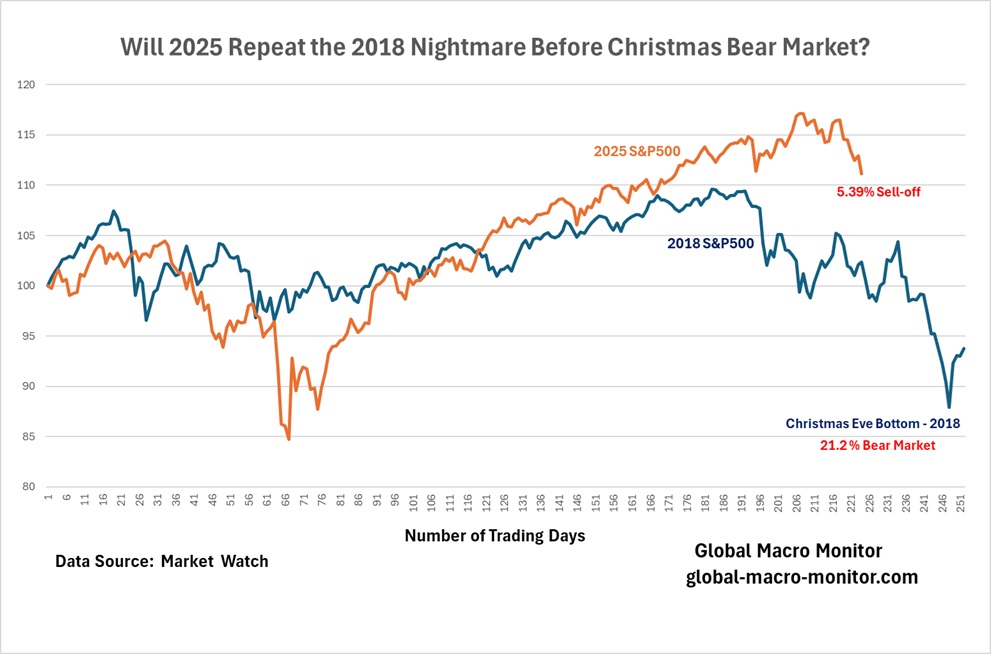

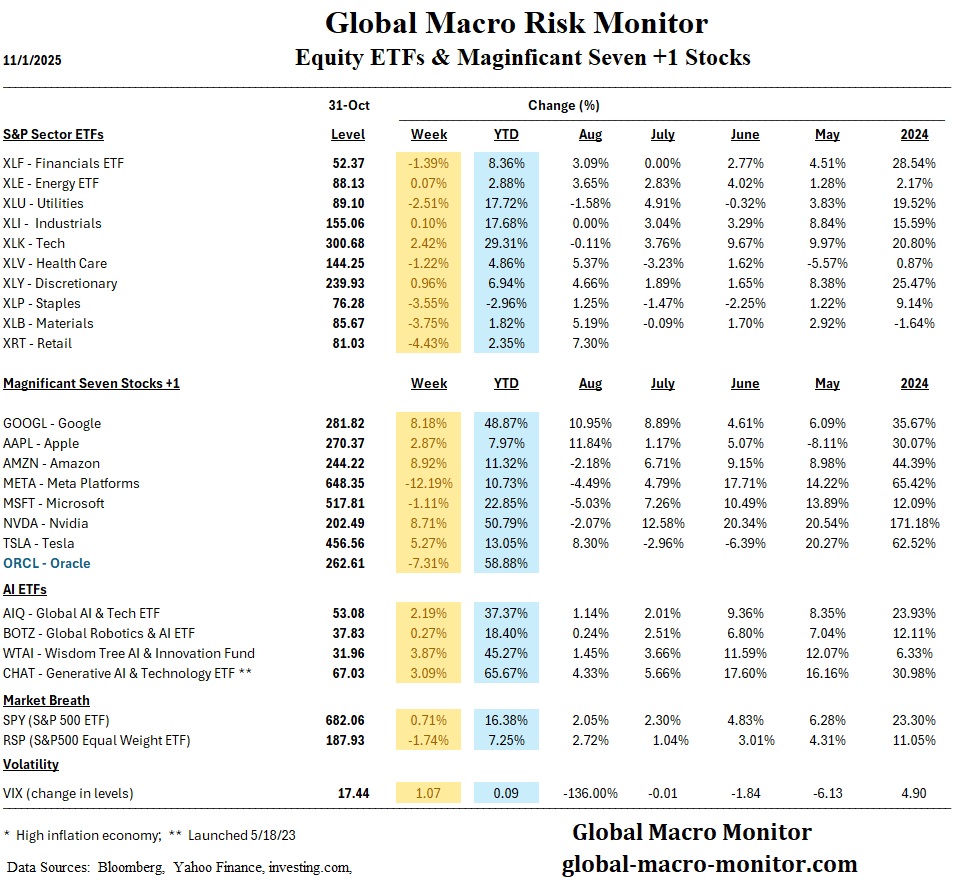

Nvidia endured a sharp and unsettling 8% reversal today, and when combined with Bitcoin’s continued slide, the pressure spread quickly across the broader market. By the close, the S&P 500 had fallen 3.5% from its intraday high, marking a swift and sizable retreat.

