I bought of very nice pair of denim jeans the other night for $9.00. When I was in grad school just a few decades ago, I paid $26.00 for a pair of lesser quality. That is about $62.00 in 2018 dollars.

Do the math.

I now have a gain of $53.00, which is an increase in real income or purchasing power that can be spent at the local diner, farmer’s market, theatre, or get that needed car tune-up from my local mechanic. That $53.00 increase in real income creates real jobs. It’s not theoretical mumbo-jumbo. Economists call this the gains from trade.

However, the company and employees who worked in the domestic denim factory and lost their market to free trade are hurt — the losses from free trade.

Political Problems

Because politicians have mostly ignored those who have lost out from globalization, offering up only anti-trade rhetoric, the political shit is now hitting the fan. Trade and globalization is now a four-letter word in the world of political campaigns. It’s hard to reason with people when emotions are running so high. Many suffer from Einstellung, a predisposition or state of mind that prevents them from finding solutions to new problems, especially with heated political rhetoric.

If we erect trade barriers to try and bring denim factories back to the U.S. in the name of creating higher paying jobs, for example, causing the price of denim jeans to go back to, say, $62.00 per pair, nobody will buy jeans. There will be no market, no new factories, no new jobs created, and those who gained from the income effect of free-trade — the local waitress, the town theatre and actors, and the auto mechanic — will lose their jobs.

That is how it works, folks. How the income effect, a net positive, of trade expands domestic growth and net jobs. Yes, in some sense, we are talking corner solutions, that is taking our example to the extreme, but we do so to convey the much needed big picture.

Still, we haven’t even touched on the expansion of foreign markets for U.S. exporters, which creates even more growth and jobs.

Trade Adjustment Assistance

Where we have failed as a nation and leader of the free world is to take care of the workers who have been hurt by trade. We have written extensively on this. See here.

What’s unfair, is to offer false hopes to those struggling in the rust belt by announcing a few cosmetic tweaks to the trade deals and then declaring victory.

…The rust belt needs a new Marshall Plan — more education, and more opportunities provided by intense vocational retraining programs, coupled with income support for older workers who have little chance of recapturing their income and regaining new employment.

Also, begin new, or bolster existing programs to deal with the opioid crisis ripping through the communities, which have been left behind by the global economy. All these programs, in the form of beefed Trade Adjustment Assistance, should be financed by taxes earmarked from the gains from trade as outlined above. – GMM, Oct 1, 2018

The President

We have given up on President Trump regarding his ability to understand the positive economic effects of international trade, both the gains and losses and how to effectively deal with the political backlash, instead of inflaming it.

Tariff Man. What a joke.

Does he even understand the basic tenets of trade? Latest reports suggest he just might. The ultimate hypocrisy.

A Marshall Plan For the Rust Belt

President Trump’s cosmetic tweaks to NAFTA 2.0 and the so-called U.S.-Korea Free Trade Agreement (KORUS) deal will do more harm than good to the global economy in the long-term. They are nothing more than political Potemkin trade deals, which, in reality, have been a relief to free-traders, at least, in the short-term but will not move the needle in helping workers in the rust belt.

No proliferation of factories, no significant increase in employment. Only disappointment, disillusion, and even more significant political blowback in the long-term.

What should be done in, in our opinion, is to take a portion — call it a tax or fee, if that will make Grover happy — of that $53.00 savings from the imported pair of jeans we mentioned above to fund a Marshall Plan for the rust belt and also help the hollowed out middle class on a means-tested basis.

The literature on trade theory is full of ideas on trade adjustment assistance.

I would still buy those jeans even if I had to pay an extra $6.00, especially if I knew the fee was going to retrain my fellow Americans in the rust belt, fund new jobs projects, or to help subsidize the income of the senior workers, who will never find work again. We can argue whether the government or the private sector should do it, but let’s Just Do It.

