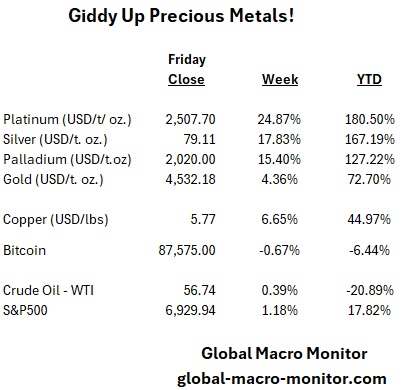

No commentary this week as the charts are doing all the shouting.

Heigh-Ho, Silver (and Platinum): The Great Fiat Exit of 2025

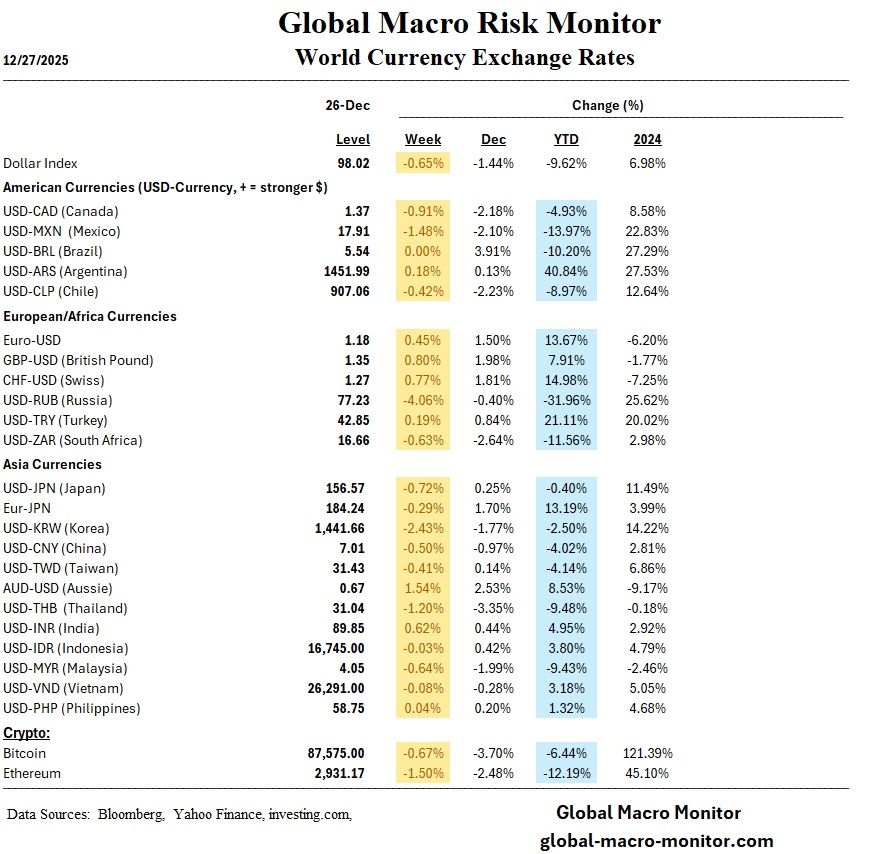

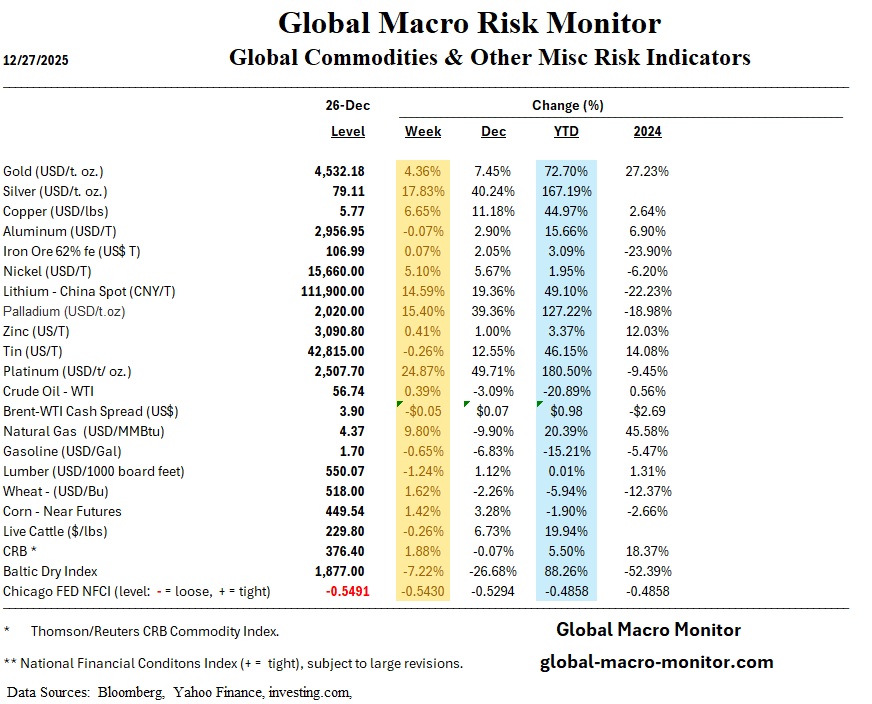

Are you actually watching this? Silver just capped an 18% weekly surge, only to be made look sluggish by Platinum’s violent 25% spike. As we head into the final days of 2025, the “Everything Rally” has officially narrowed into a “Physical Rally,” with silver closing in on $79/oz and platinum reclaiming its throne at $2,500/oz.

The Post-Mortem on the Melt-Up:

The “Fiat Exit”: This isn’t just a garden-variety inflation hedge. This is a full-scale exodus. Between aggressive Fed rate-cut fever and a geopolitical map that looks like a game of Risk gone wrong, investors are fleeing the paper theater for assets they can actually drop on their foot.

The Digital Gold Delusion: For years, we were told Bitcoin was the new gold. Yet, in the face of true global macro instability, the “crypt story” is looking a bit… skeletal. Precious metals have decisively lapped BTC this year, proving that when the world gets twitchy, capital prefers centuries-old certainty over digital allure.

Tangible Supremacy: In a world of naval blockades and supply-chain “oopsies,” physical scarcity and geopolitical neutrality aren’t just features—they’re the only insurance policies that matter.

The Bottom Line: While the crypto crowd waits for a software update, the boomer rocks (gold and silver) are riding away. When confidence wanes, the smart money trades pixels for physical.

Chinese officials have learned that the Trump administration, for all its bluster, will not follow through on its promises or its threats. – Foreign Affairs

