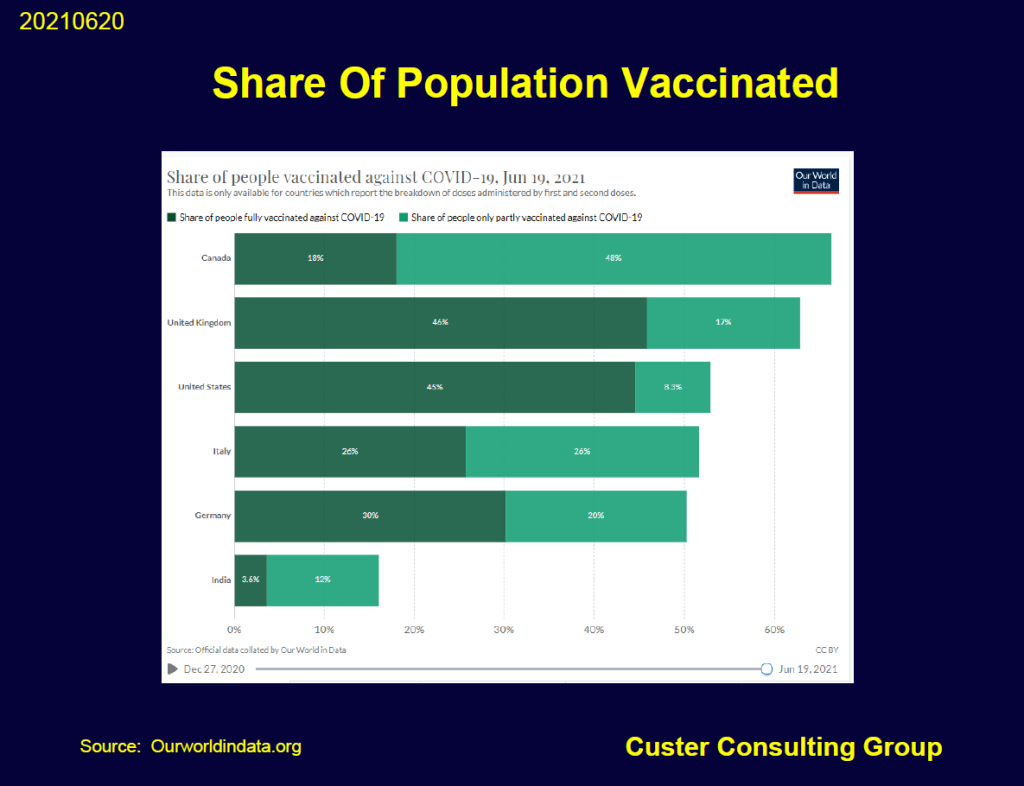

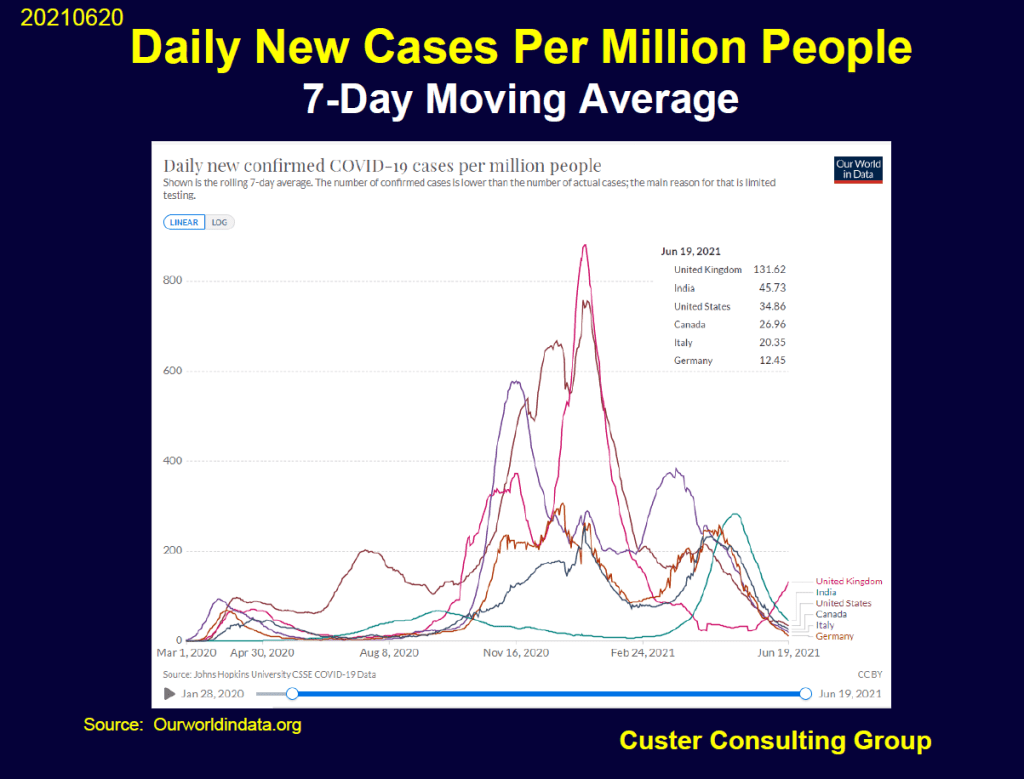

Wow, Justin is acting pretty conservative for a liberal. Canada already has some of the best COVID numbers in the world. High VAX, low new daily cases.

