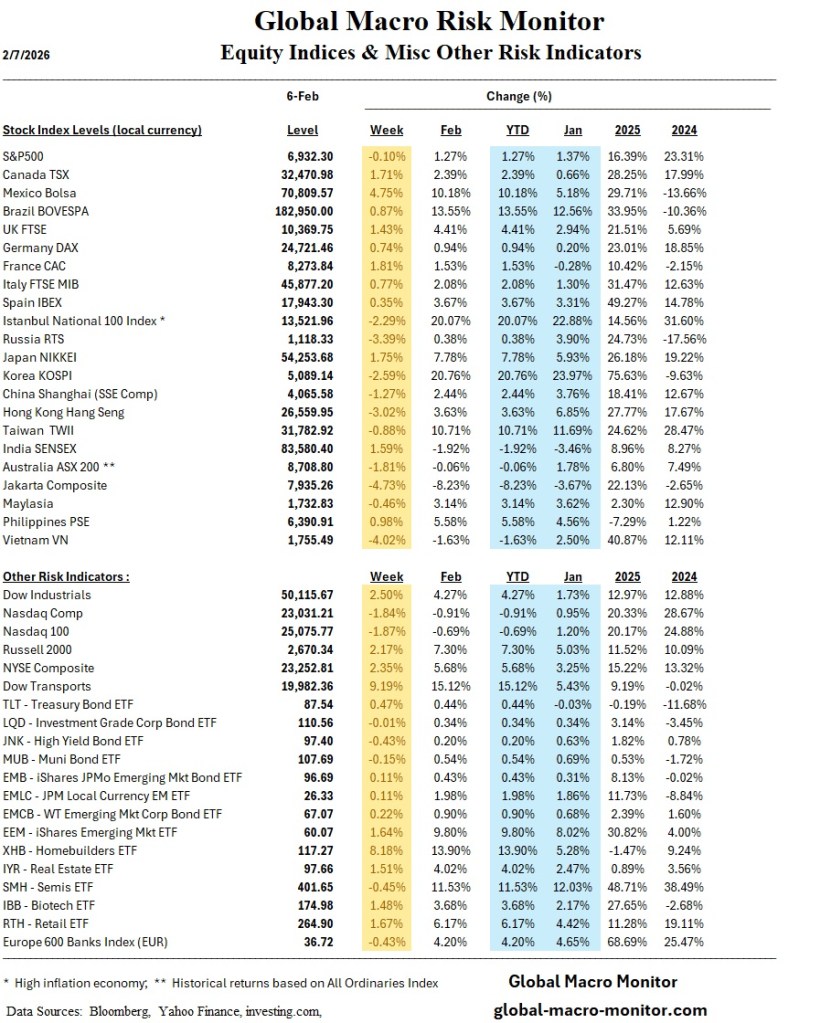

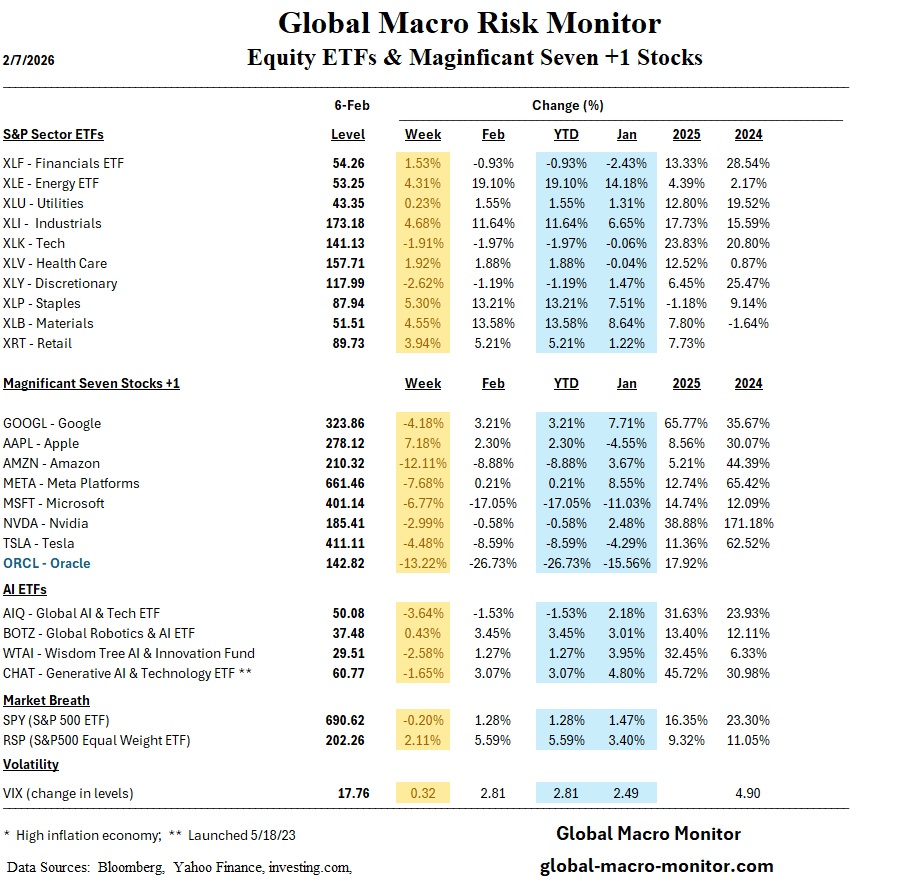

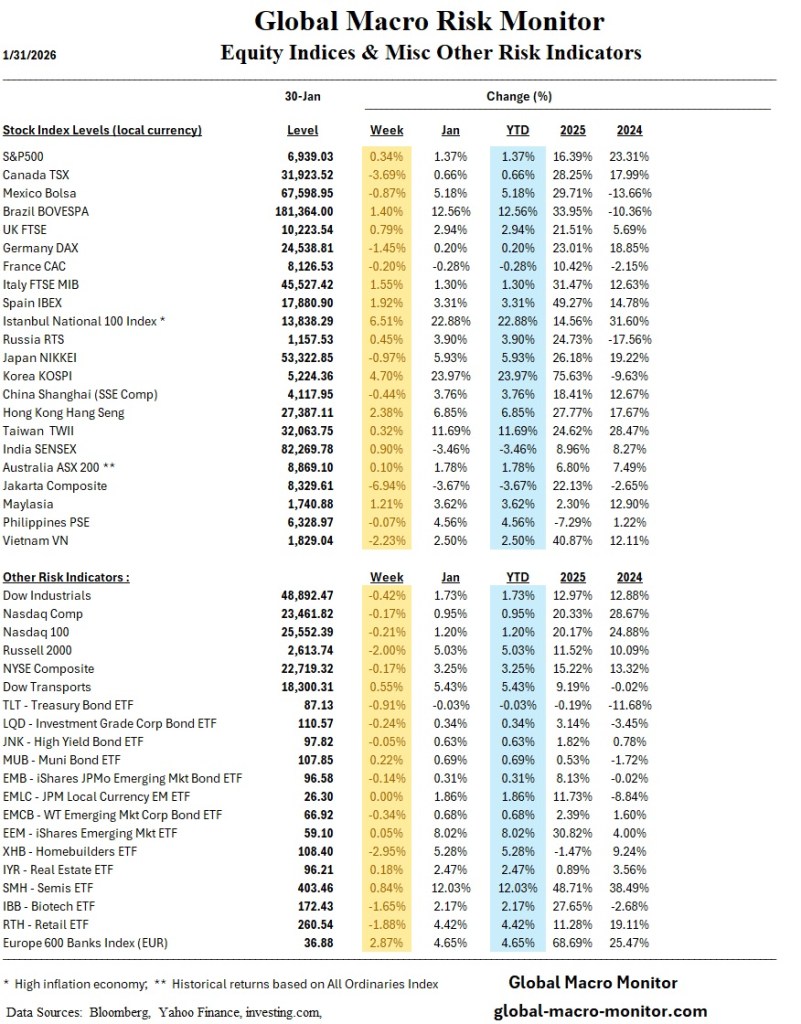

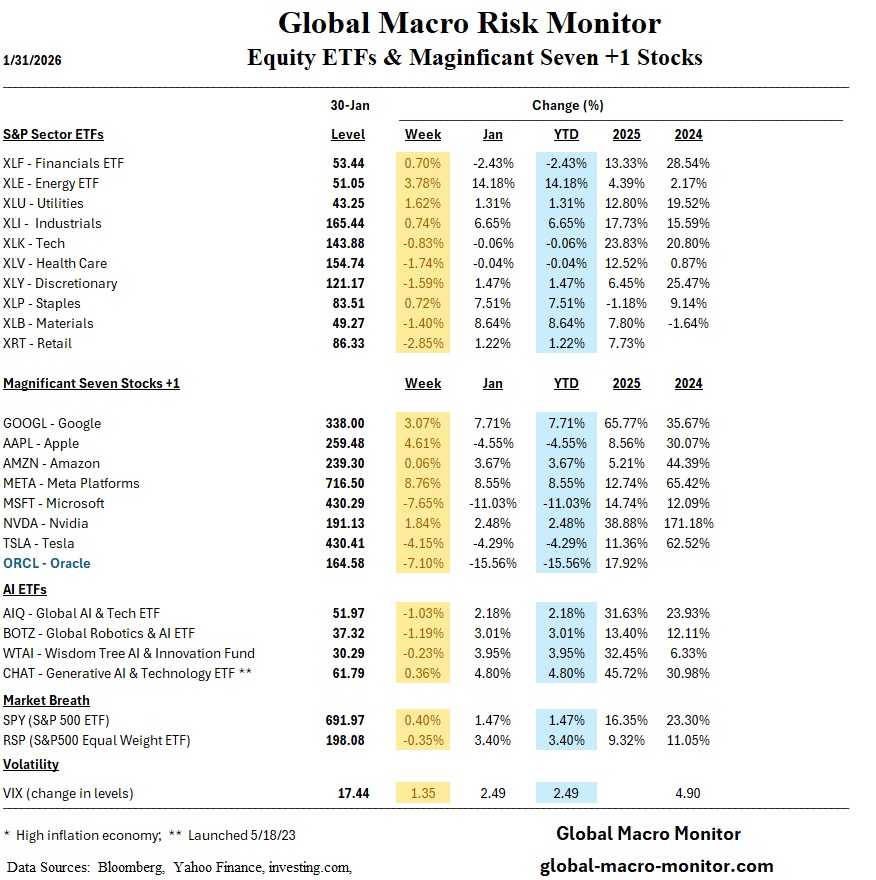

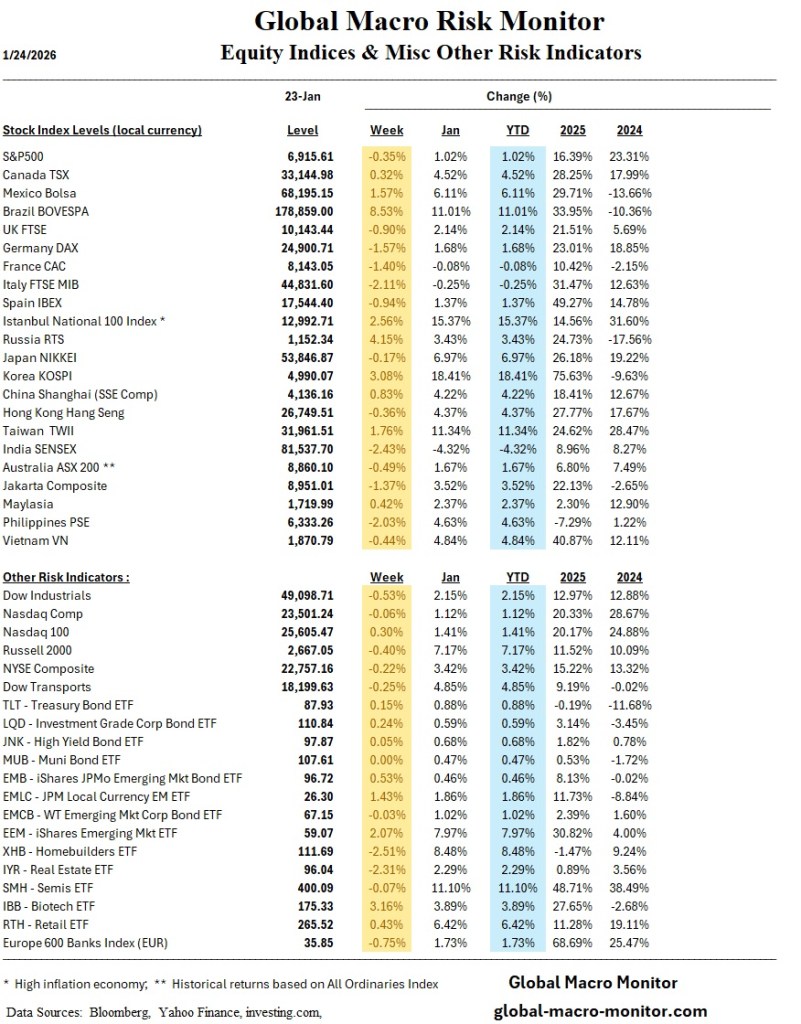

January market action reflects a clear rotation away from narrow mega-cap leadership toward broader equity participation, a shift that is both cyclical and allocational in nature. Small-cap stocks have emerged as standout performers, with the Russell 2000 and S&P MidCap indices significantly outperforming large-cap benchmarks. Most notably, the S&P 500 Equal Weight Index has outpaced the cap-weighted S&P 500 by nearly a factor of three, underscoring a broadening of market leadership rather than a deterioration in risk appetite

