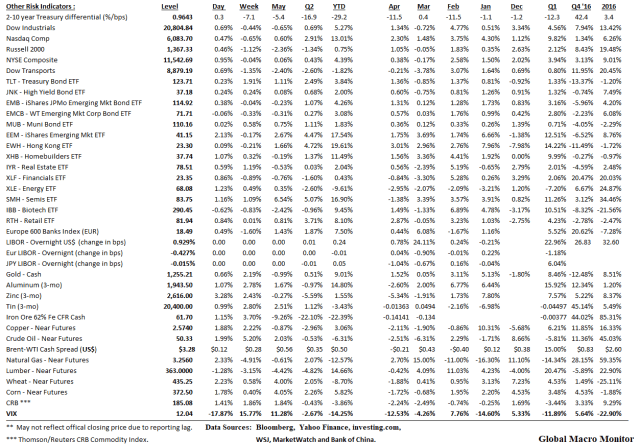

If there is one thing we have learned over the past few years, “the algos will find you out”. Add to that, always bet against the fast money crowd.

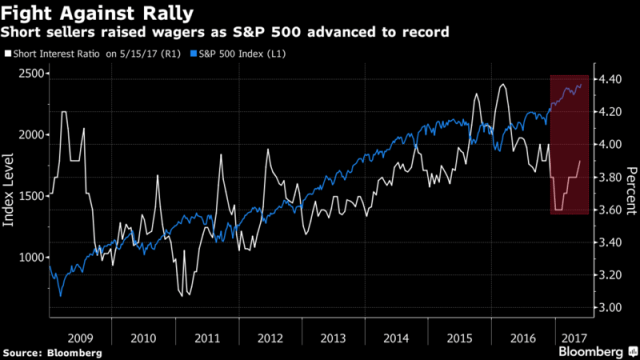

According to Bloomberg, the shorts have been upping their positions again in the S&P500. Though not yet at extreme levels.

Why not just wait for the break? That day will surely come. Maybe soon or maybe later.

And why short a trending bull market? Maybe for a scalp, but a trending market, which looks like it is starting to break out of a consolidation? Are you out of your freaking mind?

Stocks Are Expensive

Absolutely stocks are expensive, but nobody knows when the bull market will end. Alan Greenspan gave his “irrational exuberance” speech 3 1/2 years before the market topped. Stocks are expensive for a reason.

Too Much Liquidity

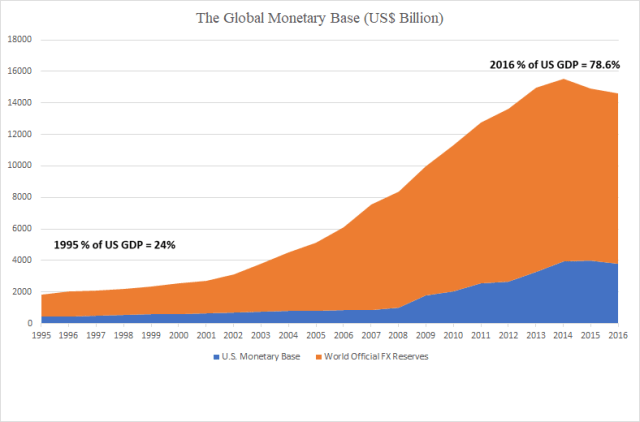

There is so much liquidity and money in the U.S. financial system today versus any time in history. Markets just aren’t functioning normally. Therefore the default scenario for the markets are lower than normal interest rates and higher than normal asset valuations.

We have estimated a global liquidity concept called the “global monetary base” which is simply the sum of the U.S. monetary base and the world’s official foreign exchange reserves. Since most of the official FX reserves — about 65 percent — are held in dollars most of the global monetary base is in the U.S. financial system.

Note that in 2007 the global base was at about 50 percent of U.S. GDP compared to almost 80 percent at the end of 2016. — Global Macro Monitor, April 26, 2017

.

If you don’t believe us, go ask the bond market vigilantes, for example, if there are any still alive. Let us know, by the way, if you can find one.

Technological Advances

Not to mention the rise in algorithmic and HFT trading that are notorious for setting short-term bear and bull traps. And how about those trading ‘bots that spoof the bid and the offer and probe the market until they find the real buying or real selling then quickly reverse?

There will come a day when all this new technology short circuits and creates a 1987-like flash crash. Please tell us that date, however.

Where Will The Real Sellers Come From?

Who is going to sell stocks unless we have some catalyst and Black Swan event? A global military conflict, or, say, a series of surprise 3-4 percent inflation prints that set off panic rate hikes and Fed rapid balance sheet reduction, for example — both, of which are pretty much unpredictable. Or maybe something like our Six Sigma political event?

By the way, the South Korean Kospi stock index is up over 16 percent and the currency has strengthened over 7 percent versus the dollar year-to-date, all while the missiles continue to fly up north. Talk about climbing a real “wall of worry.”

