Today will be the shortest day in history as Earth’s rotation unexpectedly speeds up – Daily Mail

A Celestial Signal from the Macro Gods?

Today, we’re taking a position against the long end of the Treasury curve—not just for fundamentals or flows—but because July 9, 2025 is, quite literally, the shortest day in recorded history. According to scientists, Earth will complete its full rotation 1.4 milliseconds faster than usual, thanks to a curious combination of gravitational dynamics, axial tilt, and the Moon’s peculiar position high above the equator.

This isn’t a random celestial hiccup. Earth’s rotational speed has been picking up since 2020, causing days to grow imperceptibly shorter. While we’re not feeling jetlagged just yet, timekeepers are. The International Earth Rotation Service (IERS) may soon introduce the world’s first negative leap second—a rare, almost philosophical correction that could wreak havoc on GPS systems, power grids, and yes, algorithmic trading clocks.

Back to Bonds Markets love symmetry. They crave time-tested patterns. And yet here we are, staring at an auction calendar on a day when the very rhythm of the planet has gone rogue. On this backdrop, today’s U.S. Treasury auction feels like a cosmic stress test: will buyers (especially, foreign) show up? Or will the accelerated rotation be mirrored in higher yields and faster repricing?

The scientific backdrop offers poetic alignment:

The Moon’s orbital path is tugging Earth off its usual timing, accelerating spin by fractions of milliseconds.

Researchers like Duncan Agnew (Scripps) and Leonid Zotov (Moscow State) note that even the molten core is shifting momentum—something no one modeled into duration risk.

Earth’s shape is subtly changing due to melting glaciers, redistributing mass like a nervous bond trader shifting from 10s to bills.

So we say this: on the shortest day ever measured, duration is too long. The bet? A lackluster auction. Weak coverage. Yields pushing higher in defiance of the calendar’s brevity. We’re short the bond, long the metaphor.

After all, when the planet itself starts front-running time, maybe it’s trying to tell the markets something. Watch the clock—and the yield curve.

Happy trading, and enjoy your slightly shorter spin around the axis today.

Last week’s market tone reflected a convergence of stabilizing macro forces: easing geopolitical tensions, falling oil prices, and growing expectations of Federal Reserve rate cuts. But beneath these surface-level catalysts lies a far more powerful narrative: the AI revolution.

AI to Transform Everything: Artificial intelligence is rapidly emerging as the dominant force behind market optimism. Its potential to unlock exponential gains in productivity and profitability is beginning to be priced into equity valuations. We believe the market is still underestimating the speed and scale of this transformation.

What’s unfolding is not a cyclical rally but a structural revaluation. U.S. companies are leading a wave of accelerated AI adoption, deploying the technology faster than their global peers, including even China. Americans are embracing AI tools at a pace that eclipses the adoption curves of past digital innovations, including smartphones and the internet itself.

Of the world’s ten most widely used AI platforms, eight are American, led by ChatGPT. This leadership is not just symbolic, it’s strategic. As AI diffuses across sectors, from logistics and legal services to healthcare and finance, its compounding effects will reshape business models, labor markets, and economic output.

In our view, the market is only beginning to grasp the magnitude of this shift. The coming quarters may mark the inflection point where AI-driven gains move from speculative to foundational.

Short-term Uncertainty: Nevertheless, the short to medium-term economic outlook remains complex, as signals of slowing growth persist alongside stubbornly high inflation data. Meanwhile, international developments, from congestion at European ports to China’s tentative recovery, continue to shape capital flows and investor sentiment. The result is a market environment driven by optimism around the AI trade and policy easing but shadowed by structural and tariff-related uncertainties.

Geopolitical and Market Response: Global risk sentiment improved markedly following a de-escalation in tensions between Israel and Iran. The reduction in conflict risk was a key factor in oil’s 11% weekly decline, with Brent crude falling below $72 a barrel. This decline was welcomed by equity markets as a disinflationary tailwind, particularly for rate-sensitive and consumer-oriented sectors.

U.S. markets responded with renewed strength. The S&P 500 and Nasdaq both reached all-time highs, buoyed by strong performance in large-cap tech. However, the Dow Jones Industrial Average continues to lag, sitting roughly 3% below its previous peak. Market breadth, though improving, remains below its 2021 highs. Moreover, only three of the “Magnificent Seven” members — Nvidia, Microsoft, and Meta — are making new highs.