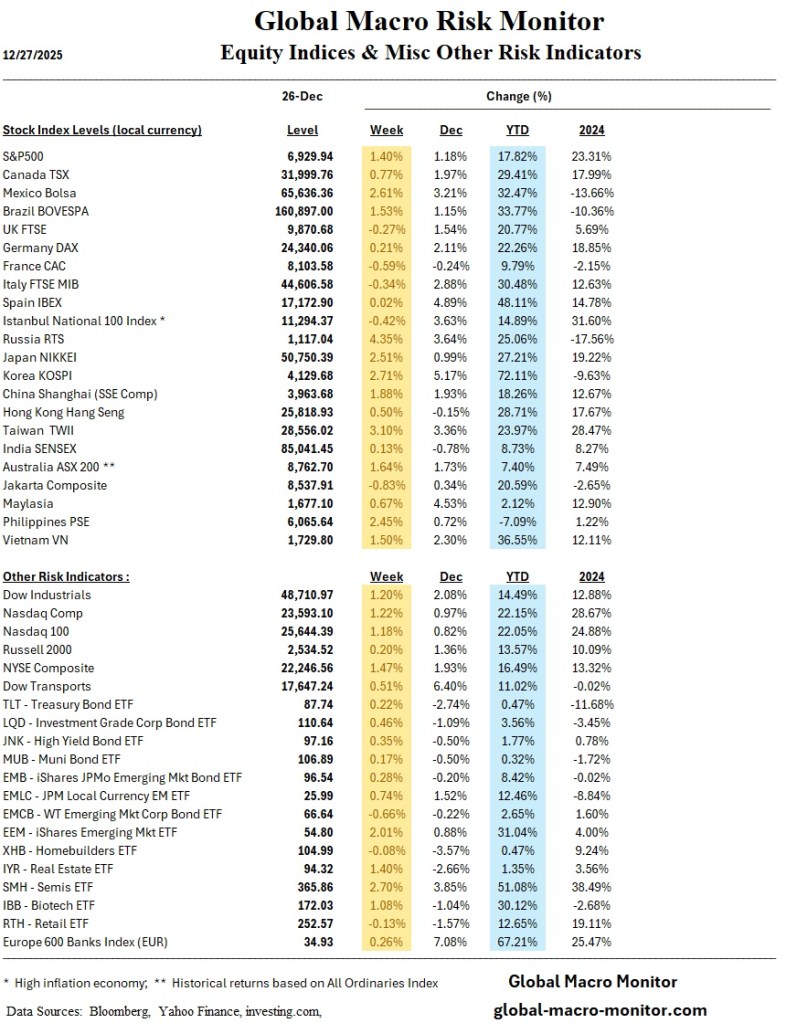

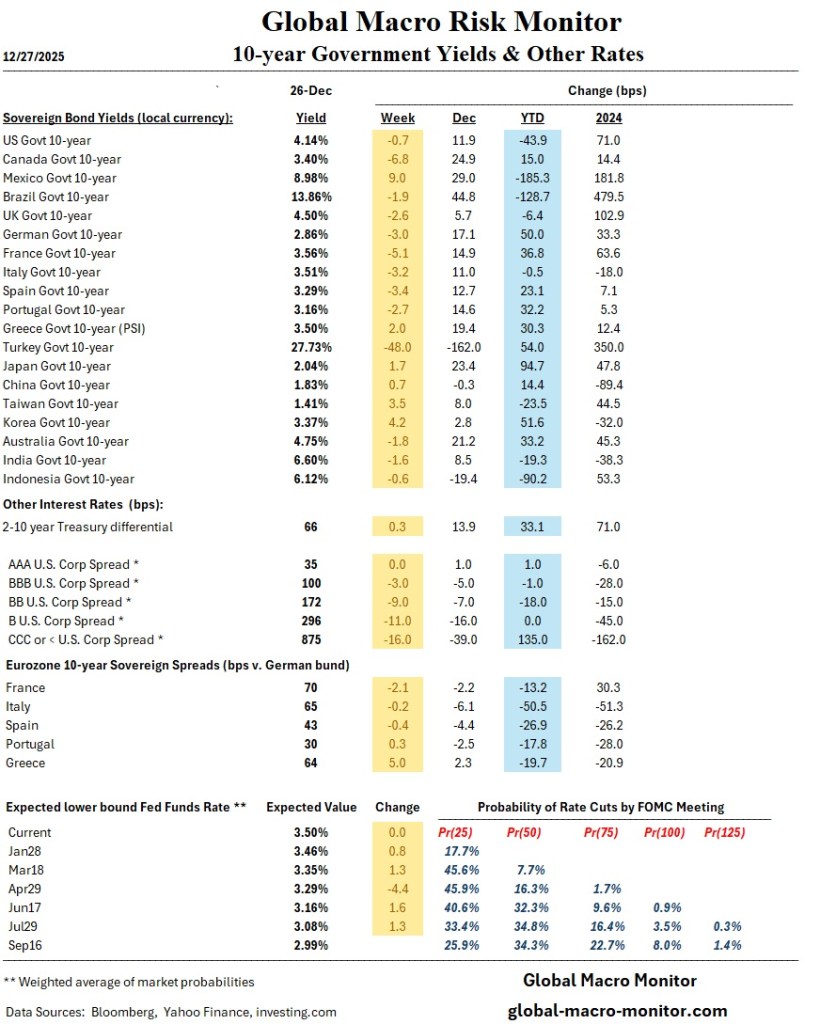

Global markets closed the week with a clear message: policy easing is supporting risk appetite, but leadership is rotating, and stresses are emerging beneath the surface. The Federal Reserve’s December rate cut reinforced expectations that the tightening cycle is firmly behind us, triggering a steepening of the U.S. yield curve, with the 2–10 spread widening by roughly 8.3 bps, a constructive signal for banks and cyclicals, but also a sign that growth and inflation uncertainty persist.

