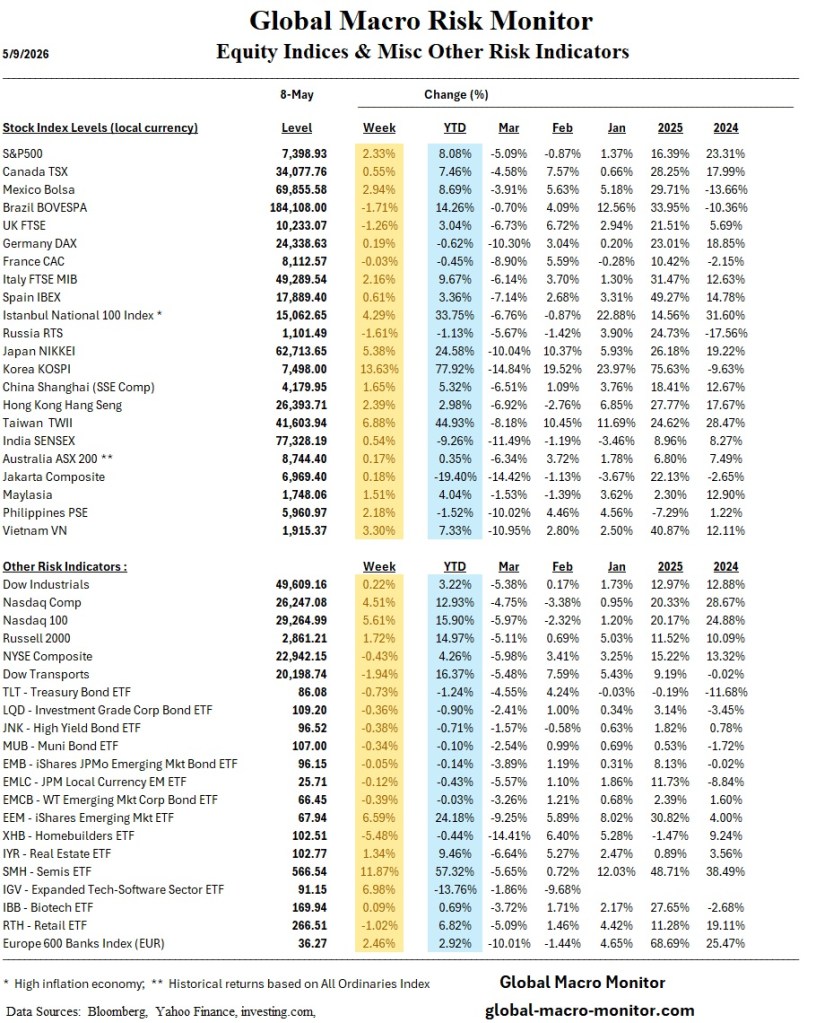

No commentary this week but Wow! Look at Korean stocks.

No commentary this week but Wow! Look at Korean stocks.

