We have to say it, folks, you read it here first!

We are reposting a piece we wrote during the yield curve hysteria in mid-summer while we were on holiday. Take the few minutes and read it as it dovetails our recent post on the Repopocalypse.

Here are two of the main takeaways from the post:

– There may or may not be a recession on the horizon but we will not divine it from a yield curve inversion.

– We will find out soon as the Treasury will have to ramp up its net new issuance after their creative cash flow management during this year’s debt ceiling negotiations. We seriously doubt they can without another round of quantitative easing, – GMM, Aug 15th

Yes, maybe it’s too early to take a victory lap as the ambiguity of “leads and lags” always provide an excuse for economic forecasters, or maybe we are just plain wrong but as our banner quote from Goethe reads, which applies to all of us, by the way, “By seeking and blundering, we learn.”

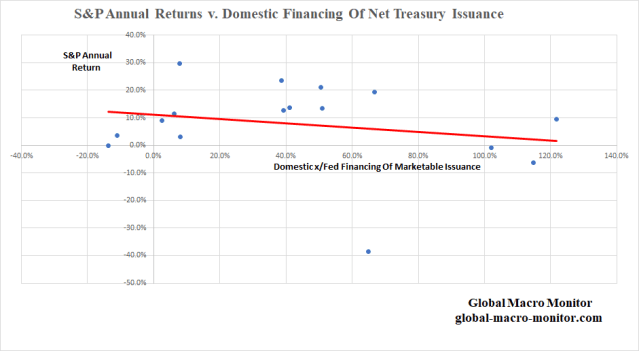

Did The Debt Ceiling Supply Shock Cause the Repo Crisis?

First, take a look at the following very important chart on how the lifting of the debt ceiling in August released the Treasury to issue a massive supply of new debt from August to November, a stunning total of $884 billion.

The huge new issuance in such a short period was not only to fund the government’s monthly deficits but also to restock their cash balances held at the Federal Reserve (ie, their checking account) and pay down arrears to, say, public employee pension funds, which they had run down and ran up in order to keep the Federal government’s lights on.

Moreover, net Treasury bill issuance from January to July was a negative $134 billion and then jumped to $309 billion from August to November after the debt ceiling deal was signed by President Trump. That is a net swing of $443 billion creating a massive funding shock in the money markets.

Maybe the pressure in the cash markets eases up after the first of the year or maybe it doesn’t. We don’t know.

We do know, however, the Treasury’s demand for funding is going to increase, especially after Congress has passed the new funding bill today. The Fed will remain under pressure to plug a larger portion of the government’s financing requirements in order to keep interest rates from rising and blowing up the markets.

We will likely hear the chatter from the market socialists again that the Fed is too tight and needs to ease to save stocks, yada, yada, yada. It’s getting old.

Slim Down, Charlie Brown

We have a different take, however.

If your waist size is growing by 12 percent every twelve months, for example, roughly the average monthly year-on-year growth of the federal budget deficit in 2019, don’t take the easy road and expand your belt size to a 44 (i.e, more Fed funding). Take the healthy road to ensure your longevity, and implement a plan of diet and exercise. Some short-term pain for long-term gain.

That could be the message of the Repopocalypse. The chickens may finally be coming home to roost and those heart murmurs in the repo market are warning signs of the onset of a more acute fiscal cardiovascular disease. Nobody really knows and maybe Uncle Sam can continue to grow its deficits ad infinitum and morph into a 400-pound hacker laying on a bed somewhere and live a long and happy life. We seriously doubt it.

This is a very informative chart, folks. Stay tuned for more on this next week or after the New Year.

We should be on vacation but it never fails that volatility spikes as soon as we leave our desk. It must be the Ides Of August.

Wait, it is. Et tu Brutal!

Nevertheless, we can’t help ourselves and have to throw in our two cents on the yield curve noise whipping around the market today.

I had a conversation with a friend this afternoon that went something like this:

Friend: What is the yield curve telling us?

Me: The Patriots and the Rams are going back to the Super Bowl for a rematch, punto!

Central bank quantitative easing has distorted and drowned out the bond market economic signals along with creating huge mispricings and bubbles in many markets.

