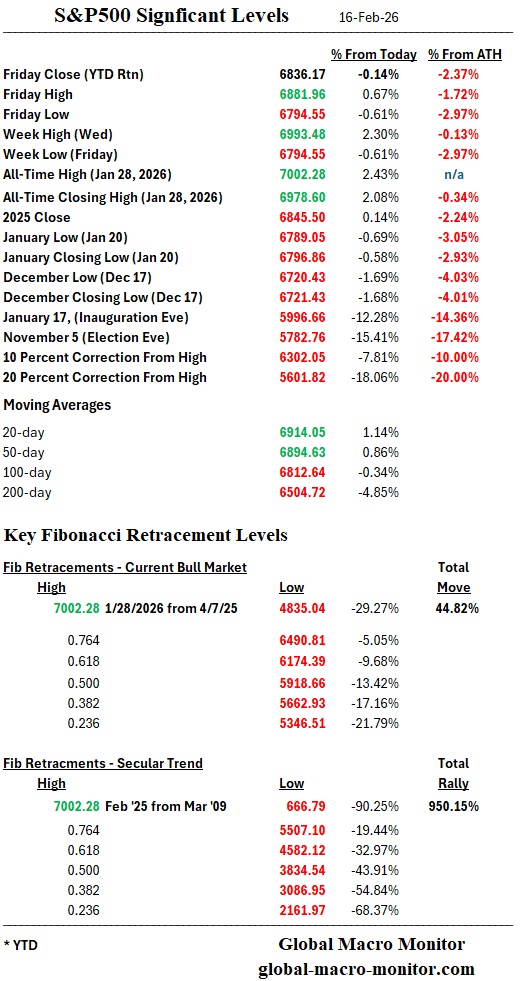

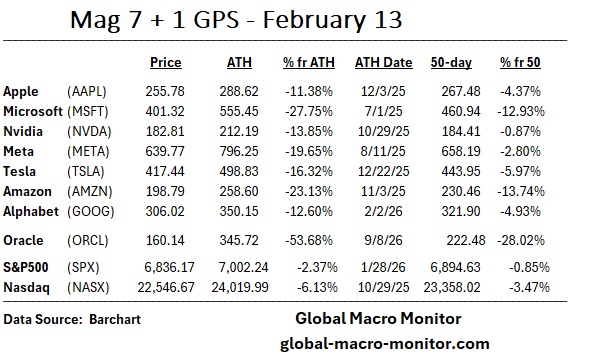

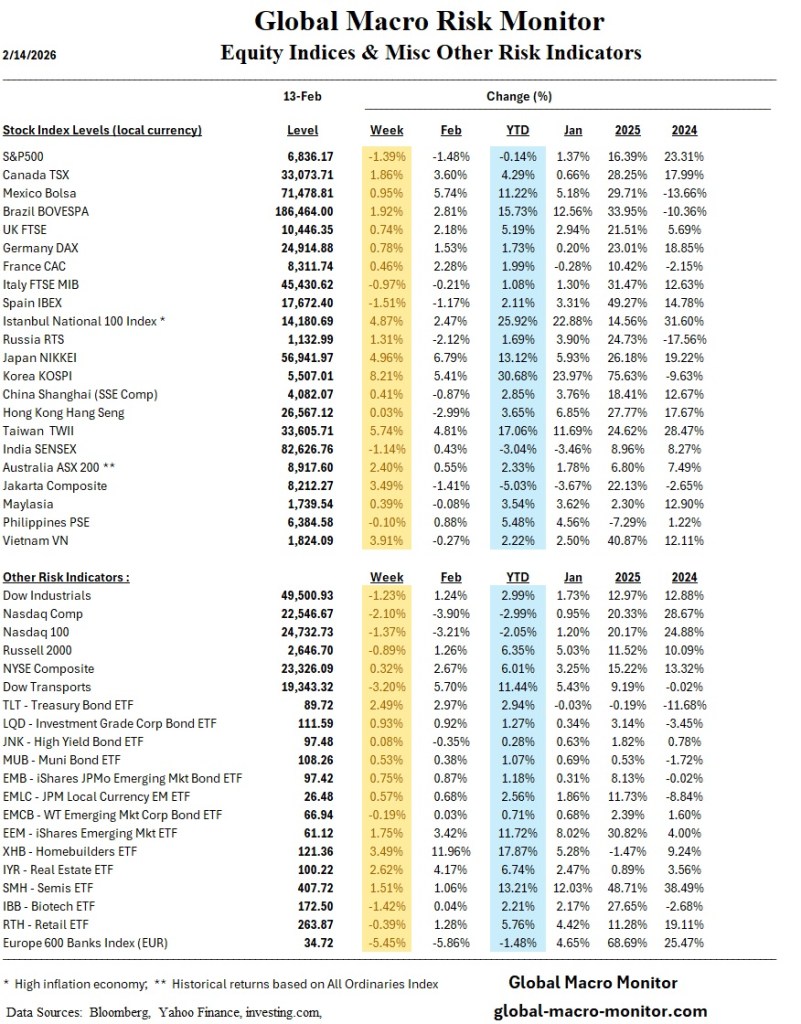

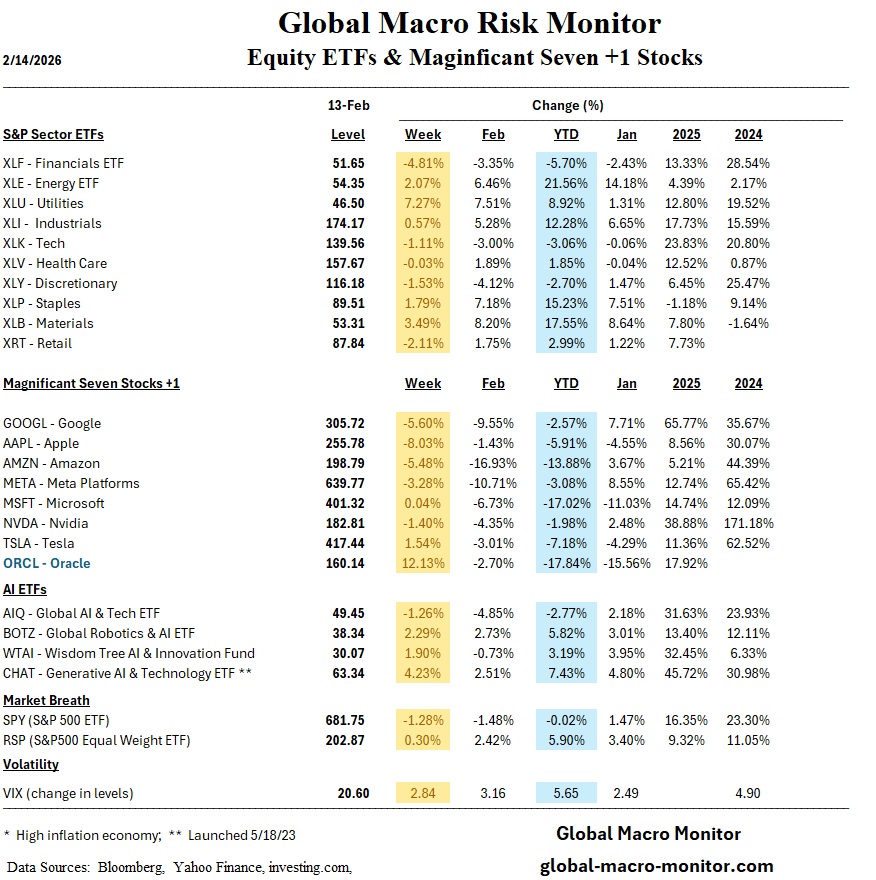

Sorry, no commentary this week. Stay tuned!

