Here’s a heads up for Friday’s employment number before we hit the beach: 1) Nonfarm payroll expectations; 2) today’s ADP release, and 3) commentary by Mark Zandi.

Here’s a heads up for Friday’s employment number before we hit the beach: 1) Nonfarm payroll expectations; 2) today’s ADP release, and 3) commentary by Mark Zandi.

QOTD: Quote of the day

Call me a traditionalist, a conservative, or what you will but I’m with Erma on this one.

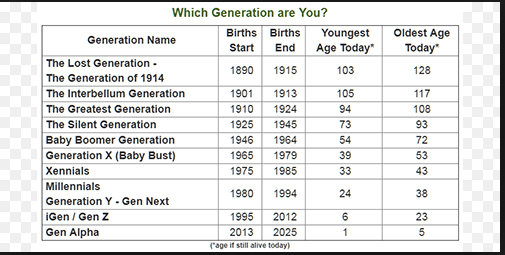

Don’t know if you caught the Democratic debate the other night, which featured Bernie and Joe, who could be the grandfathers of some of the younger candidates that were on stage, but it also confirmed the arrival of what we have been writing about for years, the Clash of Generations.

Congressman Eric Swalwell was one the young Democrats on stage with Bernie and Uncle Joe last week.

If you missed this Atlantic piece, it is definitely a must-read,

Money Quotes:

In a variety of different areas, the Baby Boom generation created, advanced, or preserved policies that made American institutions less dynamic. In a recent report for the American Enterprise Institute, I looked at issues including housing, work rules, higher education, law enforcement, and public budgeting, and found a consistent pattern: The political ascendancy of the Boomers brought with it tightening control and stricter regulation, making it harder to succeed in America. This lack of dynamism largely hasn’t hurt Boomers, but the mistakes of the past are fast becoming a crisis for younger Americans.

…Boomers didn’t only make rules that nudge young people out of homeownership. They also made new rules restricting young people’s employment. Laws and rules requiring workers to have special licenses, degrees, or certificates to work have proliferated over the past few decades. And while much of this rise came before Boomers were politically active, instead of reversing the trend, they extended it.

...The most glaring example of this growth in regulation and control is also the easiest one to pin on Baby Boomers: the incredible rise in incarceration rates. Even though murder rates are today at the same levels they were in the 1950s, the imprisoned share of the population is higher in America than in any country other than North Korea. We imprison a larger share of the population than authoritarian countries such as Turkmenistan and China.

…Even young Americans today who are free from prison are nonetheless in bondage to debt—sometimes their own debt, in the form of rapidly growing student loans or personal and credit-card loans. But on a larger scale, the problems of entitlements, pensions, Social Security, Medicare, and federal, state, and local debt are becoming more severe all the time. Already, in places such as Detroit, Illinois, and Puerto Rico, where political rules make flexible solutions hard and the population is aging very quickly, massive debt restructurings loom large. But around the country, the pressures of long-term obligations will grow.

…Making these payments will require fiscal austerity, through either higher taxes or lower alternative spending. Younger Americans will bear the burdens of the Baby Boomer generation, whether in smaller take-home pay or more potholes and worse schools.

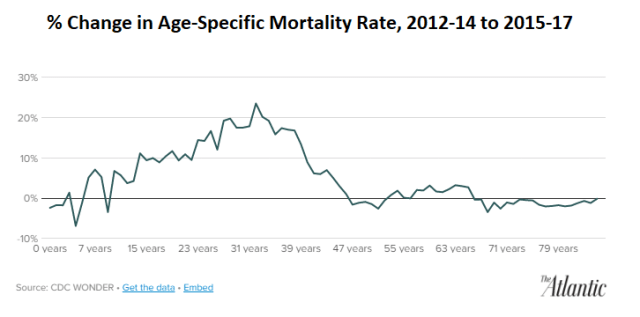

Furthermore, the basic demographic balance sheet is getting worse all the time, increasing the relative burden on young people. Working-age Americans are dying off in alarming numbers.

[Take a minute and study the above chart. Probably some of the saddest data I have ever seen. These data are often overlooked and ignored from the comfort of the gated retirement communities.]

…The odds of a 32-year-old dying have risen by 24 percent in the past five years, even as death rates among older Americans are about stable. Baby Boomers are living longer even as the workers who pay for their pensions are dying from an epidemic of drug overdose, suicide, car accidents, and violence.

…If leaders in business, education, and politics want to solve these problems, they can. Whether the gerontocracy in charge today wants solutions may be another question altogether. – The Atlantic, June 24th

Our Warning In July 2011

We posted the following in The Clash of Generations way back in July 2011,

How long before the young realize they’ve had their future stolen from them by the baby boomers? The answer to this question will determine your defined benefit pension, social security and medicare benefits. Reality meets [the boomers] at sunset. – GMM, July 2011

Now. They are woke.

