1012

Apple’s market cap hit 1012 dollars today.

Impressive but no pom-poms here at Global Macro Monitor. We would be more impressed if Apple’s main businesses were doing better and the company was more focused on electrical engineering rather than financial engineering.

Don’t get us long, I mean wrong, we were The Dallas Cowboy Cheerleaders for Apple’s stock pre-2015. Check the record.

Just the data, ma’am

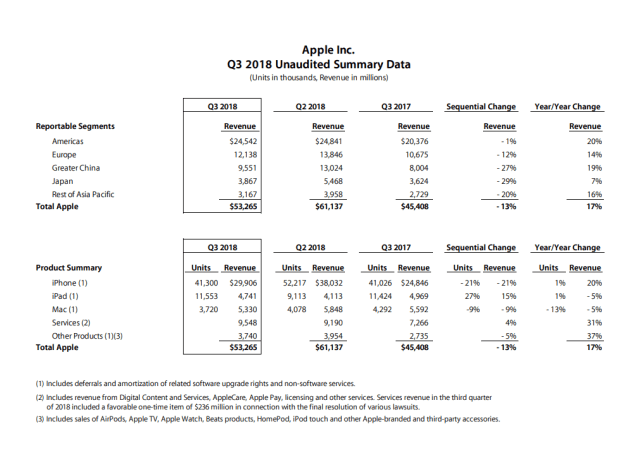

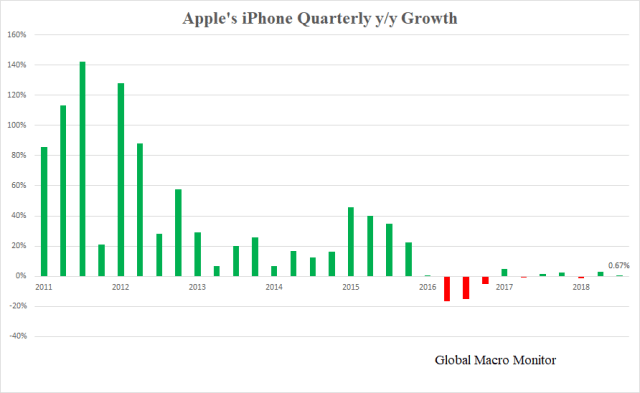

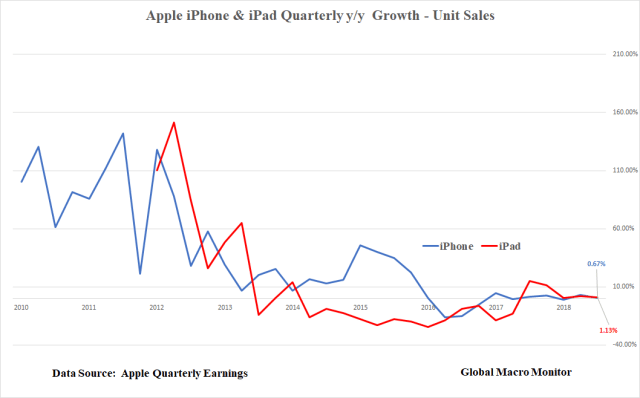

The table below illustrates that almost all of Apple’s revenue growth was driven by inflation, that is the price increase for iPhones. Unit sales growth for the company’s three major products – iPhone, iPad, and Mac – were either flatish year over year or negative. This has been the case now for several years.

If Apple were not able to significantly raise iPhone prices (mainly through the upgrade to the X) and only grow revenues by the device’s unit sales growth of 0.67 percent, Apple’s total revenues would have been about one third of what was posted, or 6.7 percent versus 17.3 percent.

One thousand dollar smart phones are not a sustainable proposition, in our opinion, folks. China, or somebody, somewhere, will, or already is producing a quality equivalent smart phone for $250.

Are iPhones Peacock Feathers?

Yes, yes, and yes, still not a Porsche. We get it.

Our sense, however, millennials, and the youngers, are not as into conspicuous consumption as the self-absorbed boomers are.

An iPhone is not peacock feathers, folks, at least we don’t think so.

Does owning an Apple iPhone really signal superior genes to the opposite sex?

Make sure to click on the peacock feathers link to understand what the hell we are talking about!

An Omen Of Coming Inflation?

Furthermore, Apple’s inflation driven earnings may be an omen of a larger inflation coming to the overall economy.

Of course, the iPhone X was a much better quality phone and will almost certainly be hedonically adjusted by the BLS so it won’t show up in the CPI.

Ridiculous. Real wages and purchasing power decline as consumers purchase higher priced items, regardless if the camera phone has a better resolution.

But, hey, if Apple can charge $1,000 for a phone why not ________ for any item. Fill in the blank for your company and seller or supplier of choice.

Great Products, But What Have You Done For Us Lately?

We love Apple products, have loved the stock in the past, and have a double digit number of Apple devices in our household.

We will like the stock much more when they are driven more by electrical engineering (product innovation) rather than financial engineering (stock buybacks).

The New Supply-Side Economics of Asset Markets

Finally, the limiting supply (shifting supply curve left) induced surge in Apple price shares due to buybacks is endemic of today’s asset markets, in general. Most notable in risk-free bonds — restricting supply through QE, which distorts the risk-free interest rate, of which all assets are priced; though this is slowly changing; housing with all cash investors and private equity — now the largest holder of single family homes, and gouging renters; and equities through the massive buyback programs.

Moreover, there is feedback loop buying bias induced by the move to passive investing.

The “Steel Bubble”

These are a few of the major factors why these overvalued asset markets are so much harder to pop than the asset bubbles of Christmas past. See our posts on the “steel bubble.”

Apple, The Stock

Toppy. Selling the hype and waiting for the “new, new thang.” If they build it, I will come.

Overall market action bullish. No sellers, until they sell. Today’s action is a signal that no-liquidity August has arrived. Go to the beach!

Stay tuned.