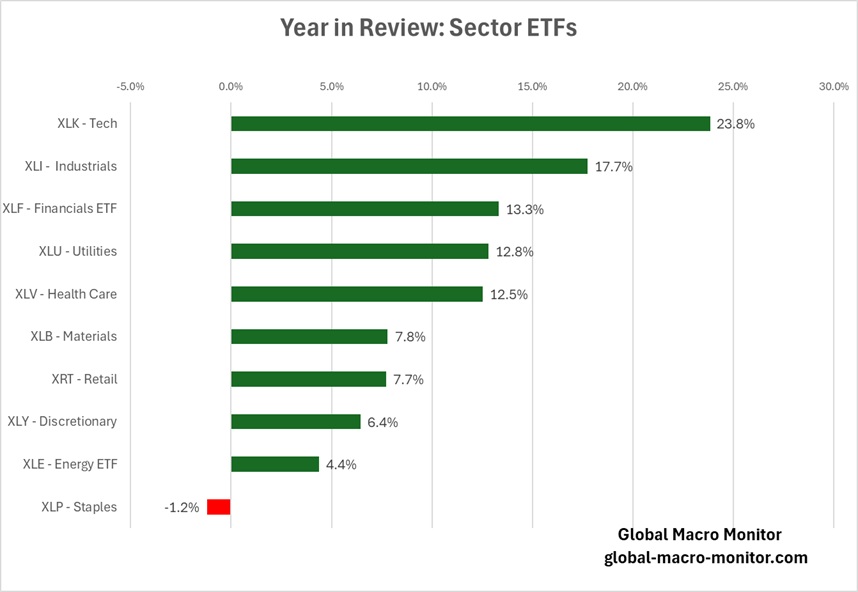

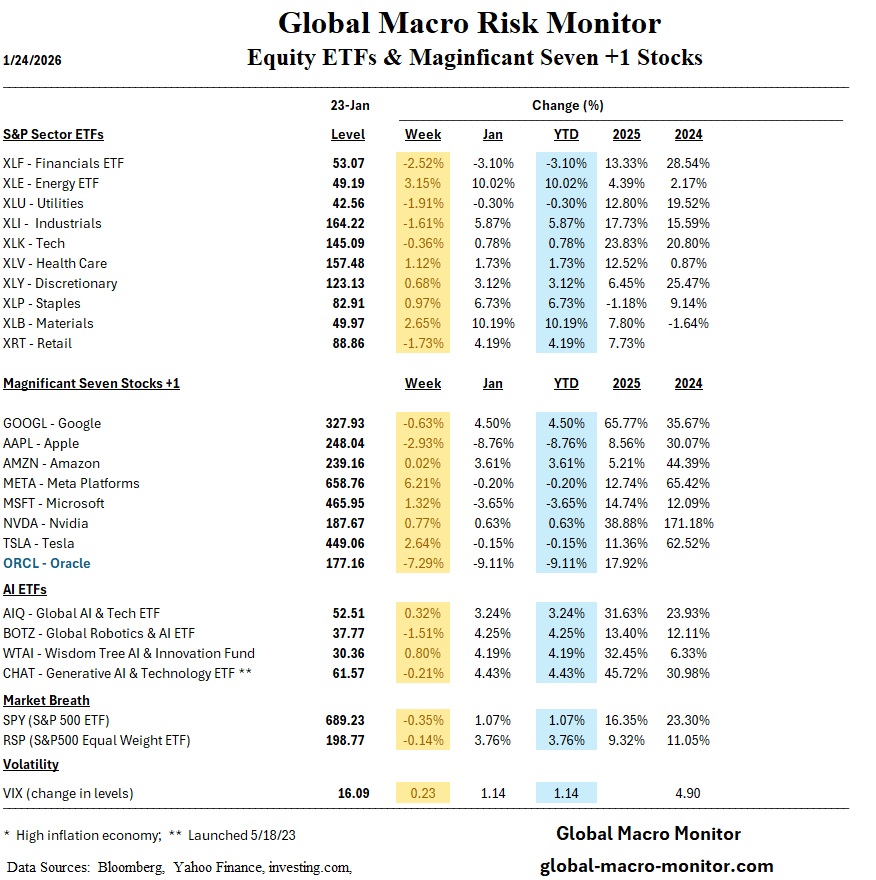

In contrast, technology—particularly AI-adjacent software and select mega-cap names—has lagged, as investors reassess valuation risk, competitive disruption from generative AI platforms, and the sustainability of earnings dominance. This underperformance appears less like a regime shift and more like early-year portfolio rebalancing, as institutional allocators rotate exposure following an outsized 2025 tech rally.