Assuming 4 percent of Canada has had (1.41 million reported cases) or has the COVID antibodies, that puts the country’s at a de facto 70 percent herd immunity rate. Enough to sleep easy, in our book. bed.

OTTAWA — Prime Minister Justin Trudeau maintains that Canada will need to meet the COVID-19 vaccines target of 75 per cent of the total population with a first dose and 20 per cent with two doses before his government lifts border restrictions.

Speaking to news that the U.S, Canada border will remain closed to non-essential travel for another month, Trudeau said Friday that, while he understands the urgency to return to some semblance of normality, permitting discretionary travel now would risk another wave of cases in this country.

“We’re not out of this pandemic yet, we’re still seeing cases across the country and we want to get them down. At the same time, we also know we have to hit our targets of 75 per cent vaccinated with the first dose, at least 20 per cent vaccinated with the second dose before we can start loosening things up because even a fully vaccinated individual can pass on COVID-19 to someone who is not vaccinated,” he said. – CTV News

He’s the PM and has to answer to the Canadian people. I am not and do not. That pretty much settles it.

PTJ, the Greatest Of All-Time (GOAT) in my book. I have few regrets in life but one is not hitting his bid when I was being pursued by his hedge fund years ago. The California beach was just too comfy back then.

His views should sound very familiar if you have been reading GMM over the past several months.

Listen up to the interview with Andrew Ross Sorkin from this morning. The 6 minutes is well worth your time. The opportunity cost of not doing so could be enormous.

Again, we are sending all the prayers, positive thoughts, energy, miracles, crystals, and manifestations in the entire cosmos to GMM’s deeply loved Carol K., who continues to fight her multiple-front illness in Boston. She contributed to this post and may or may not disagree with all the content.

Inflation And Loose Financial Conditions

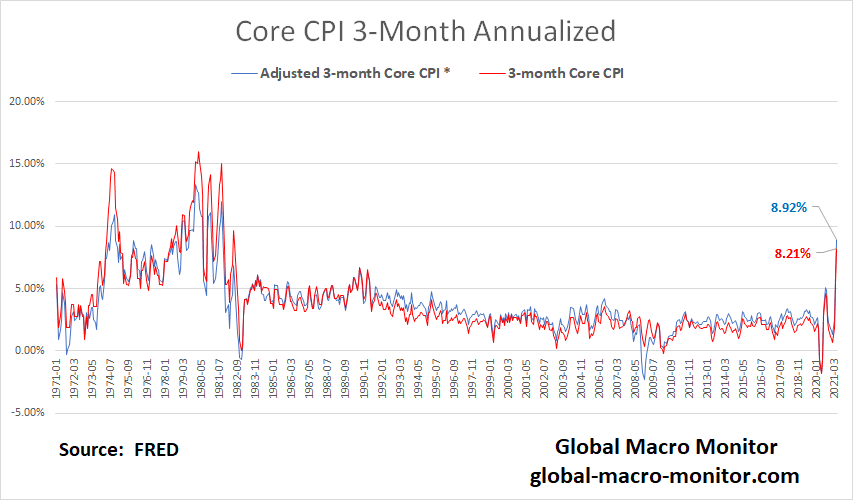

Our central thesis of last’s night piece is that inflation is rapidly accelerating, not just due to the “base effect,” and that financial conditions are far too loose.

We’ve taken the previous three very hot core inflation prints – 0.7%, 0.9%. 0.3% — to construct an annualized 3-month core inflation rate. It’s now running at 8.21 percent, its highest level since July 1982, when financial conditions were very tight during Volcker’s war on inflation, and a month that ranked in the 97 percentile in terms of the most restrictive financial conditions measured by the Chicago’s Fed’s National Financial Condition Index (NFCI).

May’s NFCI was still extremely loose. in the 14th percentile of tight monetary conditions out of the 604 months of the life of the index.

Our Point

That is our point: rapidly accelerating and high short-term inflation with extremely loose financial conditions.

The following chart illustrates our 3-month core CPI index with an adjusted version – 3-month core CPI minus a scaled-up version of the NFCI. It gives more context to the historical inflation data as to whether financial conditions are tight or easy.

Our adjusted core CPI index came in at 8.92 percent in May, the highest since September 1981.

