapidly changing, however. The Fed is out and now running down their book. Foreigners are tepid buyers, at best.

Moreover, the increase in supply in the form of future new issuance is not insignificant. Starting to catch a whiff of concern about the U.S financing its budget deficits. Triple yikes!

Nevertheless, keep the CFTC data on your radar going into Wednesday’s CPI release. If the number misses to the downside, it could get squeezy.

Upshot

Is the stock market out of the woods?

Can’t say with certainty, but as the IMF representative in Uruguay used to respond when we pressed him if the government, who was facing elections in two months, could obtain a Fund program,

“It is possible, but not probable.” – IMF Uruguay Rep, circa…

We knew damn well there would be no deal.

Will we see a new high on the S&P500 sometime soon? It is possible, but not probable.

One Last Thing

Another take away from our data crunching exercise is that if the recent S&P low at 2,532.69 is taken out, we suspect the exits will be jammed with those trying to get horizontal, and fast. Take 1987 as your analog.

Finally, we are the first to acknowledge that though the facts may be correct, our conclusions may be wrong. Also keep that on your radar.

Good luck, folks