We also exhorted boomers in an even earlier post to, as a metaphor, give up their country clubs for muni golf courses in order to free up resources and give the young a fighting chance. It is a social investment for the boomers, after all, the younger generations will determine the fate of their underfunded pensions, social security, and medicare programs

Monetization Coming

We do think the young will choose monetization to finance the shortfalls and debts the boomers have bequeathed them as the case gains political credibility through the rise of Modern Monetary Theory.

A form of a “People’s QE” is inevitable, in our opinion, and that is why we totally disagree about the end game with the deflationistas, who, suffer from recency bias and have probably never spent a day, much less a week, in an economy suffering from hyperinflation.

Zero interest rates for an extended period (as in five and ten-year slogs, ala Japan)? Not U.S. market rates, folks, if there are any remaining, which is questionable, we do concede.

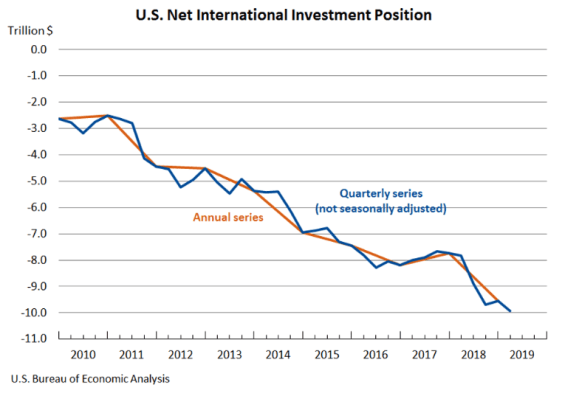

America is not a net saver, has been dependent on foreign savings to finance is public and private deficits for years, and its net international investment position (NIIP) has crossed over the $10 trillion deficit mark in Q2 2019.

This compares to NIIP surpluses in Japan and Germany of around $4 and $2 trillion, respectively.

Contemplate for a moment the long-term consequences of the above chart for, say, the exchange value of the U.S. dollar.

Hayek May Be Prescient Yet

Frederick Hayek understood demographics and the aging population would be at the mercy and charity of the young,

In 1960, Friedrich Hayek predicted in The Constitution of Liberty “that most of those who will retire at the end of the century will be dependent on the charity of the younger generation. And ultimately not morals but the fact that the young supply the police and the army will decide the issue: concentration camps for the aged unable to maintain themselves are likely to be the fate of an old generation whose income is entirely dependent on coercing the young.” It hasn’t turned out that way at all—a salutary warning that it is much easier to identify generational conflicts of interest than to anticipate correctly the political form they will take. – The Coming Generation War, The Atlantic

Just some more potential political conflict to stuff in your pipe and smoke, folks.

Not sure if the younger gens will wrestle the power torch from the gerontocracy in 2020 but they will someday.

Boomers best be kind to the Millenials, X, Y, Z, and Alpha generations.

They are woke, not happy, and left of the salad fork.

SBNN = Song Before Night Night

Must admit this is the only BMW I have ever owned. As in (B)ob (M)arley & the (W)ailers.

When I lived on the UYupper West Side (are there still Yuppies?) in a different era, my neighbors said their BMW was an acronym for (B)reak (M)y (W)indow.

Get Up, Stand Up, folks.

Hat Tip: KD

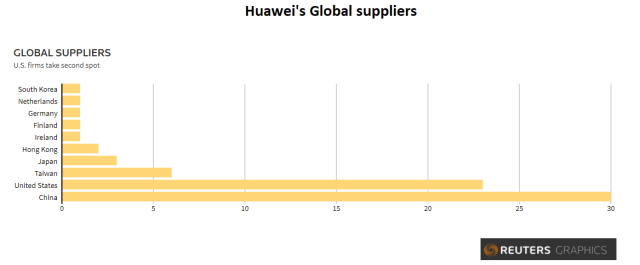

Here are some of the top American suppliers to Huawei that should Rock the Casbah in Monday trading after Trump’s rethink the Chinese company is a national security risk.

It’s still not clear what the Trump-Xi Osaka handshake and agreement mean, however. And it appears the walk back is already beginning as the administration is taking on pipe from both the left and the right for its apparent cave to get the Chinese back to the table.

White House economic adviser Larry Kudlow says U.S. President Donald Trump won’t back off national security concerns after agreeing to allow U.S. companies to sell some components to Chinese telecommunications giant Huawei.

Kudlow told Fox News Sunday and CBS’ Face the Nation that Huawei will remain on an American blacklist as a potential security threat.

He said any additional U.S. licensing “will be for what we call general merchandise, not national security sensitive,” such as chips and software generally available around the world.