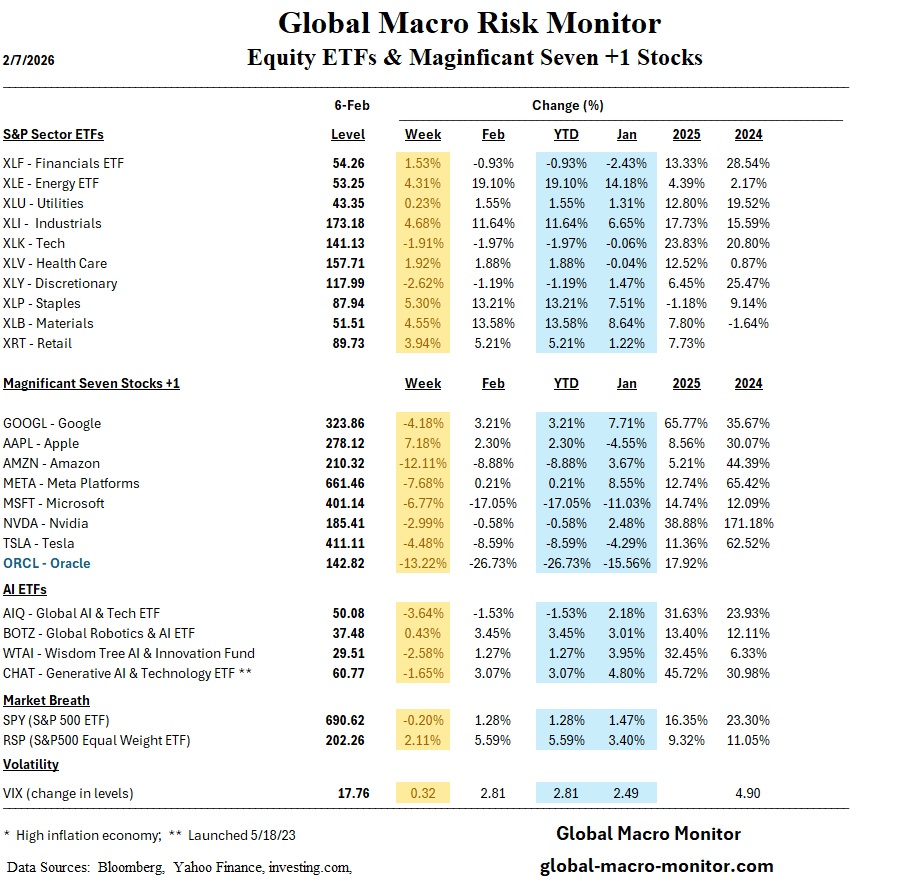

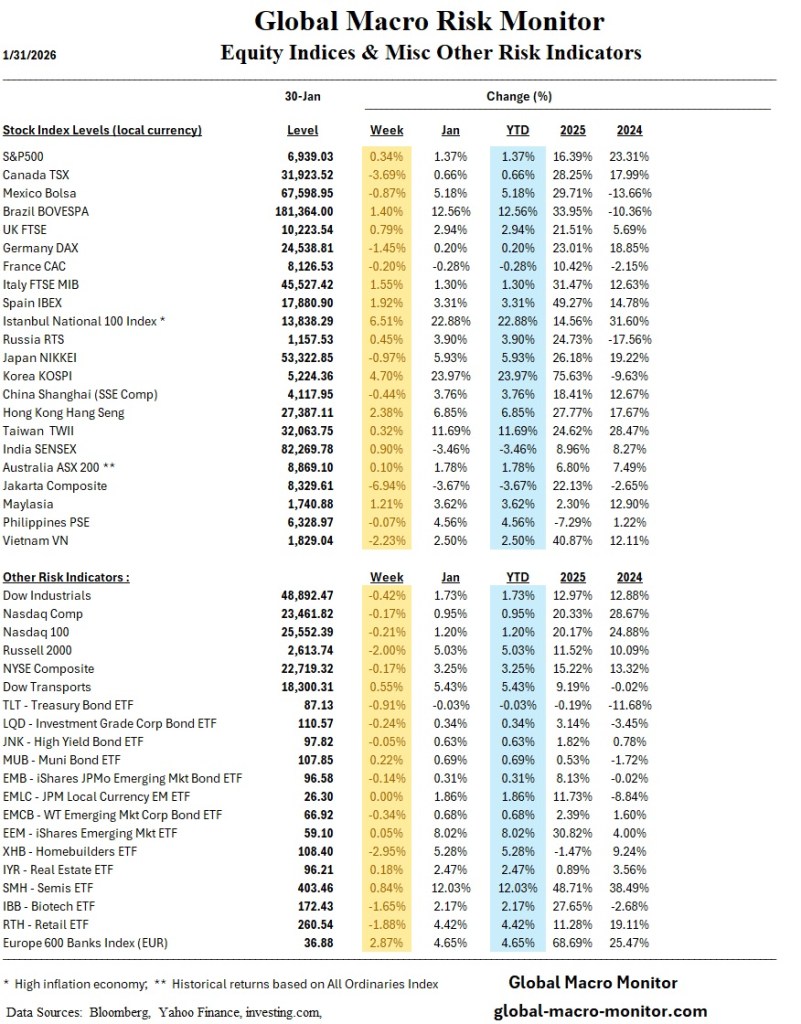

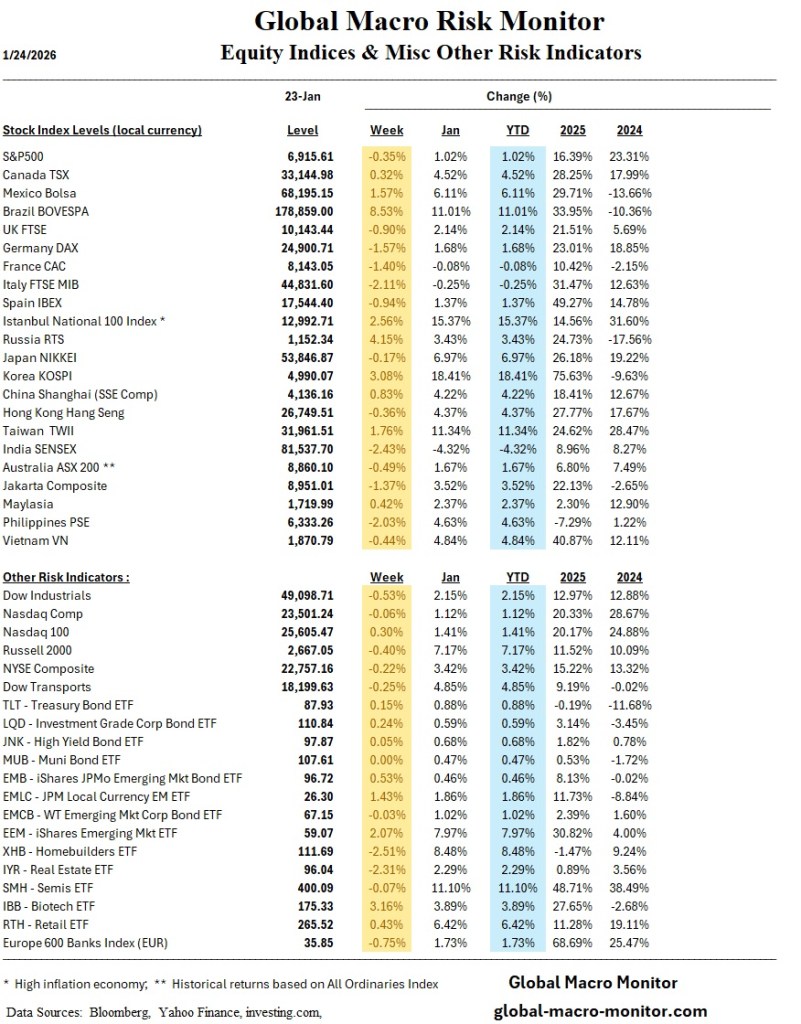

The week ending February 6 was defined by rising internal stress beneath still-resilient headline equity levels, with sharp dispersion across asset classes and regions. U.S. equities experienced notable volatility, with the S&P 500 briefly touching record highs early in the week before selling pressure intensified midweek. A sharp Friday rebound, however, reversed much of the damage and caught short sellers off guard, restoring modest weekly stability .

