I loved this commercial when everyone was a stock market genius back in the late 1990’s, that time was different, and eyeballs trumped earnings.

I loved this commercial when everyone was a stock market genius back in the late 1990’s, that time was different, and eyeballs trumped earnings.

We find it interesting that many accuse us of being China apologists because we have concluded from our analysis long ago that President Trump is taking the wrong approach in dealing with the Middle Kingdom. No argument here we have issues with China that need to be addressed. China has outgrown its developing country status and its special treatment within the WTO should be removed. We also are realistic that trying to get China to change its economic model because the U.S. demands it is a nonstarter.

Moreover, going it alone, leaving the TPP, negotiating out of ignorance, impulse, and through tweets, and using tariffs so cavalierly have been, are, and will be a disaster. We believe the deterioration in global trade is the major factor that is tanking the global economy. Go no further than Germany to confirm this.

Cuban Missile Crisis

Compare the current U.S.-China negotiations with how President Kennedy ended the Cuban Missile Crisis. There were many different paths JFK could have taken. Some of his hawkish advisers wanted to bomb Cuba immediately, some wanted regime change in Cuba, as many in Trump’s inner circle want an economic regime change in China.

Nobody disagreed the Soviet missiles in Cuba had to be removed.

President Kennedy had to weigh different advice, including starting a nuclear exchange and, you know, things like the end of the world issues. He knew what was doable and what was not.

JFK had a fluid and strategic plan and executed it. A real Art of the Deal.

He was cool, calm, and collected. Grace under pressure.

Furthermore, President Kennedy didn’t have the psychological need to be the apparent winner in the conflict. He gave the Soviets an out by pulling missiles from Greece and Turkey, which Kruschev could sell to the Moscow hardliners as an American concession. The President took a lot of heat from Congressional hawks for removing the missiles.

Oscar Shindler Jumping Ship

Today, we are finally getting a sense that many of what we call Trump’s Oscar Shindler supporters, those who don’t like him but profit from his tax cuts and economic policies, are starting to wake up to the fact that Trump is an economic nationalist, bad for the country, and is FUBARing the global economy.

Stay tuned.

P.S. Just heard a Freudian slip by a talking head on Bubblevision, “President Chump said…” It begins.

One year to this very day l flew to the east coast to check out colleges with my then 15-year old. Check Penn off the list.

The following is from an economics major from the University of Pennsylvania.

By the way, foreign money has been pouring into the U.S., not so much now, in large part due to the U.S. trade deficit. It is clear POTUS is clueless not only about monetary policy but also about balance of payments.

God help the United States of America.

The most difficult subjects can be explained to the most slow-witted man if he has not formed any idea of them already; but the simplest thing cannot be made clear to the most intelligent man if he is firmly persuaded that he knows already, without a shadow of a doubt, what is laid before him. – Leo Tolstoy

A question has been nagging us for some time. If the current sovereign yields are repressed and fake, many of which are negative, can the borrowers issue any significant amount of new debt at these current yields? Especially to long-term holders?

We are just thinking out loud here but our priors are that of the Big Three — U.S., Germany, and Japan — which have relatively transparent markets as opposed to China, the U.S. is the only government that needs to issue a significant supply of debt and bonds into the market.

Germany

Germany runs a perennial budget surplus and is actually reducing the stock of bunds in circulation with the ECB now contemplating lifting its self-imposed cap of 33 percent of holdings on a single issuer to 50 percent in the event of a new round of QE. Witness the negative 50 bps yield on the 10-year bund. Zero new supply and anticipated central bank demand. See our Bund Dearth post here.

Japan

Japan runs a budget deficit of 3-4 percent of GDP but is a net saver and the BoJ owns almost half of the Japanese Government Bonds (JGBS). We are less familiar with the JGBs x/ our painful memories of shorting them in the 1990s. Need to do further research.

Fake Yields

The current yields do not reflect fundamentals, in our opinion. We suspect the Fed and other foreign central banks now own about 40-50 percent of all marketable Treasuries outstanding with maturities of 10-years or longer and much of the rest of current holders are duration jockeys, such as stock short-sellers to timid to be exposed to the painful and nutcracking equity short squeezes, such as today. We seriously doubt these jockeys partake in the bond auctions.