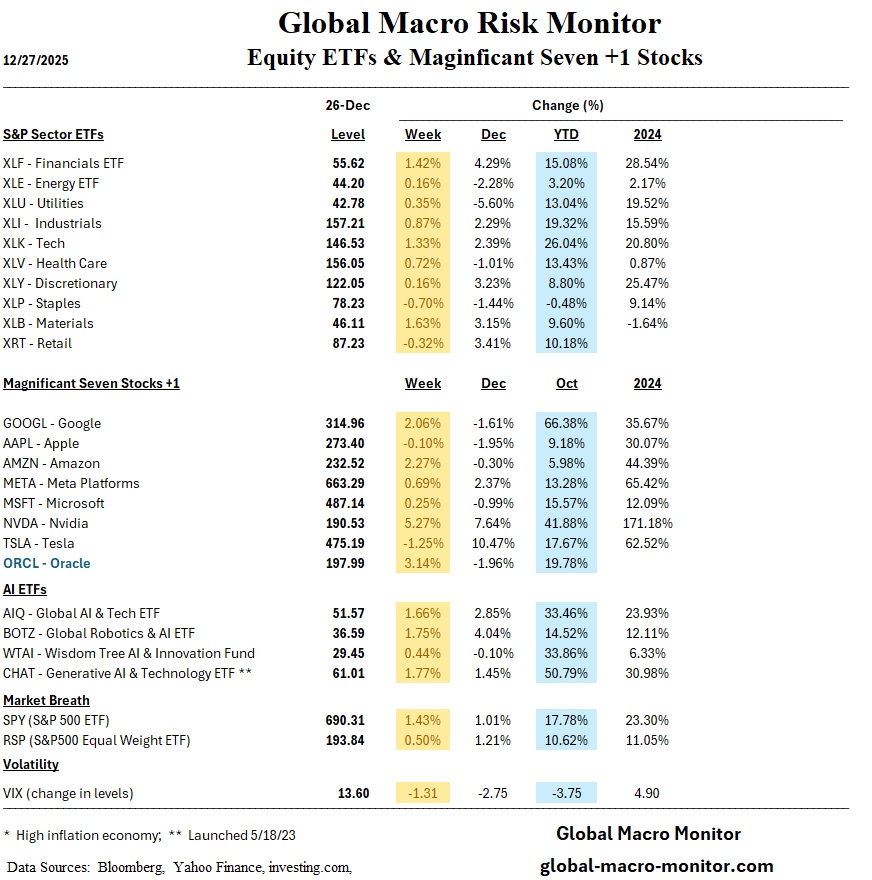

Equities continue to broaden, with small caps (Russell 2000) and the S&P 500 Equal Weight Index outperforming, underscoring investor rotation away from mega-cap tech. That rotation was accelerated by a sharp sell-off in Oracle, which reignited concerns around AI-related capital intensity and valuation discipline.

In commodities, precious metals decisively outperformed, with silver surging roughly 6% and gold adding about 2%, extending their dominance over cryptocurrencies, which lagged despite easier financial conditions. Conversely, energy markets weakened materially, led by a more than 20% collapse in U.S. natural gas prices and a notable pullback in oil.

Emerging markets delivered mixed signals: Mexico’s bond yields spiked, reflecting inflation surprises and repricing of Banxico’s terminal rate, while Vietnam’s equity market sold off sharply on liquidity concerns, highlighting uneven financial conditions across EM. Overall, the backdrop remains supportive, but increasingly fragile, as liquidity and policy optimism clash with valuation, earnings, and geopolitical risks.

Rates, Policy, and Fixed Income

Fed cut rates by 25 bps, reinforcing a late-cycle easing narrative while maintaining optionality.

Energy markets remain vulnerable, with natural gas oversupply and weak demand dynamics likely to persist unless weather or geopolitical factors intervene.

Risk Framing

Markets enter the week supported by liquidity and momentum, but with thin tolerance for negative surprises.

The dominant question remains whether policy easing can sustain growth without reigniting inflation—or whether volatility rises as that balance is tested.