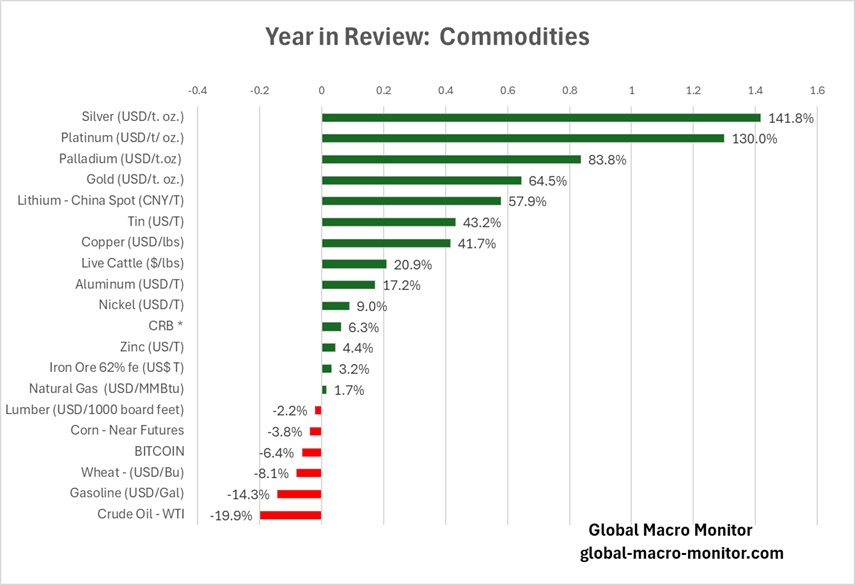

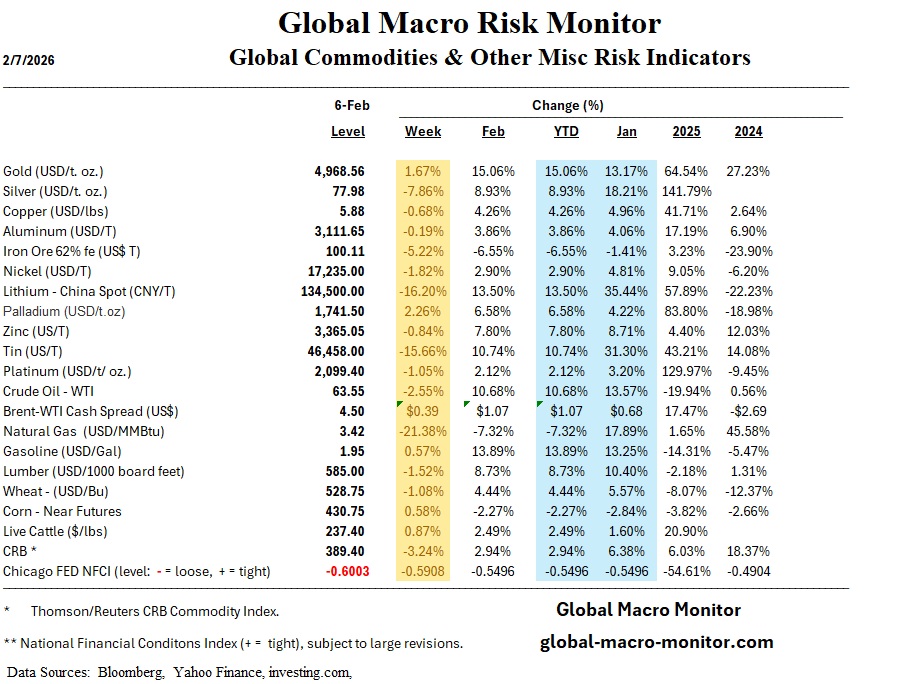

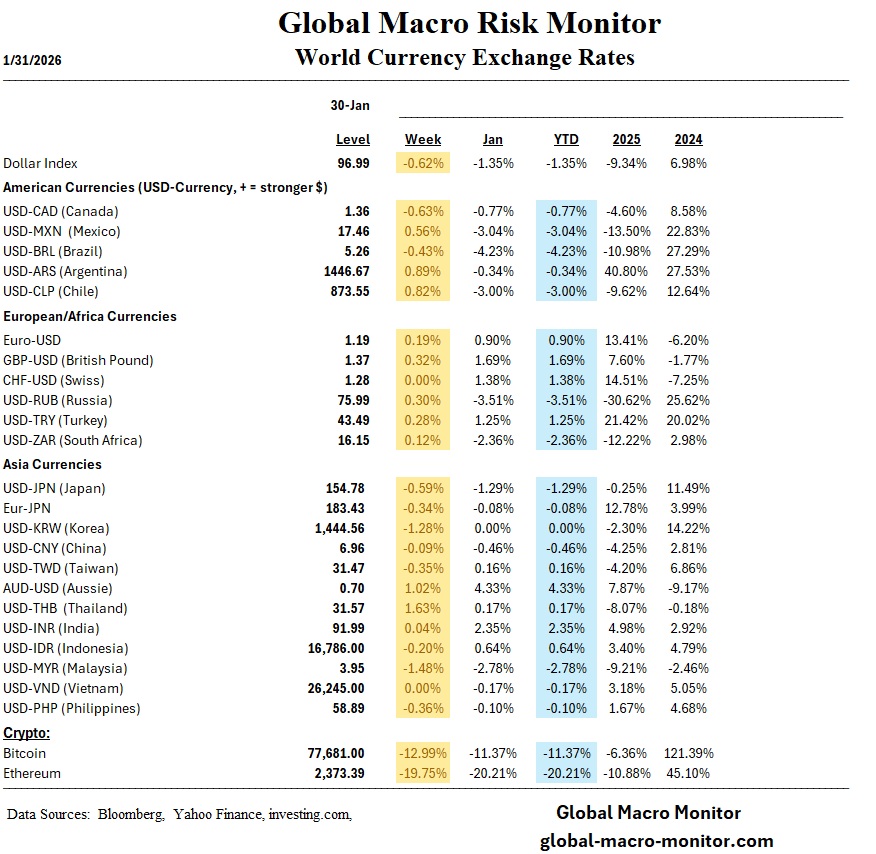

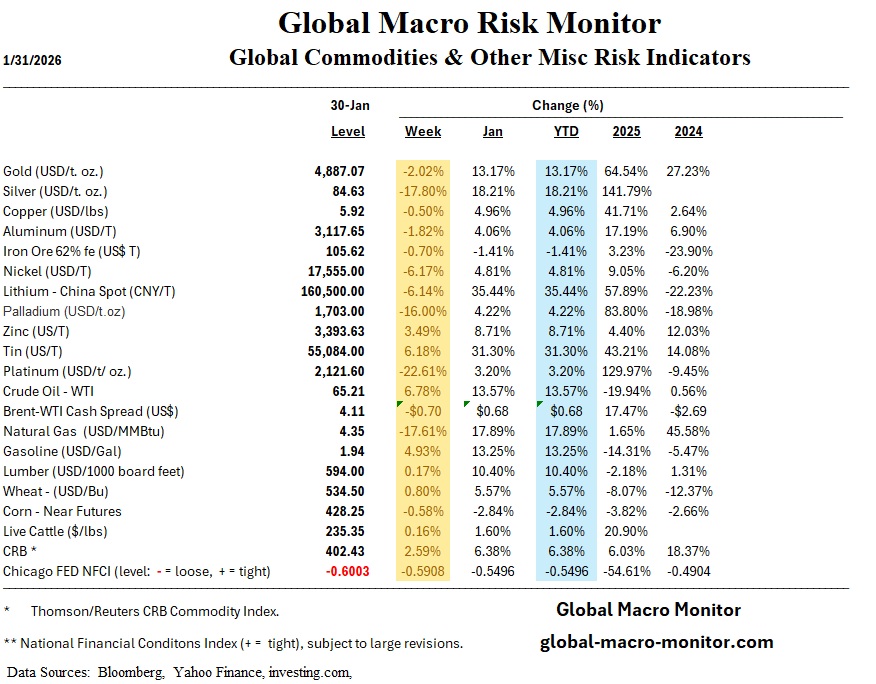

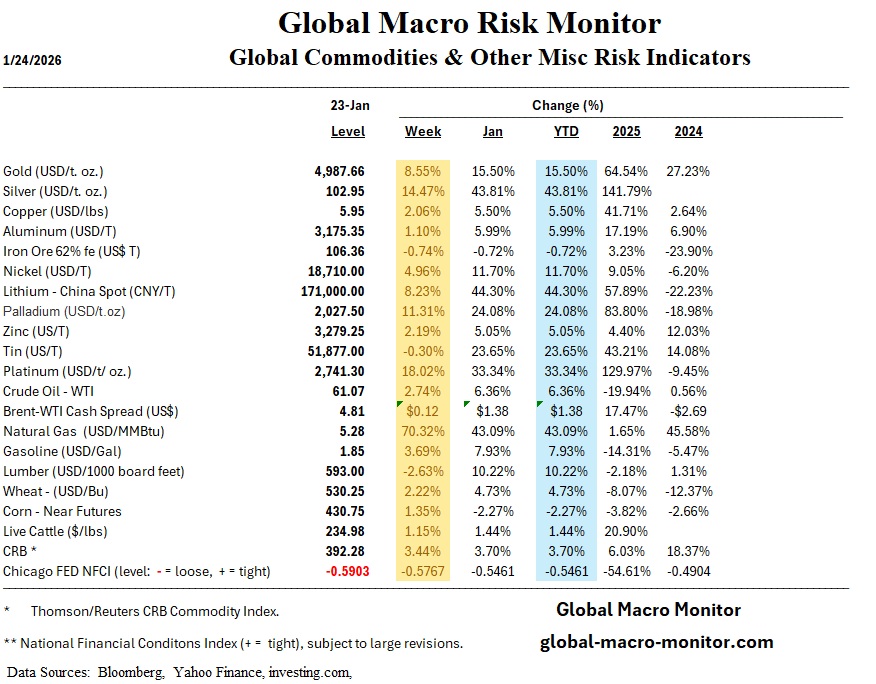

Outside equities, silver prices surged an extraordinary 25% in January, reflecting renewed interest in real assets amid geopolitical uncertainty, easing inflation momentum, and strong industrial demand signals. Lumber prices also jumped sharply, hinting at nascent reflationary and construction-related demand.