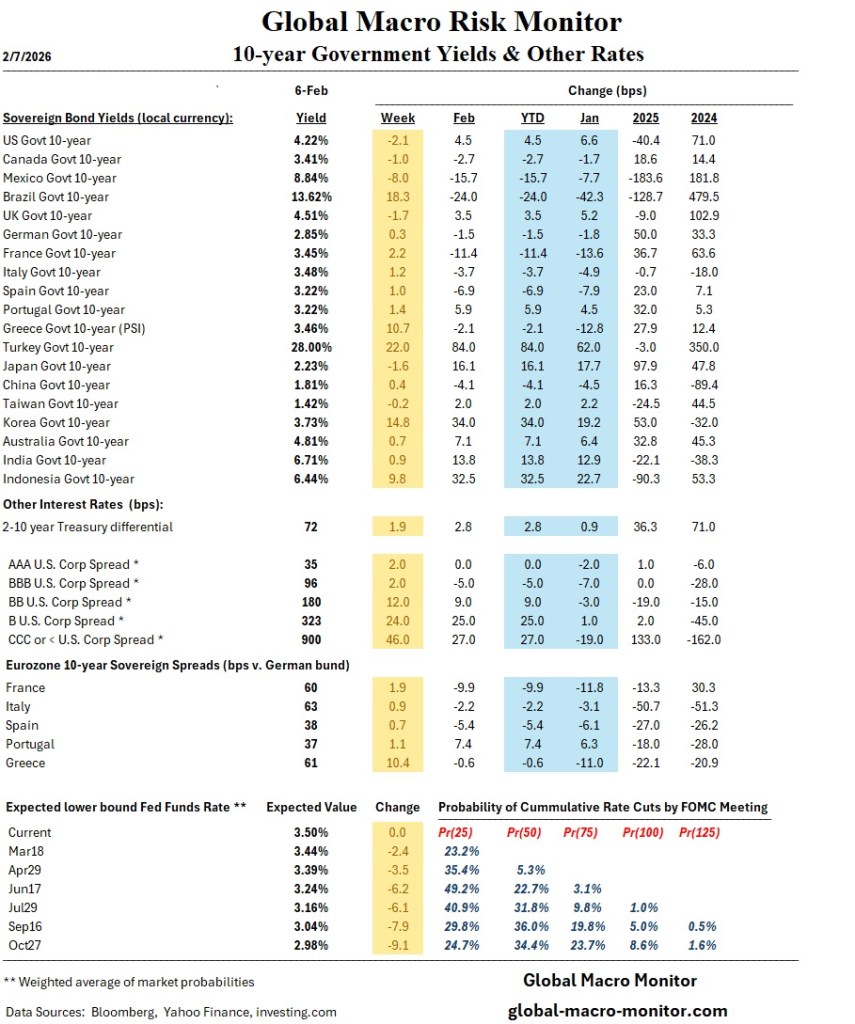

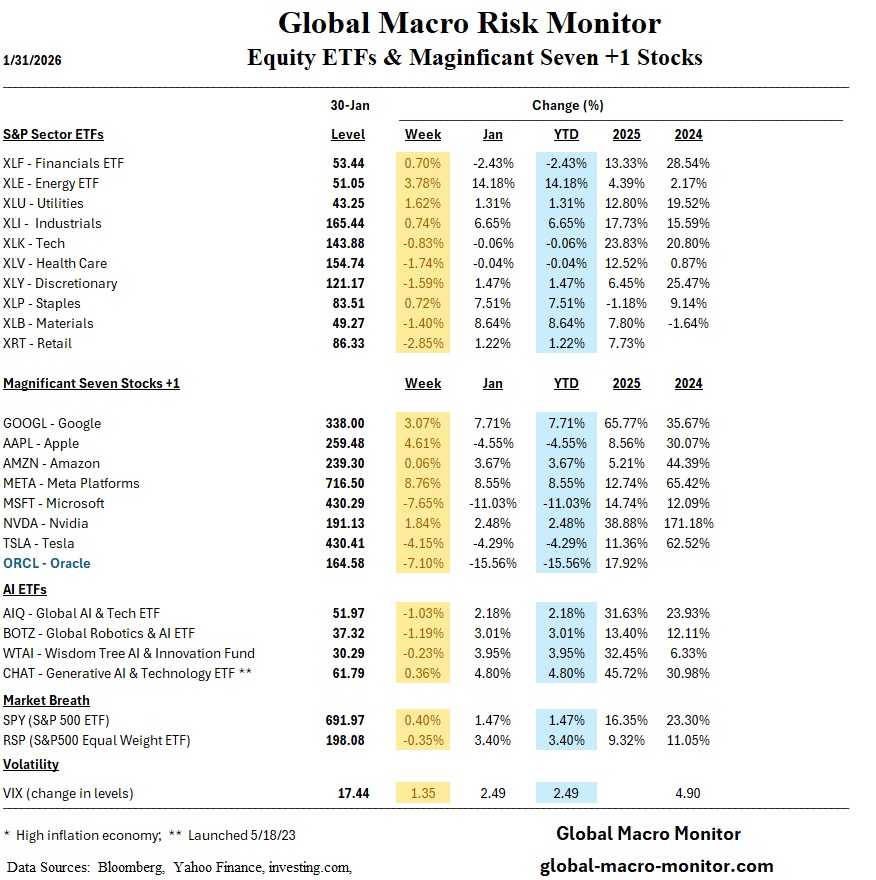

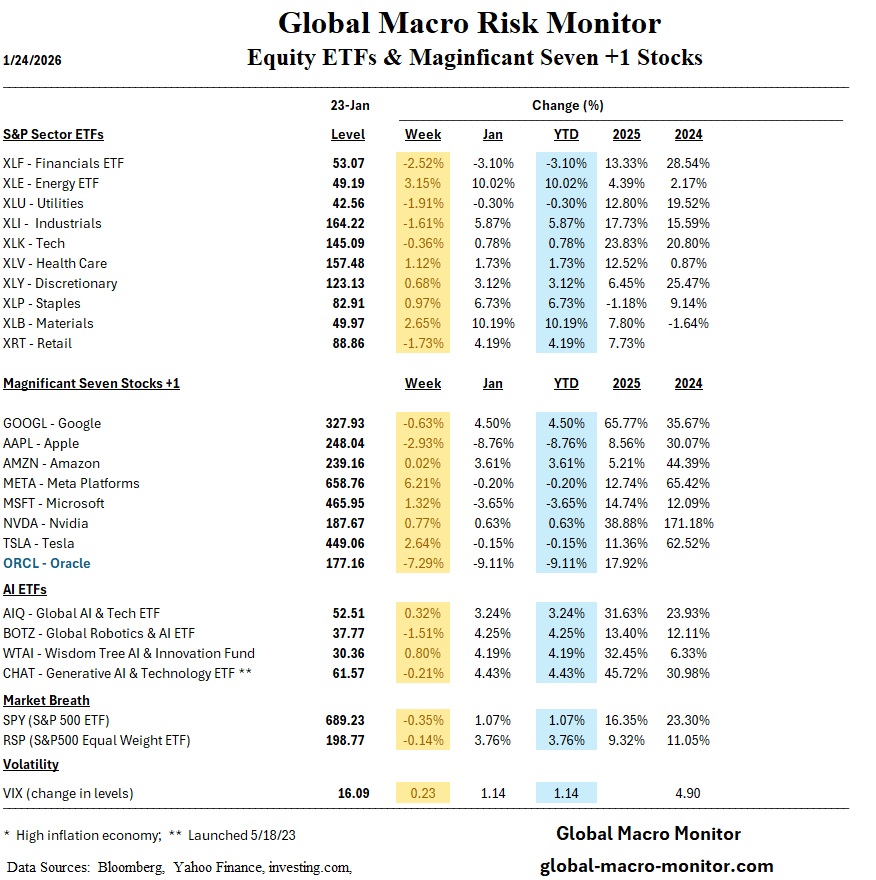

Beneath the surface, market leadership continued to broaden away from mega-cap growth, as cyclicals and value-oriented sectors—particularly energy, industrials, materials, and staples—outperformed meaningfully. In contrast, the “Mag 7” (excluding Apple) posted significant losses, reinforcing a rotation away from concentrated AI-driven equity exposure. Credit markets also reflected rising stress, with widening spreads in lower-quality credits and notable deterioration in peripheral Europe, including Greece .