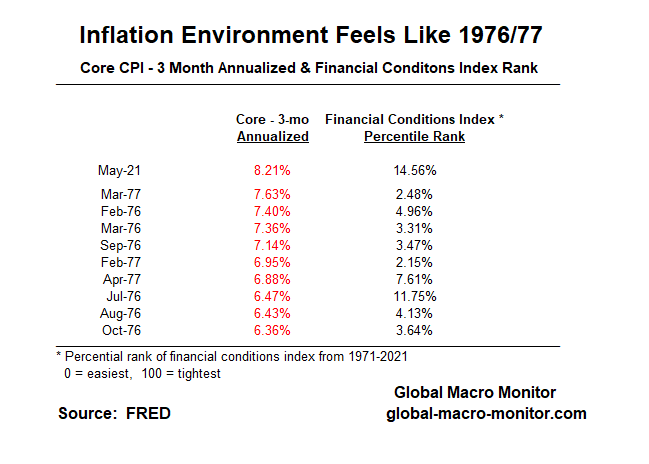

Feels Like 1977

We also looked at all the monthly inflation prints for our core CPI data in the bottom quintile of the months with the easiest financial conditions — i.e., the 20 percent of the 600 plus months where the NFCI was less than -.66215. Just an aside, the monetary authorities, though they have a considerable influence on the NFCI, market conditions, such as the stock market, credit spreads, mortgage rates, also play a huge role. Here are the 105 indicators the NFCI is constructed from.

Case in point, during the depths of the Great Financial Crisis (GFC), even while the Fed was in panic-easing mode, November and December 2008 ranked in the 96th percentile of tightest financial conditions in the history of the NFCI. That was a rare case but becoming more common as financial markets now have an outsized influence on the asset-dependent economy.

The above table illustrates that in the bottom quintile of the months with the easiest financial conditions as measured by the NFCI, the May 3-month core CPI print was the highest of the bottom quintile, somewhat disturbing as it joins the unique company of months just before the big inflation spike during the Carter administration.

Monetizing The OPEC Supply Shock

History Repeating?

Monetary policymakers are faced with a similar dilemma as they were during the mid-1970’s – though there are also many differences. Faced with the COVID pandemic supply shock, they also seem, at least to us, to be repeating the same mistaken reasoning and logic as economic policymakers did back then.

In the middle of 1973, wholesale prices of industrial commodities were already rising at an annual rate of more than 10 per cent; our industrial plant was operating at virtually full capacity; and many major industrial materials were in extremely short supply” (Burns 1974).

…The intellectual consensus among policymakers at the time was that cost-push inflation (the type of inflation arising from an increase in the prices of inputs to the economy, i.e., worker wages) was outside the influence of monetary policy (Romer and Romer 2012). In the words of an economist who presented to the Federal Open Market Committee in May of 1971, “the question is whether monetary policy could or should do anything to combat a persisting residual rate of inflation … The answer, I think, is negative. … It seems to me that we should regard continuing cost increases as a structural problem not amenable to macro-economic measures” (Romer and Romer 2012). – Federal Reserve History

Lack Of Demand Isn’t The Problem, Too Much Demand Is The Problem

We can’t understand why the Fed continues to focus on recovering all the jobs lost during the pandemic by continuing to stimulate demand. For sure, we want everyone that wants to work to have a job and at a decent wage. But…

We snapped this picture last week at a local fast food joint,

Of the 7.6 million unrecovered jobs lost to COVID, 33.3 percent are in leisure and hospitality, and that so-called “huge surplus labor pool” seems more a mirage than reality, as the Fed appears to believe.

How in God’s name is the continued monthly purchase of $40 billion in mortgage-backed securities by the Fed going to help the above restaurant hire, retain, and get its workers to show up? We even now have trouble securing Uber rides as there is a shortage of drivers on the road in our county.

The unemployment benefits have clearly distorted the labor markets. That is a positive statement absent of any political judgment. We are all for more jobs and workers making higher real wages, but it must be practical, effective, and noninflationary. We would take a different approach.

The role of policy, in our book, should be: 1) create an environment where business thrives within the rules, 2) workers are protected and given a boost, if needed, to help them become more productive 3) provide an effective and efficient safety net for those most in need. The private sector creates the wealth, often partnering with the government — markets first, then government when markets fail. Markets do fail.