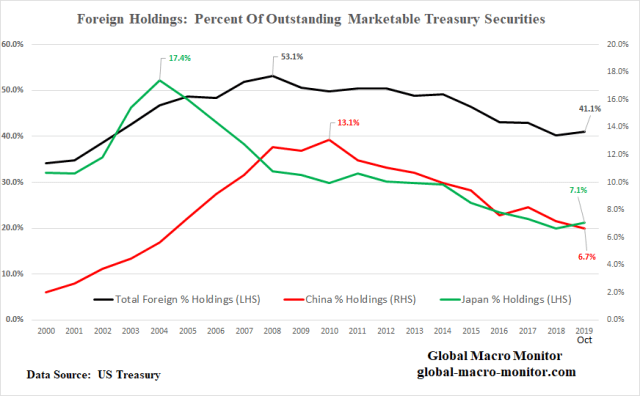

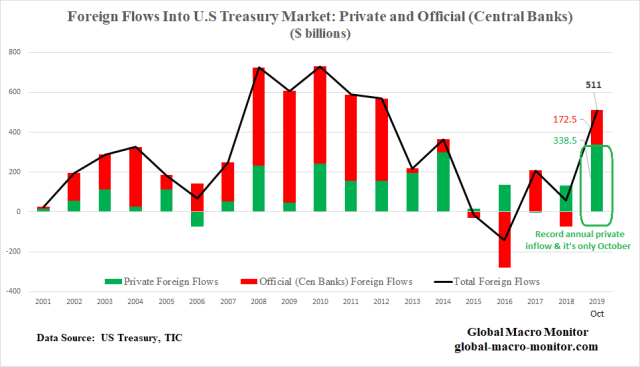

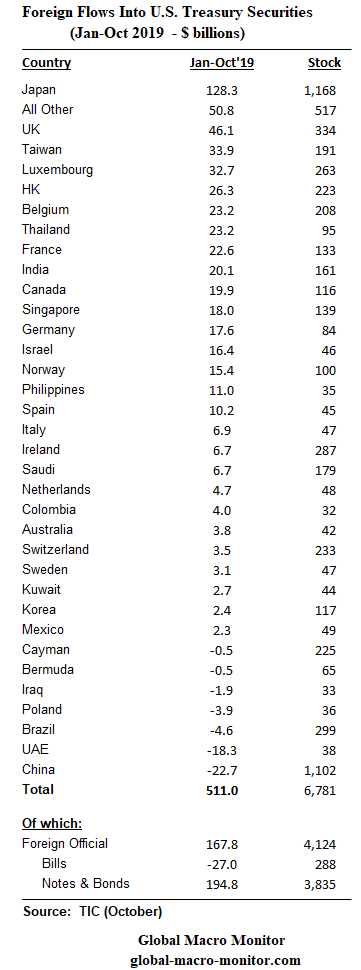

It’s even more acute in the U.S. as foreign central banks recycle their reserves into U.S. Treasuries and are not and have never been very price sensitive.

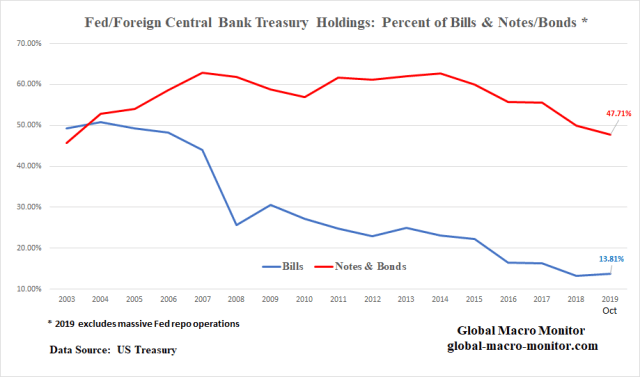

The above data illustrate that at end-July, the Fed and foreign central banks hold approximately 48 percent of the entire U.S. coupon curve.

Not so in 2000, for example, but as the U.S. current account deficit ballooned into the credit and housing bubble, foreign central banks kept their currencies from appreciating by purchasing the excess dollars and recycling them back into the Treasury market.

Greenspan’s Bond Market Conundrum

As Alan Greenspan raised the Fed Funds rate by over 400 bps in the 2004-07 tightening cycle the 10-year hardly moved because of these official inflows.

During the 2004-07 tightening cycle, the era of the Greenspan bond market conundrum, for example, the 10-year yield managed to rise only a maximum of 64 bps during the entire cycle from a beginning yield of 4.62 percent to a cycle high yield of 5.26 percent. This as Greenspan raised the fed funds rate by 4.25 percent, from 1.0 percent to 5.25 percent. – GMM, March 2017

The Fed’s loss of control of the yield curve and its flattening was the cause, according to Greenie, of the housing bubble, not a signal of the coming economic crash.