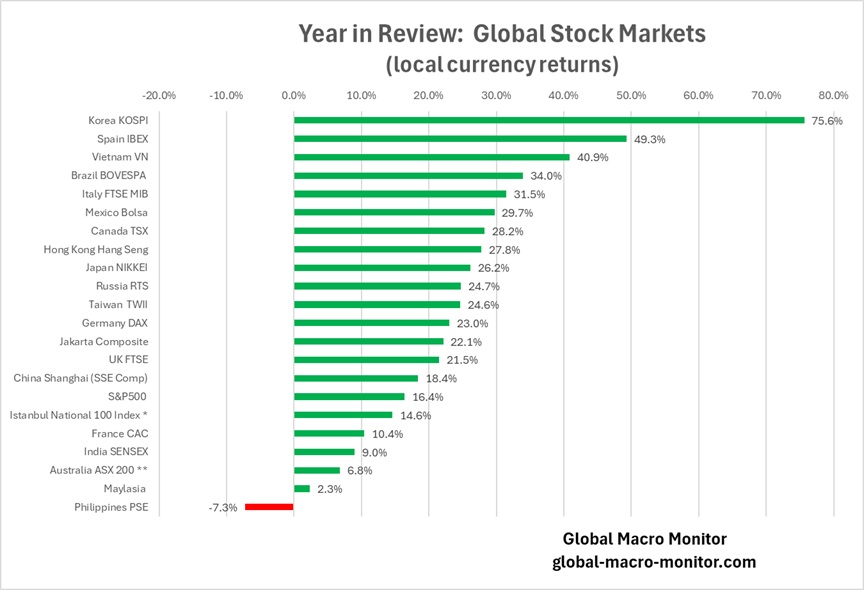

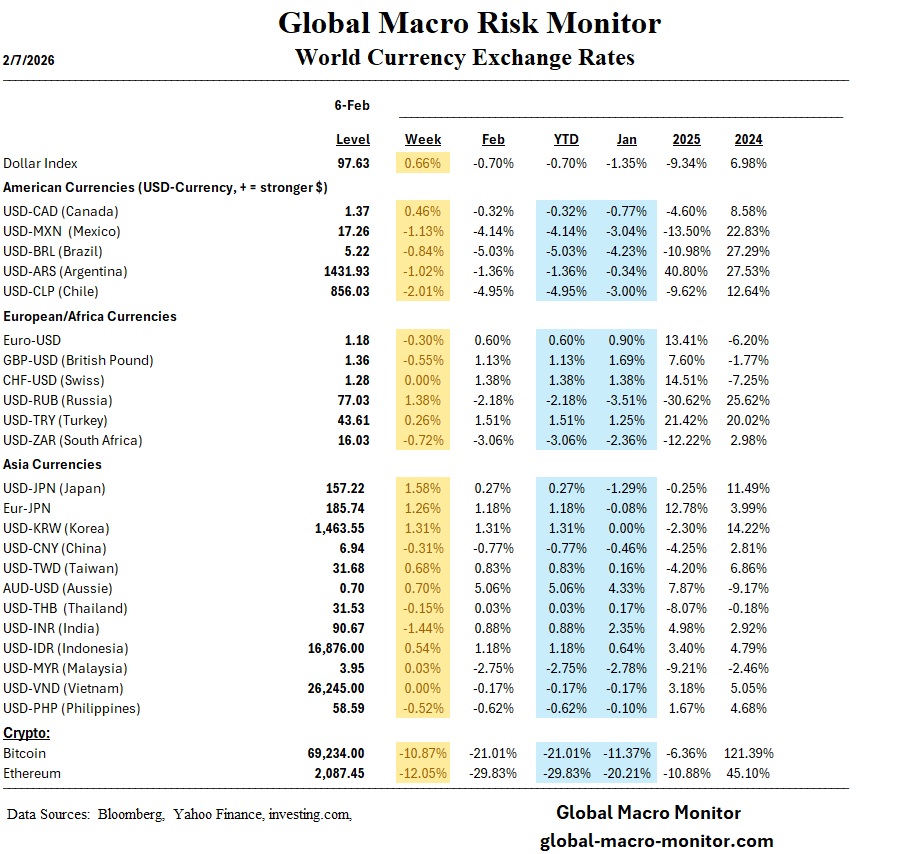

Geographically, Asia stands out as the strongest regional performer, with Korea, Indonesia, Japan, and the Philippines delivering impressive equity gains, supported by currency dynamics, export resilience, and improving domestic growth expectations. Overall, January’s market behavior signals rotation, not retreat, a constructive but fragile setup heading into a policy and data-heavy February.