Auctions

So we are watching the Treasury auctions closely and suspect they could get sloppy and ugly down at these yields.

But there’s general agreement among analysts that the plateau in issuance can last only so long. The bipartisan deal to suspend the debt limit for two years also paves the way for a $324 billion increase in government spending over the period above existing budget caps. That’s emboldening most dealers to pencil in increases in debt sales by fiscal 2021, which starts in October 2020.

“The deficit is rising and the impetus toward higher spending is very strong,” said Stephen Stanley, chief economist at Amherst Pierpont Securities. “By the second half of next year Treasury will have to raise coupon sizes again.” – Bloomberg

Rent Control Problem

With repressed yields a sort of “rent control” problem arises, where there is a shortage of funds at the given fake or below market yield. Just as the case with a shortage of housing when rents are held below their market rates.

This is just a thought and first cut and needs to be further fleshed out.

Poor Bond Auctions

If the price of Treasury’s borrowings is repressed, the excess demand will be 1) cleared by rising rates: 2) supplied by the central bank either directly (not legal in U.S.) or indirectly through some sort of QE, and/or 3) sucked out of other markets, such as equities or corporate bonds, in the the form of haven flows, for example, which means lower prices in those markets.

If foreigners make up the difference, up goes the dollar. Not many good choices, no?

Meet your new crowding out effect, folks.

Are our instincts on to something?

Investors submitted bids for 2.39 times the $38 billion of three-year notes offered by the Treasury Department on Tuesday, the smallest so-called bid-to-cover ratio for that maturity in a decade. This is no anomaly. In May, the bid-to-cover ratio at a 10-year auction was also the lowest in a decade. These are far from failures, and plenty of other factors besides creditworthiness go into investors’ decisions about whether to participate in a bond auction. At the top of the list is monetary policy. But that’s the thing — the Federal Reserve has turned dovish, suggesting an interest-rate cut could come as soon as this month. And while U.S. yields are low by historical measures, they are still higher than investors can get anywhere in the sovereign bond market in developed economies. Even so, foreign holders have cut their holdings to about 40% of the marketable U.S. debt outstanding, from more than 50% before the financial crisis. It’s hard not to come to the conclusion that demand for U.S. bonds isn’t limitless, which is a scary thought with the government on track to borrow $1 trillion to finance a budget deficit by the same amount. Expect to hear more about U.S. borrowing in coming months. Strategists expect the Treasury to exhaust its borrowing authority in late September or early October. – Bloomberg

Stay tuned, folks, this could be THE Black Swan. A low probability, high impact end of the world event on nobody’s radar.

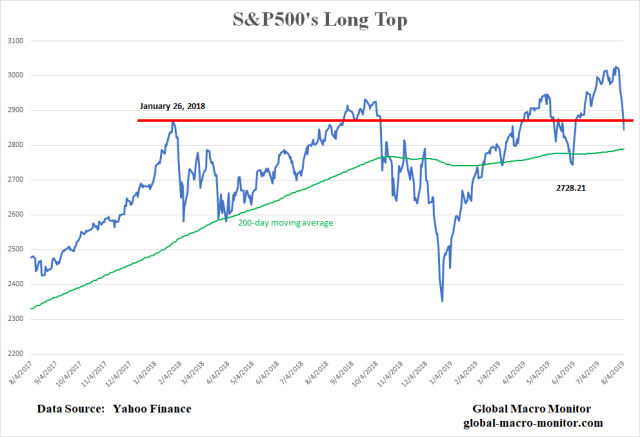

The S&P got whacked again today and is now about 1 percent below its first peak of January 26, 2018, in this very long topping process. In other words, stocks have gone nowhere for the past 18 months.

