Updated October 30 @ 1:15 a.m. – Data correction

Summary

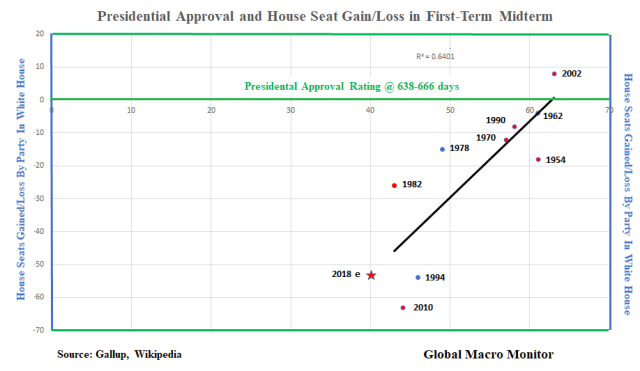

- President Trump’s Gallup approval rating has collapsed over the past week

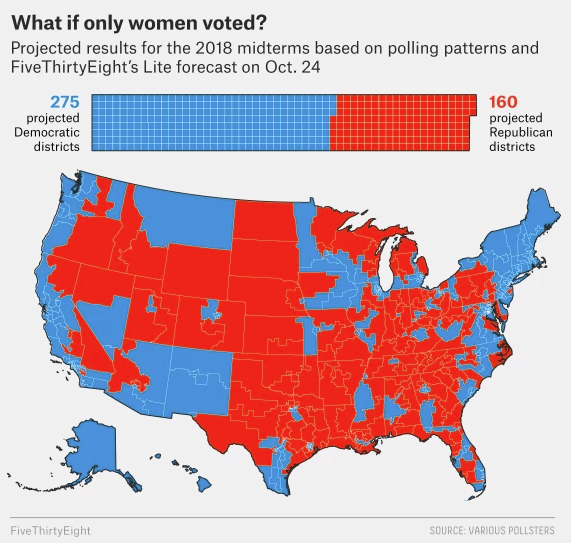

- We have updated our simple single factor model, which now projects the Republicans will lose 53 House seats next Tuesday

- We are taking the over

- Oil prices have fallen, though not yet reflected in gas prices, which may help the president on the margin

We have updated our single factor Congressional midterm model based on the latest Gallup polling data of the president’s approval rating, which is now plunging, falling 4 points in the past week. Bad time for a swoon.

President Donald Trump’s job approval rating plunged 4 percentage points last week amid a wave of violence, the latest troubling signal for Republican chances in upcoming midterm elections.

Forty percent of Americans approved of Trump’s performance as commander in chief, according to Gallup polling during the week ending Oct. 28. That was down from 44 percent the prior week, an unusually steep decline for the poll, which is based on a survey of 1,500 U.S. adults conducted Monday through Sunday each week. – Bloomberg

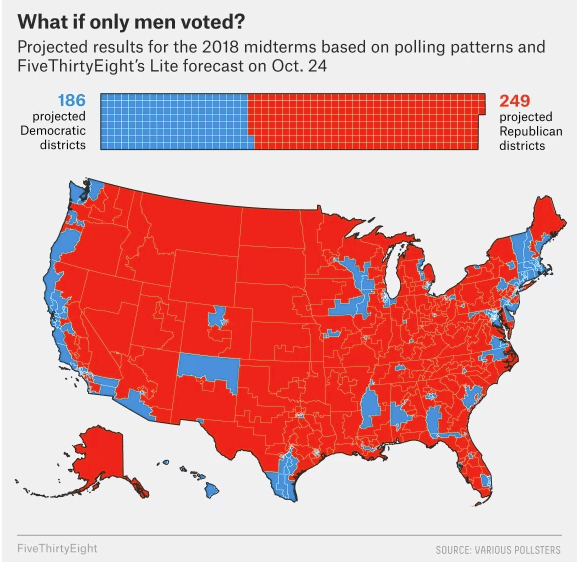

President Trump enters the week before the midterm election with the lowest approval rating of any full first-term president in modern day polling — 4 points below President Obama before losing 63 House seats in 2010, and 6 points lower than President Clinton before losing 54 House seats in 1994.

