The American political system may just be about to wake up and inching torward bipartisanship. The failure of the Republicans to “repeal and replace” Obamacare after seven years of pounding the table is a “big fail.”

After controlling both houses of Congress and the White House the Republicans, at the end of the day, couldn’t get it done.

Why?

We stand by our major conclusion in our post, A Few Thoughts On Why Health Care Went Down, when the first House healthcare bill went down. Most noteablely,

… the large majority of the country wants universal affordable health care and the next bill will be one to repair Obamacare. – Global Macro Monitor

This is not a political statement — so hold off on the hate mail — but it is a fact supported by the polling data.

New Approach

“…the Congress must now return to regular order, hold hearings, receive input from members of both parties, and heed the recommendations of our nation’s governors.” – Sen. John McCain

Imagnine what would happen if President Trump now picks up the phone to Chuck Shumer to negotiate a fix to the health care system? Probably worth 2,000 Dow points and it could reigvorate the Trump agenda. After all, wasn’t President Trump elected to transcend politics and get things done?

Or, how about Chuck Schumer reaching out to President Trump – we know the President likes that – and get the ball rolling? Look how President Trump changed his tone on the Paris Climate Accord after President Emmanual Macron reached out to him.

…at a joint press conference before French and American journalists at the Élysée Palace, Trump indicated he may reconsider his decision.

“Something could happen with respect to the Paris accord,” he told reporters with typical Trump-like vagueness. “We’ll see what happens.” – Daily Beast

Come on, get it together, politicos! Let’s get some things done! Do it for Jamie!

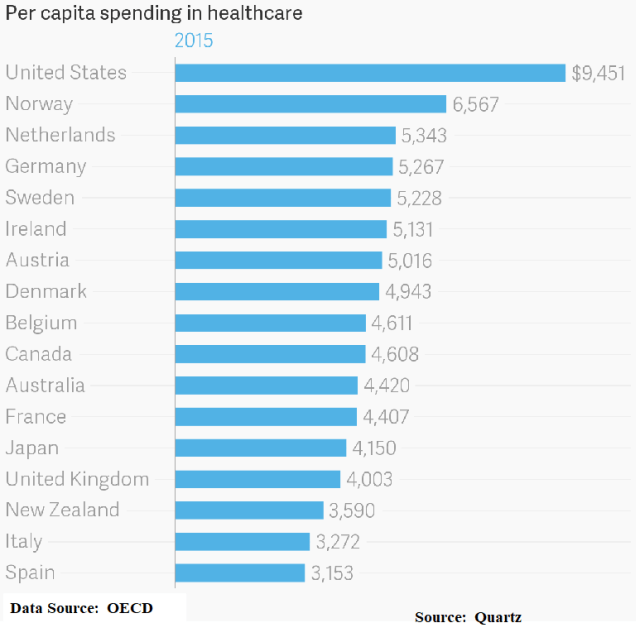

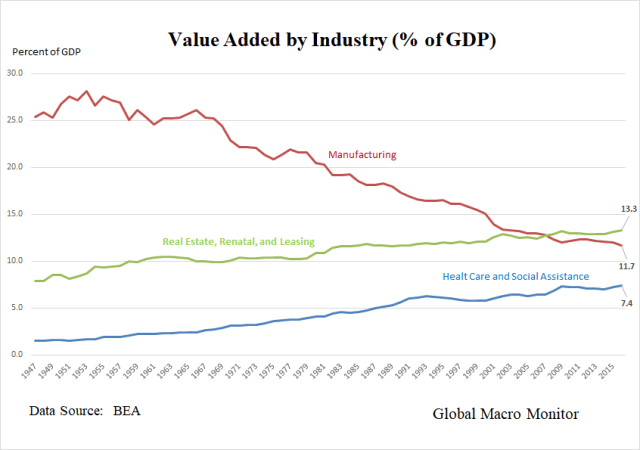

The Fallacy That Health Care is 18 percent of GDP

While we are in this space, let’s set the record straight.

There is the notion out there that healthcare is 18 percent of GDP. This is technically incorrect as that anlaysis wrongly conflates apples with oranges, for example. Gross domestic product is calculated on a value-added basis. Whereas spending, in most cases, does not, as it often includes costs of intermediate goods.