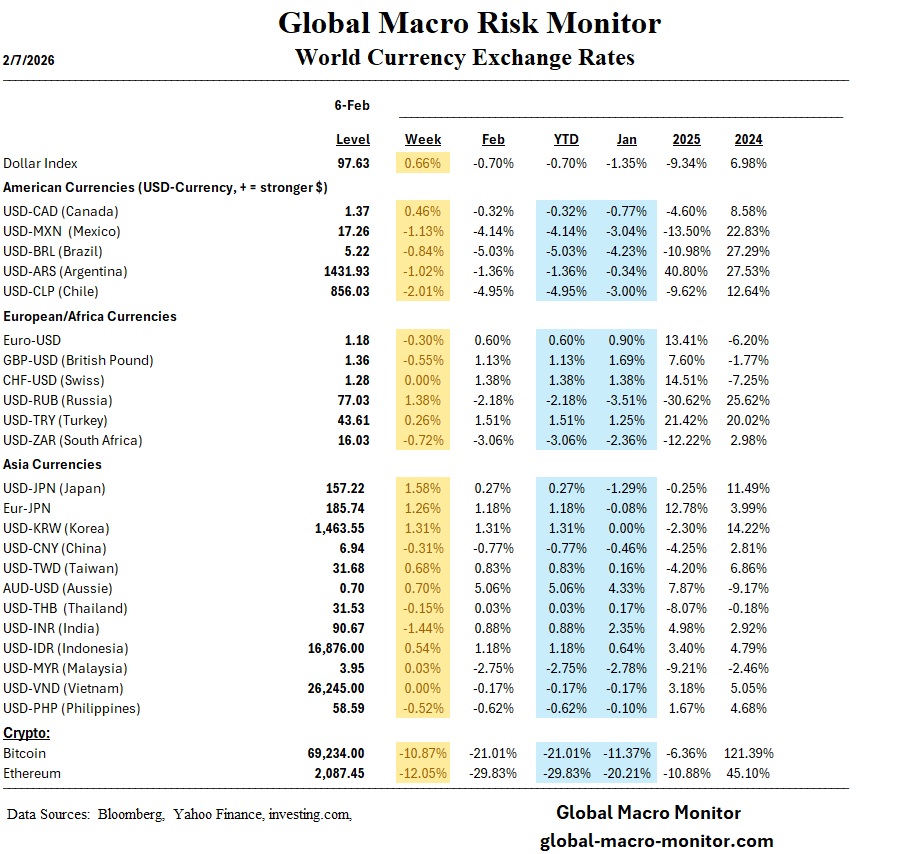

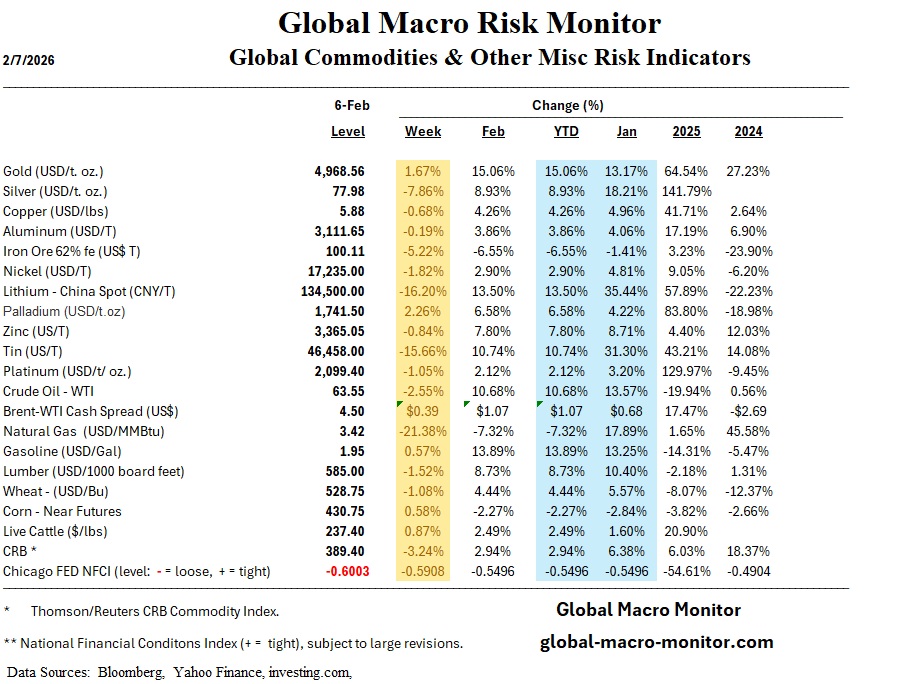

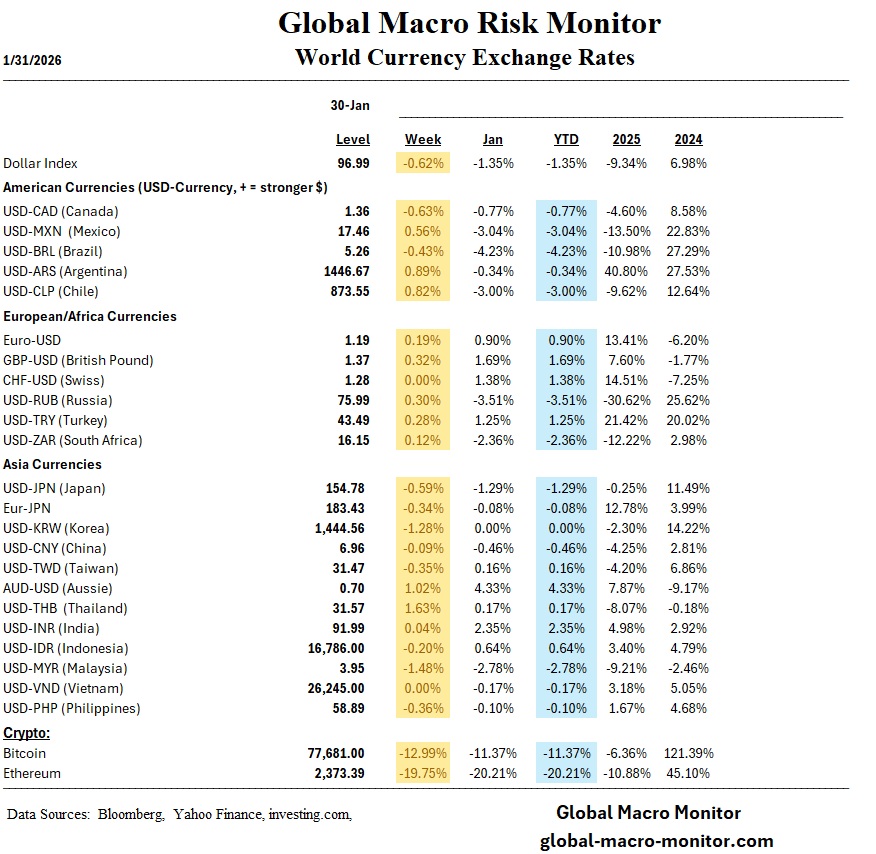

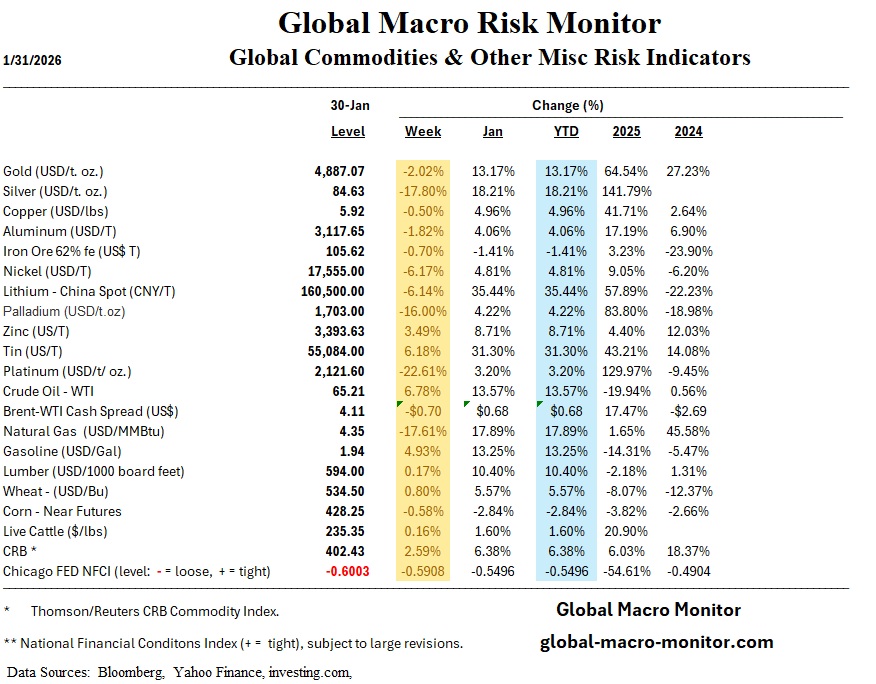

In commodities, gold strongly outperformed, finishing the week higher despite sharp early volatility, while silver lagged. This divergence underscored renewed demand for defensive, liquid hedges amid macro uncertainty. By contrast, Bitcoin underperformed sharply, ending the week down roughly 10% despite a dramatic $10,000 rebound on Friday, highlighting aggressive deleveraging across speculative risk assets.