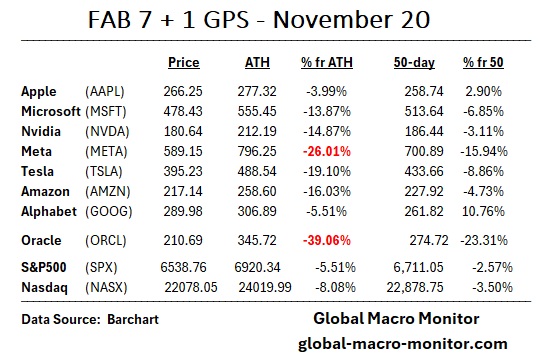

Within the Fab 7, only Apple and Alphabet have avoided double-digit declines from their recent highs. The rest have already fallen double-digits, with several either in or nearing bear-market territory—a drop of 20 percent or more.

No one can foresee what comes next, but the speed and severity of today’s reversal invite a moment of reflection. For some investors, the abrupt shift echoes the unsettling tone of the 2018 “Nightmare Before Christmas” bear market. That episode only finally came to an end on Christmas Eve, when Fed Chairman Jay Powell—after months of relentless pressure from President Trump—stepped back and began to ease up on monetary policy, effectively marking the capitulation that turned the tide.

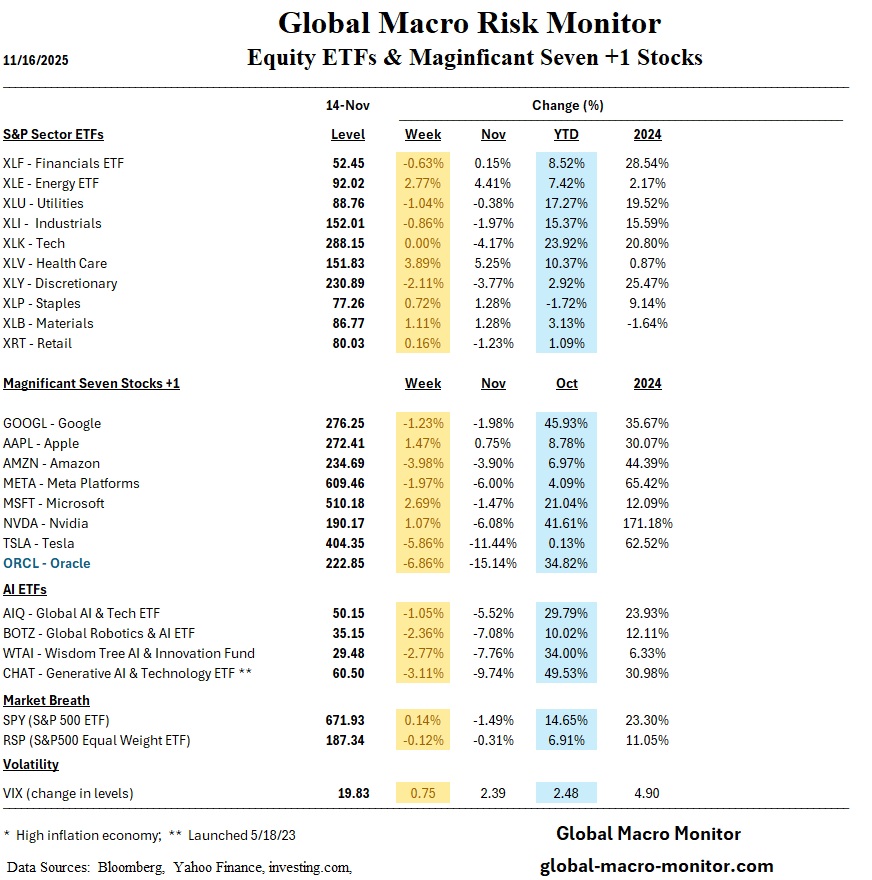

The following table shows notable divergence among the major tech names.

Apple is sitting just 1.8% below its peak, placing it within striking distance of a new record. In contrast, both Meta and Oracle are firmly in bear-market territory, each trading at more than 20 percent below their all-time highs (ATH) and double-digit discounts to their 50-day moving averages.