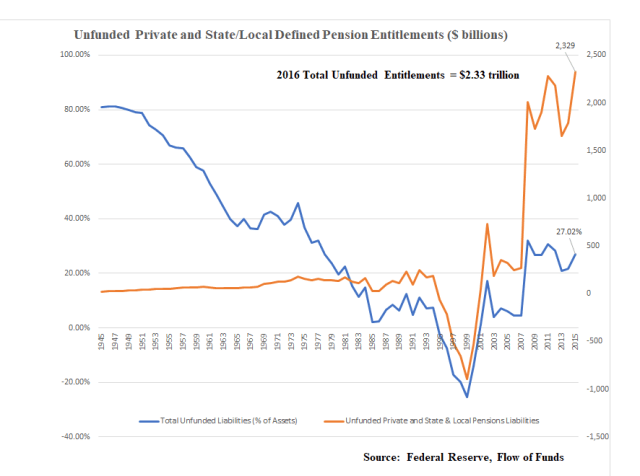

Pension Funds Underfunded

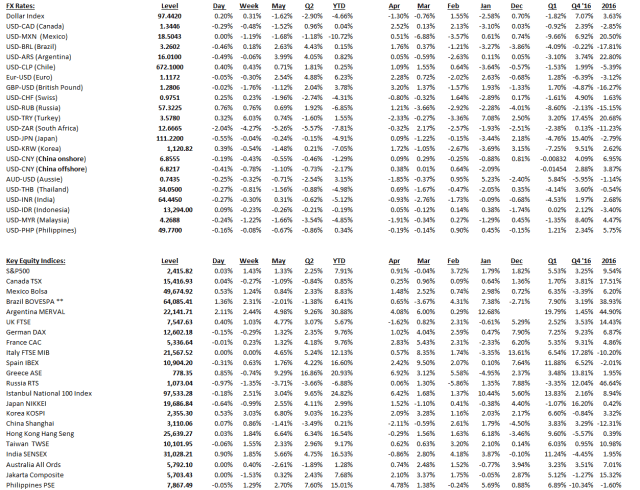

Unfunded pension fund entitlements are going parabolic and their managers have no choice but to reach for yield and return and, definitely, will not find it sitting in cash or the 10-year at 2.25 percent.

Earnings Resurgence

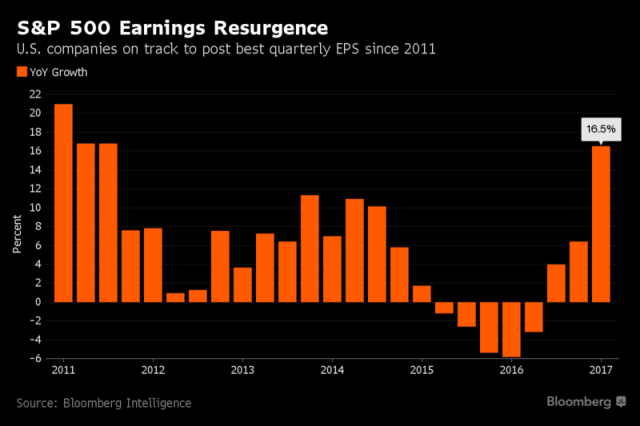

The U.S. stock market has just emerged from an almost two-year earnings recession — granted much ado about crude oil prices — but the S&P500 has kept moving higher.

Now the fundies are turning, earnings are increasing — even on the top line — albeit at higher stock prices. Stocks don’t trade levels, but on first and second derivatives of those levels.

Capital Flows

So we ask you, folks, where is the global flood of money going to go? Could be “money heaven” if all markets crash if they wake up one morning and decide to reprice and regress to their mean longer-term valuation levels. Good luck on that.

A global margin call like 2007-08 as housing credit began to contract? Not there and nowhere near the economy wide credit growth we saw in the early to mid-2000’s.

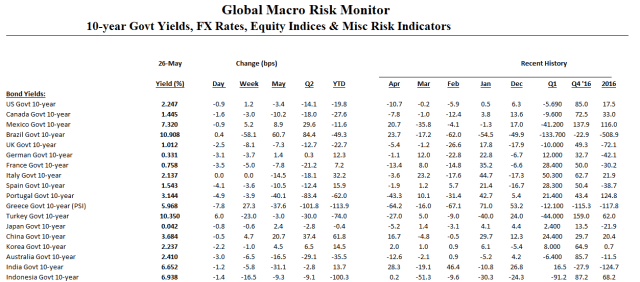

German 10-year bunds at .35 percent? The Japanese 10-year JGB at .04 percent? The 10-year U.S. T-Note at 2.25 percent (though attractive relative to European and Japanese bonds, which keeps the 10-year note well anchored below 2.60 percent)?

Though credit expansion has been relatively lackluster or weak recently, just imagine if velocity starts to reverse and the banking system really begins to extend credit. This will create an additional tidal wave of money, albeit leveraged, and a subsequent further boost to asset and real inflation. The upside scenario, but most likely a lower probability event, in our opinion.