Globally, leadership continued to shift outside the U.S., with select emerging markets such as Mexico posted outsized gains. Overall, the week reinforced a key theme: headline stability masking growing internal fragility, with positioning increasingly vulnerable to macro and policy surprises

Regional Performance Highlights

United States

Asia

Europe

Latin America

Commodities & Crypto

The Week Ahead

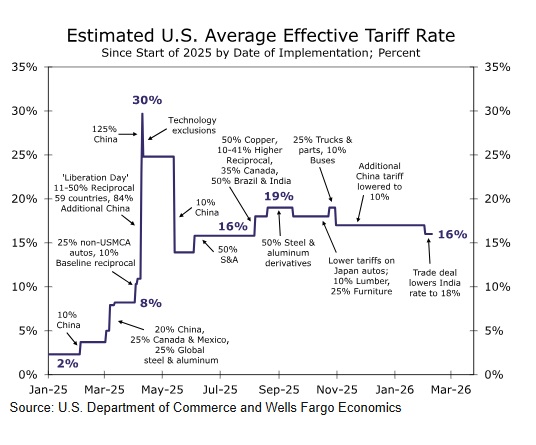

Wells Fargo published a pair of charts this week that appear to tell very different stories. On the one hand, higher tariffs are being promoted as a catalyst for job creation. On the other, job openings continue to slide meaningfully. It is increasingly difficult to reconcile those narratives. More plausibly, the growing drag on labor demand reflects the accelerating impact of AI, as productivity gains allow firms to do more with fewer workers.

Global markets ended the week with rising internal stress beneath still-resilient headline equity levels, setting up a fragile start to the new week. While U.S. equities held modest January gains, risk signals deteriorated meaningfully late in the week, culminating in a sharp weekend collapse in cryptocurrencies—a development likely to pressure risk assets at Monday’s open.

