Whoa!

Dow down 666 to close a week in which we saw a rare Super Blue Blood Moon. Sure to bring out the false “profits” [sic], now watching for an earthquake and great fire to turn the sun black. Start prepping.

Not to worry, comrades, the S&P500 bottomed on March 6, 2009 at, you guessed it, 666.

Tom Brady may need a few more quarters to rally this market to victory, however.

.

Hat Tip: @charliebilello

Hat Tip: @charliebilello

We began the week with our Watch This Space post:

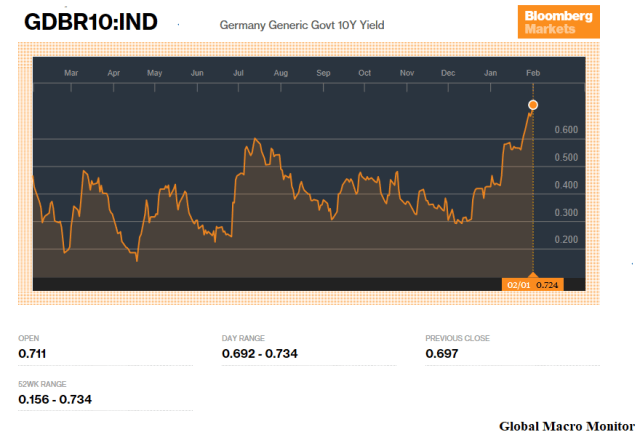

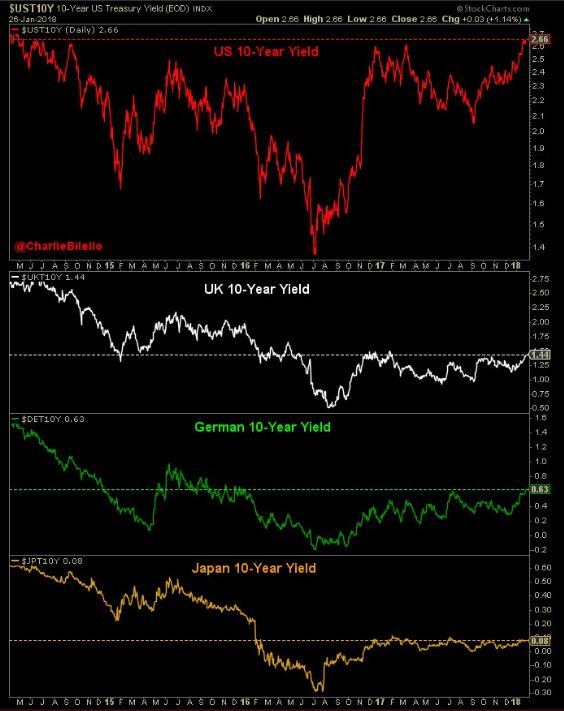

Because the eurozone is where the big bond bubble lives.

Though the euro periphery is now in Convergence 2.0 mode on hopes of eMac’s vision of a more integrated ‘zone, the German 10-year is at a critical level, and yields only 63 basis points in an economy that is probably growing close to 5 percent on a nominal annual basis. It reflects a stunningly loose monetary policy and a central bank way behind the curve.

The repressed yield is technical as the German government’s new bond issuance is virtually nil as it runs a budget surplus and the dearth of bunds is exasperated by the ECB’s quantitative easing. We have referenced this as a major factor of the “steel bubble” in asset prices, the bursting of which is very stubborn.

A spike in bund yields could put further pressure on U.S. bond yields and may be the trigger for the long-awaited and ever fleeting equity market correction. Maybe.

Stay tuned.

Full stop.

Bund yields have broke higher this week, up 10 basis points.

Greenspan Speaks

Former Fed Chairman, Alan Greenspan, weighed in yesterday talking bubbles.