Risks

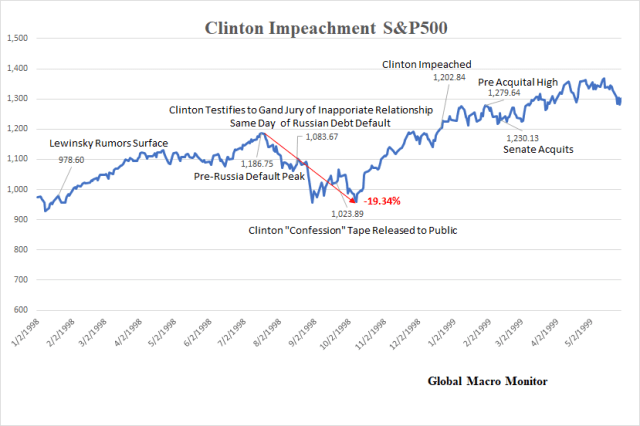

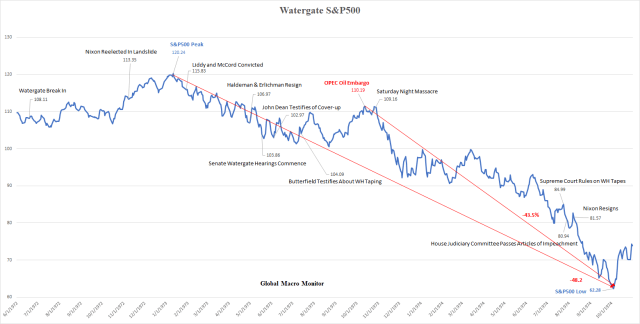

The impeachment trade? In the words of President Obama, “come on, man!” Presidental scandals alone are not sufficient to crush stocks. Hope you read our piece, Beware Shorting Impeachments.

If the Trump agenda stalls into year-end, this will only increase the risk and our conviction of an October correction. But Republicans may fear losing the House in 2018 and move to the “two-minute” drill trying to expedite legislation.

Don’t get us wrong, we are not raging bulls, are relatively bearish medium to long-term, and at these valuation levels not expecting blockbuster returns for the rest of the year. Just kind of a boring summer trading range that slowly drifts higher and shorts are forced to cover. Once again.

A relatively larger cash position in the event of a correction? Understandable, for sure.

Pain Trade

Maybe the increase in shorts is a pairs trade, say, shorting the S&P500 against emerging market or European stocks. Nevertheless, the pain trade is higher for S&P500, in our opinion, and the shorts will once again have their family jewels caught in a vice that slowly tightens in on them.

Ouch! We have been there many times.

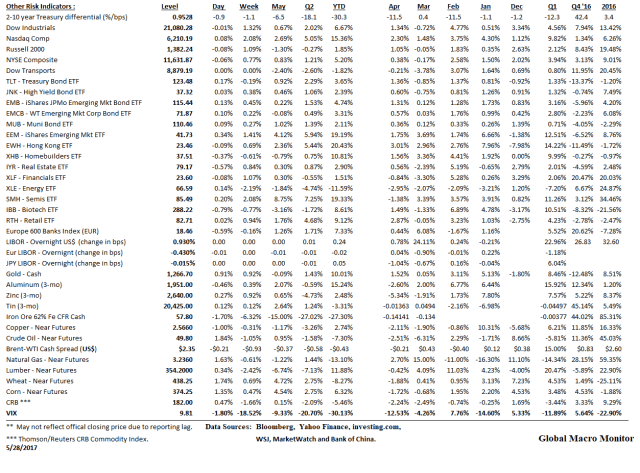

The challenge for short sellers is how long they can stay solvent before being forced to buy back the shares that they have borrowed and sold. And the pressure to cover is building. A Goldman Sachs Group Inc. basket of most-shorted stocks has jumped 6 percent this quarter, almost triple the return in the S&P 500. – Bloomberg, May 26, 2017

And beware of the “seek and destroy bots“, Mr. Short.

Conclusion

Patience, our friends, until the global central banks start draining the swamp or the Fed funds rate hits a tipping point — we think at around 3-4 percent if no Fed balance sheet reduction.

Those kind of rates will do some ugly damage to the U.S. budget deficit with higher interest payments on a much larger debt stock, which will beget an even higher debt stock and ever higher interest payments and larger budget deficits. A nasty positive feedback loop and we are not so sure the Fed will allow it and will thus choose to begin to reduce their balance sheet instead.

Nobody Knows Mr. Market

The bear market can start next week, or in five years. We have no idea, nor does anyone else. Though we do expect a nice buying opportunity in the fall.

Some expect the Fed may begin to reduce their balance sheet in the fall, China’s 19th National Congress of the Communist Party will conclude in October and the country’s economic policy put will implicitly expire. Then a possible nasty economic or policy surprise out of China creating a catalyst for some temporary global risk aversion. Maybe.

We just don’t think we have topped quite yet.

Professional money managers are not paid to sit with high cash levels and shorts, as you know, are an impatient lot.

Calculated risk and good money management, comrades. Stress test those old sleeping dogmas. Remember, asset bubbles don’t easily pop. That is until they do.