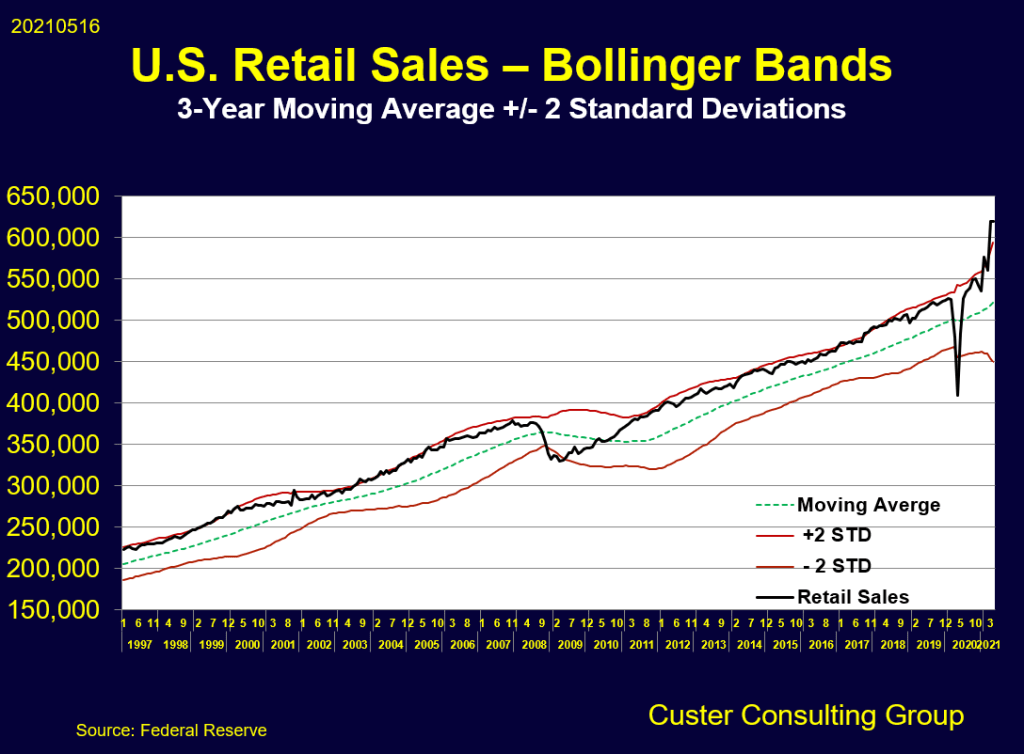

Retail Sales Whipsawed & The Bullwhip Effect

Take a look at how retail sales have been whipsawed during the panic, which has wreaked havoc in global supply chains — yes, excess demand is the main problem — through the “bullwhip effect.”

Let’s consider a retailer sells on average 10 ice creams per day in the summer season. Following a heatwave the retailer’s sales increase to 30 units per day, in order to meet this new demand, the retailer increases their demand forecast and places an increased order on the wholesaler to 40 units per day in order to meet the new customer demand levels and to buffer any potential further increase in demand, this creates the first wave in the exaggerated demand being driven down the supply chain.

The wholesaler noticing this increase in demand from the retailer may then also build an incremental increase into their forecast so generating a larger order on the ice cream manufacturer, rather than ordering 40 units to be manufactured, the wholesaler may order 60 units from the manufacturer, this will further exaggerate the demand down the supply chain and so creates a second wave of demand increase.

The manufacturer also feeling the increase in demand from the wholesalers may also react to the increase by increasing their manufacturing run to 80 units, this creates a third wave in the exaggeration of demand.

The retailer may run out of stock during the heatwave whilst the manufacturer is producing new stock and may take the option of switching to an alternative brand to meet customer demand, this will then create a false demand situation as sales appear to slump to next to nothing so the retailer may then not place further demand for the original ice cream brand even though the manufacturer has increased their production runs. Alternatively, if the weather changes and the end consumers slow down on purchasing ice creams, this could result in an overstock situation across the supply chain as each tier of the supply chain has reacted to the heatwave sales and increased their demand. This is an example of the waves and troughs in the bullwhip effect. – CIPs

The problems in the supply chains are now starting to reduce production and constrain economic growth. Of course, it’s more complicated than our little story but using monetary policy to fine-tune the economy is like trying to thread a needle with boxing gloves on.

Nevertheless, excess demand is a much better problem than no demand, but the stimulus should have been more targeted to those in most need, which is more of a fiscal issue.

Hindsight and criticism from those not in the arena?

Guilty as charged but let us learn from our mistakes.

Upshot

Even if the problems in the supply chain are resolved relatively quickly, we still believe inflation is headed higher for longer, provided the financial markets don’t collapse. The following chart makes us confident – though not certain — of our view.

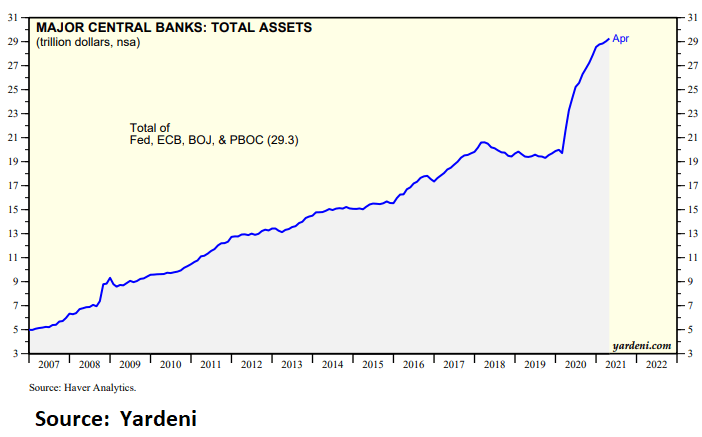

Global central banks have increased their balance sheets by $10 trillion, 50 percent in the past year, and banks now seem eager to lend into the coming Summer of Love The global money punch blow overfloweth big time

Corner Solution: Inflation Or Deflation

Finally, we believe there is very little middle ground in the inflation/deflation debate — i.e., only a corner solution, either high inflation or deflation.