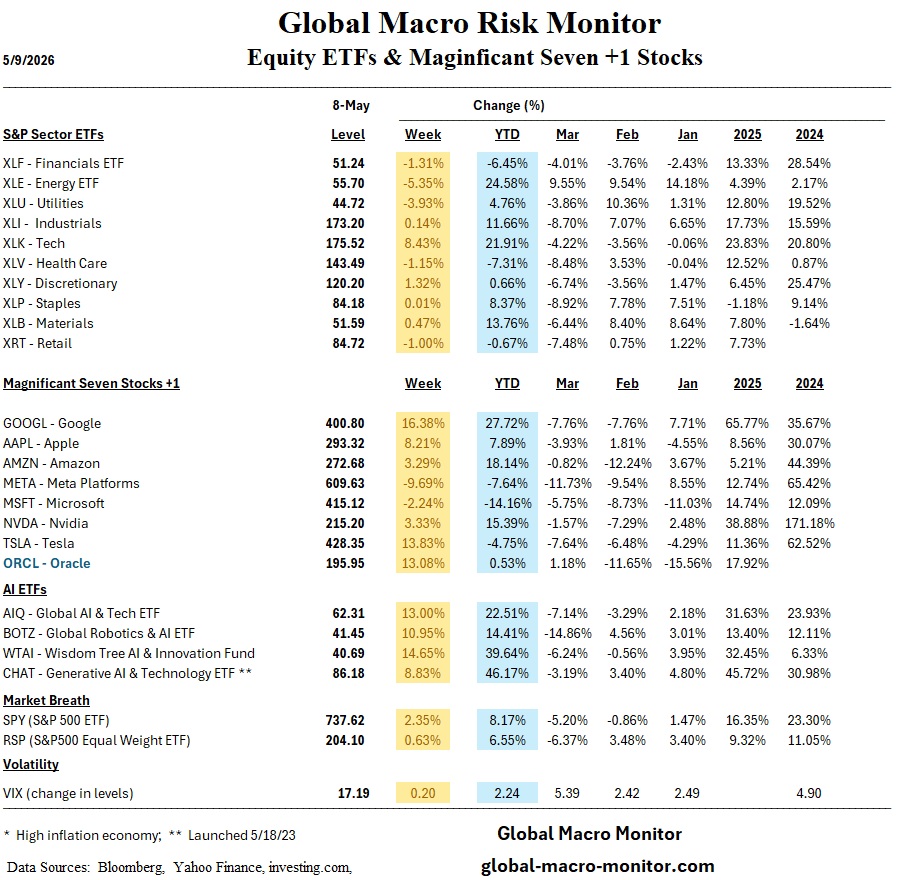

In 2026, the age-old investment rule that “rising oil kills transport stocks” has seemingly been thrown out the window. While WTI crude has skyrocketed 70% year-to-date, a massive cost headwind for airlines and truckers, the Dow Jones Transportation Average (DJTA) has defied gravity, posting significant gains.

But look closer at the index’s mechanics, and you will encounter the “Avis Distortion.” Unlike the market-cap-weighted S&P 500, the DJTA is price-weighted. This means that high-priced stocks carry a disproportionate influence on the index’s total movement, regardless of the company’s actual size. With Avis Budget Group (CAR) undergoing a parabolic short squeeze, its surging share price has effectively propped up the entire index.

Analytical estimates suggest that this single stock’s volatility is responsible for roughly 30% of the index’s YTD point gains. Once you strip away this liquidity-driven anomaly, the true “health” of the broader freight and logistics sector looks far more modest.

Investors relying on the DJTA as a barometer for economic strength should exercise caution. This rally isn’t purely about demand; it is a technical artifact. Distinguishing between genuine operational growth and the Avis Distortion is essential to reading the market’s true pulse.

Big Tech’s Moment of Truth: What to Watch This Week

Investors are bracing for a high-stakes week as the market enters a pivotal stretch defined by two major narratives: the “Magnificent 7” earnings bonanza and Jerome Powell’s penultimate Federal Reserve meeting.

With five of the seven tech giants set to report this week, the focus has shifted dramatically. The debate is no longer just about whether AI demand is real enough to justify massive infrastructure spending. Instead, Wall Street is demanding proof of the Return on Investment (ROI). Analysts will be scrutinizing everything from cloud growth and advertising durability to how these companies are translating massive data center expenditures into bottom-line results. Given that these seven companies now account for over half of the Nasdaq 100’s weight, any earnings disappointments could trigger significant volatility across broader indices.

Simultaneously, all eyes are on Jerome Powell as he nears the end of his tenure as Federal Reserve Chair. As the Fed holds its latest meeting, market participants are looking for signals regarding the path forward for monetary policy in an environment where economic resilience remains the dominant trend.

In short, this week will test whether the current market optimism holds up against the realities of corporate profitability and central bank policy.