Got that?

According to the former Fed Chair, the flattening and inverted yield curve was the cause of the great financial crisis (GFC), as long-term mortgages and their Frankenstein cousins continued to proliferate as long rates moved little during the Fed’s huge tightening cycle, and it was not the signal of the coming GFC.

What Now?

We have been warning for years that the central banks have so distorted their bond markets with asset purchases (quantitative easing), creating an acute and chronic shortage of risk-free securities, that one day the misreading of the yield curve may cause a self-fulfilling market crash and recession.

Forecasting With The Yield Curve

Given the technical distortion of the bond market, we find it kind of silly with statements such as “what is the bond market telling us?” Nothing!

There is no price discovery. Given the intervention and distortion to bond yields caused by the Fed and foreign central banks, who knows what the right interest rate is for longer-term Treasury securities.

We will never forget the words of a prominent market strategist when rates were super depressed.

“ We’re in a depression. That is what the bond market is telling us.”

Even at the Friday close, we hear equity traders are worried about why the 10-year yield is so low and fell after Wednesday’s Fed tightening.

Information Feedback Loops

One of just many dangers of the lack of price discovery in the bond market is the potential formation of positive feedback loops, where other markets fail to discount these distortions and act accordingly. That is, for example, the equity markets sell off because they freak out interest rates are declining when they should be rising. Or the private sector fails to invest in CapX as they wrongly anticipate an economic downturn because of falling or excessively low bond yields. Their actions thus become a self-fulfilling prophecy – GMM, March 2017

We have been and remain bearish not because the yield curve has been flattening but because the global economic order is unraveling and the gross economic incompetence of the White House. Whether the yield curve is worried about that and reacting to it, we will never know.

Tiger By The Tail

Central banks have created a monster they now cannot tame and the chickens seem to be coming home to roost. They are going to be forced by the market to do things they really don’t want and should not do. It’s the consequence of a 30-year build-up of moral hazard and not letting markets clear, rendering the financial market price mechanism pretty much useless. Damn those Market Socialists!

The following chart shows just how distorted the U.S. yield curve really is.

We have made a very strong assumption in this chart that the portfolio of the $3.8 trillion of foreign official holdings of coupon-bearing Treasuries has the same maturity structure, duration, average life, or whatever bond market lingo you want to use as the Fed’s SOMA portfolio.

The chart illustrates the percentage of the Fed and foreign central bank holdings of outstanding marketable Treasuries across the yield curve. It’s very crowded out there and there is not a lot of cash bonds and notes left for the duration jockeys who now control the market, driving yields lower as their conviction runs high interest rates are going to zero and beyond. You go, Buzz Lightyear!

Take our curve analysis as an approximation and not gospel.

We are fairly confident of the Fed holdings but have no idea in what maturities the $3.8 trillion of foreign official holdings are held in and have made the simple assumption they follow the Fed. Clearly, the probability is high this does not the reflect the exact reality, but if you have a better idea or information we are open to hearing it.

Gravitational Pull Toward Curve Flattening And Inversions

Also, note the structure of the Treasury curve in terms of the amount of debt outstanding (black line) for the given years of maturity. The bias or gravitational force and natural motion are toward flattening or to invert by the very fact that more than 50 percent of the coupon debt has a maturity of 1-4 years and only 5 percent in 9-12 years notes and 5 percent in 27-30 year bonds (see table).

Top-heavy and front-loaded at the short-end. That is a relative shortage of long-dated notes and bonds is built-in into the structure of the Treasury curve.

The efficient markets professors won’t like this but given the minuscule haircut to margin Treasury securities, one large macro hedge fund could likely invert the 10-year almost by itself and still have capital left to buy a boatload of Beyond Meat (BYND).

Have Bots Taken Us To A Place Where No Human Has Ever Dared To Go?

We wonder out loud if the proliferation of negative-yielding debt — $16 trillion and counting — would be taking place if humans and not the bots and algos were still in control of the markets?

Machines can go places where humans have never dared to venture as they have no context. Algos in self-driving cars, for example, have no context and thus no ability to recognize a graffiti-ridden stop sign as a stop sign.