Asset markets are now divorced from economic reality and extremely overvalued. They have such an outsized influence on the economy that any significant correction or disruption will severely tighten financial conditions.

The central banks’ digital printing presses will then be fired up even further, and the endgame, in our opinion, will probably be high inflation for an extended period.

There is no longer any political will to allow true price discovery in the markets. Every 20 point drop in the S&P, the Wall Street clowns cry for a bailout.

Upshot

We believe the U.S. economy is in an unstable equilibrium — if there is such a thing — and fancy the following chart as it encapsulates our macro view in one simple illustration.

We now eagerly wait to be lectured by the 14-year doggie coin traders to tell us how wrong we are.

We’re hedged, however, as we always reserve the right to wrong, and often are.

Calling the markets? Not in your wildest dreams. It’s hard to predict what kind of pizza Elon may eat on any given day and how it may affect what he Tweets.

Never in my wildest imagination did I think the financial markets would become the farce they have.

Stay tuned, folks. and please continue to pray/think positively for CK’s recovery.

First, folks, please send your prayers, thoughts, good feelings, positive energy, miracles, healing touch, whatever you got, and whatever it takes to GMM’s beloved Carol K., who keeps battling, never giving up against a serious disease in Boston at one, if not the best hospital in the world. Even in her critical condition, she contributed to this post — though she may not agree with all its final points. She’s truly an amazing and incredibly strong human being. Semper Fi and Godspeed, CK.

We had a few requests to write up something about today’s hot U.S consumer price inflation data. So we put together a quick note in honor of our friend from down in the Land of Oz, GMac, one of the most decent human beings on earth. He is one proud father of a super studly 18-year son, who is an incredible surfer and someday wants to surf Mavericks. God. Bless. His. Soul.

Let us preface our inflation note with one of our favorite quotes:

World War II was transitory – GMM

Recall our post in January, Ready For 4 Percent CPI By Mid-Year?, when we speculated the U.S. would be experiencing 4 percent inflation, possibly 5 percent by mid-year. We were beaten down like a red-headed stepchild (I am at liberty to say that as I have been a ginger most of my life).

GMM was also one of the first to point out the base effects (12-month comps) would kick in April and May 2021 due to the deflation that troughed last year from the COVID crash. But don’t be gaslighted the lastest few month-on-month core prints essentially negate the base effect excuse for high inflation as three-month core CPI is now running at 7.9 percent on an annual basis.

We don’t know for certain if inflation will stick and move higher or lower but as betting folk we are taking the over, however.

Liquidity Tsunami

We do know the major global central banks have pumped in a shitload of high-powered money into the global financial system over the past year — as in around $10 trillion, close 50 percent increse of their collective balance sheets. Here’s Dr. Ed’s excellent chart,

Moreover, banks now seem eager to start lending, thus creating more endogenous money on top of the trillions upon trillions of base money central banks have already injected.

Transitory? Yeah, right.

It’s not a question whether the Fed has the tools to reign it in, it’s do they have the ‘nads? Given the multiple asset bubbles that would burst, and bust spectacularly, if the Fed draws it word, we seriously doubt it.

The following chart from Dr. Ed also illustrates not only has the digital printing press been working overtime, the credit system is just fine and dandy as deposits are expanding. Don’t be confused by, yes, the base effect, as the money aggregates have a much large base to grow from they did a year ago before the pandemic.

Tough to beat comps after expanding over 25 percent

Note, these are monetary aggregates, which include cash in circulation, bank deposits among near money and other short-term time deposits, not the expansion of the Fed’s balance sheet, though it does hugely influence the data.

Big spurts from the digital printing press without a credit crisis and an impaired financial system — as was the case after the Great Financial Crisis — will almost always generate inflationary pressures. Stimulating demand without production during a supply shock is not optimal unless carefully targeted to those who need it most.

It’s very amusing to us to see the FinTweets, “peak inflation has arrived.” True, if the financial markets crash. But what do they base their conclusion on? A warm feeling in their tummy?

Banks now seem eager to start lending, thus creating more endogenous money on top of the trillions of base money central banks have injected.

Loans are “starting to pick up,” and there’s plenty of borrowing capacity because companies have unused credit lines, {BofA CEO Brian ]Moynihan said. Loan growth has been a challenge across the banking industry because many consumers and businesses are sitting on cash from savings and stimulus during the pandemic. – Bloomberg, June 6

This should send shivers up the Fed’s spine, but we are not so sure. We are also not so sure they are not flying blind and will again miss the next big one just as they have in the past.