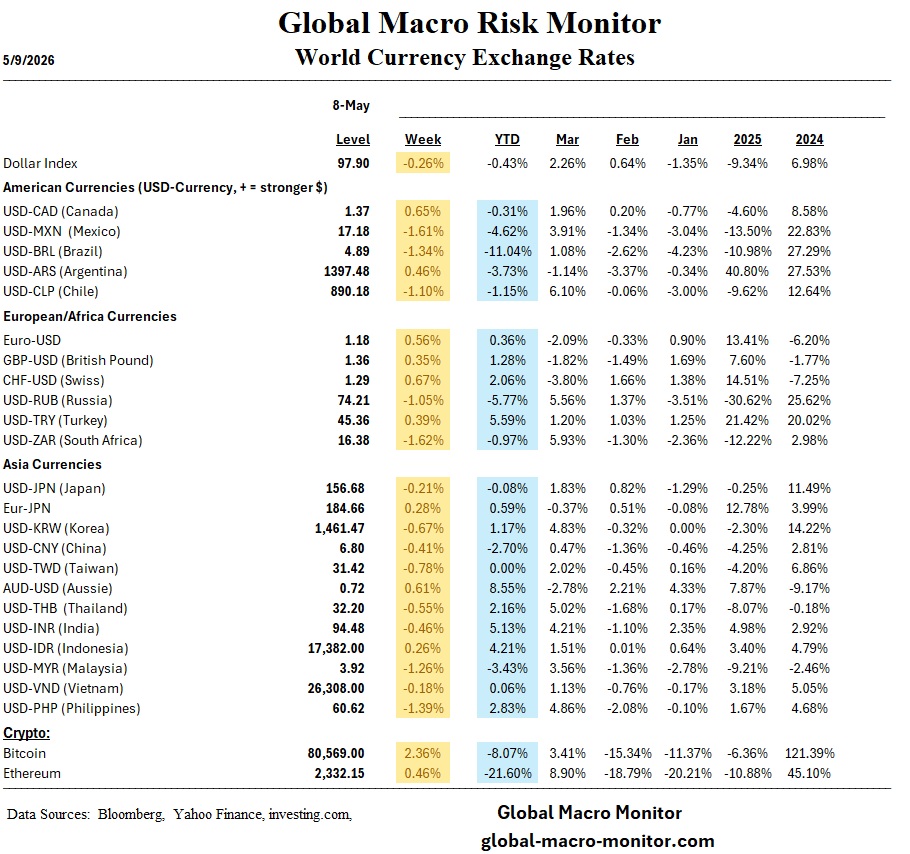

Markets are currently behaving with the volatile, erratic energy of a teenager on a sugar high, oscillating between “the war is over” euphoria and the sobering realization that geopolitical stability is currently being drafted on a napkin in a war room. The headline-driven rally has been a masterclass in price discovery through chaos. Markets priced out aggressive rate hikes and sprinted toward record highs on the premature assumption that a ceasefire between Israel and Lebanon, coupled with a pledge to open the Strait of Hormuz, meant the geopolitical risk premium was dead.

Of course, the reality of the weekend was far less cooperative. Iran’s Revolutionary Guards promptly declared the Strait closed again, citing the continued U.S. blockade on Iranian ports, a maneuver the Guards termed “strict control”. President Trump, playing his part in this theater with characteristic flair, dismissed the Iranian maneuvers as “getting a little cute” while simultaneously maintaining the very blockade that necessitates the closure. It is a delightfully circular logic: the U.S. blockades ports to choke off funding, Iran retaliates by choking off shipping, and the market spends the weekend sweating the resulting oil price volatility.

Forecasting in this climate is essentially a parlor game for the desperate. When price action is dictated by whether a foreign minister or a President decides to tweet or hold a press conference, “fundamental analysis” feels like an exercise in nostalgia. The suspicious efficiency with which some desks seem to position ahead of these policy flip-flops suggests that the “insider trading” playbook is not just alive and well,but thriving in the current volatility. We are seeing a market that wants to believe the oil price shock is “short-lived,” yet the technicals, specifically the extreme RSI overbought readings across major indices, suggest that we may have outrun our own shadow. Caution is not just warranted; it’s likely the only thing preventing a catastrophic exit when the next headline inevitably spoils the party.