Some Republican senators criticized Trump’s announcement Saturday, describing the company as a threat to U.S. national security. In a tweet, Sen. Marco Rubio of Florida called the move a “catastrophic mistake.” – CBC

Equivocal Tweets Coupled With The Ambiguity of Stock Values

Tough trading with an Equivocator In Chief tweeting ambiguous and cryptic messages all with the goal to goose the stock market, which, by its very nature, has equivocal and ambiguous valuations. See our must-read and timeless Ambiguity of Stock Value post.

The Ambiguity of Stock Value

Stock prices are likely to be among the prices that are relatively vulnerable to purely social movements because there is no accepted theory by which to understand the worth of stocks….investors have no model or at best a very incomplete model of the behavior of prices, dividend, or earnings, of speculative assets. – GMM, Dec. 2010

The default is always markets do like to go up.

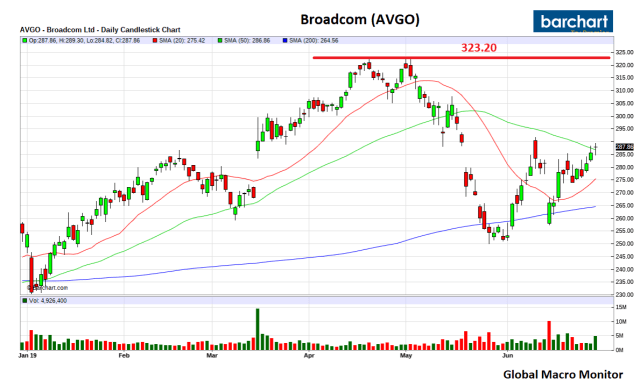

Watching Broadcom (AVGO)

Broadcom is the large-cap ($115 billion) stock we will be monitoring closely to see if the market really believes the G20 Osaka Sino-American handshake on Huawei and by extension the credibility of a potential U.S-China Trade deal. A close above its all-time at 323.20, 12.28 percent from Friday’s close, would be nice confirmation the markets believe.

About to get even more interesting. Stay tuned

Broadcom The Stock To Watch

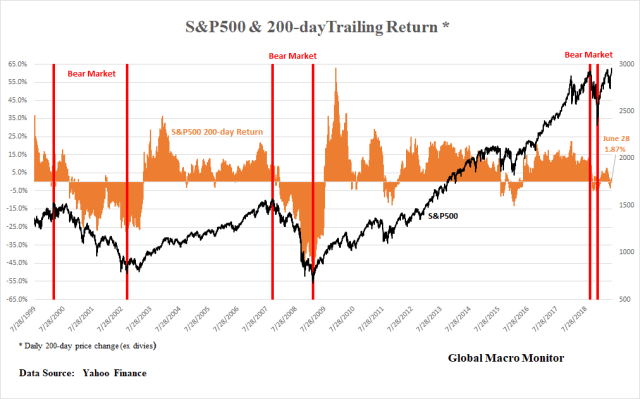

The S&P 200-day rolling return is an interesting chart but not much in the way of signals with the exception to illustrate the S&P500 does not fall out of the sky and enter bear markets after a strong 200-day run.

Bear Markets

Bear markets usually begin with a topping process, after all, markets are cold-blooded beasts and adapt and rationalize their bullish biases to negative news and deteriorating conditions. Until they don’t.

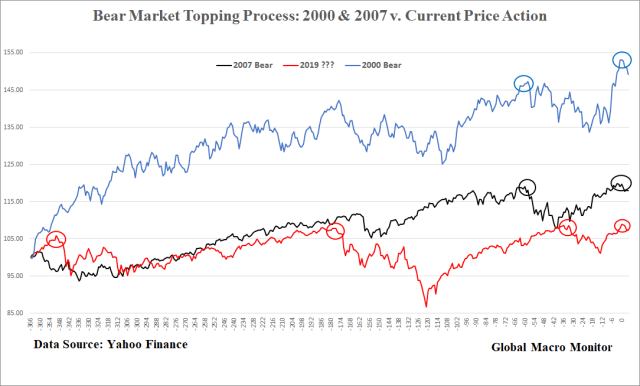

Inertia is innate in the stock market, in part due to Wall Street’s and the buy side myopic focus on the year-end bonus, but if equities can’t break out after making several local tops (see the second chart), caveat emptor and be warned something is rotten in the state of Denmark.