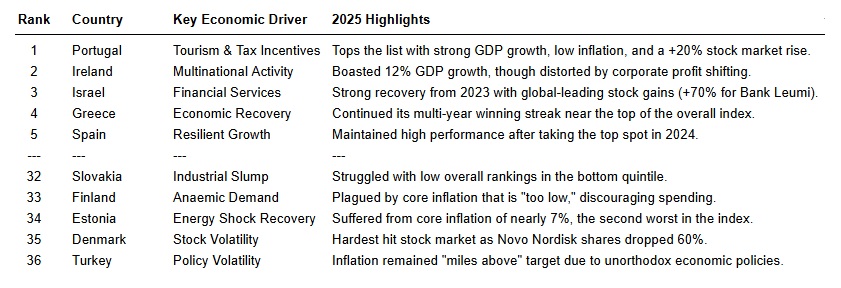

A great piece from TheEconomist ranking the performance of global economies. Here is a concise summary.

Despite fears of a trade-war-induced recession, the global economy proved resilient in 2025. With global GDP growth steady at 3% and unemployment remaining low, the primary concern shifted toward sticky inflation, which remains above the 2% target across the OECD.

Top Performers and Surprises

The star of the year is Portugal, which combined robust GDP growth with low inflation and a thriving stock market. Southern Europe’s streak continues, as Spain and Greece also ranked near the top. Israel saw the world’s best stock market returns, driven by its banking sector, while Ireland’s growth remained spectacular, though distorted by multinational accounting.

Regional Divergence

The Laggards: Northern European nations like Estonia, Finland, and Slovakia struggled.

The Giants: The United States landed in the middle, hindered by higher inflation despite a respectable job market.

Deflation Risks: Countries like Sweden faced the opposite problem—anaemic inflation, which raises concerns about long-term spending and debt burdens.

Ultimately, 2025 favored economies that managed to balance tourism and tax incentives against the pressures of high interest rates and global trade friction.

Global risk sentiment stayed constructive this week despite a sharp back-up in global bond yields and lingering growth concerns. Higher long-end yields across 19 bond markets—led by a 27 bp rise in Canada—coincide with markets pricing an 80–90% chance of a 25 bp Fed cut, but limited conviction on further easing into March. Equities ground higher in the U.S. and Europe, with transports, cyclicals, and small caps outperforming as investors rotate toward rate-sensitive and economically geared sectors.

Data continue to paint a mixed global picture: U.S. manufacturing remains in contraction while services expand at the fastest pace in nine months; labor indicators are softening at the margin, but initial jobless claims sit at a three-year low. Eurozone inflation has ticked up slightly above 2%, reinforcing an ECB-on-hold stance, while Japan edges closer to BoJ rate normalization as JGB yields hit multi-year highs. China’s PMIs underline weak domestic demand, even as exports and tech/AI themes support local equities. Across EM, policy is drifting more dovish, with India and several Asian and EEMEA central banks cutting rates. Overall, valuations look increasingly stretched, leaving the rally vulnerable to rates, earnings, or policy surprises.

Regional Economic Insights

United States

Mixed labor data: ADP showed the largest job loss in two years while jobless claims hit multi-year lows.

Stock performance supported by weaker inflation (core PCE below expectations) and Fed-cut optimism.

Oil, yields, and gold moved in response to shifting expectations for next week’s FOMC call.

Eurozone

Market sentiment influenced by inflation divergence—CPI roughly aligned with expectations while PPI remains firm (from broader template structure).

Japan

JGB yields rising, interacting with U.S. yields and potentially altering risk sentiment next week.

China

No new macro updates in Week_Dec5; monitoring holiday-related demand trends (per document structure).

Inflation: CPI–PPI Dynamics

U.S. core PCE inflation cooled slightly in the latest release (0.1% below expectations), helping maintain the disinflation narrative.

Producer prices (PPI) due next Thursday are a potential catalyst for volatility.

Markets

Equities

Strongest sectors: consumer durables, transportation, and manufacturing.

Dow Transports had an outsized weekly gain, breaking into leadership territory and signaling cyclical momentum.

Bonds

Yields fell on weak ADP data but reversed higher on cooling inflation expectations and anticipation of the FOMC meeting.

Energy, Metals & Crypto

Oil: Rose mid-week on geopolitical tensions, then moderated on inventory builds.

Gold: Softened after the prior week’s 3.8% rally.