Foreign markets were mixed. Japanese equities gained on supportive monetary policy signals, while European indices underperformed as tariff uncertainty and port congestion weighed on investor confidence. According to reporting on European logistics, congestion has intensified due to changes in U.S. trade policy and low river flows, leading to longer shipping delays and rising costs, factors that could limit Europe’s export competitiveness in the near term.

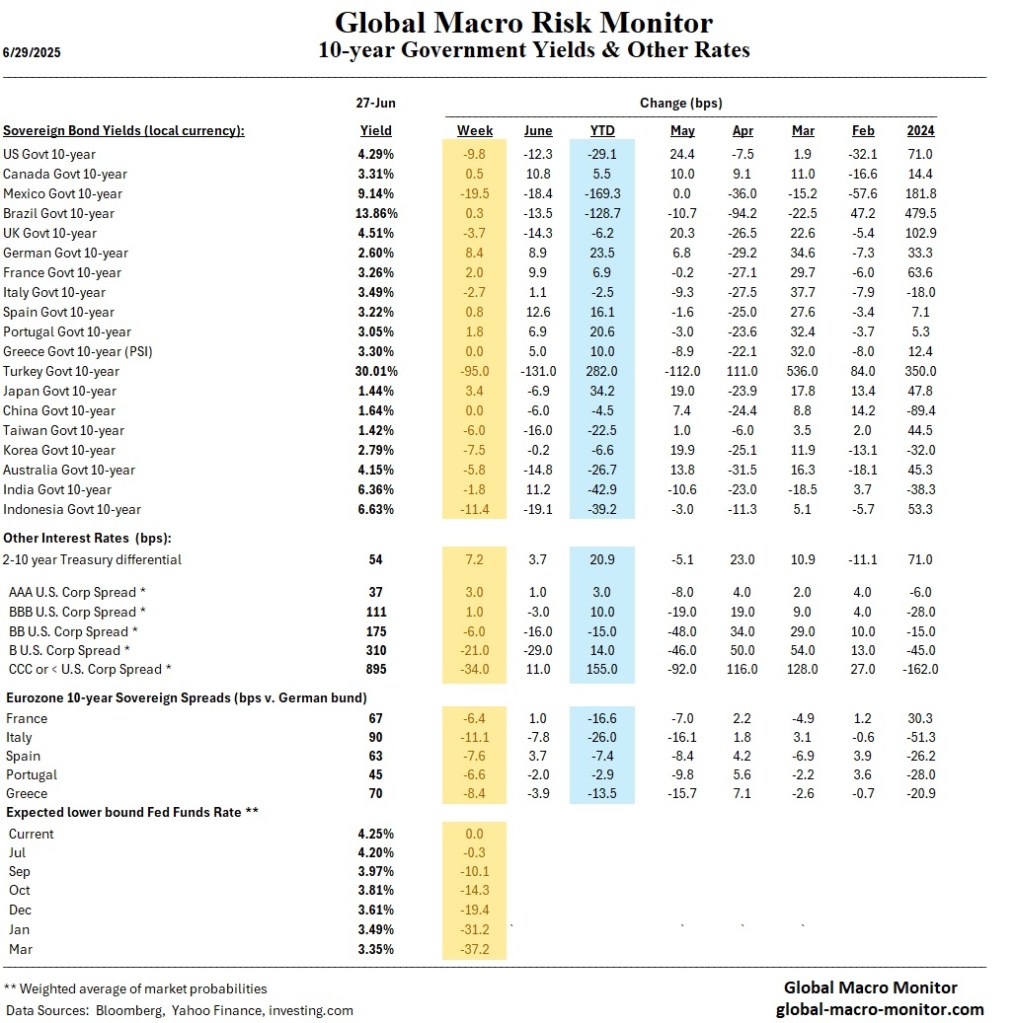

Monetary Policy and Inflation Outlook: Investors’ expectations for monetary easing accelerated this week. The Global Macro Monitor’s updated yield table (see tables below) reflected a market increasingly confident in a rate cut as early as September, with nearly four 25-basis-point cuts now priced in through March 2026. This dovish shift in expectations followed a batch of mixed economic data.