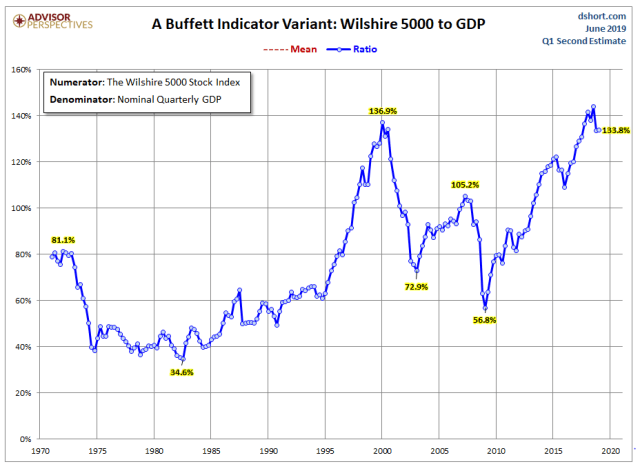

We remain medium-term bearish on U.S. stocks based mainly on macro valuations as the charts below illustrate there is not much room for stocks to run from here. Unless “this time is different” and trees stocks don’t do grow to the sky.

Surely, the S&P500 will rally tomorrow on the announcement of the restart of China trade talks. Is it sustainable?

Will the Trump concession on Huawei to get the Chinese back to the table, which is very bullish for the company’s American suppliers, soon be offset with concerns the Fed may now rescind some of its dovishness?

In our June 26th post, we stated,

Our best guess, however, is given President Trump’s low approval ratings moving into an election year, he is highly motivated to kraft some sort of truce or Potemkin China trade, which will be sold as the “greatest deal ever,” to give the market one last boost.

An S&P top of around 3025-3060 would repeat the topping zip codes of past history. — GMM, June 26th

Key Levels

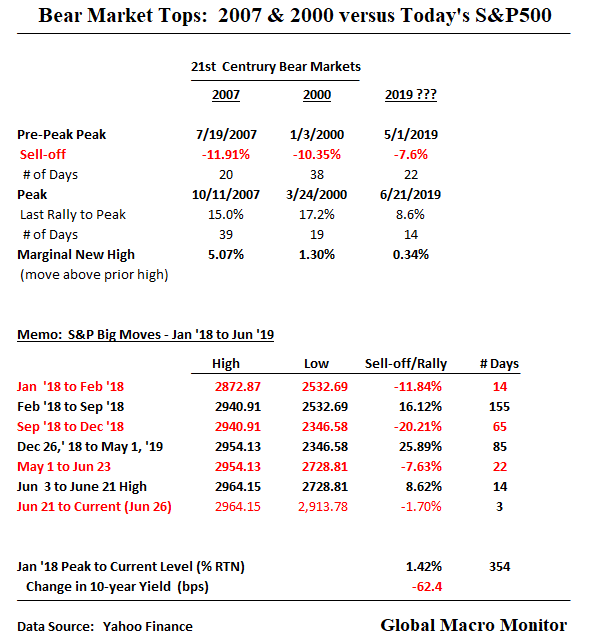

Given the topping behavior of the 2000 and 2007 bears (the Sep’18 bear market was short and barely cleared the bar, down 20.2 percent peak to trough), an S&P top in the range of 3000-3100 would be consistent with recent history and the nominal highs made in 2000 and 2007. These levels are in the range of around 1-5 percent above the May 1st and June 21st high.

Until the S&P clears 3115, we will maintain our medium-term view that investors should be reducing risk by selling into strength. If the index does clear the key level, it will be time to suspend disbelief and move to the Venezuelan model of stock valuation.

A bear market could also ensue with time. Stocks could churn and burn around these levels for years. As of Friday’s close, the S&P500 is only 2.4 percent above its January 2018 local peak.

In the short-term, we have relatively high conviction traders will remain lathered up on the prospects — emphasis on prospects —of a China trade deal and Fed easing. We don’t and won’t fight that. No strategic shorts put out until the mid-3000 level unless the markets show clear signs of breaking.

Scalping the market with short-term buying and selling is a different story. That’s getting harder and harder with the rise of Auto & Algos (AA), however.

In the long-run, we shorts are all dead.

As always, we reserve the right to be wrong.

This post seems more relevant than ever as many believe the initial conditions of today are very similar to those of the Spring and Summer of 1914.

One wrong turn, one small change in initial conditions can change the course of history enormously.

Originally June 27, 2017

The butterfly effect is the concept that small causes can have large effects. Initially, it was used with weather prediction but later the term became a metaphor used in and out of science.

In chaos theory, the butterfly effect is the sensitive dependence on initial conditions in which a small change in one state of a deterministic nonlinear system can result in large differences in a later state. The name, coined by Edward Lorenz for the effect which had been known long before, is derived from the metaphorical example of the details of a tornado (exact time of formation, exact path taken) being influenced by minor perturbations such as the flapping of the wings of a distant butterfly several weeks earlier. Lorenz discovered the effect when he observed that runs of his weather model with initial condition data that was rounded in a seemingly inconsequential manner would fail to reproduce the results of runs with the unrounded initial condition data. A very small change in initial conditions had created a significantly different outcome. — Wikipedia

On this day in history, June 28, 1914, 105 years ago to the day, the driver for Archduke Franz Ferdinand, nephew of Emperor Franz Josef and heir to the Austro-Hungarian Empire, made a wrong turn onto Franzjosefstrasse in Sarajevo.