Crypto: Bitcoin and Ethereum whipsawed; ETH boosted temporarily by its Fusaka upgrade.

United States Outlook (Week Ahead)

Key releases include JOLTS, ECI, PPI, crude oil inventories, and the FOMC decision on Dec. 10.

Central Bank Actions

The FOMC is expected to cut rates by 25 bps, though committee dissents are likely; guidance suggests fewer cuts ahead.

Risks & Outlook

Volatility expected in the latter half of next week due to Fed messaging and Oracle earnings—a binary catalyst for AI-linked sentiment.

Rising JGB yields may pressure U.S. long rates and shift the market tone.

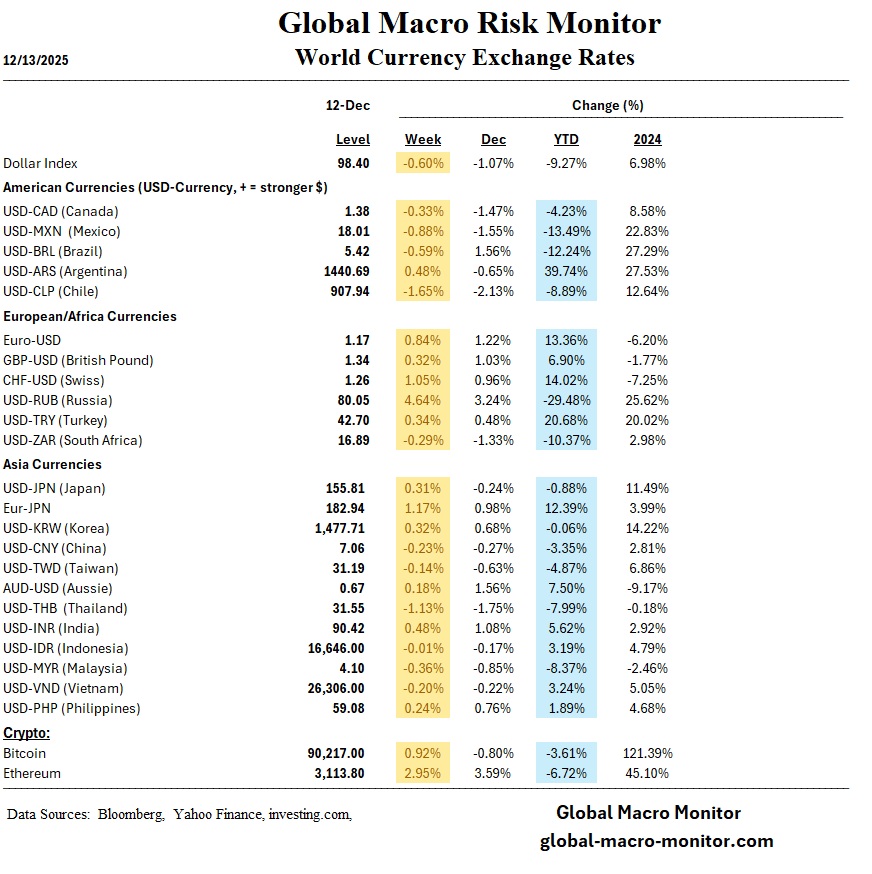

Silver surged 13% for the week and is now up over 90% year-to-date—vastly outperforming Bitcoin, which is down 3% on the year.

Eurozone banks climbed 5% during the week and are now nearly 70% higher year-to-date when accounting for the currency boost.

Market volatility fell sharply, with the VIX dropping 7 points to 16, signaling stronger investor risk appetite.

These developments: precious metals momentum, European banking sector strength, and a major decline in volatility were central to global market behavior this week.

GLOBAL MARKETS SUMMARY

Risk assets rallied across global markets. U.S. equities posted broad gains in a holiday-shortened week, supported by softer economic data and dovish messaging from Federal Reserve officials. The markets have priced an 86% probability of a 25 bps rate cut by the Fed at its December 10th meeting. Small caps outpaced large caps, and technology shares rebounded strongly.

The standout move came from silver, which surged 13%, a move reflecting both inflation concerns and increased demand for safe-haven or alternative assets.

European markets also strengthened, with a notable rally in bank stocks. Meanwhile, volatility dropped substantially, creating a supportive backdrop for equities and credit.

