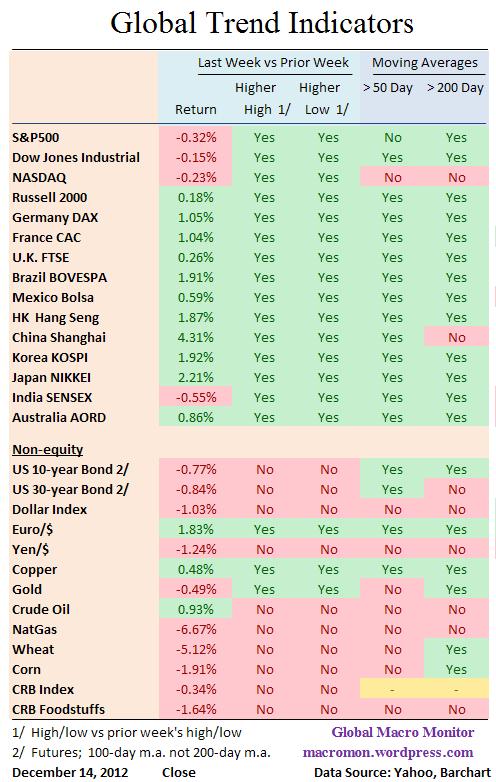

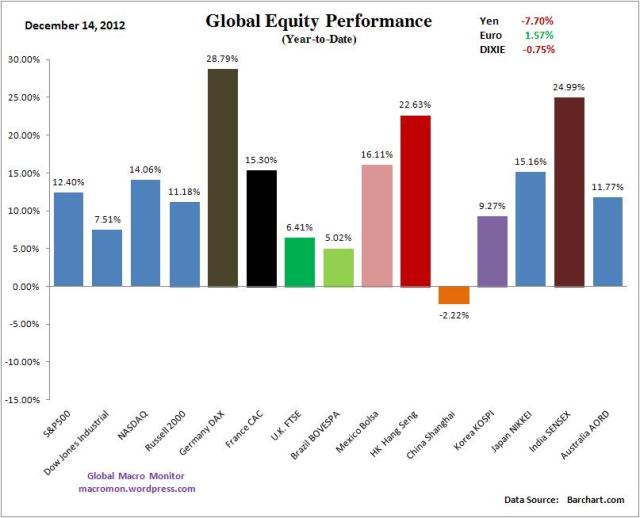

As stock markets have been breaking out all over the world, U.S. equities have lagged over fiscal cliff fears. We think the U.S. catches up as the ROW (rest of the world) takes a little breather.

Clearly the two big macro swans that have held markets back over the past few year have flown the coup, at least for now.

European sovereign spreads are at their lowest levels of the year. Greece restructured sovereign bonds are among the best performing in the world, with yields coming down 1560 bps (26.62% to 13.02%) since July. European equities are screaming.

China’s Shanghai Composite has bounced big as hard landing fears fade. Japan has elected Shinzo Abe who is promising huge fiscal and monetary stimulus. Let’s hope tensions over the rocks in East China Sea fade for awhile.

The U.S. housing market is coming back and financial stocks are leading the recent leg up.

Are the world’s problems fixed? Hardly. We have concerns and fears about many things, some, of which, have appeared in past posts. But markets want to go higher and our fears could be misplaced or just flat wrong.

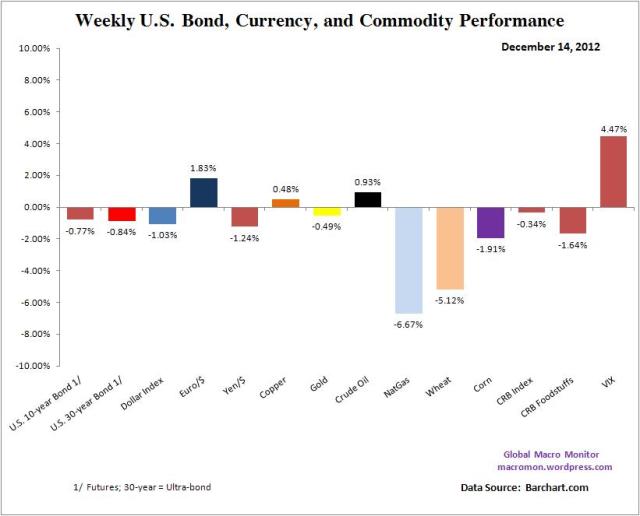

Global central banks have or have promised to go all in. Money flows are being channeled in equities. Commodities aren’t working, bonds are expensive, and cash yields a negative 2 percent in real terms.

Until the markets reach a tipping point that printing money is bad — and we think it is and markets will eventually come to the same conclusion — equities are going to rally.

Will they wake before the New Year and begin to contemplate the consequences of current global monetary policy? Doubt it.

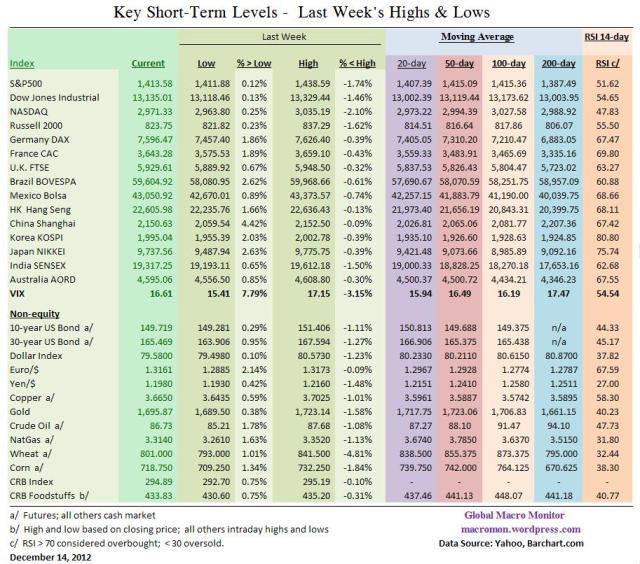

Look how the Nikkei is ripping higher (though it is due for pullback). Japan is going to be the big test for the new monetary theorists next year. Will the market really allow a massive stimulus and monetary easing with such a huge stock of public debt? Stay tuned.

Nevertheless, we welcome Santa Claus and plan on enjoying the sleigh ride into the New Year. Even Apple had a nice test of $500 and closed at its high of the day, generating a bullish outside day. The stock would have been in big trouble if closed down on the back of the good iPhone numbers out of China.

Meredith Whitney just announced meaningful upside in financials. Giddy up!

P.S. Don’t miss Mark Dow’s must read piece on the markets. The guy is one smart dude.

(click here if charts are not observable)

(click here if charts are not observable)