Just hours earlier, Franz Ferdinand narrowly escaped assassination as a bomb bounced off his car as he and his wife, Sophie, traveled from the local train station to the city’s civic city. Rather than making the wrong turn onto Franz Josef Street, the car was supposed to travel on the river expressway allowing for a higher speed ensuring the Archduke’s safety.

Yet, somehow, the driver made a fatal mistake and tuned onto Franz Josef Street.

The 19-year-old anarchist and Serbian nationalist, Gavrilo Princip, who was part of a small group who had traveled to Sarajevo to kill the Archduke, and a cohort of the earlier bomb thrower, was on his way home thinking the plot had failed. He stopped for a sandwich on Franz Josef Street.

Seeing the driver of the Archduke’s car trying to back up onto the river expressway, Princip seized the opportunity and fired into the car, shooting Franz Ferdinand and Sophie at point-blank range, killing both.

That small wrong turn, a minor perturbation to the initial conditions, or deviation from the original plan, set off the chain events that led to World War I.

Stumbling Into The Great War

Fearing Russian support of Serbia, Franz Josef would not retaliate by invading Serbia unless he was assured he had the backing of Germany. It is uncertain as to whether the Kaiser gave Franz Josef Germany’s unequivocal support. Russia, fearing Germany would intervene, mobilized its troops forcing Germany’s hand.

The great European powers thus stumbled into a war they didn’t want through complicated entanglements and alliances, and miscalculation. Russia backing Serbia; France aligned with Russia, Germany backing the Austro-Hungarian Empire; and Britain, who really didn’t have a dog in the fight except for her economic interests, aligned with France and Russia.

Later the U.S. would enter the war due to Germany’s unrestricted submarine warfare threatening American merchant ships and the Kaiser floating the idea of an alliance with Mexico in the famous Zimmerman Telegram, which was intercepted by the British.

Of course, some will argue that the Great War in Europe was inevitable

The great Prussian statesman Otto von Bismarck, the man most responsible for the unification of Germany in 1871, was quoted as saying at the end of his life that “One day the great European War will come out of some damned foolish thing in the Balkans.” It went as he predicted. – History.com

Nevertheless, maybe the course of history would have been different if not for that wrong turn on June 28, 1914, which created the humongous butterfly effect, which we still are experiencing the consequence to this very day.

The botched Treaty of Versailles sowed the seeds the for World II. The War contributed to the Russian revolution and eventually the Cold War. The redrawing of borders in the Middle East after the Great War created the conditions for the instability and breakdown into tribalism the region still experiences today.

A map marked with crude chinagraph-pencil in the second decade of the 20th Century shows the ambition – and folly – of the 100-year old British-French plan that helped create the modern-day Middle East.

Straight lines make uncomplicated borders. Most probably that was the reason why most of the lines that Mark Sykes, representing the British government, and Francois Georges-Picot, from the French government, agreed upon in 1916 were straight ones. — BBC News

If Franz Ferdinand had not been murdered on this day in history, that conflict between the Serbs and the Austro-Hungarian Empire may have been contained to just the Balkans. Maybe.

The butterfly effect. Think of how many small events, decisions, mistakes, one small turn, or “minor perturbation” in plans have had enormous consequences in your own personal life.

Update: It is the rising geopolitical risks, rapidly shifting global economic tectonic plates, and collapsing post-war global order that keeps us up at night and pose the greatest threat to the world economy and stock markets. We believe the probability of a major bear market — down 40 percent plus — in the next 6-12 months is much, much higher and a galaxy away from most traders and investors’ radars.

Technically, no.

Spiritually? Nor sure, but definitely, there’s is something happening here. What is ain’t exactly clear.

S&P Flat For Past 17 Months

Even with all the Strum und Drang since the massive volatility shock of January 2018 — which includes a technical bear market > 20 percent sell-off from September 21st to December 26th and a ripping Fed-led 26 percent rally from December 26th to May 1st — the S&P is up only 1.52 percent. Stunning and exhausting.

It feels as if we have traveled Around the World in 80 354 Trading Days and yet have gone absolutely nowhere.

Bull Market Tops

We do feel stocks are topping and are in, or about to enter a major bear market. For long-term investors, rarely does it pay to try and time a bear market but given the rising geopolitical and economic risks, we believe this is one of those times.

Stocks do like to go up,

…the Dow has generated positive returns 68 percent of the years since 1921, and the S&P more than 72 percent since 1951. – GMM, March 22nd

Yet, there have been two brutal bear markets already in this young century, which took the S&P500 down 51 percent from March 2000 to October 2002, and 58 percent from October 2007 to March 2009.