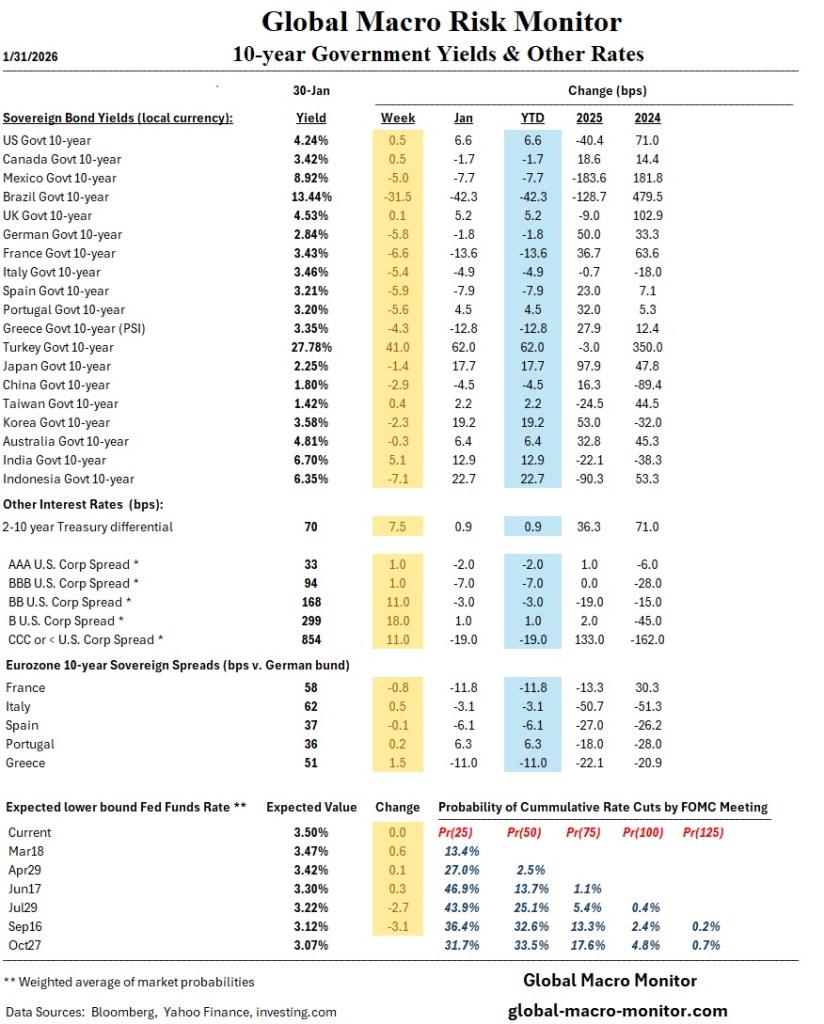

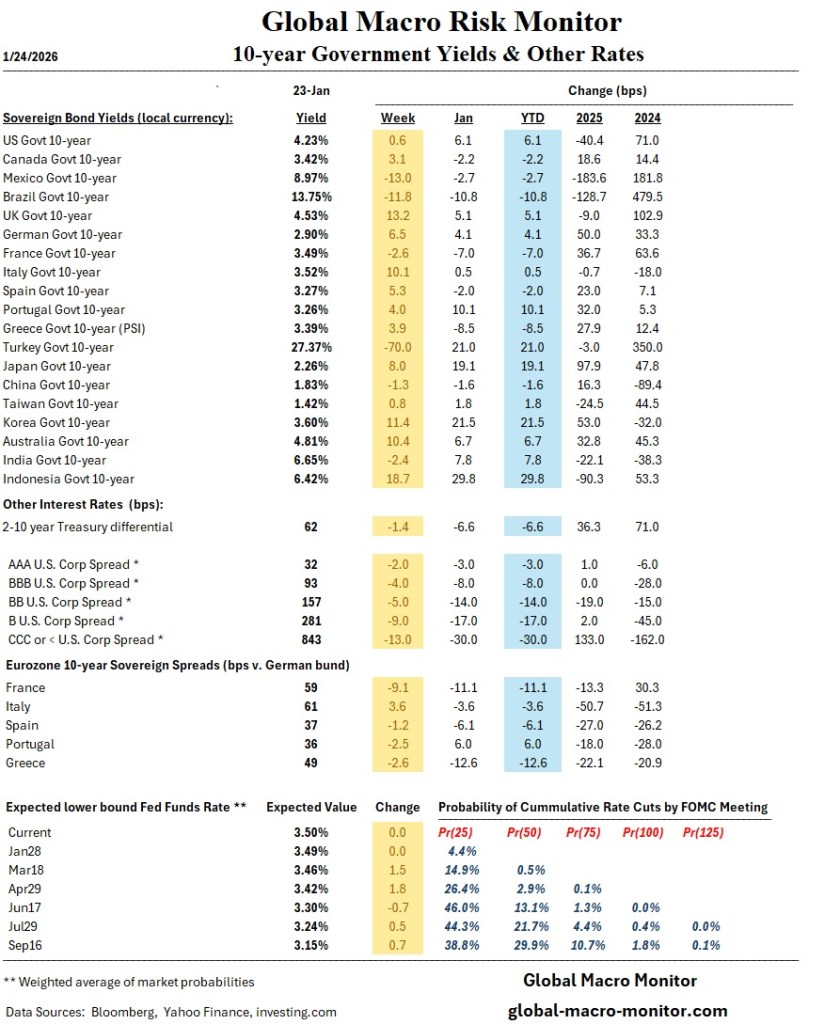

Beneath the surface, financial conditions remain extremely loose (see the NFCI in our Commodities Table), but cracks are emerging. The U.S. yield curve steepened sharply, with the 2s–10s spread widening to ~70 bps, signaling improving growth expectations but also greater sensitivity to inflation and policy risk. Equity leadership narrowed, small caps pulled back, and volatility rose into the month-end.

Globally, however, performance outside the U.S. was exceptional, led overwhelmingly by Asia. South Korea stood out as the best-performing equity market in the world, driven by massive capital inflows, AI-led earnings momentum, and its growing role as a global trading and technology hub. Taiwan and Brazil also posted outsized January gains, reinforcing the theme that global leadership is rotating away from the U.S. margin.

The most acute near-term risk comes from crypto markets, where Bitcoin fell nearly 10% over the weekend, confirming aggressive deleveraging at the far end of the risk spectrum. Historically, such moves tend to spill over into equities, particularly high-beta, small-cap, and speculative segments, raising the probability of a risk-off tone early in the week

Regional Market Performance Highlights

United States

Asia (Clear Global Leader)

