Check out the latest from the Cleveland Fed president, Loretta Mester:

Mester advised that there is “no evidence” for thinking that a flatter curve signals a weaker economy at this time, Reuters reported. She added that “structural factors,” such as bond-buying by central banks, are compressing the curve.

Mester’s comments coincided with a further narrowing of the yield spread based on the 10-year and 2-year Treasury rates. The yield difference between the two maturities fell to 52 basis points yesterday (Mar. 27 26), close to the lowest level since the recession ended in mid-2009. In January, the 10-year/2-year spread dipped to 50 basis points, a post-recession low. – Capital Spectator

Information Positive Feedback Loop Many in the market, we fear, are being hoodwinked by the flattening yield curve, however. It’s purely the result of technicals and not economic fundamentals.

Nevertheless, some still look to the badly distorted bond market as a signal of the health of the economy and act accordingly. Such as delaying capital spending; becoming more risk averse; and cutting back on consumption, for example.

A flatter yeld curve also makes bank lending less profitable.

This could thus lead to what George Soros calls “reflexivity“, a feedback loop where the negative, but false, signal from the bond market actually causes an economic slowdown or leads to a recession. So much for efficient markets.

“ We’re in a depression. That is what the bond market is telling us.”

Or the ubiquitous, “what is the bond market telling us?” Come on, man! – GMM

Time For The Reverse Twist

We have also recognized the flow of new issuance and the drying up of demand by the Fed and foreign central banks poses a new risk for the yield curve. It is one reason, we believe, bonds have not been a benefactor of the “flight-to-quality” trade in this nasty correction, which is very rare.

We were surprised that the Fed did not unwind Operation Twist, where it swapped short-term bonds for long-term bonds, when it decided to end quantitative easing (QE). The majority of the stock of long-term Treasury notes and bonds remains in the hands of the Fed and foreign central banks, which distorts the true market signal of risk-free yields.

Given that market and the global economy are now so prone and susceptible to perverse feedback loops, where a misread of the yield curve could feed into the real economy, maybe it is time the Fed finally unwinds Operation Twist. It will surely steepen the yield curve and give us a clearer signal of “what is the bond market telling us?”

This next quarter is going to be a major battle between the cyclical bulls and structural bears.

Cyclical Bulls

The bulls have the strength of current earnings, which may, or may not be priced (probably the later as the market is still at extreme valuations). Furthermore, short-term indicators reflect too much bearishness – put-call ratio high at 134 percent. Thus, we wouldn’t be surprised by a big push and full on frontal assault by the bulls in the first part of the quarter.

Seasonals also favor April.

Effects of Tax Cuts

Much of the bullish data derives from the recent tax cuts. We believe, though the tax cuts improve the accounting for profits, they haven’t changed the underlying economics and fundamentals of the stock market.

We seriously doubt the tax cut will increase aggregate demand enough to get companies lathered up to really step on the gas of capital expenditures in a meaningful way. Maybe at the margins but not a game change.

Moreover, is the tax cut going to pave the way for new life changing products from Apple Open up new export markets for Boeing or Intel? Significantly increase domestic demand for good and services? Those will happen independent with or without a tax cut.

Buybacks? Yes.

The big mistake is to assume that what’s scarce is cash. The reality is that profitable investment opportunities are scarce.

What can we learn from the recent surge in stock buybacks, in which companies buy back their own shares, effectively returning their spare cash to shareholders?

Quite possibly, nothing, as far as the merit of the tax cuts goes. Standard economic theories suggest buybacks would occur whether or not the tax cuts succeed at stimulating investment. – NY Times, March 30

Increased demand and expanding markets are the mother’s milk of profitable opportunities. Tax cuts, less so. It was a good attempt by government to jump into the financial engineering game, however.

At some point, we expect the market to come to the same conclusion, and that epiphany will be further complicated and coincide with a realization of the perverse fiscal impact of tax cuts, coupled with stepped up government spending leading to debt concerns.

Having said this, we still think the corporate tax cut was the right policy but it is certainly not the economic Shangri-La that many and the markets may hail it to be.

Structural Bears

The structural bears have, what appears to be, the shifting of tectonic plates of the underlying fundamentals that have driven the global bull market in stocks. The ground is beginning to move under the bull markets’ feet.

But those macroeconomic outcomes result from policy decisions abroad and the market-clearing movements of financial prices. Officials in important emerging-market economies chose to accumulate Treasury securities, because US yields, albeit low, were higher than in other advanced economies. A confrontational stance on trade, together with greater reliance on government debt, may well extract a higher toll to balance flows of goods and services and of capital. Moreover, the US will be paying for its current excesses with the promise of future payments, and inefficient stimulus now will not give future generations the productive resources needed to make good on it. – Carmen Reinhart, Project Syndicate, March 30

If the S&P500 trades above 2,802, and is sustained, we will reassess our view and concede the market just doesn’t care, at least for now.

The Coming Donnybrook

We expect a major donnybrook between the cyclical bulls and secular bears in the coming quarter. In fact, the next quarter may be one of the most important quarters in the financial markets in the past 50 years; maybe not as significant as Q3 & Q4 2008, however.

Can the positive cyclical forces mentioned above outweigh the structural issues challenging the market’s long-term positive momentum? We seriously doubt it but don’t entirely dismiss we may be wrong.

After all the natural trajectory are for markets is to move north and the bulls have the gravitational pull on their side, they always do. The bears will have their work cut out for them in the next three months. This bull won’t die without a fight. Expect some bloody battles ahead.