Topping Process

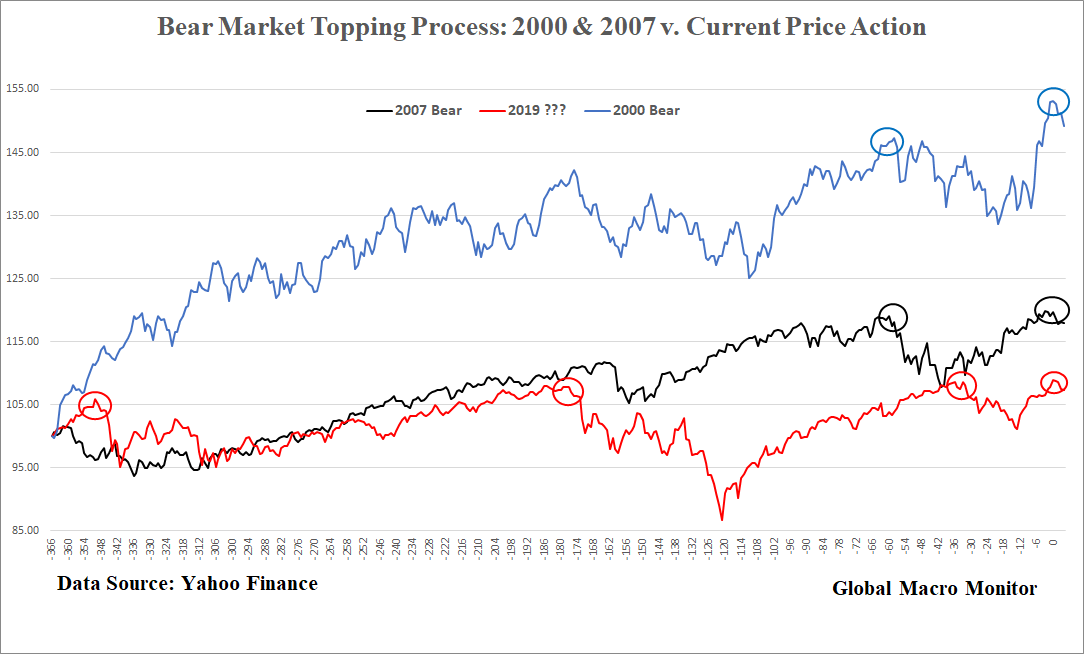

In both bears, the S&P500 made an initial top, sold off 10-12 percent over 20-40 trading days, experienced a reflex rally of 15-17 percent over 20-40 days, before rolling over for good. The data in the table and chart reflect the topping process of these markets compared with the price action of the current S&P500.

The chart illustrates the two bear markets 366 days prior to making their respective tops and then 4 days after. It overlays the current S&P (red line), which topped on June 21st.

Nobody knows if June 21st was THE top, which would be 3.1 percent above the first made on January 26, 2018. Our best guess, however, is given President Trump’s low approval ratings moving into an election year, he is highly motivated to kraft some sort of truce or Potemkin China trade, which will be sold as the “greatest deal ever,” to give the market one last boost.

An S&P top of around 3025-3060 would repeat the topping zip codes of past history.

Basing Or Freebasing?

A bear market could also unfold through time rather than price, where the index does nothing for years. If that’s the case, we are already 1 1/2 years in.

Conversely, the S&P could be just basing, working off a 10-year overbought condition and preparing for another big leg higher, boosted by more Fed liquidity.

Au contraire, comrades. It is our view, and we could be and often are wrong, the markets are freebasing on the expected Fed crack before overdosing and rolling over.

Watch The Key Levels

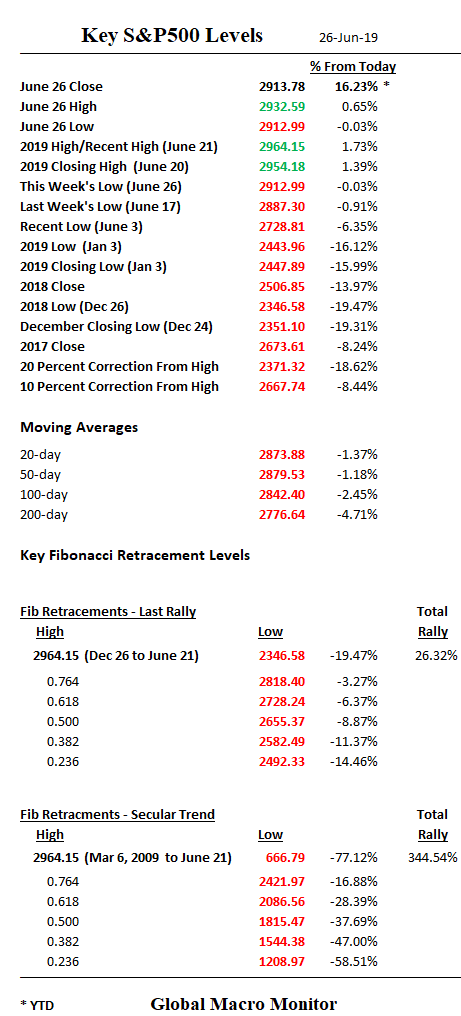

Only the market will reveal its true status so it’s important to monitor key levels. Let’s start with 2964.15, the all-time high, on the upside, which could easily be taken out if Trump and Xi kiss and make up in Osaka over the next few days.