Meta is down more than 14% from its 50-day, reflecting ongoing volatility tied to concerns about rising AI-related expenses. Oracle sits nearly 20% below its 50-day after a sharp month-long slide driven by cloud-margin worries.

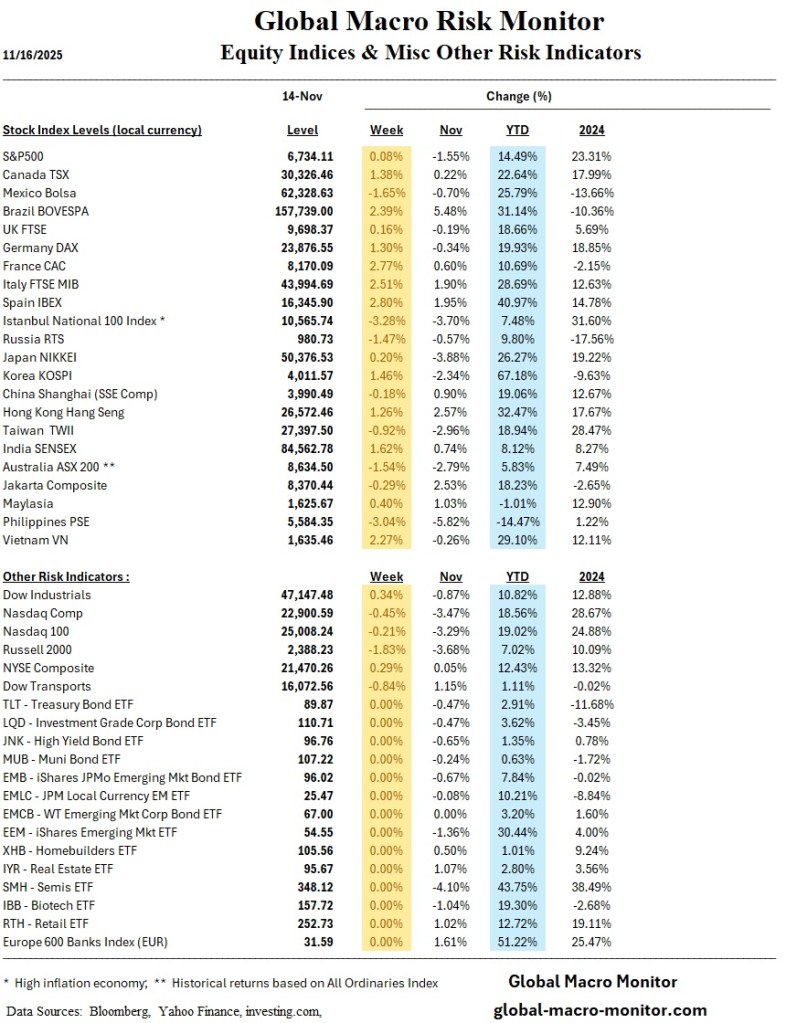

Global economic activity showed mixed momentum, with markets navigating a choppy week shaped by the end of a prolonged 43-day U.S. government shutdown and increasingly hawkish Federal Reserve communications. U.S. equities initially rallied on optimism but ultimately ended broadly flat to slightly lower, while bond markets adjusted to fading expectations of a December rate cut. International data presented uneven growth signals, and several regions continued to struggle with inflation pressures and policy uncertainty.

Global Markets

Markets experienced volatility: early-week rallies faded by Thursday’s sell-the-news reaction after the U.S. government reopened, leaving the S&P 500 and Dow marginally higher for the week and the NASDAQ slightly lower.

Market breadth improved modestly, with more stocks trading above 200-day moving averages across the S&P 500, Nasdaq, and Russell 2000 indices

Global activity indicators were mixed: UK growth held modestly, Australia’s labor market strengthened, while China’s activity continued to soften

Regional Highlights

United States

Federal Reserve:

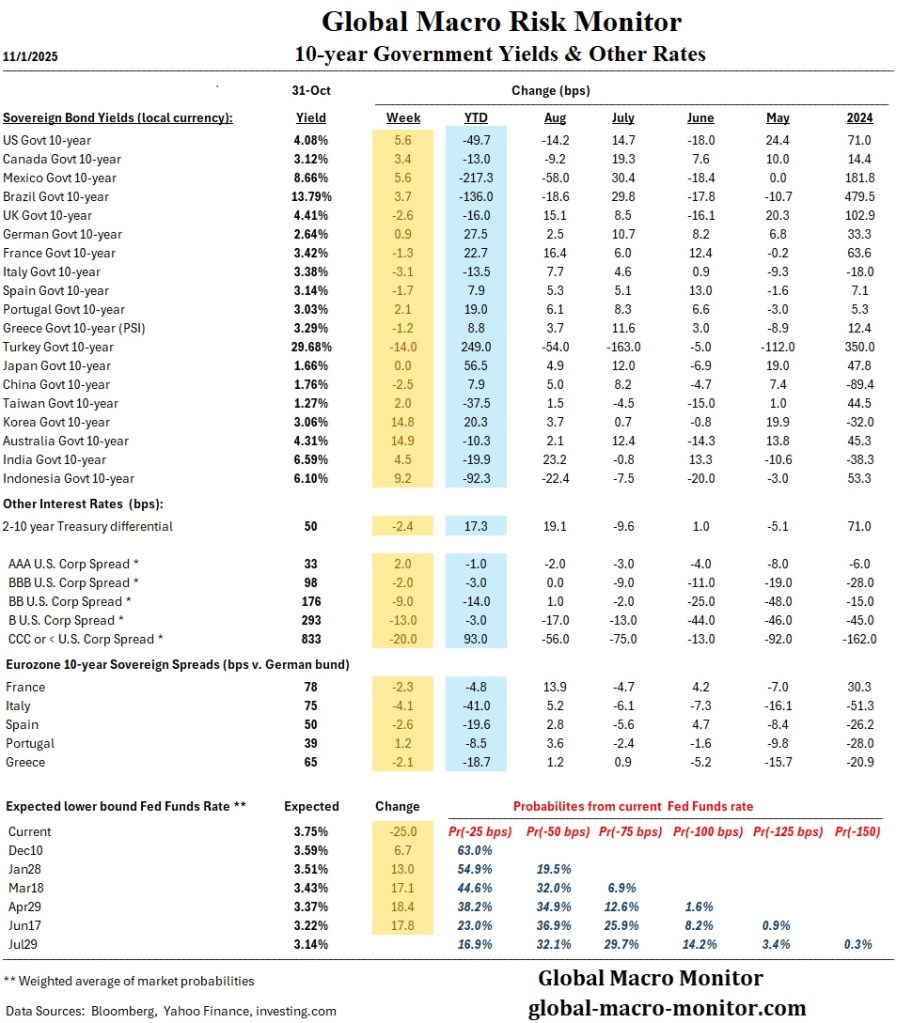

Multiple Fed officials sent hawkish signals, sharply reducing expectations of a December rate cut. Probabilities fell from ~63–70% to roughly 41–46% during the week.

Officials emphasized lingering inflation risks and uncertainty due to data gaps caused by the shutdown

Economic Indicators

CPI data release delayed; estimates point to +0.2% MoM and 3.0% YoY inflation; core CPI nowcast at +0.3%.

PPI expected +0.2% MoM, reversing -0.1% prior month

Government shutdown resolution will slowly clear data backlogs, with the September jobs report scheduled for release November 2.

Market Performance:

Early-week equity rally driven by shutdown-ending progress; tech led initial gains before rotating out later in the week.

Treasury yields rose slightly after hawkish Fed commentary

Europe

UK reported modest Q3 growth with slowing wage gains—part of broader mixed global activity data.

Romania kept its policy rate at 6.50%, facing elevated inflation (9.76% in October) driven by VAT hikes and removal of electricity price caps. Policymakers foresee modest declines in inflation over coming quarters

Japan

Japan GDP release scheduled for the following Monday, noted as a key upcoming data point in the global calendar

No additional Japan-specific data was included in the visible excerpts.

China

China’s activity data “continued to soften,” signaling ongoing demand challenge.

Trade- or manufacturing-specific details were not included in the retrieved excerpts.

Emerging Markets

Romania highlighted as maintaining steady rates amid “high uncertainties and risks,” with inflation well above desired levels due to energy policy shifts and tax increases.

No additional emerging-market political or macro developments were present in the visible material.