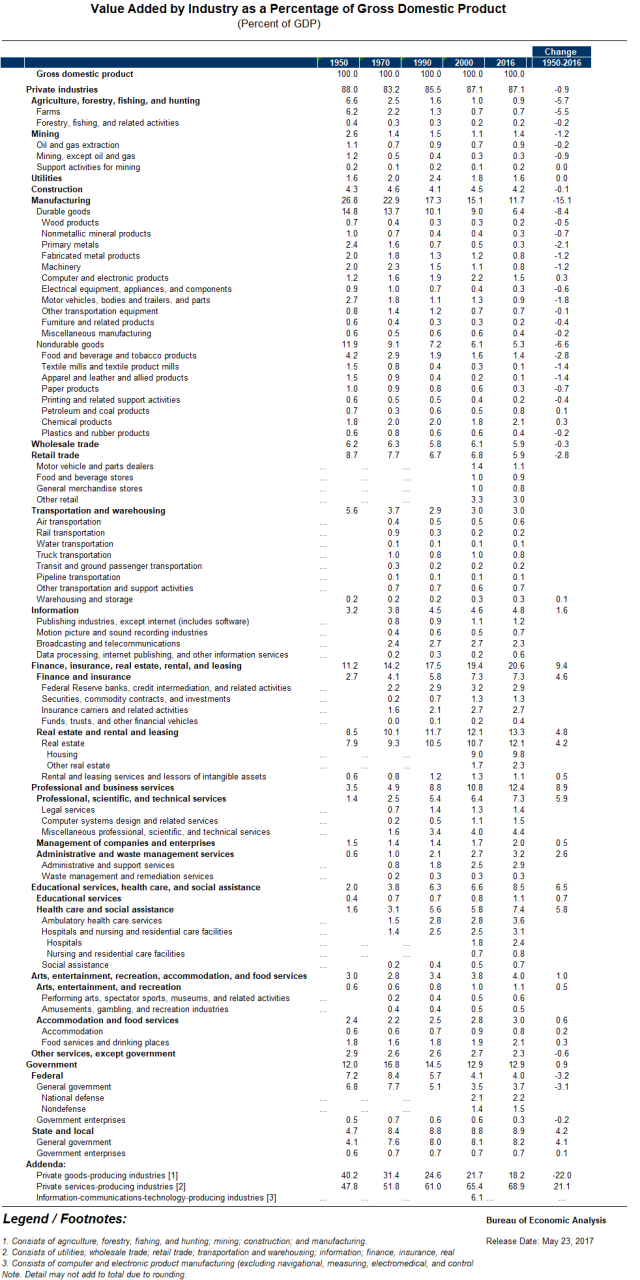

It is probably true to say that the U.S. spends 18 percent of GDP on health care, but it is not true to say health care is 18 percent of the U.S. economy. In fact, on a BEA defined value-added basis health care is only 7.4 percent of U.S. GDP, smaller than the real estate sector, for example, which is now the largest subcomponent of GDP.

The Bureau of Economic Analysis explains the differences,

Since the circular flow of macroeconomic expenditures (demand) or income (supply) are consistent, these different measures should produce the same result for the U.S. economy as a whole. Industry-level value added (income) data are published in the GDP by industry accounts by BEA. One challenge for applying this relationship to the health sector is that of the 65 unique industries identified in these accounts, only two of them clearly are health care industries: ambulatory health care services and hospitals and nursing and residential care. The combined value added (supply) of these two sectors was 6.6 percent of GDP in 2012, well short of health expenditures’ (demand) share of 17.2 percent of GDP. One reason for this gap is that some important health care activities are subsumed in other industries. Among these are pharmaceutical manufacturing, which is part of the chemicals industry; electro-medical and therapeutic apparatus manufacturing, which is part of the computer and electronic products industry; and medical equipment and supplies manufacturing, which is included in the miscellaneous manufacturing industry. – BEA

New Measures of GDP

Our good friend, Jose Cerritelli, and legendary M.I.T. eonomist is doing some good research on the shortfalls of measuring GDP. In many developing countries the data are no better than educated guesses. In fact, some are now using satellite-recorded luminosity as a proxy for economic activity.