Let me put it to you this way. I think there are two bubbles. We have a stock market bubble, and we have a bond market bubble. I think at the end of the day the bond market bubble will be the critical issue……we are working our way to a major increase in long-term interest rates. – Alan Greenspan

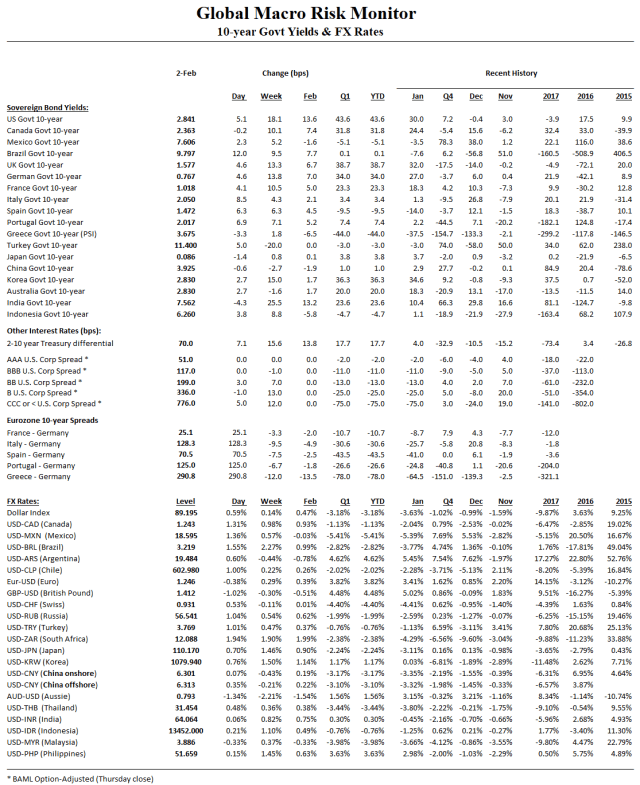

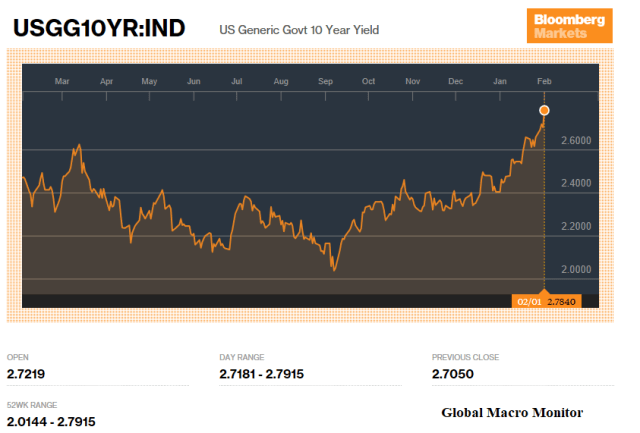

Global Bond Yields Spiking In New Year

Bond markets of the advanced economies are having a rough start to the year as the global economy gathers steam and inflation expectations pick up.

More importantly, the markets are beginning to discount the supply distorting effects of quantitative easing coming to an end.

The U.S. budget deficit is set to accelerate, which will increase supply, coupled with the confluence of potential negative demand factors: 1) the Fed bid is gone and are now running off their Treasury book; 2) Bund yields are finally moving higher, reducing potential portfolio substitution; and 3) the direction of the dollar is dubious, which may spook off foreign buyers. In addition, a new and untested Federal Reserve Chairman.

Moves Off Low Base

The table illustrates the carnage in 10-year local currency sovereign bonds.

The absolute basis point moves mask the pain as the increase in yields started from such a low base. Focus on the relative moves in percentage terms.

The German bund yield has moved up almost 70 percent since the beginning of the year, and the Japanese JGB yield has more than doubled.

The U.S. 10-year is up nearly 40 bps, though smaller in percentage terms, but still substantial relative to the annual moves over the past three calendar years: 2015 – +9.9 bps; 2016 – +17.5 bps; and 2017 – -3.9 bps.

No sugar coating, folks. It’s been fast and furious.

.

We believe the bond market reaction to tomorrow’s employment numbers will be a huge tell. Bonds seem to be oversold and the fast money may be a bit offside going into the number (see the Quandl CFTC chart below). If a repricing is taking place and a bubble is indeed bursting, however, no need to be a hero by stepping in to catch a falling knife.