Commodities & FX

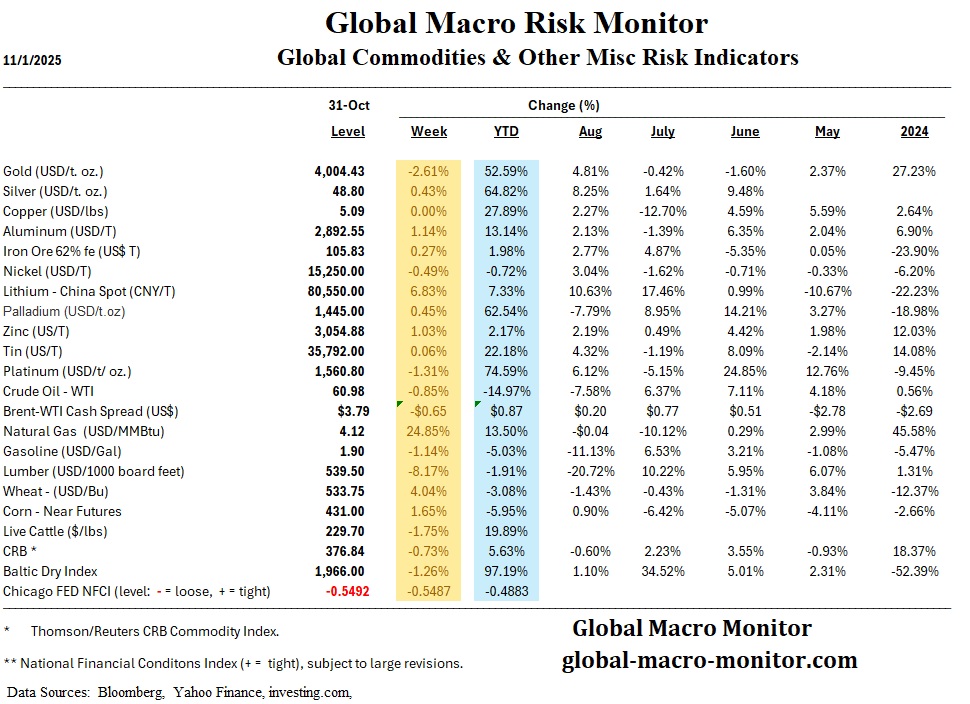

Oil: EIA crude oil inventories rose by +6.41 million barrels.

Natural Gas: EIA natural gas inventories increased by +45 bcf

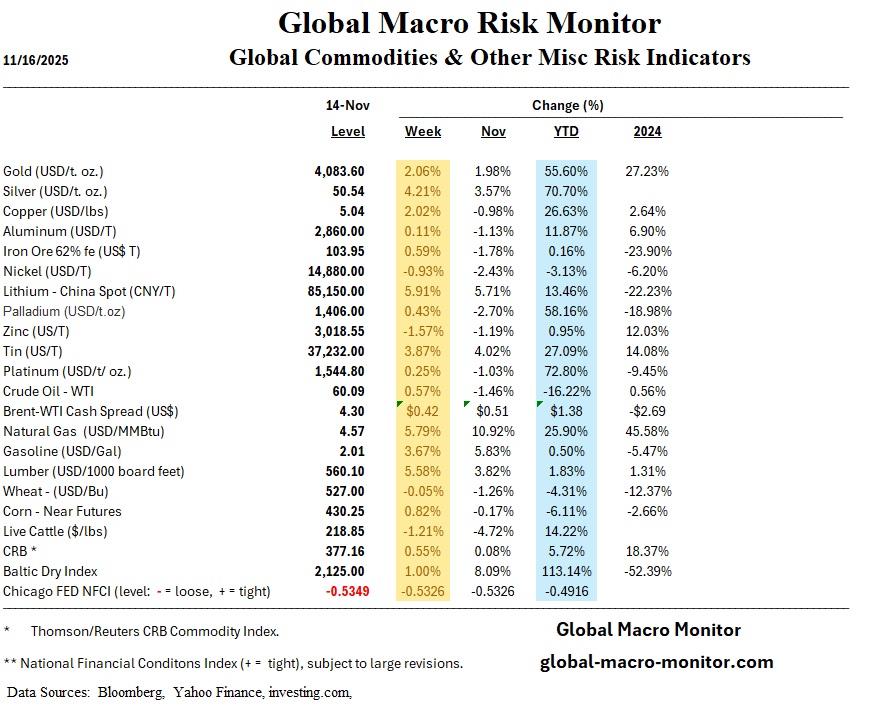

Gold/BTC: Gold rose 2 percent and is now up over 50 percent on the year, a major outperformance relative to Bitcoin, which is up only 2 percent in 2025.

Week Ahead

United States:

Nonfarm Payrolls expected Tuesday or Wednesday; Existing Home Sales on Thursday.

Global:

Japan GDP (Mon.)

Canada CPI (Mon.)

Eurozone PMIs (Fri.)

