The juxtaposition is stark. As Bloomberg reports Wall Street is pouring billions into marinas for ever-larger yachts, the BBC reminds us that U.S. homelessness reached a record high in 2024.

Winners and Losers of Free Trade

This contrast, in part, encapsulates the uneven dividends of globalization and free trade. The opening of global markets allowed firms to slash costs by offshoring production, boost profit margins, fuel stock prices, and funnel massive wealth to shareholders. At the same time, the income effect of free trade (purchasing power expansion) increased demand for domestic goods and services, creating millions of jobs and enriching many American workers. Moreover, every American consumer benefits from a broader selection of goods and services at lower prices.

Yet a minority, those displaced by trade and globalization, paid a steep price. Deindustrialized regions have slid into long-term decline. Today’s backlash is not a rejection of global integration itself, in our opinion, but a verdict on decades of policy failure. Trade Adjustment Assistance (TAA) to those displaced has been, at best, minimal, while retraining programs are underfunded, poorly targeted, and largely ignored by policymakers.

White House Interview

Late in President Reagan’s tenure, I interviewed for a junior economist position at the Council of Economic Advisers (CEA). The role was tailored for Ph.D. students who had completed their comprehensive exams and were beginning their dissertations. The CEA was stacked with free marketers, fresh off the Milton Friedman assembly line, preaching the gospel of free markets, mostly from their perch at the University of Chicago.

Trade Adjustment Assistance (TAA)

At the time, Congress was floating a trade adjustment bill to cushion the damage of a surging dollar and a flood of imports. Its centerpiece? A one-time $100,000 check ($301k in 2025 dollars) for laid-off steelworkers. The idea was simple: buy off the casualties of free trade and hope they retrain quietly.

The first question of the day-long interview was, “Gregor, what do you think of a bill writing a $100k check to displaced steel workers?” I answered earnestly, “We should focus on retraining and skills development.” The reply was swift: “That’s what the Democrats think.” The Chicago doctrine held that the market, not government, should determine how and where displaced workers retrain. I didn’t get the job.

Paying the Piper

That bill never passed. But at least at the time, free traders acknowledged the collateral damage of globalization (we use “free trade” and “globalization” interchangeably). Today, after decades of neglecting those left behind, the political cost has finally come due.

Globalization has generated massive wealth, created millions of new jobs, and fueled innovation. But we failed badly at cushioning the losses. Redistributing even a small share of the gains from global markets to those displaced would have been, and still remains, the smarter path forward.

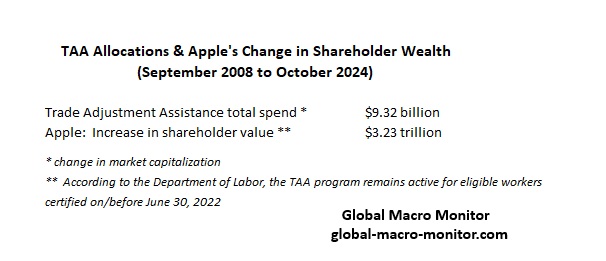

TAA Allocation vs. Apple’s Market Capitalization

Few juxtapositions better capture the myopia and unfairness of our trade policy than the gap between what we’ve spent on displaced workers and what Apple shareholders have gained. Since 2008, the U.S. government has allocated just over $9 billion through Trade Adjustment Assistance (TAA) to support workers who lost or were threatened with losing their jobs due to foreign trade. In that same period, Apple’s shareholders have seen their wealth grow by more than $3 trillion.

Apple Inc. has expertly leveraged free trade and globalization to build an ultra-efficient supply chain, sourcing components from over 40 countries and assembling products in lower-cost regions like China, driving gross margins consistently above 40%. By tapping into global consumer markets, especially in Asia and Europe, Apple now generates over 60% of its revenue internationally, propelling its market capitalization past $3 trillion and enriching its investors.

What’s often overlooked is that this shareholder wealth has, in part, been built on the backs of displaced workers. Surely, a small fraction of those gains could—and should—be reinvested in the people and communities left behind.

Social Infrastructure Investment

Apple shareholders are now feeling the political backlash of globalization, as an Administration, claiming to represent displaced and marginalized workers, pressures the company to onshore operations in ways that defy economic logic. We argue that investing in social infrastructure, whether through Trade Adjustment Assistance or another targeted mechanism to cushion the impact of free trade, would have left Apple, its shareholders, and the nation far better off in the long run.

AI Cometh

Stay tuned because our massive wealth gap and the uneven distribution of income are about to be supercharged by the coming AI revolution.

Universal basic income (UBI) is the new $100k check for steel workers, folks.

Let’s hope we don’t fumble again, because AI is coming for jobs, big time.

Appendix

Trade Adjustment Assistance

The map below visualizes over a decade of federal Trade Adjustment Assistance (TAA) funding, showcasing how different states have absorbed the brunt of economic displacement from globalization and trade liberalization. States in the industrial Midwest and parts of the South received disproportionately high allocations, reflecting the decline of manufacturing sectors in those regions.

Conversely, lower funding levels in parts of the West and Northeast may indicate either less industrial exposure or underutilization of the program. While TAA has been a central pillar of U.S. trade policy aimed at helping displaced workers retrain and reenter the workforce, this map underscores the persistent regional imbalances in economic vulnerability and the ongoing need for targeted adjustment strategies as new forces like AI and reshoring reshape the labor landscape.

To provide better context, we divided each state’s total Trade Adjustment Assistance (TAA) spending by the size of its labor force, calculating the TAA dollars spent per worker. This normalization reveals sharp disparities—for instance, West Virginia received $168 per worker, while Nevada received just $4.