South Korea – Exceptional Outperformance

Taiwan

Japan

Europe

Latin America

Commodities & Crypto

Week Ahead: Risk Catalysts & Market Focus

Bottom line:

Markets enter the new week with strong global performance contrasts but deteriorating risk signals. Asia—especially Korea—remains the standout structural winner, but the crypto-led deleveraging shock materially raises near-term downside risk. Expect higher volatility, sharper dispersion, and a defensive bias until risk appetite stabilizes.

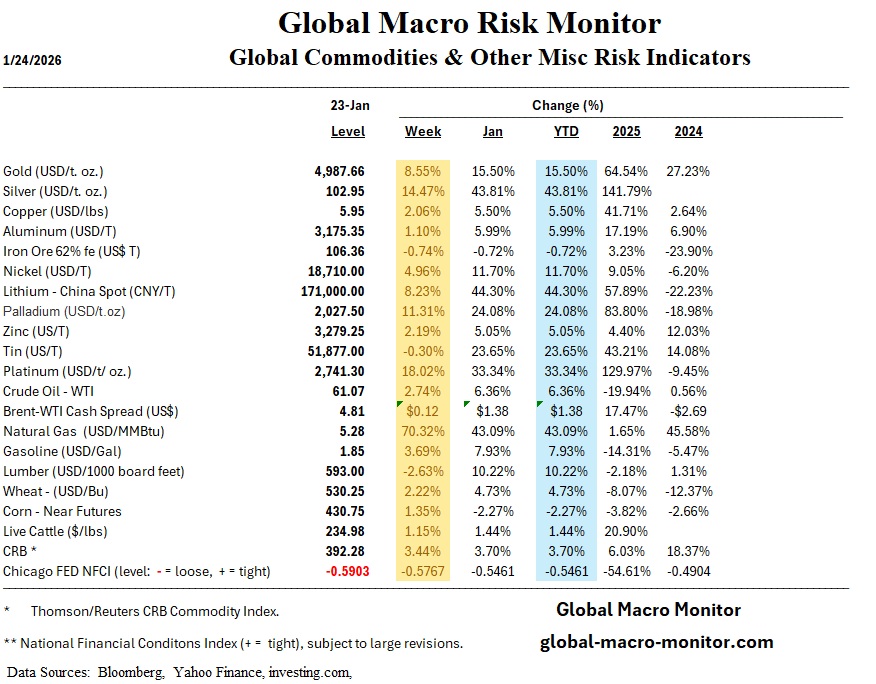

This week’s global financial landscape was characterized by intense volatility and a continued and significant rotation across asset classes. A prominent trend is the marked shift toward small-cap stocks, as investors move away from the high-valuation mega-cap technology sector that dominated the previous year. This rotation has been underscored by the notable underperformance of technology stocks in January, with investors largely shying away from the sector amid concerns over AI-related valuations and higher interest rates. Conversely, the commodities market witnessed an extraordinary surge. Silver prices have skyrocketed, rising by over 44% this month alone, while gold has also shown strong gains. Energy markets were equally explosive, with natural gas prices spiking more than 70% this week, driven primarily by a severe cold spell.