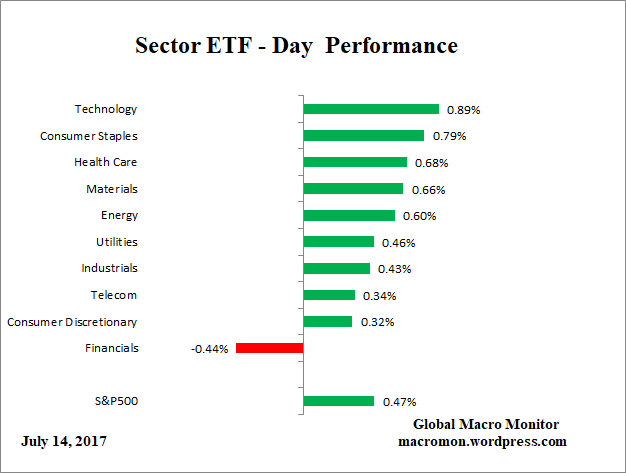

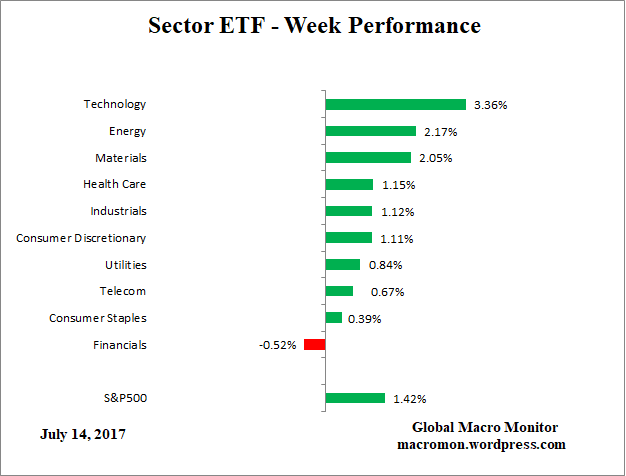

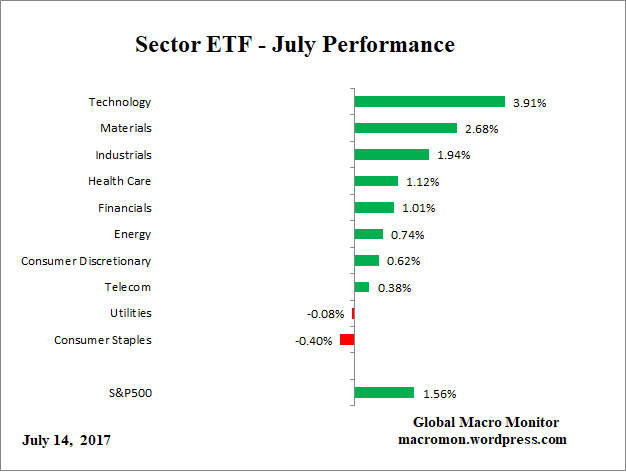

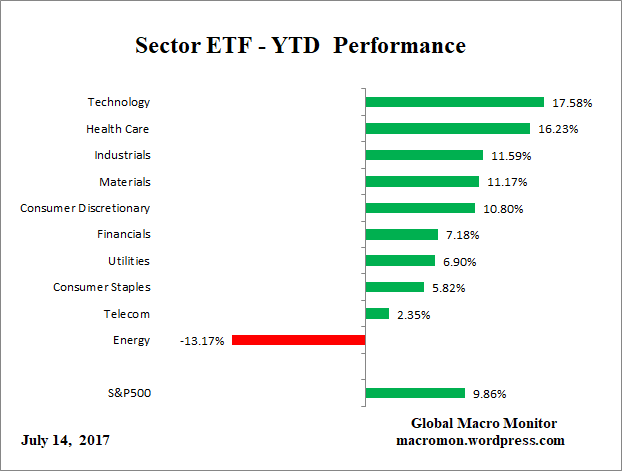

Data Appendix