The New Narrative

We now hear that bond yields are just in the process of moving back to normal in an global economy that has healed thyself. Don’t worry.

We are always worried! Will markets be internally consistent here and also normalize asset values with the interest rate move, which are currently at rare historic extremes?

Probably not overnight, we suspect.

The rise in rates have landed a body blow to equity markets over the past few days, however, just like a Joe Frazier left hook. Stumbling, temporary down, but no knockout punch.

Warning Signal

Rising interest rates coupled with a falling currency, the ugly cocktail currently be mixed in the U.S., is never a good signal and always a red flag, in our book. Ask any veteran of emerging markets.

Moreover, ignore the large increase in public (and private) debt in many of the advanced economies over the past ten years at your peril. Rising interest rates will feedback into budget deficits, which will feedback into bond markets. Not exactly the loops we prefer.

.

Even global macro jockeys must monitor the world’s largest company.

Amazing that an $850 billion market cap company can still grow y/y revenues at 13 percent. Just for some scale perspective, Apple’s quarterly revenues exceed the GDP of almost 70 percent of world’s country GDPs. Hackneyed analysis, but stunning, nonetheless.

Earnings

Apple comes in a little light on iPhone sales, unit sales down 1 percent (ditto for Macs), but revenues made up by higher prices. It looks like the price point on the new iPhone is becoming prohibitively expensive. Can’t raise prices to the sky.

The iPhone X starts at $999 for a 64GB model, but survey data indicated that most early adopters willing to pay big bucks for the latest iPhone were springing for the $1,149 model that has four times the storage. As such, analysts predict that the average price of phones sold during the quarter rose to a record of $752, up more than $50 from a year ago, according to FactSet. – Market Watch

Services continue robust growth, up 18 percent, and comes in at 10 percent of total revenues versus 16 percent last quarter. The iPhone was 70 percent of revenues for the quarter. We continue to monitor service revenues to see if the company can transform itself from hardware to a software and services company.

China came in about 20 percent of revenues versus 40 percent for the Americas.

Net cash now around $180 billion ($284 b less $103 b debt).

Stock Price

The stock is whipping around in AH, falling a couple of bucks after release and now up $6 as of 6:00 pm eastern. The stock is down 3 percent from its January 18th all-time high versus about a 1 percent rise in the S&P500.

No clue where the stock price is headed.

“Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.” ― George Soros

(QOTD = Quote of the Day)

We suspect the duration and resolution of the twin bubbles will be a bit more complicated than the dot.com and credit/housing bubble — i.e., a swift waterfall collapse followed by a sharp rebound driven by the Federal Reserve to even higher ground. The nature of the leverage and type of “money” driving assets are “different this time.”

Furthermore, if you listen carefully to Greenspan and read between the lines, it sounds like the rise of inflation, possibly via a collapsing dollar, will burst the bubbles. That could hamstring monetary policy and force the U.S., now much more vulnerable to higher interest rates due to our a relatively larger and growing debt stock, into an emerging market-like stabilization program to arrest the market turmoil and assure our foreign creditors. That is tight monetary and fiscal policy.

The potential downside of withdrawing, or being to be perceived to, from the global community when at the mercy of global creditors. Isn’t it starting to feel like China is about three to five moves closer to checkmate?

Let me put it to you this way. I think there are two bubbles. We have a stock market bubble, and we have a bond market bubble. I think at the end of the day the bond market bubble will be the critical issue……we are working our way to a major increase in long-term interest rates. – Alan Greenspan, January 31, Bloomberg TV

.

Click here for Greenspan’s full interview. His comments on twin bubbles begin at 6:14 minutes in. We recommend listening to the entire interview.

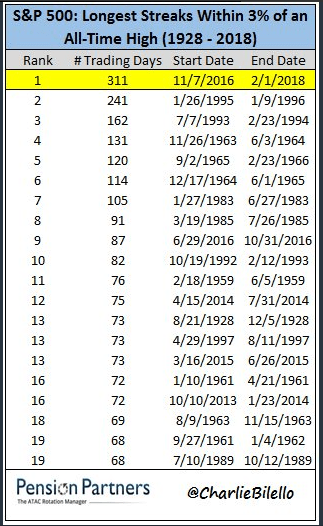

Wow!