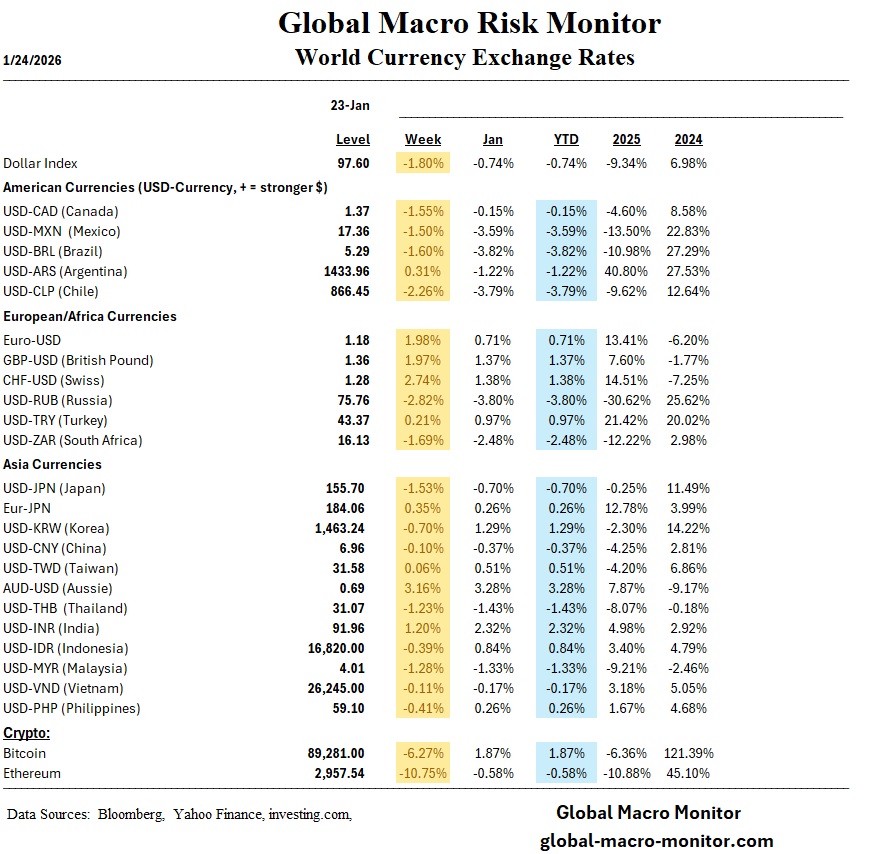

In international markets, Asian equities—particularly in Korea—continued their impressive trajectory, with Korean markets up 18% in January following a massive rally in 2025. This occurs against the backdrop of a sharply declining U.S. dollar, with the DXY index dropping 1.80% over the week. While U.S. GDP growth was revised higher to 4.4%, persistent inflation and geopolitical tensions, specifically regarding trade threats, continue to weigh on market sentiment.

Summary

Regional Economic Insights

Inflation: CPI-PPI Divergence

Valuations and the “Low Fuel Tank” Risk

Precious Metals: Gold & Silver

Energy: Natural Gas

Energy: Crude Oil

Industrial Commodities & Agriculture

Week Ahead

The upcoming week is expected to be marked by “Higher Volatility” as investors navigate a dense schedule of high-impact earnings from the technology sector and a pivotal Federal Reserve meeting.

Major Economic Indicators

Key Earnings Releases

Global Events & Factors

In celebration of MLK Weekend, we are reposting a repost of a repost of post in honor of Dr. King, one of our most outstanding Americans, a true patriot, and a modern-day saint. Hard to believe it’s been thirty years.

During my Lehman days as a young bond strategist, the firm’s research group would do a January roadshow in many of America’s major cities to present our ideas to institutional investors. One particular year, we were in Atlanta at end of the week and scheduled for another “greatest show on earth” in Chicago the following Tuesday.

A Weekend In The Peachtree Hyatt

Rather than flying home to New York, I decided to stay over in Atlanta and migrate north on Monday evening. It was MLK weekend, and I wanted to attend services at the Ebenezer Baptist Church, where Martin Luther King, Jr. was baptized as a child and gave his first sermon. If my memory is correct, I believe his father also pastored the church. His mother was shot and killed while she played the organ in that church in 1974.

Dr. King’s tomb is located just outside the side door of the church in the middle of a reflecting pool.

Three Memories Of Ebenezer

I recall my three main takeaways from that Sunday morning.

First, I was maybe one of ten whites out of 600-700 people sitting in the pews. Sadly, as Dr. King said almost 60 years ago.

I think it is one of the tragedies of our nation, one of the shameful tragedies, at 11 o’clock on Sunday morning is one of the most segregated hours, if not the most segregated hour in Christian America. – MLK, Jr Meet the Press, April 17, 1960

Nevertheless, I felt incredibly welcome and never — not for one nanosecond — was conscious about such a silly thing as the difference in the color of my skin. During the greeting time, the Ebenezers made me feel so welcome and a part of their family.

Second, not to contradict Dr. King, but I believe the service started at 9:30 AM and went to almost 1:00 PM! Maybe it was an exceptional MLK weekend service. The pastors in the primarily white churches I have attended have trouble keeping the congregation’s attention for more than 20 minutes.

Third, the sermon differed entirely from those I had experienced in middle-class white churches. Less doctrine, though similar theology, and more authentic life experiences. The struggles of raising children in poverty. Grandparents raising their grandchildren. Troubles with children with drug addiction. The struggles of being black in white America, all of the life struggles which are just as ubiquitous in the white and all communities of color. No pretense of sinless and perfect, no holier than thou vibe, judgment, condemnation, guilt, or shaming. All love, compassion, kindness, and forgiveness. Just like the real Jesus.

Also, the sharing of the same joys and blessings. New babies, college graduates, marriages, medical recoveries, and others.

“Daddy King” was referred to several times.

It truly echoed the genius and saintliness of Dr. King.

I walked away convinced the Church for the African-American community was much more — that is a considerable part of their life — than what I had experienced in white evangelical America.

Yes, maybe some of us attend more than just Sunday services, but many, such as yours truly, often do so with the dubious motive of seeking the blessings of personal peace and personal prosperity. The community of the Church, as it is for the African-Americans, though not always, is secondary.

I spent the next day, Martin Luther King Jr Day across the street at the King Center.

More Empathy, Less “Being A Dick“

What great memories from that unforgettable MLK weekend.

I grew up in the middle-class white suburbs of Los Angeles, attending an all-white high school. Fortunately, I had a father who was politically left of the salad fork (out of a rebellion, I became a conservative in college), and also spent my first 25 years playing sports, fighting in the baseball trenches with, pulling for, breaking bread, and downing brewskies with my teammates of color; or as I grew to learn colorless.

I am very thankful for those experiences. It helped me integrate into and see the real greatness of America.

I feel sad for my many brothers and sisters who have not had the same privilege and are stuck still watching black and white television, unable or unwilling to embrace and enjoy the tremendous diversity of this great country.

Ditto for the similar ignoramuses from other races and ethnic groups.

I can’t imagine eating steak and potatoes every day and every night.

Ignorance And Racism Know No Boundaries

Let me finish by qualifying all of the above.

Racism is a prominent feature of so many human societies that some evolutionary psychologists have concluded it is “natural” or “innate.” We don’t know about that but are sure it is not just a “white thing,” a “black thing, or a “brown thing,” etc.

I have shared the story of my brother who was murdered by an undocumented worker, who stated, after stabbing him, “all anglos need to be exterminated.” This sociopathic asshole killed my brother not because he was brown or undocumented but because he was one sick and crazy mother f$@ker.

Now, more than ever, it is time to commit to expanding our menu. Let’s make it a point to understand and enjoy the perspectives and cultures of all the different races and ethnic groups.

Allegorically and literally, let’s eat more balaedas, falafel, babaghanoush, borscht, moussaka, and bouilli, among others. The steak and potatoes will taste sooo much better.

Sorry to end on a note that violates the spirit of Dr. King but I can’t help myself.

Any white man (probably less so for a white woman) who thinks he knows what it is like to be an African-American growing up and living in America, has his head…well…you know where.

Bring it on!