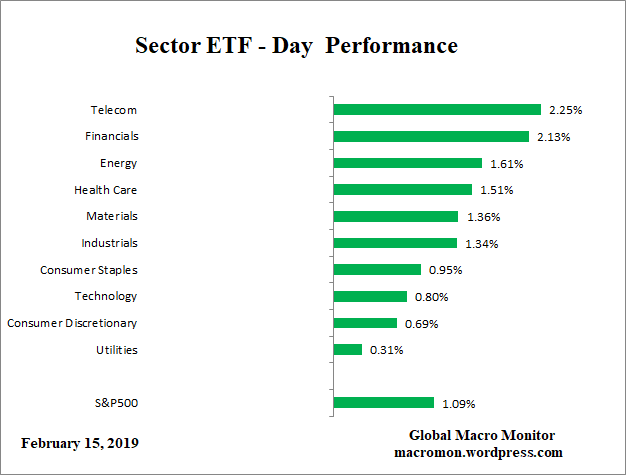

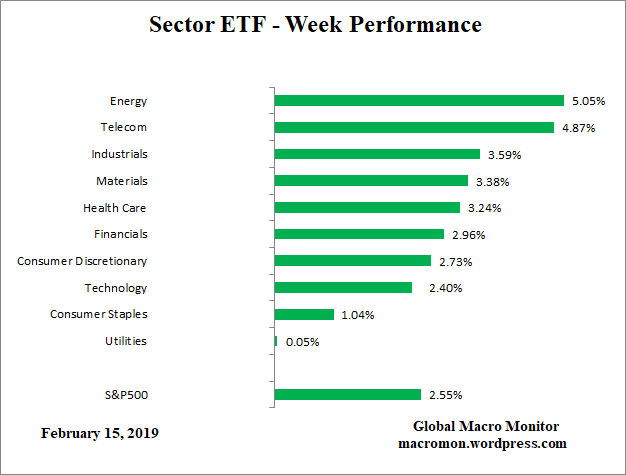

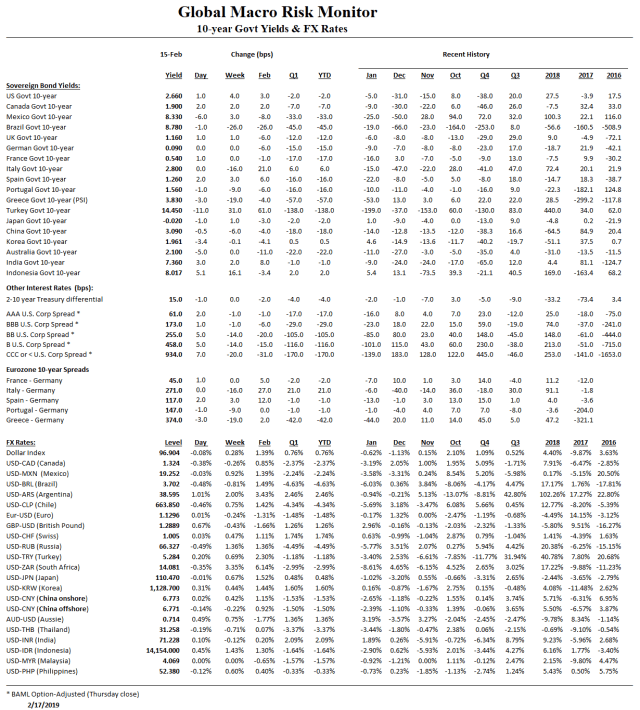

Wow! Not one red bar. Don’t think we have ever seen this. Must be a contrarian signal.

Wow! Not one red bar. Don’t think we have ever seen this. Must be a contrarian signal.

Forbes asks the $382 billion question this morning, Is A China Trade Deal Slipping Away?

President Trump and Chinese leaders are trying to put a positive spin on their marathon trade talks, but the fact is that there is little sign of progress. – Forbes, Feb 16th

That is our thinking and watched with astonishment the Puff The Magic Dragon rally on Friday, with the Dow closing up over 400 points.

You know our thoughts,

Seriously, folks, do you really think the Middle Kingdom, with all its history and past glory, after climbing back to global superpower status after hundreds of years, is now going to cave and give up some of its sovereignty because Trump demands it?

President Xi already seems to be preparing his population for the worst case scenario, warning of “challenging times ahead” possibly in the event Trump goes ahead with the tariff hikes. Maybe we are reading too much into it and maybe not. – GMM

No way in hell will the Chinese give up sovereignty because Trump, whom they now view as Paper Tiger, demands it. No doubt they were watching the government shutdown negotiation debacle with great interest and learning.

Potemkin Trade Deal

So, it looks like we will get an extend and pretend of the March 1 deadline unless Trump decides to play hard and bring down the markets and economy. Xi’s big gamble is that he is too politically weak to do so and won’t.