UNITED STATES

Equities & Markets

Major indices posted weekly gains:

Dow: +3.18%

S&P 500: +3.73%

Nasdaq: +4.91%

The Russell 2000, a gauge of smaller companies, rose 5.52%, reflecting a shift toward risk-on sentiment.

Economic Data

Retail sales: +0.2% for September, below expectations.

PPI: +0.3% headline; +0.1% core.

Jobless claims: Declined to 216,000, the lowest since April.

Consumer confidence: Fell to 88.7, signaling growing economic caution.

Policy & Rates

Fed Beige Book:

Employment edged lower.

Prices continued moderate increases.

Consumer spending weakened further.

Treasury market: Yields fell as investors priced in a likely December rate cut. The yield on the 10-year Treasury note fell 5 bps to 4.02%

EUROPE

Equities

STOXX Europe 600: +2.35%

DAX: +3.23%

CAC 40: +1.75%

FTSE 100: +1.90%

Eurozone Banks: Weekly and Year-to-Date Standouts

Banks in Europe rallied roughly 5% for the week and are now nearly 70% higher year-to-date when currency gains are factored in. We doubt anyone believed at the beginning Euro banks would outperform Nvidia by a factor of 2x by December 1st.

Key drivers included:

Higher net interest margins

Strong capital positions

Stable inflation near ECB target

Improved sentiment toward European financials

Macro Developments

Inflation across major eurozone countries remained subdued.

UK’s new budget introduced £26 bn in tax increases.

Germany’s business sentiment weakened, while consumer willingness to buy improved.

JAPAN

Japanese markets rallied strongly:

Nikkei: +3.35%

TOPIX: +2.45%

Momentum was fueled by dovish signals about global monetary policy, a rebound in tech/AI shares, and steady Tokyo inflation at 2.8%, reinforcing speculation that the Bank of Japan may contemplate a future rate hike.

The 10-year JGB yield rose to 1.82%, approaching levels last seen 17 years ago.

CHINA

Chinese equity benchmarks advanced:

CSI 300: +1.64%

Shanghai Composite: +1.40%

Hang Seng: +2.53%

Despite these gains, industrial profits fell 5.5% year over year, indicating slowing momentum and highlighting persistent structural challenges—particularly within manufacturing and real estate.

OTHER KEY MARKETS/GEOPOLITICAL DEVELOPMENTS

Russia–Ukraine Peace Framework Discussions

A 28-point U.S. proposal has gained traction among NATO and EU members, offering a potential basis for negotiations but still requiring major concessions from both sides.

South Korea Monetary Policy

The Bank of Korea kept the Base Rate at 2.50%, noting rising inflation but maintaining flexibility for future cuts amid global uncertainty.

MARKET VOLATILITY TRENDS

The VIX dropped sharply to 16, falling 7 points in one week.

This move signals:

Declining hedging costs

Renewed appetite for equities and credit

Possible overconfidence if economic data fails to stabilize

The drop in volatility was one of the most influential forces shaping global risk sentiment the past and upcoming week.

PRECIOUS METALS: SILVER’S POWERFUL SURGE

Silver’s 13% weekly rally has pushed its year-to-date gain beyond 90%, dramatically surpassing Bitcoin’s –3% performance.

Key catalysts include:

Strong industrial demand

Elevated geopolitical tensions

A softer U.S. dollar

Growing investor preference for tangible, inflation-resistant assets

EUROPEAN FINANCIAL SECTOR: BANKS BREAK OUT

Eurozone banks delivered another standout performance this week. Their strong gains reflect:

Stabilizing macroeconomic conditions

Attractive valuations

Positive earnings momentum

Enhanced foreign interest due to currency strength

This sector remains a cornerstone of the European equity story in 2024.

OUTLOOK: WHAT TO WATCH NEXT

Federal Reserve: Market expectations remain aligned with a possible December rate cut.

Eurozone Inflation (Dec 2): A reading near target could support earlier ECB easing.

Bank of Japan: Investors await guidance on potential tightening.

China: Markets look for signs of additional stimulus as growth softens.

Volatility: With the VIX at 16, markets could be vulnerable if data surprises to the downside.