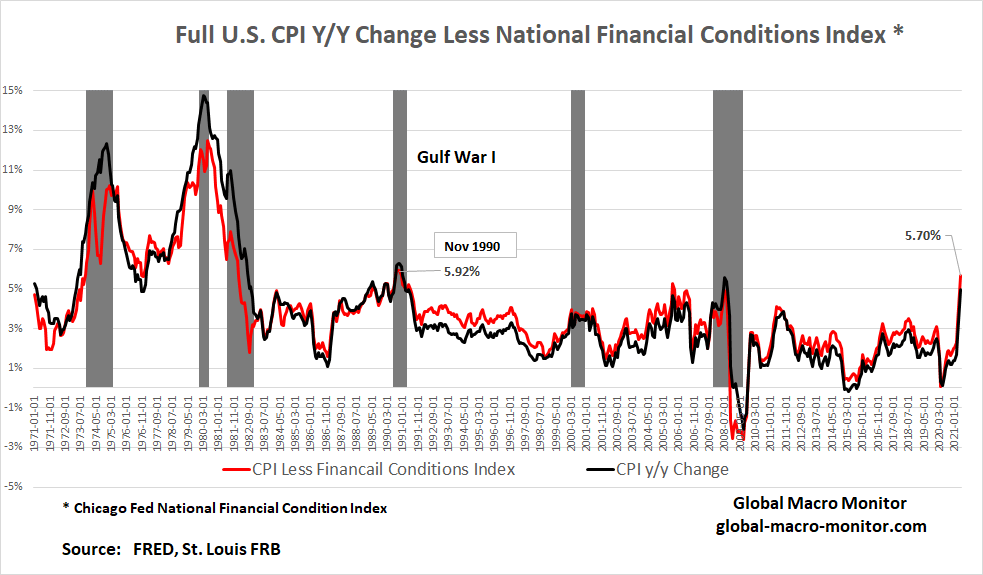

The Chart: Liquidity Adjusted Inflation.

It’s late and we want to present the chart in honor of GMac.

We have taken the non seasonaly adjusted year-on-year change of CPI and subtracted a scaled up version of the Chicago Fed’s National Financial Conditions Index (NFCI), which measures how loose or tight monetary conditions are in the U.S.. It’s has been running at an extreme historical low — i.e., very loose financial conditions.

We are trying to give context to the inflation data of how loose and accomodative finnancial market and monetary conditions are currently. As you can see, today’s year-on-year CPI print less the NFCI is at the highest level since November 1990, which was in the middle of the first Gulf war, Where the Fed was facing spiking inflation due to the run-up in oil and a recession.

Prior to that our adjusted inflation index hasn’t been so high since the high inflation late 197Os and early ‘80s. Gulp.

Clearly, it is a different environment in today’s economy. In fact, just the opposite – the economy is ready to roar for the next several quarters as consumers are flush with cash, the supply chain is still a mess due to the “bullwhip effect” (more on this in a future post), and new businesses should be looking for credit and loans to rebuild and start new ventures.

Most of all, folks, the central banks still have their pedal to the metal and balls to the walls, and as we all know (well some of us),

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output. – Milton Friendman

The Upshot

Inflation is way too high given exremely easy financial and monetary conditions. There will be blood.

Finally

Life is transitory.

Inflation has eroded my purchasing power in my transitory life. Bring back the $.35 Big Mac, which was only about 20 percent of the minimum wage. Now? About 40-50 percent. Enough to spark a revolution.

Finally, the Democrats should begin to worry.

Biden inflation is real, and it’s happening right now. It’s hurting Tennessee’s poorest families and workers the most, and is a clear and immediate tax on the middle class. pic.twitter.com/tvcStztWah

— Senator Bill Hagerty (@SenatorHagerty) June 10, 2021

I am asking GMM readers to send thoughts, prayers, postive energy or whatever you got to our beloved Carol K., GMM’s Chief Money Printer, as she battles a serious illness in Boston. She’s the best, we’re hoping for the best, and she deserves the best. Godspeed, CK.

Great chart from our friends at Strategas, one of the best research shops on the Street.

It looks fairly clear, at least to us, the U.S. has put the pandemic in the rear view mirror and is now ready to fully reopen the economy.

We think so. The daily new case curves are turning down and though the death curve will lag for a few weeks, it will also start to turn down soon.

Thank, God, we can see the light at the end of the tunnel. – GMM, Jan 24

Last April, using a simple exponential growth model, we said this,

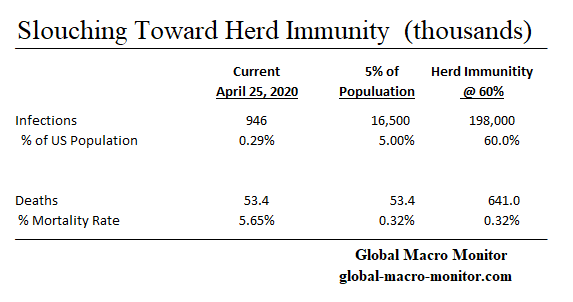

We’ve put together some back of the envelope calculations in the following table based on simple assumptions that 5 percent of America’s population is currently infected, which drops the concurrent mortality rate down to 0.32 percent, very generous compared to the 2 percent estimate that holds with the conventional wisdom.