U.S. Data Backlog:

September jobs report scheduled for November 20; additional delayed releases remain unscheduled due to shutdown disruptions

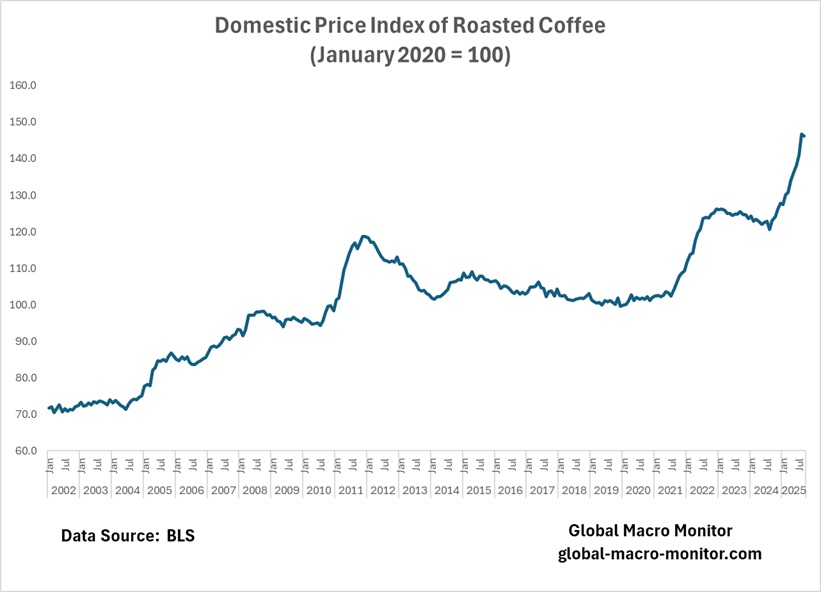

The strategy’s incoherence is evident in absurd measures such as, for example, a tariff on coffee, an import for which the U.S. lacks viable domestic production except de minimis production in Hawaii and Puerto Rico. These policies reflect a reactive, politically charged agenda rather than a cohesive economic strategy. Ultimately, market forces are likely to compel a reversal…

Doesn’t the Administration understand the most basic concept of international trade and economics – Comparative Advantage? – GMM

We grabbed a 2½-pound bag of coffee at Costco this week and nearly fell over—prices are up more than 20% from a year ago. With that kind of sticker shock hitting everyday items, Trump’s latest tariff reversal doesn’t come as a surprise at all. It fits the broader pattern we’ve been tracking: policy swings that feed directly into higher consumer costs.

Many of the commodities that will no longer face “reciprocal” tariffs have seen some of the biggest price increases since Trump took office, in part because of tariffs he imposed and a lack of sufficient domestic supply.

For instance, Brazil, the top supplier of coffee to the US, has faced tariffs of 50% since August. Consumers paid nearly 20% more for coffee in September compared to the prior year, according to Consumer Price Index data. – CNN, November 14

Impact on Bond Markets

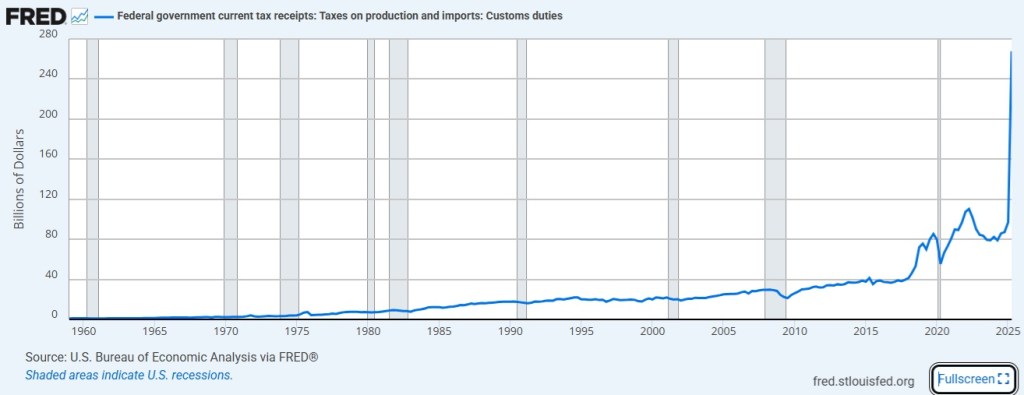

The real issue is whether global bond markets will start to price in the broader implications of a Trump tariff rollback—one that extends well beyond food imports. Customs duties have quietly become one of the fastest-growing revenue streams for the federal government, a rare source of fiscal buoyancy in an otherwise deficit-heavy landscape. If those tariffs come down, then—ceteris paribus—the Treasury loses a meaningful chunk of income, mechanically widening the budget deficit unless offset elsewhere. Emphasis on “extends well beyond food imports” for meaningful impact on federal tax receipts.

In that sense, tariff policy isn’t just a trade variable anymore; it’s a fiscal lever with direct consequences for supply dynamics in the Treasury market. Investors already nervous about persistent deficits and elevated issuance may view a tariff unwind as one more pressure point on the government’s financing needs. And in today’s environment—where duration supply, term premia, and fiscal credibility are back at the center of global macro—the bond market’s reaction function could turn decidedly less forgiving.