Core PCE, the Federal Reserve’s preferred inflation gauge, edged higher to 2.7% in May, but remained well below last year’s peaks. Consumer spending slowed slightly, while durable goods orders surged, reflecting resilience in business investment, especially in aerospace and defense. Treasury yields drifted lower across the curve, reinforcing the view that policy easing may come sooner and proceed more aggressively than previously expected.

T. Rowe Price noted that market participants are recalibrating their inflation expectations, especially as energy costs recede and supply chains stabilize. However, the firm also emphasized that volatility could return quickly if inflation surprises to the upside or labor market conditions deteriorate unexpectedly.

Trade and International Developments: Trade policy continues to play a pivotal role in shaping global sentiment. Canada’s withdrawal of its planned digital services tax is seen as a diplomatic concession to the U.S., aimed at preserving broader trade talks. Meanwhile, the situation in Europe remains strained. Port congestion, partly attributed to recent tariff disruptions, coupled with low river flow is creating bottlenecks in key supply routes. These issues may contribute to higher near-term inflation in the region and complicate the European Central Bank’s policy outlook.

In Asia, China’s economy showed signs of tentative recovery, supported by policy stimulus and a slight improvement in industrial activity. However, structural headwinds, ranging from weak property markets to soft external demand, limit the scope for a robust rebound.

Conclusion: Markets appear to be responding positively to declining energy prices, lower inflation expectations, and the prospect of accelerated monetary easing. Last week’s record-setting equity gains reflect investor confidence in smooth sailing ahead, bolstered by the view that the Fed is preparing to support growth. Yet, the combination of shifting market leadership, uneven economic data, and unresolved global trade issues warrants a balanced approach. While surface-level indicators remain strong, prudent risk management remains essential as markets navigate the intersection of macro optimism and underlying fragility.

Markets

U.S. equities advanced further, supported by rising confidence that the Federal Reserve may begin cutting rates later this year, reduced geopolitical tensions, which led to lower oil price.

S&P 500 neared the 6200 level, with technical momentum fueled by rate-sensitive sectors and declining Treasury yields.

Market breadth strengthened, with financials, industrials, and consumer discretionary stocks benefiting from the outlook for lower interest rates.

Expectations of Fed rate cuts lifted risk sentiment, though geopolitical and trade-related uncertainties still present headline risks.

U.S. Market Analysis

Rate cut anticipation drove investor positioning, with cyclical sectors and small/mid-caps outperforming defensives.

Earnings season reflected margin resilience, with forward guidance increasingly referencing expected relief from interest rate pressures.

Economic growth remained modest, but markets interpreted the policy shift as supportive of extending the expansion.

Bond yields fell across the curve, as Fed funds futures increasingly priced in multiple rate cuts by March 2026.

Credit spreads narrowed, especially on lower grade bonds, suggesting markets expect rate cuts to reduce refinancing pressure and support corporate balance sheets.

Global Market Analysis

Europe: Major equity benchmarks edged higher, tracking U.S. gains. Eurozone banks rallied on spillover expectations that ECB policy may follow Fed easing.

Germany’s equity market rebounded, supported by expectations of global monetary policy coordination favoring pro-growth stances.

Japan: Equities were mixed, with exporters gaining on yen weakness tied to diverging rate paths between the BoJ and the Fed.

BoJ maintained ultra-loose policy, while market participants assessed the global implications of potential U.S. easing.

China: Mainland equities saw modest gains; anticipation of U.S. rate cuts bolstered sentiment in emerging markets via currency and capital flow channels.

Cross-border fund flows shifted, as investors repositioned toward higher-beta international equities on improved global liquidity outlook.

Economics

U.S. Economic Overview

Labor market data showed stability, but rate cut expectations dominated market pricing and commentary.

Consumer demand held steady, with analysts anticipating a boost in credit-sensitive spending as rates fall.

The Fed’s communications signaled data dependency, but markets interpreted the tone as incrementally dovish.

Housing activity showed early signs of revival, aligned with the outlook for more favorable mortgage rates.

Core PCE inflation came in a bit higher than anticipated.

Global Economic Overview

Eurozone confidence improved slightly, aided by expectations of a more accommodative global rate environment.

BoE officials noted global rate developments, adding to speculation that synchronized easing could occur in H2.

Asia-Pacific equities gained, as investors positioned for capital inflows and better financing conditions amid easing bets.

