Wow! That was a close one.

Didn’t realize how serious it was during my last post, “Do You Believe In Omens.”

Before I go on, let me THANK my readers from all over the world for the kind and encouraging comments and emails. I will never forget them. A special shout out to my good friends, Joe from RCM, Leo, DS, KD, and JC, who has always had my back, and my special twitter buddies, CG, CK, and GM.

Another Fat Tail Life Event

The following is lifted directly from my medical report.

CONCLUSION: Extensive pulmonary embolism throughout all lobar branches including a saddle embolus.

Evidence of right heart strain.

CONCLUSION: Occlusive thrombus extending from the mid left femoral vein into the popliteal vein.

I asked my doctor yesterday, “how rare is a saddle embolism?” He responded, “it is rare you survived.” Yikes!

Another fat-tailed life event. Thankfully, this one on the right side of [the] mean.

A lifelong friend told me the other day, “you have always beat the odds.”

I don’t know about that but one thing I learned during this whole episode is that when the Grim Reaper (GR) makes the margin call, and all of us will eventually receive one, only three things matter: 1) family; 2) friends; and 3) faith. The GR is the great equalizer.

She doesn’t care about the value of your portfolio, the size of your house, the car you drive, or if you wear French neckties. As Denzel says, “you’ll never see a U-Haul behind a hearse.”

Doctors In The United States

Thank goodness for immigrants from those “shithole countries.”

My pulmonologist was from India and my lead doctor, Dr. R., from Syria. Sadly, Dr. R. felt as if he had to apologize or rationalize why he was here when I asked him where he was from. I would have nothing to do with it.

I told him one of my best friends in grad school was from Syria and went back to become the Economy Minister for Assad; and that Syrians were good and very tough people.

Go no further than Dr. R’s sad response to understand the legacy of slavery in the United States. The racist rhetoric that spews from Trump is doing structural damage to America’s social infrastructure. We suspect, with great hope, that may be about to end in 2019, however.

Immigration And The Medical Industry

Nevertheless, the impact of immigration on the medical services industry in the United States is nothing less than stunning.

Why are your medical bills rising?

Here is one reason:

“India, China, Philippines, Korea, and Pakistan are the top five origin groups for physicians and surgeons,” said Jeanne Batalova, a senior policy analyst and demographer at MPI.

Iran and Syria, two of the countries whose citizens are no longer allowed entry to the US, are the sixth and 10th largest contributors, respectively. “So we’re talking about substantial representation from these countries [in the doctor workforce] here,” she added. The ban on these people will likely be felt at hospitals and clinics across the nation. – Vox

Foreign-trained doctors make up more than 50 percent of geriatric medicine specialists and nearly 40 percent of internal medicine doctors.

The data speaks. Is the administration listening?

We do think the overwhelming majority of Americans are, however.

Take Heed

I learned much about pulmonary embolisms (PE) during my little event.

They are one of the leading causes of death in the United States; they do not discriminate by age or health: Serena Williams has had two, and one ended the career of basketball star Chris Bosch; and that airline pilots, police officers, truck drivers, and office workers are the most susceptible to DVTs and PEs due to their propensity to sit for long spells in a restricted position.

My doctor and I have traced back the origins of my blood clot, which began in the left calf, to a flight to the east coast during the summer, which included long periods of driving up and down the eastern seaboard. I also can sit hours doing research, crunching data and writing without getting up. Believe me, those days are over.

All you traders or researchers, who tend to sit for long spells, should learn from my lesson. Get up and move – just as the Dow has over the past few weeks! Don’t just sit there for hours. Blood, just like capital, clots if it isn’t flowing.

Grab some compression socks, move your legs, get up from the desk at least once an hour. Your life may depend on it.