Tariff Revenues to the U.S. Government ($ billions)

Coffee Tariffs

Shortly after tariffs first landed in early April 2025 with “Liberation Day,” most imports were given a 10% rate. That alone was disruptive—this was the first time in recent memory that U.S. coffee imports were hit with tariffs. The shock was immediate, the questions were many, and the impact was felt across the specialty coffee supply chain. Four months later, tariffs on coffee are higher than ever. The landscape is shifting, and the situation is escalating. Here’s where things stand now, and what it means for you as a roaster.

While tariffs on coffee imports from many countries still face a 10% duty, geopolitical tensions have driven some rates much higher. Goods from Brazil, the world’s largest coffee producer, are now subject to a staggering 50% tariff. Other large coffee producers, like India (25%), Vietnam (20%), and Indonesia (19%), have also been hit with steep increases. These changes are reshaping the coffee trade in real time. — Genuine Origin

Juan Perón Resurrected

At Global Macro Monitor, we’ve been direct about this: Trump’s erratic, favor-driven policy style is steadily grinding the economy into a less efficient machine. Government by whim—and too often by favor or implied corruption—forces businesses to spend more time deciphering political signals than deploying capital. The economic gears are gumming up: investment gets delayed, supply chains get hedged into absurdity, and firms operate under the constant threat that today’s rule could be tomorrow’s tweet

The only thing masking the damage is a stock market still levitating on momentum, and even that looks like it’s on its final, exhausted leg. The parallel is obvious to us—this is the modern Juan Perón dynamic, where political volatility and personalist rule corrode economic performance long before financial markets finally reprice the risk.

Global markets ended the week mixed as a U.S.–China trade truce and a widely anticipated Federal Reserve rate cut drove both relief and uncertainty. While U.S. equities held near record highs, global sentiment was tempered by uneven central bank actions and signs of slowing global trade momentum. Investors are navigating a “fog of policy”—one where monetary and trade decisions, rather than economic fundamentals, continue to dominate asset prices.

The disinflation trend remains intact across advanced economies, but diverging growth patterns suggest that synchronized easing may be harder to sustain. The United States remains resilient, Europe stabilizes modestly, Japan shows strength under policy continuity, and China grapples with soft demand and fading stimulus traction.

Regional Highlights

United States

The Federal Reserve cut the target range for the federal funds rate by 25 bps to 3.75%–4.00%, marking a second consecutive easing.

Chair Jerome Powell emphasized that a December cut “is not a foregone conclusion,” reflecting a widening split within the FOMC.

The government shutdown, now exceeding 30 days, has delayed major economic data releases including GDP, PCE, and employment figures.

Consumer confidence fell for a third month to 94.6, a six-month low, with pessimism over job prospects rising.

Pending home sales were flat in October, and mortgage rates edged back above 6% following the Fed’s hawkish tone.

Earnings season remains strong: roughly 82% of S&P 500 firms beat EPS expectations, with average EPS growth of 10.7%.

Amazon and Google fared well after their earnings release, while Mr. Softee and Meta got hammered.

Market breadth narrowed sharply as the S&P 500 hit new highs, yet only 56% of its components trade above their 200-day average.

Europe

The ECB held rates steady at 2.00%, reiterating a data-dependent stance.

Eurozone GDP grew 0.2% QoQ and 1.3% YoY, slightly above consensus, supported by France and Spain.

Headline inflation slowed to 2.1%, with core CPI at 2.4%; services inflation remains sticky at 3.4%.

The UK housing market showed resilience, with Nationwide HPI up 0.3% MoM, while mortgage approvals reached a nine-month high.

Japan

Nikkei 225 rose 6.3% for the week and 16.6% for October, its best month since 1994.

The BoJ held its policy rate at 0.50%, maintaining a cautious stance amid stronger Tokyo inflation (2.8% YoY).

Governor Ueda noted upside risks tied to wage talks and tariffs, while Finance Minister Katayama issued warnings over yen volatility.