Regional Performance Bullet Points

The Week Ahead

The consensus for the coming week is leaning toward a “profit-taking” pullback. We are technically overbought, and the market’s propensity to assume a best-case scenario regarding the Strait of Hormuz feels like an accident waiting to happen.

Bottom line: The current risk-on stance is fragile. With the Strait of Hormuz situation still unresolved and technical indicators flashing warning signs, we are leaning into a “Slight to Moderately Bearish” posture for the week.

QOTD: Quote of the Day

“Markets are not properly pricing risk, because they really don’t have to. They have assumed that the U.S. government will not allow them to implode, and that assumption is putting the world economy at stake.” – Kyla Scanlon, NY Times

“Moral hazard” is a concept in economics and insurance referring to a situation in which an individual or institution takes on greater risk because the negative consequences of that risk are partially or fully borne by others. This shift in behavior arises when protection—such as insurance coverage, government guarantees, or bailouts—reduces the incentive to act cautiously, thereby distorting decision-making and potentially leading to inefficient or reckless outcomes

The term ‘Amen Corner’- used to describe the series of holes around the 11th, the par three 12th and 13th holes – was first used in print by author Herbert Warren Wind in an issue of Sports Illustrated in 1958. However, in another piece 26 years later, he revealed that 1930’s jazz number entitled ‘Shoutin in that Amen Corner’ was his inspiration. – Golf 365

Read the full article here

Brothers and sisters we got hypocrites in this crowd

Brothers and sisters some of you are shoutin’ too loud

You’ll find out on judgment day you can’t fool the Lord that way

Brothers and sisters hear all I’ve got to say

You can shout with all your might but if you ain’t livin’ right

There’s no use shoutin’ in that amen corner

If your name on that roll all that noise won’t save your soul

So stop your shoutin’ in that amen corner

Just because you’ve paid your dues doesn’t mean your saved

You can’t win them golden shoes if you haven’t behaved

you better think before you shout for your sins will find you out

So stop that shoutin’ in that amen corner

I can’t hear my own self praechin’

For your shoutin’ and your screachin’