The presidential approval model predicts the Republicans are set to lose 53 House seats next Tuesday. Ouch!

Of course, the midterm election will be determined more than just President Trump’s rating. Moreover, the single factor model is simplistic, though it does have a decent R-squared of .64, history may not be prologue, and the data points are a bit imprecise.

Nevertheless, we believe President Trump’s doubling down on the Caravan and “they are coming for us” narrative, and moving the military to the border is going to backfire politically. Though our perspective doesn’t infect the model, but we firmly believe it is the major factor in the collapse of President Trump’s approval rating.

Country Looking For Healing And A Leader To Unite

Here is what the traditionally conservative Dallas Morning News wrote, even before the tragic events of the past week, in endorsing of the young RFK-esque Beto O’Rourke over Ted Cruz to represent Texas in the Senate. It sums up the mood of the country, in our opinion.

In looking at the race for United States Senate in Texas, we recognize that this country stands on a precipice. Whether we fall off the edge depends on how we answer this question: Can we set policy differences aside, even for a moment, and agree to treat each other with the respect befitting a great nation, with acknowledgment of the humanity of each person?

We have been at divisive political moments before, and we know those often end when leaders emerge who find ways to get along personally even when they are engaged in grand, tectonic political debates. That is one of the underappreciated stories of the 1980s, when President Ronald Reagan and House Speaker Tip O’Neill worked together. Even when they fought it out on tough issues, they fostered an enduring friendship.

For this reason more than any other, we favor U.S. Rep. Beto O’Rourke for U.S. Senate. The pivotal issue before our country is public leadership, and here we believe O’Rourke’s tone aligns with what is required now. This inclusive and hopeful tone, along with O’Rourke’s approach of starting with shared principles and working toward solutions, offset any policy differences we have with him. Leadership is more than policy, and whether we are addressing the very real challenges before us now turns on our ability to find points of agreement. – Dallas Morning News

Oil Prices And The Midterm

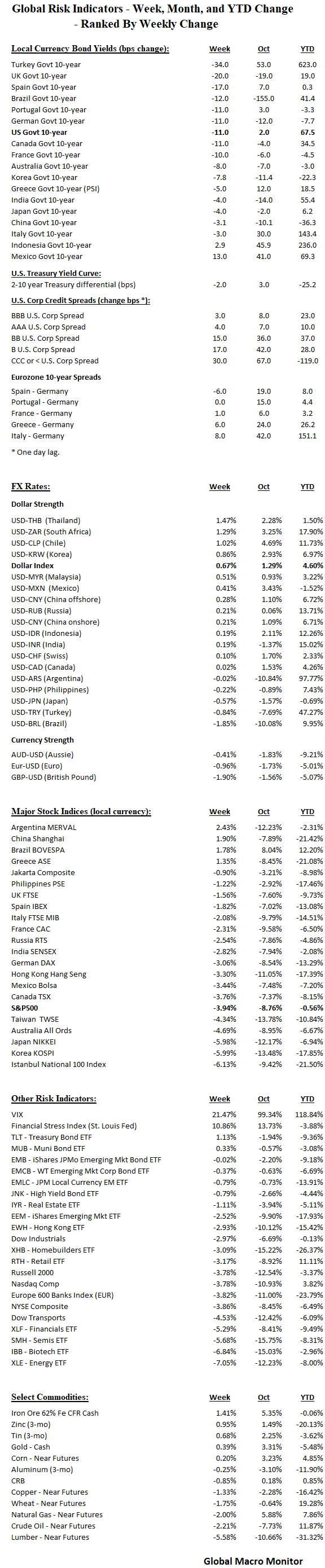

Oil prices have fallen since our last analysis, which may help the president on the margin. Though, anecdotally, we don’t see it showing up in a drop in the price of gasoline at the pump.

Stay tuned, folks. Prepare for Mr. Toad’s Wild Ride!