Using that mortality rate, assuming 60 percent of the American population is eventually infected, the death toll will rise to 641,000, which puts us in about two outs in the bottom of the first in a nine-inning baseball game. – GMM, April 25, 2020

We didn’t get all the math right but, very sadly nailed the estimate of the final pandamic death toll. We projected U.S. deaths would rise to 641k from the then level of 53.4k, which invited a week of pushback, beatdowns and hate mail.

The final death toll is going to come in pretty close to our estimate. COVID related deaths in the U.S. are currently running around 601k.

History will write that many of the deaths could have been prevented and were the result of the country’s lack of leadership and toxic politics. At the same, historians will look back at the almost miraculous creation of a vaccine less than a year after the breakout as a sign of America’s ingenuity. Shameful but thankful.

Can’t wait to hear the Chairman justify zero rate policy and deficit monetization with inflation roaring at > 5 percent. It would be entertaining, if it weren’t so damaging.

Watch Jay Pow stumble over this question of why they are buying $40 billion a month in mortgages when there is a dearth of supply in housing.

Here’s a pretty good theoretical model (follow the entire thread) estimating that U.S. inflation may reach double digits by Q1 2022. One of the premises is that monetary authorities have no way out of this rabbit hole and are constrained by the risk of severely disrupting financial markets in an asset dependent economy.

Recall our view that deflation/inflation is a corner solution and Wall Street’s “Goldilocks” scenario is still just a marketing gimmick. Deflation as markets try to move back to mean valuations – a lot lower – or inflation, and lots of it.

1/n How much excesss liquidity has US monetary easing created? And how much inflation will it create?

Anyone with a better model, lay it on the table. Stop with the “fake news” or “don’t worry” nonsense. CPI prints > 4 percent in May and you heard it here first.

GMM’s HealthWars

CK and I are battling some serious health issues. Mine, an acute skirmish, which I am now recovering.

CK’s, a three-front protracted war. Her courage to get up and fight everyday has been such an inspiration during my little battle. She also saved my life by forcing me to “ignore my primary doctor’s diagnosis of “all is well” and aggressively pursue my symptoms.” If not for that, the Grim Reaper would have liquidated my position and GMM would be no more. Thanks, CK.

Love this kid and his refreshing dose of common sense in a world of panic buying and creation of “fake scarcity” with too much money driving asset prices, and now prices of goods and services. Maybe he, like I, is just not woke enough to the miracles of Modern Monetary Theory.

I am fairly confident, 80 percent probability, year-on-year CPI prints above 4 percent in May, and believe there is a much higher probability than markets are pricing that a 5 percent CPI prints sometime this year.

Base effect? Yes, partially, for the next few months. Transitory? Only if money supply growth falls dramatically but can it without asset markets collapsing?

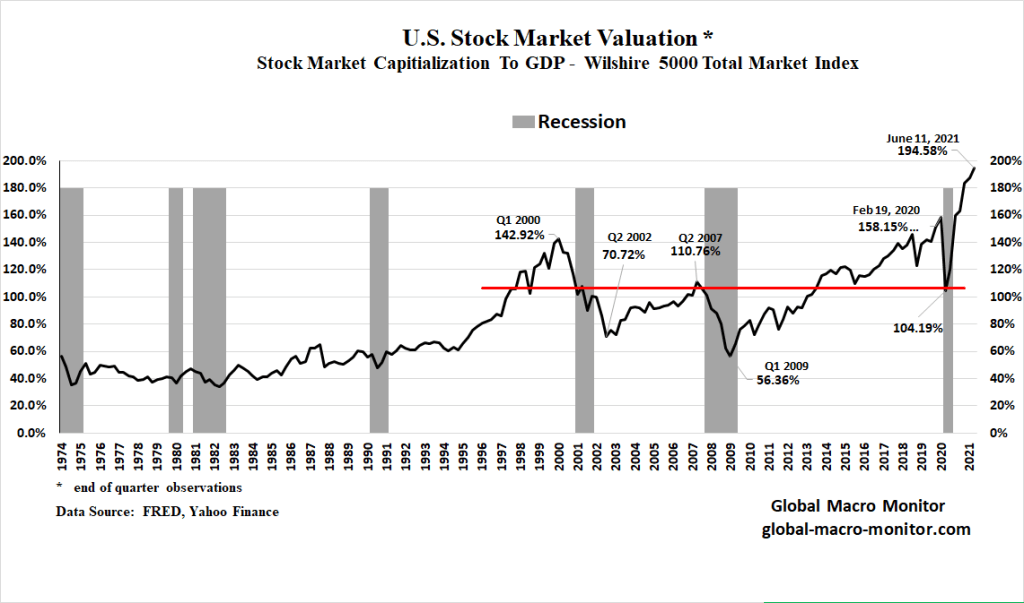

At the market close on Friday, we estimate the U.S. stock market cap hit 200 percent of GDP, which is 40 percent higher than the dot.com peak. That is a 40 percent higher valuation folks, not levels.