Back-to-back more than 1/2 percent down days for the S&P500 ending a streak going way back to January 2016.

Feels like we just landed on Mars or in the Bronx after Joe DiMaggio’s 56-game hitting streak was snapped, no?

.

We often post political analysis but rarely stray into the crocodile-infested swamp of partisan politics. It is our duty to our readers from across a broad political spectrum to stay true to our mission to provide, mostly, positive economic, financial, and political analysis.

FBI Caught In The Political Cross-Fire

After today, however, we do have to register our disgust with how the good men and women of the Federal Bureau of Investigation (FBI) have been and are currently being used as political pawns by both political parties.

We have been around the block a few times and have had the privilege of knowing, personally, federal agents and members of the secret service, all charged with protecting the lives of Americans and various government leaders from President Jimmy Carter to former Secretary of State Hillary Clinton, among others.

All had their political perspectives and views and personal feelings on the leaders they protected. By no means were their politics uniform and some did not even care for those they were charged to defend. Yet we have no doubt each would have taken a bullet for those they had the responsibility to protect.

They were consummate professionals with the same constitutional right to their own opinions, political views and perspectives, and religion, for that matter. Thank goodness it was the good old days before the new tech NSA could crib our conservations or text messages.

2016 Presidential Election

During the 2016 presidential campaign, we felt for FBI Director James Comey, who was in an impossible situation. We remember reading he had no choice to break precedent and speak up about the Democratic candidate’s email problem as he had a revolt on his hands at the FBI, which, according to the reporting at the time, consisted mostly of conservatives,

After Hillary lost, Bill Clinton summed up what many Democrats and even some Republicans still believe: “James Comey cost her the election.”

… why someone who prides himself on being apolitical became embroiled in a great political scandal

… why, long before October, did he set himself on a course where he began violating strongly held Justice Department and F.B.I. norms that prohibit speaking publicly about investigations, particularly of people you don’t charge and particularly when doing so might interfere with an election?

…F.B.I. agents still tend to be white males. In a way, this situation is systemic: to be promoted, you have to be willing to relocate, which can be difficult for women with children. A current agent also says that there’s a strong conservative bent: if a TV is on in an F.B.I. building, it’s likely to be Fox News. – Vanity Fair, February 2017

Republicans Turn

Now it’s the Republicans turn.

Today was a dark day for American democracy, in our opinion. Not only was the FBI deputy director forced to resign early, but the House (not so) Intelligence Committee also voted along party lines to release classified material with the appearance of the sole purpose to distract and obfuscate the ongoing investigation of Special Counsel Robert Mueller of Russian interference in the 2016 presidential election.

The majority party also announced they have opened an investigation into the Department of Justice and the FBI. Smells like shoddy and shady politics to us, maybe even crossing the Rubicon in an attempt to obstruct justice. No doubt the special counsel will be looking into it.

Trump Campaign Under FBI Investigation Before Election

One fact that looms large, at least to us, and seems to undercut the Republican suspicions of biasness at the Department of Justice and FBI is that the Trump campaign was already under an FBI investigation before election day. In fact, it began way back in July 2016.

If the American voting public had been aware of the investigation and the seriousness of the allegations — potential campaign collusion with the Russians — it would have surely swung at least the 77K votes in the three key swing states that put Trump over the top and, instead, thrown the election to Hillary Clinton.

By commenting publicly on the Clinton investigation and leaving the public in the dark on the Trump FBI investigation, if anything, in hindsight the FBI appears to have been biased toward the Trump campaign. Are we missing something?

Consequences Of Nasty Politics

The unintended consequences of today’s ugly politics in the U.S. could torpedo the global bull market in stocks.

What appears to be an attack on the rule of law in the United States could, if not checked, quicken an already plummeting perception of American leadership throughout the world and may give rise to domestic political instability. No wonder the dollar is tanking when the fundamentals dictate it should be soaring.