On the downside, the 50-day and 20-day beckon in the 2970 range, which will be taken out faster than a hot knife through butter if either Trump or Xi pack it up and come home with no real resolution.

Pain Trade

Or, the market further lathers itself up on, say, a bad trade tape bomb out of Osaka, believing extra goodies will be served up by the Fed. Who said this business is easy?

Remember, folks, predicting short-term stock moves is really a mug’s game and only profitable for professional scalpers.

Don’t talk to me about snowflakes. I have one daughter in college and one about to enter and we have had some very interesting and, let’s just say loud, discussions about free speech, triggers, snowflakes, and safe spaces. On one occasion, they became very upset that I took the position that the political shock-jock, Ann Coulter, who, by the way, is antithetical to my own political views and I find repulsive, should be able to speak on the UC Berkeley campus. In fact, I was ready to drive down to the campus and protest for her right to speak.

I tried to explain to my daughters if only popular ideas were protected, there would be no need for the First Amendment. If you do not defend the free speech rights of the unpopular, even if their views are repulsive to you, our liberty will never be secure. My experience is that many university students have trouble grasping this concept. It is not to say they don’t have the right to not invite someone to speak but to block a speaker, which one group has invited? Come on, man!

Ironically, when I mentioned to the youngest how much we paid in taxes during the bountiful years, she was outraged. Maybe today’s high schoolers are sensible fiscal conservatives?

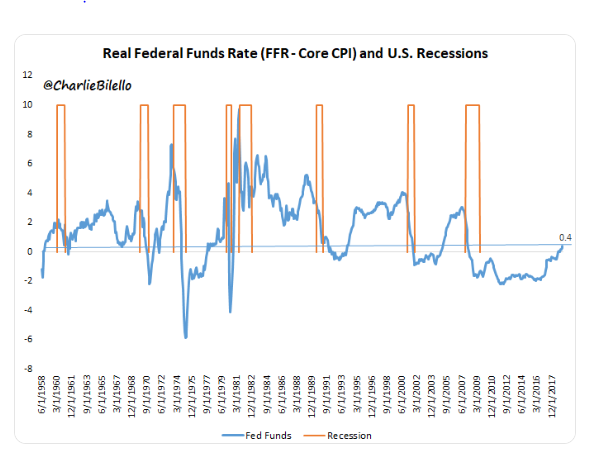

Lowest Terminal Real Fed Funds Rate Ever!

Moving on, Charlie B. throws together a nice chart and also notes,

The REAL Fed Funds Rate (Fed Funds minus inflation) stands at 0.4%, which, if the Fed is done hiking (market saying 100% probability of a cut next month), would be the lowest terminal rate of any expansion ever. Monetary policy remains extraordinarily easy. – Charlie Bilello

Now, do you still wonder why gold is having a Ralph Kramden moment? “One of these days, you’re going to the moon, Alice!”

Q: How robust is an economy or stock market that freaks out over a barely positive real Fed Funds rate, is triggered if the word “patient” is not removed from an FOMC statement, and considers a less than super-dovish Fed as a microaggression?

A: A “snowflake” economy and market.

The market thought it had found its safe space with the dovish Fed and three rate cuts baked in. We seriously doubt it and are prepared for a macroagression.

Coming Up Next: The Trump Economy Scorecard

We have been very busy working on data to provide you with a full and comprehensive scorecard of the Trump economy as the presidential campaign gets underway and the B.S. starts to fly in earnest, on both sides. It should be out in the next few days so watch for it.

Here is a little appetizer.