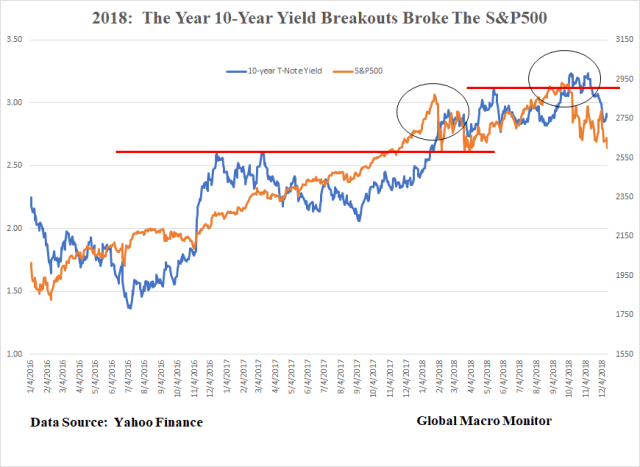

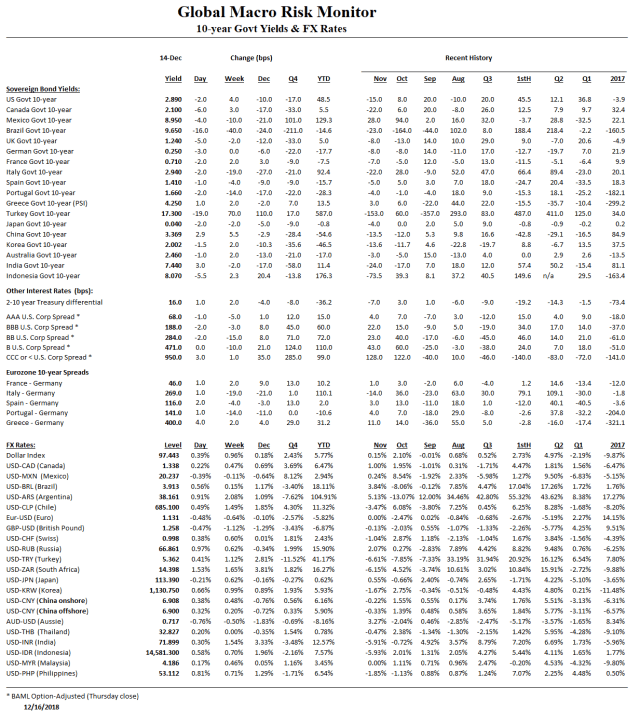

2019

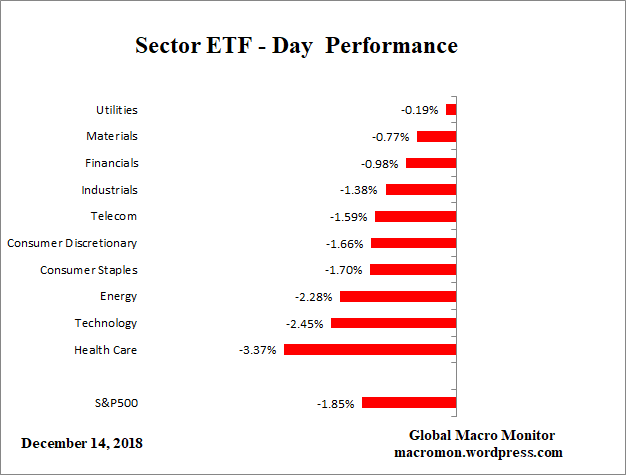

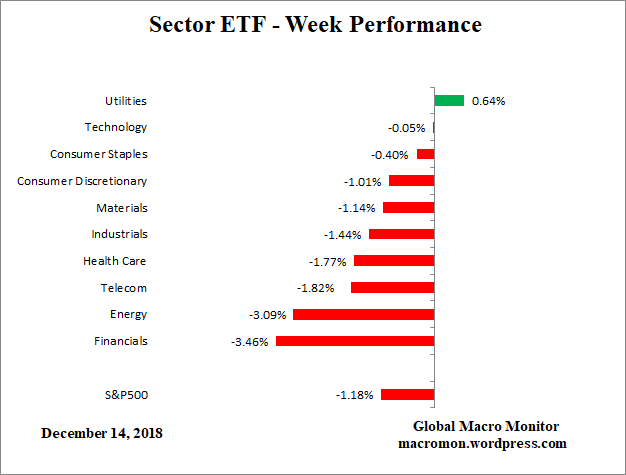

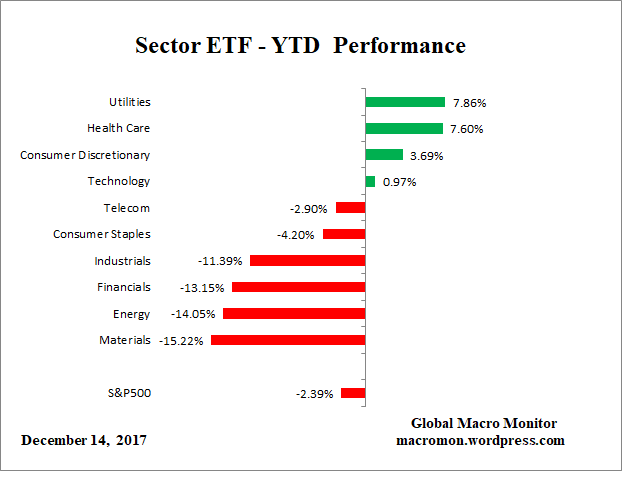

I am looking forward to 2019, which is shaping up to be a volatile one and a watershed year. The markets are in the midst of a major speed wobble and having trouble diagnosing the causes of the volatility. We have our ideas and look forward to sharing them with you. We are fairly certain it isn’t the next 25 bps in the Fed funds rate.

It was entertaining, yet, at the same time, a disgrace, to lay for a week in my hospital bed watching all the forces, including POTUS, CNBC, and Jim Cramer, pressuring Jerome Powell and the Fed to bow down, kiss the ring and come to the rescue, saving the market from itself.

We are not sure how long he can hold out but we do hope the Chairman and other members of the FOMC resist becoming Mr. President and Mr. Market’s bitch. Using cyclical policy tools to address structural problems is one reason why we find ourselves in the current economic and political mess.

If the economy can’t withstand a barely positive real Fed funds rate, is that an economy you want to invest in? Weaning the markets from the monetary crack is the first step toward moving to a sustainable economy. But has it ever been really about a sustainable economy or is it just the short-term gain — the year-end bonus or next election or news cycle? We are hoping, maybe beyond hope.

GMM’s New Model

In early November, we solicited your thoughts about the Global Macro Monitor (GMM) moving to a paid subscription model. We had a tremendous response but many of those interested were from weak currency countries and found the monthly nut restrictive. We toyed with price discrimination but along came our little medical event and haven’t had the time nor the energy to work on it any further.

We are now leaning more toward a voluntary model for the GMM. Yes, as always, the free rider problem and we do hope it will work.

If you have followed us during the last year, we got many things right and many things wrong.

We also were the first to nail many of the major issues, including our declaration there will be no BREXIT and the Dems would take at least 37 seats in the midterms with a Lavender Wave.

BREXIT ain’ gonna happen. The political extremes on both ends have “woke” the sleepy and complacent middle, women, and the young…

A second vote on BREXIT is an uphill battle, but if the Trump administration gets “bitch slapped” in the November midterms the momentum and pressure for a new BREXIT vote will build, in our opinion. – GMM, October 20th

Pressure Building For A People’s Vote

Note the pressure now building for a second BREXIT referendum, which the remainers will almost surely win. Buy cable.

Back to you soon. Happy New Year, folks!