They can be rare—gold bars, diamonds, houses on Victoria Peak, bottles of 1982 Pétrus, Van Gogh paintings, or

They can generate cash flows over time

We have been writing for years how the supply-side (relative shortages) has been increasingly driving financial asset values.

Also, run, don’t walk to our donut shop analogy. – GMM, July 2020

Market Anarchy

Markets have become what hedge fund manager, David Einhorn, calls quasi-anarchic, and on the verge of “breaking completely.” We just call it what it is, unhinged and morphing into a complete farce.

Someone pointed us to Hometown International (HWIN), which owns a single deli in rural New Jersey. The deli had $21,772 in sales in 2019 and only $13,976 in 2020, as it was closed due to COVID from March to September. HWIN reached a market cap of $113 million on February 8.

The largest shareholder is also the CEO/CFO/Treasurer and a Director, who also happens to be the wrestling coach of the high school next door to the deli. The pastrami must be amazing. Small investors who get sucked into these situations are likely to be harmed eventually, yet the regulators – who are supposed to be protecting investors – appear to be neither present nor curious. From a traditional perspective, the market is fractured and possibly in the process of breaking completely. – Greenlight Capital Letter To Investors

Ya’ know that one deli in Jersey is scarce, they are not making another one.

My Boston Buddy’s Kid

My buddy, a fund manager from Boston conveyed to me today his teenage kid believes he is a genius Dogecoin trader using his Robin Hood account. He wanted to borrow money from his parents to buy more. He’s made $800 on a $500 investment.

To wit, I sing,

How much is that Dogecoin in the window worth? The one chasing Elon’s tail How much is that Dogecoin in the window worth? We do hope that Dogecoin will sail [to the moon]

What could ever go wrong? As an old trader, I get the trade but I have seen this movie many times. It doesn’t end well.

Who would of thunk “Infrastructure Week” at Augusta meant hiring German WWII POWs to build bridges at Golf’s Mecca.

My top three picks this week for total money won: Jon Rahm, Jordan Speith, and Phil, with the Spaniard (Rahm) taking home the Green Jacket.

Golf’s Ultimate Shame

Awesome to see Lee Elder hit the ceremonial first tee shot. Lee Elder was the first Black man to play in the Masters back in 1975. Shame on Augusta National for not allowing a Black Man to play their tourney until 19-freakn’-75. Shame on the PGA Tour’s “Caucausian only clause,” in place from 1934-19-freakin’ 61, that prevented non-whites from competing on the PGA Tour.

Anthony Kim posted 11 birdies in the second round of the 2009 Masters.

Here’s some more 19th hole fodder to impress your buddies and something I bet you didn’t know about Augusta: German POWs from nearby Camp Gordon built the bridge over Rae’s Creek next to the 13th tee box during WWII. They were part of Rommel’s Panzer division in North Africa responsible for building bridges to enable tanks to cross rivers.

While Augusta National is famed for its almost unnaturally beautiful flora, as it turns out some rather interesting fauna once called the course home as well: 200 heads of cattle and more than 1,400 turkeys. From 1943 until late 1944, Augusta National was closed for play and transformed into a farm of sorts to help support the war effort. Some of the turkeys were given to club members during Christmas (meat rations were in effect) while the rest were sold to local residents to help fund the club. And the cows? Well, they acted as natural lawnmowers but also inflicted quite a bit of damage to Augusta National, devouring many of the course’s famed plants and shrubs.

To help repair cattle-related damage and revive Augusta National for its reopening, 42 German prisoners of war from nearby Camp Gordon were shuttled back and forth to work on the course.

“The POWs had been with the engineering crew serving Rommel, the Desert Fox, in North Africa, part of the Panzer division responsible for building bridges that enabled German tanks to cross rivers. It was a useful skill for the renovation work to be done at Augusta National. The Germans were asked to erect a bridge over Rae’s Creek adjacent to the tee box at the thirteenth hole.”

The Masters resumed at Augusta National — now free of German prisoners and barnyard animals — in 1946. And interestingly enough, the Supreme Commander of the Allied Forces in Europe during World War II, Dwight D. Eisenhower, later became a member of Augusta National. Two Augusta National landmarks bearing Eisenhower’s name still stand today: the Eisenhower Tree (a loblolly pine at the 17th hole that the former president and avid golfer repeatedly struck with golf balls and requested be cut down; photo above) and the Eisenhower Cabin (built in the 1950s according to Secret Service security guidelines by the club for the former president’s visits).