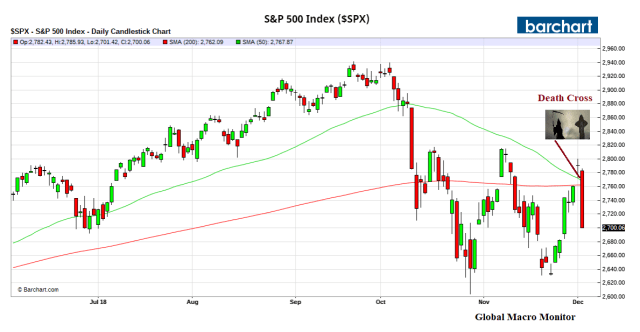

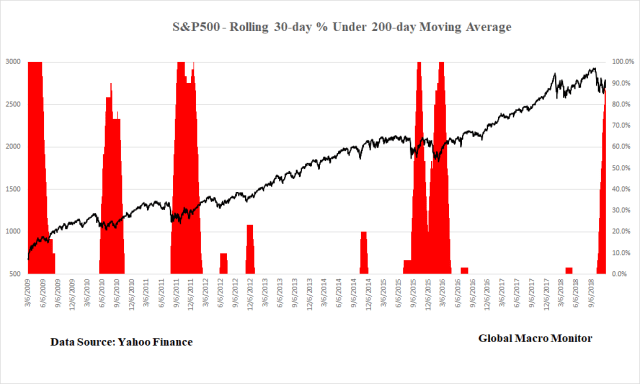

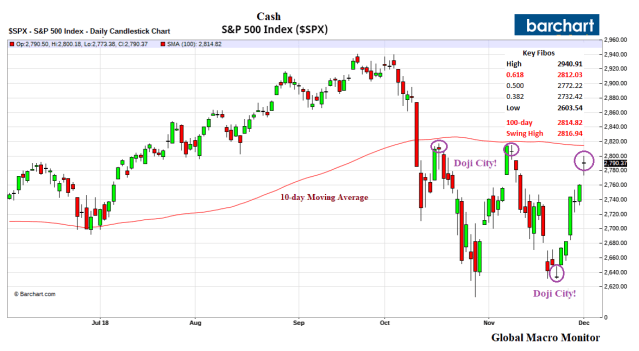

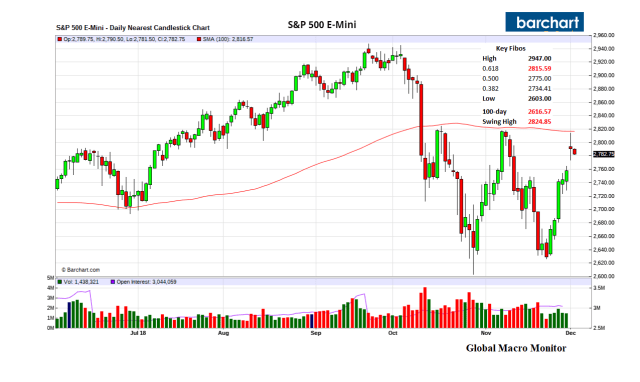

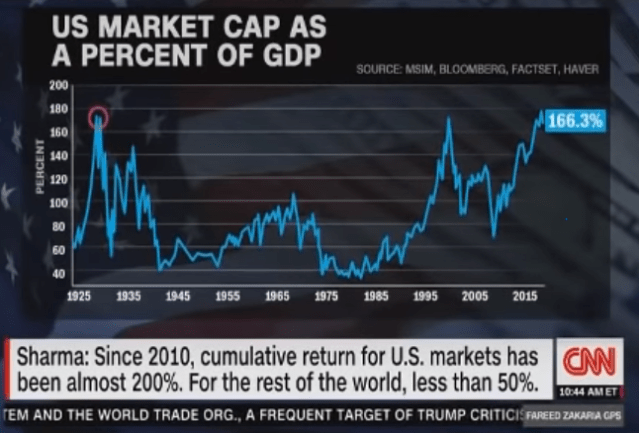

It’s time for bold leadership folks. Mr. Market is worried the post-War order is crumbling and crumbling fast it is.

We are all stumbling in the dark to an uncertain future. Markets don’t like uncertainty.

Certainly, China needs to reform its trade policy and we should do that by strengthening the international institutions, such as the WTO. The U.S. and its allies should press for a “better deal” — more market access, intellectual property rights, etc. — but another, half-baked, politically driven Potemkin unilateral trade deal with China may only goose markets in the short-term. It will be ephemeral probably lasting about 5 minutes in today’s markets.

Markets want a long-term fix and looking for leadership to expand the global economy and commerce while fixing the fracturing political global consensus for a more liberal trading order.

The alternative is very dark and Mr. Market is starting to sense it.