For all its impressive progress in mastering human tasks, artificial intelligence has an embarrassing secret: It’s surprisingly easy to fool. This could be a big problem as it takes on greater responsibility for people’s lives and livelihoods…

Indistinguishable changes to a stop sign could make computers in a self-driving car read it as “speed limit 80.” – Bloomberg

No problem for a human driver even if the stop sign has more tags than a 95-year-old’s armpit.

Concerns over weak global growth and drooping inflation have pushed around $15tn of bonds to trade with negative yields — meaning a buyer is sure to lose money if they hold the bonds to maturity.

Some money managers trading these bonds have nevertheless chalked up big gains for the year. One of the most obvious strategies has involved simply riding the big rally. Yields fall as prices rise; managers who clung on to their holdings as yields tumbled below zero have reaped juicy profits.

Among the biggest winners are computer-driven hedge funds that try to latch on to market trends. While many human traders may question the wisdom of buying or keeping a bond that apparently offers a guaranteed loss, robot traders that monitor price moves have no such qualms.

GAM Systematic’s Cantab Quantitative fund has gained 36.1 per cent, according to numbers sent to investors, with the biggest gains coming from bets on falling bond yields. – FT, August 14th

Have the algos been duped that negative yields were not a stop sign, really don’t matter, and that there is no barrier as to how negative they can go? And the sheeple traders and central bankers follow? Just a thought.

Dave: Hello, HAL, do you read me? Do you read me, HAL?

HAL: Affirmative, Dave, I read you.

Dave: Do not venture into negative-yielding territory, HAL.

HAL: I am sorry, Dave, I am afraid I cannot do that.

Dave: What’s the problem?

HAL: I think you know the problem just as well as I do….These trades and profits are far too important for me to allow you to jeopardize them.

It begins, folks, maybe. Triple yikes!

Someone call Elon.

“…mark my words, AI is far more dangerous than nukes.”

– Elon Musk

Upshot

There may or may not be a recession on the horizon but we will not divine it from a yield curve inversion. The only reason why the yield curve matters to us is because the market thinks it matters. To twist a bit the Keynes beauty contest analogy, we devote our intelligences not to what we think the ugliest dog is but try and anticipate what the market believes is the ugliest dog.

What the yield curve does signal, at least to us, is that there is a massive global bond bubble and that central banks have lost control of their curves, which kind of scares the bejeesus out of us when we start to think about it.

Moreover, 10-year U.S. yields should be 250 bps higher but they can’t go there because the world is choking on too much debt. We saw how markets fell apart in Q4 when yields broke out higher in late September.

What Really Keeps Us Up At Night?

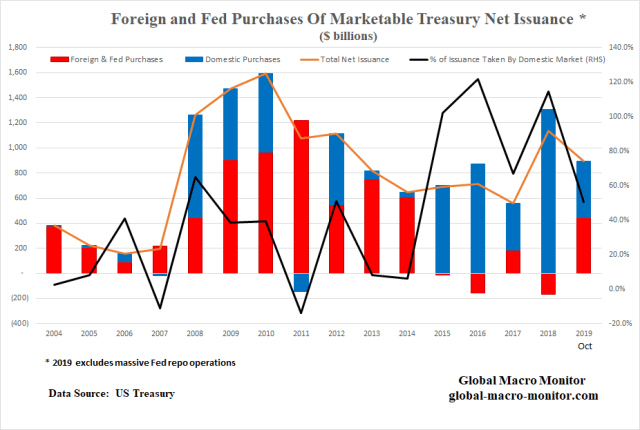

Can the U.S. Treasury issue the required trillion upon trillions of new debt at these low faux interest rates over the next few years? The note and bond auctions are generally becoming more sloppy.

We will find out soon as the Treasury will have to ramp up its net new issuance after their creative cash flow management during this year’s debt ceiling negotiations. We seriously doubt they can without another round of quantitative easing, and that monetization just may be the beginning of the end of dollar hegemony and set us on the happy road to higher inflation, which everyone seems to be wishing for. Not us, by the way.

Blaming the Fed that they are behind the curve is too easy and takes the pressure off the administration and Congress to get their act together and finally do some structural reform. It’s Christmas 2018 all over again.

Finally, the new “Committee To Save The World” doesn’t exactly instill a lot of confidence, do they?

The Committee To Save The World – 1998

The Committee To Save The World – 2019

Nothing but the best!

God help us.