You make me forget my text

Every meetin’ leaves me vexed

Why you come here and pray on Sunday

Then you serve the devil Monday

If you want to save your soul

Better get some self control

You can shout with all your might but if you ain’t livin’ right

There’s no use shoutin’ in that amen corner

If your name on that roll all that noise won’t save your soul

So stop your shoutin’ in that amen corner

Shoutin’ here don’t mean a thing if your playin; with fire

Change your ways or you won’t sing in that heavenly choir

Makes no difference how you look if your record ain’t in that book

You’ve heard my preachin’ every one

so put old satan on the run

So stop that shoutin’ in that amen corner

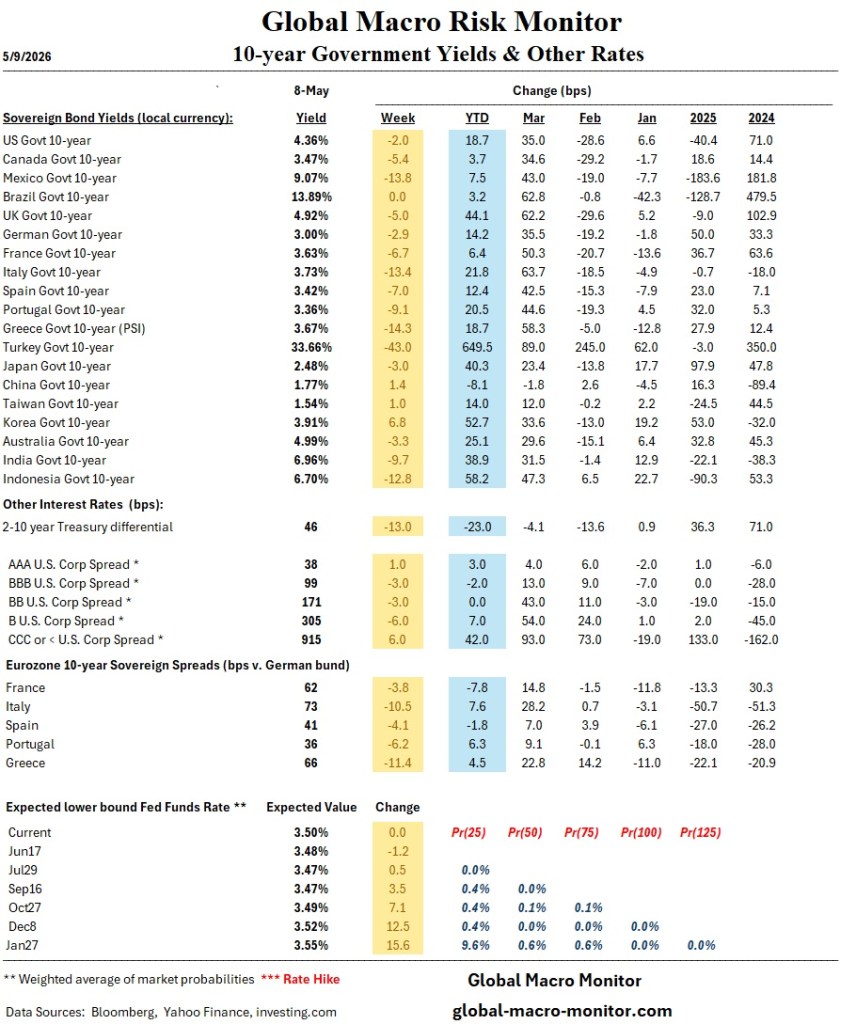

The global oil market is currently flashing a “code red” for portfolio managers and energy traders. While headline futures remain relatively anchored, the physical market is screaming of a systemic shortage. As reported by the Financial Times, a desperate scramble by European and Asian refiners to secure immediate supplies has catapulted North Sea physical prices to historic levels, fueled by Iran’s ongoing blockade of the Strait of Hormuz.

The $50 Basis Gap The most striking indicator of this crisis is the unprecedented decoupling of physical barrels from paper benchmarks. Forties Blend—a critical marker for immediate delivery—surged to nearly $147 a barrel this week. To put that in perspective, while the Brent June futures contract hovers around $97, the physical “Dated” Brent is trading at a staggering premium of roughly $50. This is no longer a speculative play; it is a frantic hunt for molecules.

Exchange Infrastructure Under Strain We are witnessing a rare breakdown in market mechanics. The volatility in Brent Contracts for Difference (CFDs)—the primary tool for hedging the gap between immediate and future delivery—became so extreme that prices breached the Intercontinental Exchange’s (ICE) reporting thresholds. With CFD spreads exceeding $30, the exchange essentially hit a circuit breaker, forcing trading into the less transparent “over-the-counter” (OTC) shadow markets. For hedge fund managers, this loss of price discovery and liquidity in standard hedging instruments is a significant red flag.

Geopolitical Disconnect Despite optimistic rhetoric from Washington suggesting that Iranian transit will resume “very quickly,” the data tells a different story. Goldman Sachs reports that exports through the Strait of Hormuz are currently at a mere 8% of normal levels. The vulnerability is most acute in Asia, where 80% of petroleum imports rely on this waterway.

The supply side is facing a “perfect storm.” Beyond the Hormuz bottleneck, Saudi Arabia’s capacity has been slashed by 600,000 barrels per day following strikes on the Khurais and Manifa fields, and the East-West pipeline—a vital bypass route—has seen its throughput crippled.

The Macro Outlook Portfolio managers should prepare for a prolonged “physical-first” rally. Even if a diplomatic breakthrough occurs tomorrow, experts warn it will take at least 20 days to resolve the logistical backlog. As Helima Croft of RBC Capital Markets aptly noted to the FT, futures are currently a “lagging indicator” for the grim realities of Middle Eastern waterways. In this environment, the physical market is the only truth-teller.

“Here it comes. Oh my goodness. In your life have you seen anything like that?” — Vern Lundquist, 2005 Masters