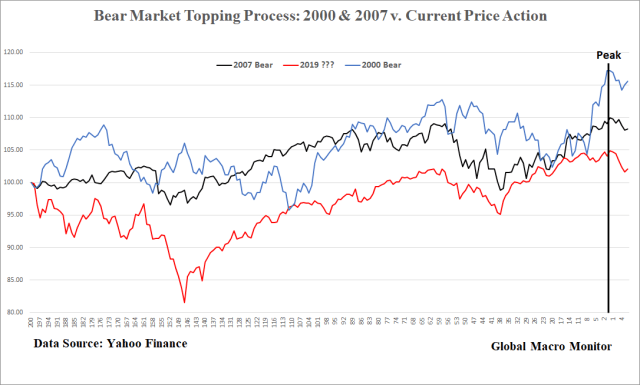

We believe a bear market began in January 2018 with the massive volatility spike and the S&P500 has been banging around with lots of volatility making three marginal new highs before peaking at the intraday high of 3027.98 and closing high of 3025.86. That is how bull markets top. It’s a process as you can see in the second chart.

We believe that the top is in for some time and we did call the very peak on the very day, by the way. We are also very proud of the fact we didn’t raise our target of 3025 when it was hit on July 26th. We try not to allow the price action to drive our narrative nor do we retrofit the fundamentals to market moves.

That is trap the central banks are caught up in. It is not surprising, however, as the global economy has morphed into one big asset market over the years.

Bretton Woods Order Collapsing

The post-Bretton Woods order is collapsing, especially the economic relationship between China and the United States, which has been a big driver of global growth, corporate profits, and margins for the past 20 years.

The markets are holding on to the belief that one tweet can return us to the good old days. Good luck with that one.

The politics in both countries are just not that easy. Sure, the market is gullible and shorts could get slaughtered in the short-term by a tweet from President Trump — a self-proclaimed economic nationalist, by the way, which we believe the market truly hasn’t internalized or fully understands — but come on, man, this is getting old. The trade war feels like it has now crossed the Rubicon.

If Hong Kong blows, forget about it.

Key Levels

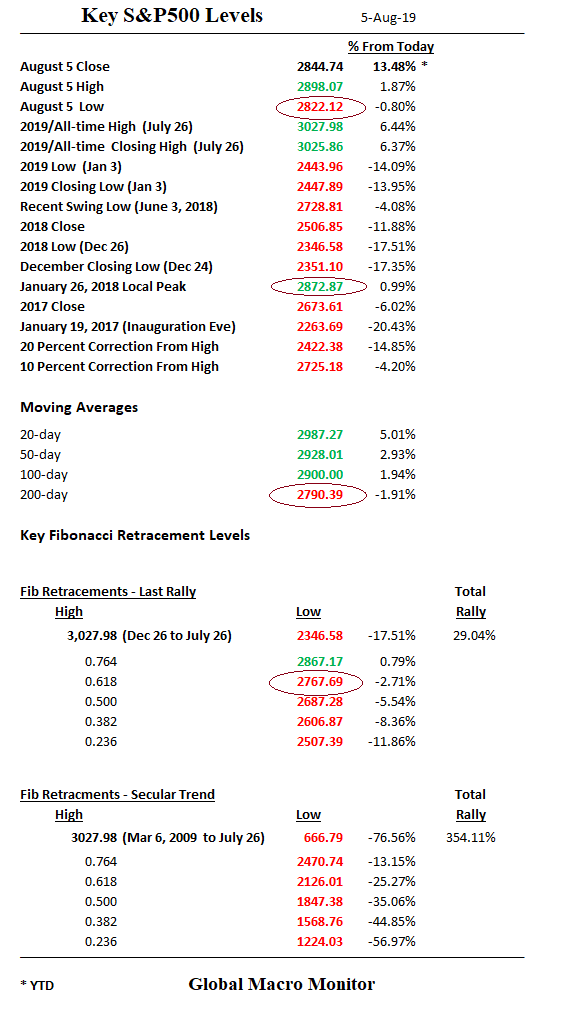

The levels to watch now to the downside are today’s low at 2822.12; the 200-day moving average at 2790.39, and the key .618 Fibo at 2767.69. The market has sold hard over the past week and a bounce may be in store quite possibly at those levels. In fact, in overnight trading that is exactly the level futures did find a bottom at 2775.75 after the Treasury labeled China a currency manipulator and then bounced big when the PBOC set the RMB official rate stronger than expected.

Then watch 2728.21, the June low, which is must hold.