Emerging market central banks signaled flexibility, citing potential Fed rate cuts as a catalyst for domestic easing cycles.

Week Ahead (June 30 – July 4)

Key U.S. Events:

Economic Data

Mon: ISM Manufacturing Index

Tue: Factory Orders

Wed: ADP Employment, Services PMI

Thu: Nonfarm Payrolls, Jobless Claims

Fri: Independence Day – Markets Closed

Earnings Highlights

Mon: Lennar, BlackBerry

Tue: Walgreens, Paychex

Wed: Levi Strauss, RPM International

Thu: Constellation Brands, Helen of Troy

Fri: None Scheduled

Key Global Events:

China Services PMI: Signals domestic demand resilience

Eurozone Retail Sales: Insight into household consumption

Japan Wage Data: Watchpoint for policy expectations

Global Central Bank Commentary: Key for rate cut signaling across regions

Alec Stapp’s chart isn’t just data—it’s a geopolitical pulse check. China is gobbling up global electricity capacity like it’s at an all-you-can-generate buffet, now pushing past 2,500 GW while the U.S. idles near 1,300 GW. That’s not just scale—it’s intent. China is building everything: solar fields that can be seen from orbit, wind farms taller than skyscrapers, and yes, still some coal, because energy security’s their religion.

Meanwhile, the U.S. is making respectable renewable gains, but in relative terms? It’s bringing a garden hose to a fire hydrant fight. China’s capacity additions are so massive they’ve turned the global clean energy transition into a national industrial strategy—and they’re winning. Fast.

Why does this matter? Because whoever electrifies fastest sets the rules. They control the tech, the supply chains, and the climate narrative. The chart is the plot twist: the West keeps talking net zero, but China’s building it—at scale, at speed, and with steel.

Ignore the chart and you’ll miss the future. This isn’t just about electricity—it’s about leverage, emissions, and economic dominance.

And right now, Beijing’s playing chess. Washington? Still arguing over the rulebook.

Anyone who has observed the last two decades of history in the Middle East would think hard about unleashing such an attack. You would want to think several steps ahead, and there is no evidence that the President has done that. His tweet and his public comments have given the impression that this is the end of war and the commencement of peace, but I suspect the Iranians think differently. – Karim Sadjadpour, Carnegie Endowment for International Peace

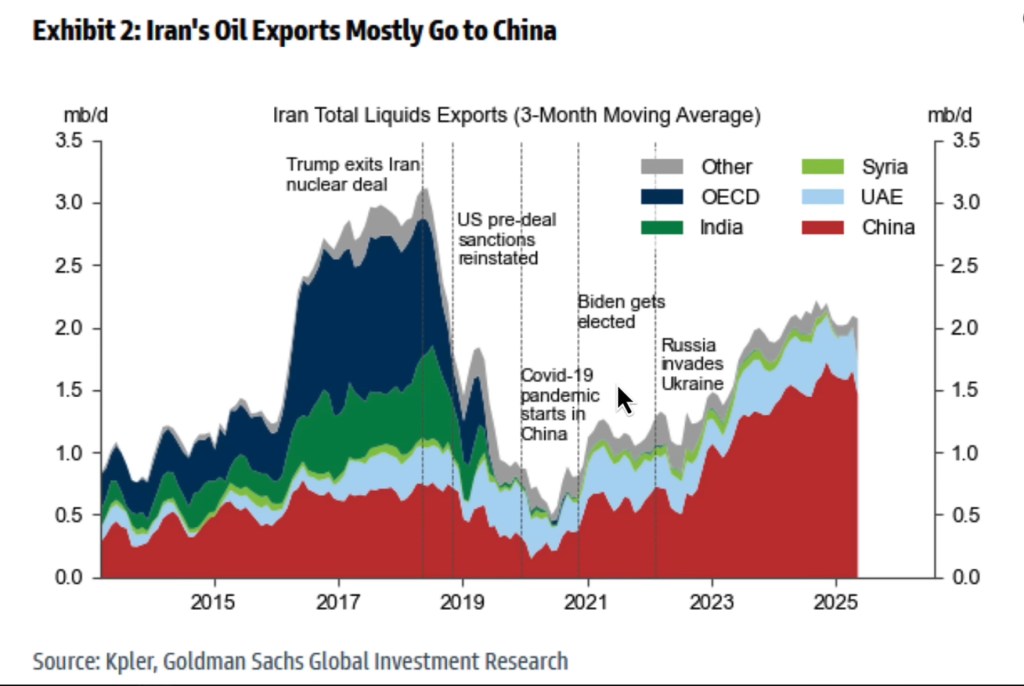

China’s role in the Iran‑Israel conflict isn’t born of strategic grandstanding, but of pragmatic energy calculus. Iran, tightly constrained by Western sanctions, has increasingly tethered its oil lifeline to Beijing, now accounting for approximately 85 percent of its oil exports. This near‑monopsony suits China: discounted crude in exchange for geopolitical reticence.