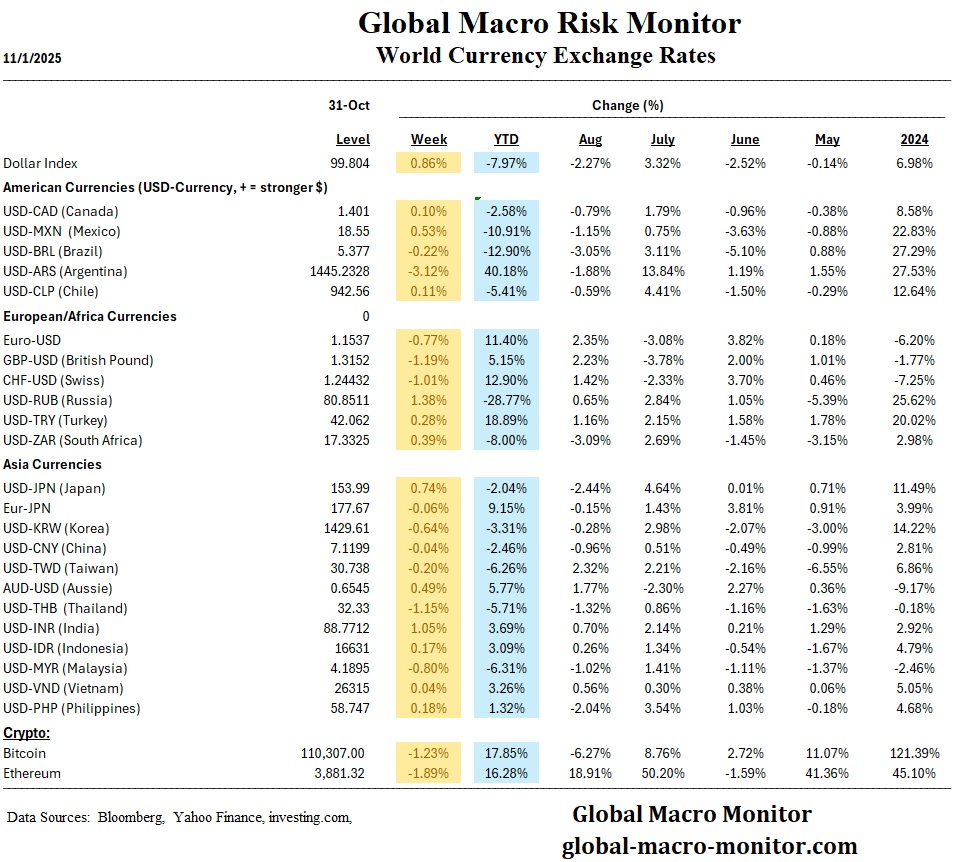

The yen weakened to ¥154 per USD, and retail sales rebounded 0.5% YoY.

China

Mainland markets were mixed; the CSI 300 fell 0.4%, while the Shanghai Composite gained 0.1%.

October manufacturing PMI slipped to 49.0, signaling continued contraction, while the non-manufacturing PMI inched up to 50.1.

Following the Xi–Trump meeting, limited progress was made—tariff relief was modest, and export controls on chips remain intact.

Policymakers pledged to re-orient growth toward domestic demand and consumption, though concrete measures were lacking.

Emerging Markets

Argentina’s midterms strengthened President Milei’s reform mandate, with his coalition securing 41% of congressional seats.

Chile’s central bank held rates at 4.75%, citing mixed domestic data but improved external conditions and rising copper prices.

South Africa’s external trade position improved amid higher commodity revenues.

Banxico is expected to cut rates by 25 bps to 7.25% this week, following weak Q3 GDP and subdued inflation.

Commodities & FX

Oil fell early on OPEC+ output concerns but rebounded on lower U.S. inventories and trade optimism.

Natural Gas rose 25 percent on the week on expectations of a frigid U.S. winter

Gold declined for a second straight week but remains +3% for October.

Bitcoin retreated 6% after recent gains, while Visa announced expanded stablecoin integration across 40+ countries.

The dollar strengthened modestly on Powell’s hawkish comments, while the yen and euro softened.

Week Ahead (November 3–7, 2025)

U.S. Events

ISM Manufacturing (Mon) – Expected to remain in contraction near 49.0, reflecting tariff pressures and slowing new orders.

ISM Services (Wed) – Forecast flat at 50.0, with AI-related demand offsetting tariff drag.

Treasury Refunding Announcement (Wed) – Focus on issuance mix and implications for yield curve steepening.

Jobless Claims (Thu) and Employment Report (Fri) – Data scarcity from the shutdown limits reliability; private estimates suggest modest hiring softness.

Earnings Highlights – Reports from Palantir (Mon), AMD (Tue), Toyota (Wed), AstraZeneca (Fri).

Global Events

RBA Meeting (Tue) – Expected hold at 3.60%, following hotter-than-expected Q3 inflation.

BoE Meeting (Thu) – Likely to stay at 4.00%, but markets eye a possible December cut.

China Trade & PMI Data (Thu–Fri) – Key test for domestic demand momentum and post-summit sentiment.

Eurozone Retail Sales (Fri) – Could validate modest recovery trends seen in Q3 GDP.

Key Takeaway

Markets are recalibrating expectations: central banks are still easing, but hesitantly; fiscal drag, trade frictions, and data gaps complicate visibility. Investors should expect volatility as the U.S. navigates the fallout from the shutdown, earnings season matures, and policy “fog” lingers into year-end.