Fear The American Street

If you have been reading us over the past year, we are very worried about the tranquility of the “American Street”, especially given the widening wealth gap. A constitutional crisis, which may very well result from today’s events, could lead to a major political rupture in the U.S. body politic. Not good for capital flows.

The rally on the Street seems to thus far pacified the “American Street” for now, however, turning new investors and Bitcoin moms into the new trading geniuses, as they whip and drive their crypto and cannabis stocks.

Let’s Not Lose Our Souls

All we are saying is give peace Mueller and the FBI a chance. Let the chips fall where they may and let justice be done.

Finally, let’s not lose our souls in this bull market by looking the other way and letting our most trusted democratic institution, the rule of law, which, has probably been the most significant factor of the world’s secular bullishness on America, fall by the wayside.

And what do you benefit if you gain the whole world but lose your own soul? – Jesus of Nazareth

By the way, this just in:

Washington (CNN) The Trump administration has declined to impose sanctions against companies and foreign countries doing business with blacklisted Russian defense and intelligence entities.

The administration was required by law to name the companies and individuals Monday, and possibly sanction them under a 2016 law meant to punish Russia for its interference in the 2016 US election, as well as its human rights violations, annexation of Crimea and ongoing military operations in eastern Ukraine. – CNN

If Deputy Attorney General Rod J. Rosenstein is forced to resign? Tilt, game over.

Buckle up, folks.

Because the eurozone is where the big bond bubble lives.

Though the euro periphery is now in Convergence 2.0 mode on hopes of eMac’s vision of a more integrated ‘zone, the German 10-year is at a critical level, and yields only 63 basis points in an economy that is probably growing close to 5 percent on a nominal annual basis. It reflects a stunningly loose monetary policy and a central bank way behind the curve.

The repressed yield is technical as the German government’s new bond issuance is virtually nil as it runs a budget surplus and the dearth of bunds is exasperated by the ECB’s quantitative easing. We have referenced this as a major factor of the “steel bubble” in asset prices, the bursting of which is very stubborn.

A spike in bund yields could put further pressure on U.S. bond yields and may be the trigger for the long-awaited and ever fleeting equity market correction. Maybe.

Stay tuned.

Summary

The wealth effect – boosting consumption out of what is perceived as permanent wealth -seems to be kicking in. Consumers are feeling flush with the humungo gains in stocks and housing over the past few years. It also appears consumers are not cashing in on their theoretical wealth but rather reducing savings and taking on debt to finance the increase in consumption. Or, it could be, those who do not own assets are reducing savings and taking on debt to finance their consumption.

David Rosenberg, Chief Economist & Strategist, Gluskin Sheff, dishes on the latest GDP release

We’ve seen this picture before. Wealth is not always so permanent and therein lies the new “boom-bust cycle” of the new millennium. “It’s the economy stock market, stupid.”

The global economy and stock markets are now in a positive feedback loop.

Fixed-income

– Global 10-year yields breaking higher across the G3 economies;

– U.S. 10-year at highest since April 2014;

– Germany highest since December 2015;

– Japan highest since July 2017;

– China down 10 bps after making a new multi-year high in past few weeks;

– Euro yields in Convergence 2.0 as the eMac Euro vision takes hold;

– Credit behaving bigly as the stock gains feedback into the bond markets.

.

Source: @charliebilello

Currencies

– Dollar flop continues after Secretary Mnuchin’s Davos faux pas.

– Traders sell the Trump walk back.

Stocks

– Ditto last week: global stocks keep ripping, especially emerging markets;

– Brazil, baby, on Não Lula! Country’s ETF now up 17 percent in dollars for the month.

Other Risk Indicators

Other Risk Indicators

– Biotech and retail having a gangbuster January;

– Euro banks confirming breakout;

– Russell 2000 lagging, even though up almost 5 percent for the month. Stunning;

– Bad week for Trannies. Watch this space.

Commodities

– Nattie with another yuuuge week on the nation’s cold snap. Look to fade;

— Crude up on massive net positioning by specs. Look to fade.

Source: Quandl