As reported by DW, Chinese foreign policy architect William Figueroa characterizes Beijing’s posture as disinterested—“no appetite to be involved”—not out of moral high ground, but capacity constraints. China lacks the regional military flexibility to act without risking broader escalation.

Still, China’s leverage through energy dependence is undeniable. Iran’s oil-for-infrastructure deals and shadowed military nods were strategically banked on Beijing’s commitment. Yet today, when conflict flares, China leans on diplomacy, not arms. It presses for de‑escalation, cautioning both Tehran and Jerusalem to respect sovereignty, even rarer is criticism of either side .

The energy dependency is a double‑edged sword for Iran. Beijing’s near‑total reliance on Iranian oil funds Tehran’s missile program and nuclear ambitions, aggravating Israel’s security paranoia. But it also binds China into a delicate balancing act: supporting Iran’s financial engine, while publicly prioritizing stability over alliance.

China’s strategic calculus is clear: high stakes in Middle Eastern energy flows, particularly through the Strait of Hormuz, where Iranian turbulence can rattle global oil markets. Yet China remains reluctant to step into the fray militarily. For Iran, this means continued economic lifelines without the military umbrella it may have hoped for .

China, the unwilling oil financier, perches on the periphery holding Tehran’s purse-strings but keeping its own hands clean. China offers Iran economic oxygen, but not military shelter, its cowed neutrality now the least risky of many bad options.

Recent intelligence from June 2025 confirms a sharp uptick in Iranian cyber activity directed at U.S. critical infrastructure, particularly the electrical grid. As Iran ramps up its offensive cyber operations, utilities and cybersecurity officials have observed increased phishing attempts, credential harvesting, and infrastructure scanning.

These intrusions remain largely within the IT domain, but their timing and intensity suggest Tehran is employing cyber operations as a deniable yet strategic tool of retaliation. Rather than risk overt military confrontation, Iran appears to be leveraging digital asymmetry to test U.S. resilience, probe for vulnerabilities, and signal resolve amidst intensifying geopolitical friction.

Ted Koppel’s Strategic Warning

Ted Koppel has long flagged the grid as a national vulnerability. In his 2017 Boston lecture, he stated: “The largest threat … is the electrical grid,” not terrorism in isolation. Lights Out pushes this further, warning that a focused cyber strike on one of the U.S.’s three power interconnections could trigger a collapse of much broader infrastructure. Koppel argues that, unlike nuclear threats, there exists no deterrent like mutual assured destruction in cyberspace, making the grid uniquely exposed.

Iranian cyber units—such as APT33 and OilRig—have demonstrated the ability to infiltrate utility IT systems through credential-spraying and phishing. While current operations remain focused on reconnaissance and IT infiltration, the shift in posture suggests a calibration phase: mapping defenses, identifying ICS/SCADA weaknesses, and building access. As conflict with Israel unfolds, the risk evolves from espionage to disruption.

The U.S. Grid’s Structural & Defensive Hardening

The U.S. grid is unusually resilient: decentralized across Eastern, Western, and Texas interconnections; regulated by over 3,200 utilities. Post-Colonial Pipeline and Texas freeze, the Department of Energy, NERC CIP standards, and regular exercises like GridEx have fortified both cyber and physical defenses. Moreover, improvements in detection, incident response, and public–private intelligence collaboration help counter emergent threats.

The Absence of Cyber “Mutually Assured Destruction”

Koppel draws on Cold War lessons; unlike nuclear arsenals, cyber platforms lack clear, visible retaliation mechanisms. The U.S. cannot credibly threaten proportional digital retaliation against Tehran. This imbalance of asymmetric risk may embolden Iran to deploy cyber tactics as a strategic lever, particularly if its kinetic options head south.