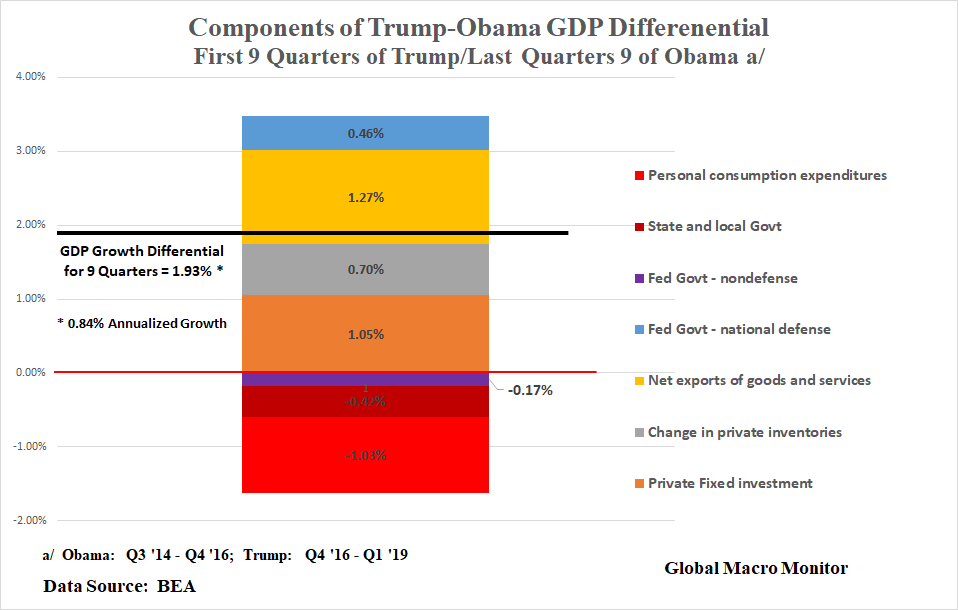

Because the current POTUS is always comparing his economy with that of his predecessors, we juxtapose several economic indicators during his first 2 1/2 years in office to the same timeframe as President Obama’s last few years in office. President Trump essentially inherited an economy on autopilot and goosed it with tax cuts and some deregulation.

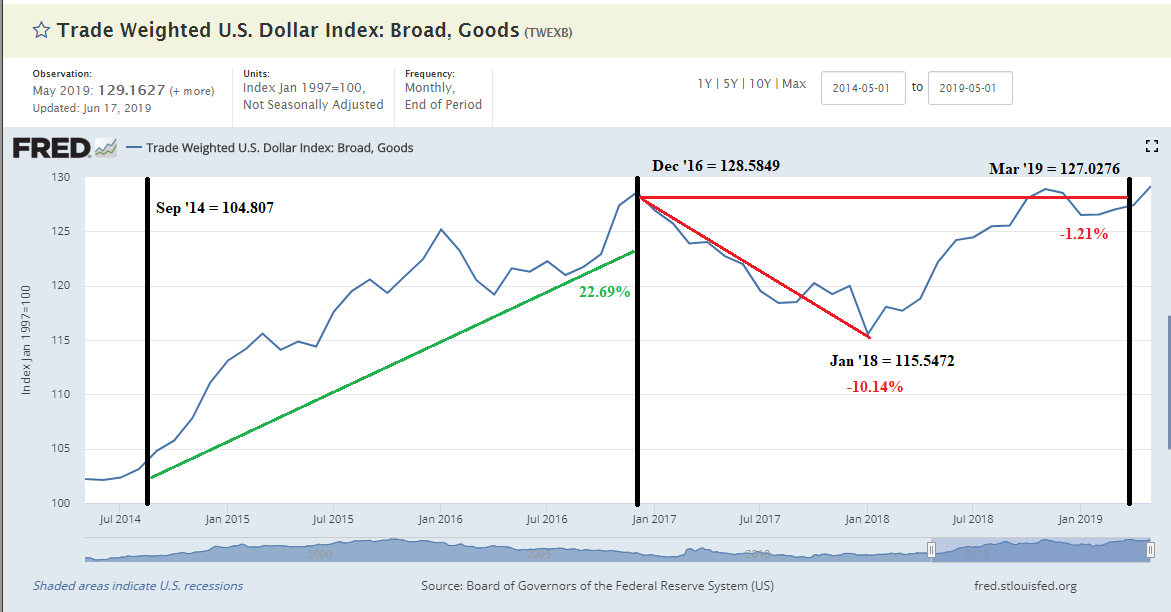

The chart below illustrates that economic growth in the first 9 quarters of President Trump economy was 1.9 percent (0.8 percent annualized) higher than the last 9 quarters under President Obama. Net exports were the main positive contribution to the differential, which makes sense as the trade-weighted value of the dollar increased by over 20 percent during the Obama timeframe and declined 1.2 percent under President Trump, which also includes a 10 percent decline in his first year in office. By the way, not one peep from the Obama administration about the Fed as the strong dollar created a more than massive economic headwind during their last few years in office.

Private fixed investment, mainly in nonresidential structures and equipment, was the second largest contributor to the growth differential, though residential investment has significnatly lagged under Trump.

Personal consumption, federal nondefense and state and local govenrment consumption and investment were big drags (negative) on the Trump-Obama growth differential.

Though nominal wages have grown faster during the Trump economy, inflation has almost doubled, resulting in lower real wage growth than in Obama’s last several months in office, which is also consistent with lagging real growth of personal consumption expenditures. The Phillips Curve does liveth.

Much more to come. Stay tuned, folks.