To the upside, the first Fibo at 2867.17 and the 100-day at 2900.80. We will sell any strength and head for safe harbors or get shorter.

Be careful out there, folks.

It feels like the rivets are really starting to pop on the global international order as we have been warning over and over and over. The markets smell it.

If China moves on Hong Kong, things can really go sideways quickly and in an unpredictable linear fashion.

Haas fully understands it and nails it in his tweet this morning.

Here we go again. The Summer Friday afternoon ramp.

We posted how the S&P tends to ramp into the close in our post on Monday (see below).

No different today. The S&P had traded in a 34.44 point range high-to-low and has been ramping this afternoon. It is now, with about 15 minutes left in the cash session, 30 points off the lows, or 88 percent at the top of the range.

Please show this to the proponents of efficient markets.

In our July 26th post, Enter The Selling Zone, which we suspected it was time to start selling and shorting and, by the way, came on the same day of the intraday and closing highs in the S&P, we stated,

We expect the summer Friday afternoon ramp into the close, which will be an opportunity to start letting some go or setting some up. It’s hard to sell strength but much more enjoyable than selling into weakness and into a big hole. – GMM, July 26th

Summer Friday Ramp Jobs

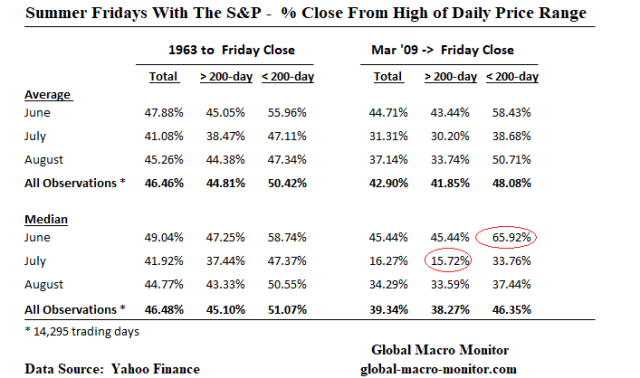

Is there anything to our suspicions of the summer Friday ramp job into the close? Absolutely, especially during the month of July.

The data below show there are certainly differences from the mean and median daily closes from the high on summer Fridays. Someday when we get our firewall up, our contributors will get more in-depth statistical analysis, which should include a t-test on these data.

Data

To clarify, the data illustrate the mean and median values of where the S&P closed from its high of the day for all Fridays in June, July, and August, broken down by: 1) total observations; 2) above the 200-day moving average; 3) below the 200-day, and 4) broken out since the bull market began in March 2009. We calculated the day range from the low to high price and what percentage was the close of the day off of the high given the range.

For example, in July since the current bull market began, the median percent close from the day high when the S&P was above its 200-day moving average was 15.72 percent. That is the S&P tends to close at or near its high of the day on Friday’s in July since the current bull market began when the index is above its 200-day.

The data distribution for July is also heavily skewed, which reflects long Greek fat tails to the left. Also interesting is the June data when the S&P is below its 200-day, which we suspect reflects skittishness of traders to go home long over the weekend during illiquid summer months.

We also added data for all observations for every trading day since October 1962.

Upshot

Yes, comrades, summer Friday afternoon ramp jobs do exist, especially since the bull market began and when the S&P is above its 200-day. Efficient markets professors will argue this is not possible but take it from a practitioner, who has been trading all kinds of markets for several years: Bulls and traders love to paint the tape on illiquid Friday afternoons during the summer months.

The data show the easy money is made in July.

Stay tuned for similar analysis to come during the week.

Just connecting the dots. It doesn’t take a genius, folks.

Stop politicizing mass shooters you say? My arse we will.

Here are some countries who politicize against mass shootings and one that doesn’t with the caveat if the data are correct. It passes the smell test.

https://twitter.com/keithedwards/status/1157740352838742016?s=21

This is a must view, folks. If you don’t have Netflix, grab some friends and subscribe for one month so you can watch this. Stunning.

Everything you wanted to know about Cambridge Analytica but were afraid to ask.

See full story here.

We have been all over this one since early spring. Never works out exactly as expected but content to be in the same zip code.