Implications & Strategic Tasks

Key Points:

Iranian cybersecurity activity is on the rise, closely tied to U.S.-Israel dynamics.

Koppel’s insights underscore the existential stakes: grid disruptions could cascade into systemic collapse.

The U.S. has improved defenses, but cyber escalation remains plausible absent stronger deterrence and attribution capabilities.

Implications:

Cyber-to-physical escalation may occur: IT breaches morphing into ICS attacks during flashpoints.

Investment in active defense, public attribution campaigns, and legal/policy frameworks for cyber deterrence is essential.

Timing is critical: If a major conflict with Iran erupts, let’s hope we have shored up our vulnerabilities, improved real-time detection, and have a credible response wrapped and packed.

Iran’s evolving cyber posture, when combined with geopolitical friction over Israel, mirrors exactly the grid-threat scenario Koppel warned against. The U.S. must no longer treat cyber as a secondary battlefield—it is now the frontline of national resilience.

We have no confidence that the current Administration has thought this through. It must be the 5D chess.

In 30 minutes, crude oil futures will flicker to life, and this isn’t just another session. With tensions between Israel and Iran hitting kinetic levels, traders are watching the Strait of Hormuz like it’s the Nasdaq in March 2020. One headline from Tehran and the whole thing re-prices. Fast.

Straight of Hormuz

Let’s not forget where we are: the Strait of Hormuz is the world’s oil aorta. Two narrow shipping lanes, 21 miles wide — Iran to the north and Oman to the south– carrying nearly 20.5 million barrels of crude per day, about 30% of all seaborne oil. If the global energy market has a single point of failure, this is it.

And Iran knows that. They’ve known it for decades.

Iran has used the Strait as both shield and sword.

1980s Tanker War: Iranian and Iraqi forces attacked over 400 tankers, dragging in the U.S. Navy. Operation Earnest Will turned the Gulf into a Cold War naval theater.

2011–2012: As sanctions piled up over Iran’s nuclear program, top generals threatened a full closure. Brent jumped, premiums widened, and war-risk insurance exploded.

2019: In response to U.S. withdrawal from the JCPOA, Iran didn’t close Hormuz—but it did detain tankers, mine the waterway, and use drones on Saudi facilities. Brent surged $10 in a matter of hours.

Notice the pattern? Full closure isn’t necessary. Tehran only needs to look serious.

From Threats to the “Taco Trade”

Now we’re hearing traders talk about the “Taco trade” again—only this time, it’s less “Trump Always Chickens Out” and more “Tactical Action, Crude Oil.” But don’t discount the political pressure valve: a spike to $120 per barrel could put the “fear of Allah” into Trump and force his hand toward de-escalation. For Tehran, the bet is simple—weaponize oil, drive markets into a panic, and make Washington blink.

It’s the idea that Iran, boxed in by regional war and domestic unrest, will use crude prices as a bargaining chip.The setup:

Hint at closure

Launch a proxy drone or detain a tanker

Send Brent up $30–$50 in a week

Let the West sweat, while Tehran tightens its grip on negotiations

Iran is considering closing the Strait of Hormuz, Iranian news agency IRINN has reported, citing key conservative lawmaker Esmail Kosari, as the conflict with Israel intensifies. – Al Jazeera

This isn’t an oil trade—it’s a geopolitical hostage negotiation wrapped in barrels.

What the Tape’s Telling Us

We’re already seeing stress on the curve.

Brent in backwardation, meaning the market is pricing tight near-term supply.

Options market loading up on $85–$100 calls.

Tanker insurance costs have doubled.

API and EIA data showing steep inventory draws.

And crude hasn’t even opened yet.

What to Watch in the Next Hour

Any fresh intel on tanker disruptions = +3–5% price pop

Western or Gulf military response = volatility spike

Diplomatic olive branch = profit-taking, but elevated floor

This is the Taco moment—if Tehran pulls the lever, every macro desk from London to Singapore will pivot from equities to energy.

Final Thought: The Strait Is the Strategy

Iran doesn’t need to win the war. It just needs to raise the price of fighting it. And that price? Measured in barrels.

Crude opens in 30. The Strait of Hormuz may already be priced for peace. But one fast boat, one drone, or one headline from the IRGC—and the whole tape rerates.