The Market As The Final Political Arbiter

Finally, the markets are going to be the final political arbiter as to whether the Trump administration is either #Making America Great Again (MAGA), or ruining the country and its standing in the world. The president has placed his bet on the stock market as a weighing machine for his policies, economic management, and competence of the White House.

No political statement as we leave it to the markets to vote.

The biggest overall risk, in our opinion, is that we now live in an asset driven global economy, which is prone and susceptible to perverse feedback loops. The inflation/deflation dialectic, and subsequent asset moves will be on full display during the bear market until global markets finally realize the major central banks can not and and will not allow debt deflation to occur.

If the central banks have to directly monetize, say, universal basic income and/or pension shortfalls to stimulate demand, we have no doubt they will.

Sorry, deflationistas, that sounds a lot like Argentina. Let’s hope we never have to go there.

Last year’s Republican tax plan was hailed as a victory for US President Donald Trump, but it carries a hidden cost: a ballooning US trade deficit. As happened after Ronald Reagan’s cuts in the 1980s, Trump’s cut is almost certain to widen the budget deficit and fuel growth in the US current-account deficit.

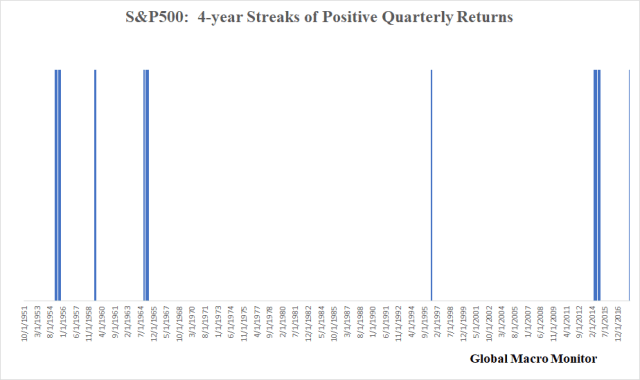

Going into Q1, the S&P500 had delivered positive returns for 16 consecutive quarters or four straight years. The chart illustrates how rare the streak has been over the past half century.

There have been only five other clusters of similar streaks.

The below table shows the post 3, 6, and 12-month returns after the 4-year streak was snapped.

Mixed results with no discernible pattern, however.

We fully expect a “revolution” in the measurement of economic data as “big data” takes an increasing role in society and dominates metrics and measurements.

It won’t be long before we have precision real-time measurements from everything to real economic activity, inflation, and labor market conditions.

Gross domestic product is the defining metric of the last 80 years. It arose from the ruins of the Great Depression to serve as the ultimate measure of an economy’s welfare, the indicator to end all indicators. But GDP’s long run may be coming to an end.

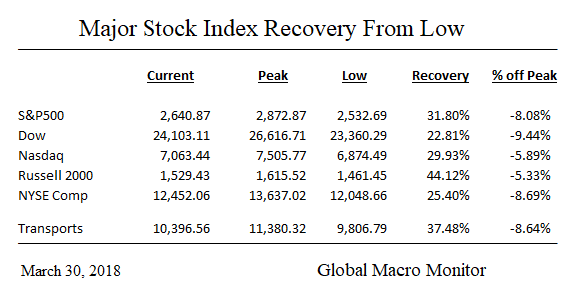

The markets closed out the quarter trying to recover from one of the biggest volatility shocks in history, which began in early February. The question for Q2 is: Was the v-shock a one-off or a regime change? We lean toward the latter.

The next quarter will likely be a battle between the cyclical bulls and structural bears.

The bulls have the strength of current earnings, which may, or may not be priced (probably the later as the market is still at extreme valuations). Furthermore, short-term indicators reflect too much bearishness – put-call ratio high at 134 percent. Thus, we wouldn’t be surprised by a big push and full on frontal assault by the bulls in the first part of the quarter. Seasonals also favor April.

Da’ Bears

The structural bears have, what appears to be, a shifting of the tectonic plates underlying the global bull market in stocks. That is the ground in shifting before the markets’ feet.

But those macroeconomic outcomes result from policy decisions abroad and the market-clearing movements of financial prices. Officials in important emerging-market economies chose to accumulate Treasury securities, because US yields, albeit low, were higher than in other advanced economies. A confrontational stance on trade, together with greater reliance on government debt, may well extract a higher toll to balance flows of goods and services and of capital. Moreover, the US will be paying for its current excesses with the promise of future payments, and inefficient stimulus now will not give future generations the productive resources needed to make good on it. – Carmen Reinhart, Project Syndicate, March 30

That is more than a wall of worry, in our opinion.

The Coming Donnybrook

We expect a major donnybrook between the cyclical bulls and secular bears in the coming quarter, which may be the most important quarter in the financial markets in the past 50 years. The natural trajectory are for markets to move north.

Finally, the markets are going to be the final political arbiter on whether the Trump administration: is #Making America Great Again (MAGA), or ruining the country and its standing in the world.

No political statement here, we will leave it to the markets to decide.

This could end America’s free-ride: no more QE; no more balance of payments deficits without tears; and no more foreign financing of the U.S. budget deficit.

We hope the Administration at least is concerned and has it on their radar.

No doubt it is, in part, the result of this (see here).

Good morning from the US home of world's undisputed reserve currency. BUT Dollar's supremacy is slowly eroding. Latest SWIFT payment data highlights that euro continues to close the gap on the dollar. Euro's status continues to grow amid backdrop of potential US-China trade war. pic.twitter.com/T880oroh3T