Global Market Strategy Analysis

Cross-Asset Market Signals

-

Equity leadership is broadening, with small caps and equal-weight indices leading performance rather than mega-cap concentration

-

S&P 500 Equal Weight Index outperforming cap-weighted S&P by ~3x YTD highlights healthy internal market breadth

-

Technology and AI-linked equities lagging, particularly software, as valuation sensitivity rises

-

Silver +25% in January, signaling renewed inflation hedging, industrial demand optimism, and geopolitical risk pricing

-

Lumber prices surged last week, reinforcing early-cycle and reflationary signals

Equity Rotation & Style Dynamics

-

Small caps “rocking” after prolonged underperformance in 2025

-

Rotation appears allocational rather than fundamental, driven by:

-

Early-year portfolio resets

-

Valuation dispersion

-

Catch-up trade dynamics

-

Too early to declare a lasting regime change; positioning is likely still fluid

-

AI enthusiasm remains structurally intact

- Software names under pressure amid disruption fears

- Mega-cap tech is experiencing valuation digestion

- Semiconductors are more resilient than software, supported by infrastructure demand

Likely near-term consolidation before selective re-entry

Regional Equity Performance

Asia – Clear Outperformance

-

Japan: Strong equity rally on fiscal stimulus expectations and yen weakness

-

Korea: Semiconductor exports and improving global demand are driving gains

-

Indonesia & Philippines: Benefiting from EM capital inflows and domestic growth resilience

-

Asia ex-China continues to attract incremental global capital

Europe

-

Modest gains, supported by easing inflation but capped by weak growth momentum

United States

-

Rotation-driven gains beneath flat headline indices

-

Value, small-cap, and cyclical exposure outperforming growth

Macro & Policy Backdrop

-

Markets are currently filtering out policy noise, focusing instead on:

-

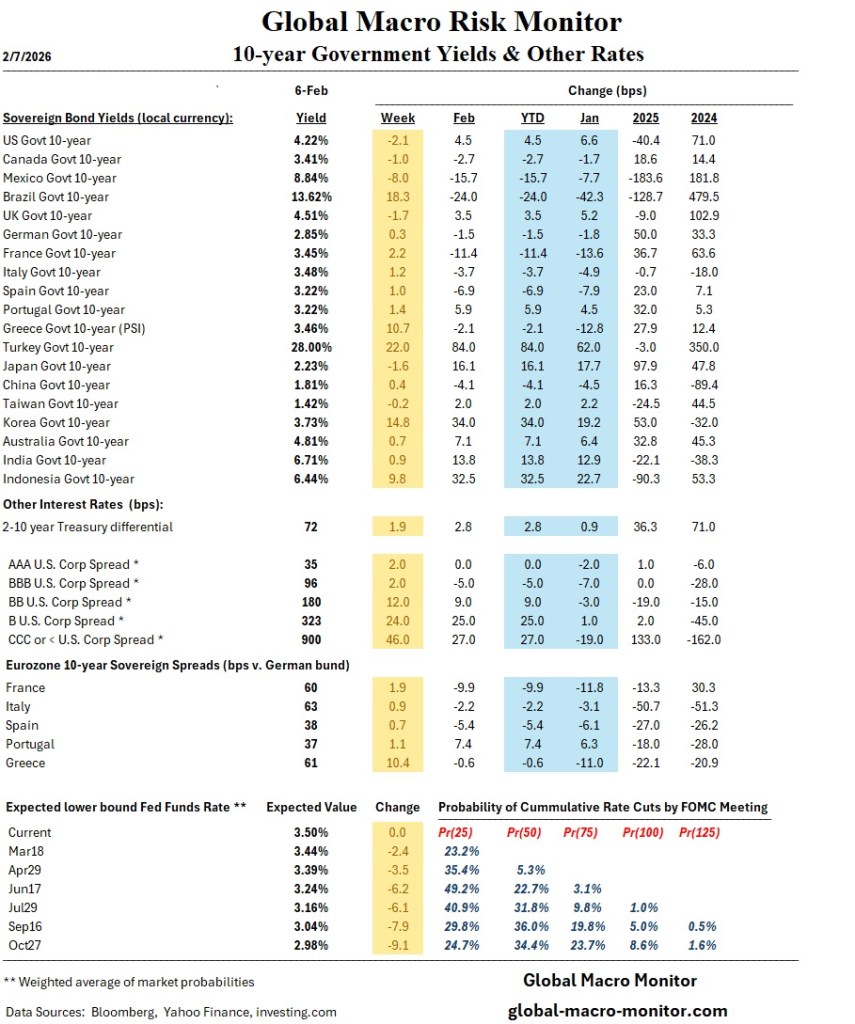

Cooling but resilient U.S. inflation

-

Stable labor market

-

Earnings durability

- Upcoming risks:

-

President Trump’s Davos speech

-

Fed leadership uncertainty

-

Shifts in rate-cut expectations could test market complacency

-

-

Strategic Takeaways

-

This is rotation, not risk-off

-

Broadening participation is constructive, but momentum is vulnerable to policy shocks

-

Commodities—especially silver—are quietly signaling macro regime hedging

-

Asia remains the cleanest relative growth and equity story in the near term

-

Maintain flexibility: early-year moves often exaggerate signals before fundamentals fully assert themselves