There is a possibility that I will extend the date. And if I do that; if I see that we’re close to a deal or the deal is going in the right direction, I would do that at the same tariffs that we’re charging now. I would not increase the tariffs. – President Trump, Feb 15th

The Trump team has run into a “Great Wall” of Chinese negotiators and seem to have failed to access what the deal breakers are for President Xi, which is one of the first principles of good negotiating. Bullying and threats of tariffs won’t work and will result in a worse situation than the status quo.

The final deal will be some sort of convoluted Potemkin trade deal (yet another one) with little structural reform to the Chinese economy, which will then invite great criticism of the administration. That is that he caved once again.

Again, we reserve the right to be wrong and will eat our crow BBQ style drowned in sriracha sauce.

BS Degrees From MSU

All administrations, political parties, and governments, in general, are full of officials with BS degrees from MSU. BS, as in Bull Shit; MSU, as in Make Shit Up.

But they seem more ubiquitous in the Trump administration, starting at the top. Weak in economic training, expertise, and understanding, and strong on ideology,

…Malpass nomination highlights the remarkable character of Trump’s economic appointments.

Remarkable in what way? Well, remarkably bad. Every economist, yours truly very much included, gets it wrong sometimes. But Trump only seems to choose men who have been wrong about everything.

Beyond that, however, what’s remarkable is the extent to which this president consistently chooses economists whose ideology is at odds with his own professed views on policy. – Paul Krugman, Feb 14th

When will Mr. Market learn?

Nice piece in ZH on Jeff Gundlach dishing with Yahoo Finance on the vulnerability of the corporate bond market in the next recession. In our data analysis piece, which we reposted below, we highlight the fact largest holders of U.S. corporate bonds are “weak handed” foreigners. Given the diminishing market making capacity of the Street, good luck finding a bid when they decide to hit the exits.

Money quotes from the Bond King,

Major risks facing the market

JULIA LA ROCHE: Right. Well, a lot certainly has changed, as you mentioned. And you’re someone who’s known as someone who always looks at risk. You look at various risks. So I’m curious, what is on your radar right now? What are you focused on?

JEFFREY GUNDLACH: Well, I think the biggest risk– and it may not materialize for a little while longer– is that when the next recession comes, there’s going to be a lot of turmoil because the corporate bond market is extraordinarily leveraged. The ratings of the corporate bond market are very low. There’s a study by Morgan Stanley research that said that if you use leverage ratios alone– and there are other variables that the rating agencies used, but the most important, of course, is leverage ratios of a corporation. And if you use leverage ratios alone, that 45% of the investment grade bond market would be rated junk right now. Right now.

So if there’s a recession, obviously, these ratings will have to be lowered. For now, the rating agencies are listening with sympathetic ears to reassuring statements by some large corporations that they’re aware that their leverage ratios are kind of high, but they plan on addressing that sometime in the next few years. If there’s a recession, it’s obvious that the leverage ratios will not be addressed, and the ratings will have to go. So that’s a really big risk.

Also, during the next recession, we’re going to have an extraordinary national debt problem, because the national debt is growing at a very rapid rate already. And we’re supposedly, if I listen to Larry Kudlow and the president, they keep telling me that it’s the best economy ever. I know that they know that they’re being hyperbolic. But it is a growing economy. Real GDP is 3% year over year of the most recent reading. And yet, the national debt in fiscal 2018, which ended September 20, was increased by $1.27 trillion. – Yahoo Finance

Our latest data work on the corporate bond market is very interesting and kinda flew under the radar. We repost it, right here, right now!

Summary

We spent most of the day crunching numbers on the U.S. corporate bond market as stocks went on another roller coaster ride. Given all the hand-wringing and concern over the buildup of corporate debt since the Great Financial Crisis (GFC), we have a real need to see and understand the data.

The Data

We look at the changes in level, profile, and ownership of the corporate bond market over two different periods with the Fed’s Flow of Funds data. Our point of reference is Q4 2007, which was not only the end of the early century bull run in stocks and beginning of the GFC but also the quarter where nonfinancial corporate debt as a proportion of the corporate bond market was at its lowest (26.6 percent).

Fast forward 43 quarters to Q3 2018, the latest available data, and lag back 43 quarters from Q4 2007 to Q1 1997, and there you have our three points of measurement.

Conclusions/Data Inferences

1997 Q1 to 2007 Q4

2007 Q4 to 2018 Q3

Who Owns The Corporate Bond Market

Upshot

You now have the data and charts, folks. Short and sweet, easy to read.

Now you have the knowledge and can’t claim you were unaware of the risks if the GE refrigerator falls through the kitchen floor.

Data Source

Help keep the lights on at the Global Macro Monitor. Contribute any amount based on your perception of our value added by clicking the PayPal donate widget at the right side of the screen. You don’t need a PayPal account just a credit card. Thank you!

Bonus

Click here for video.

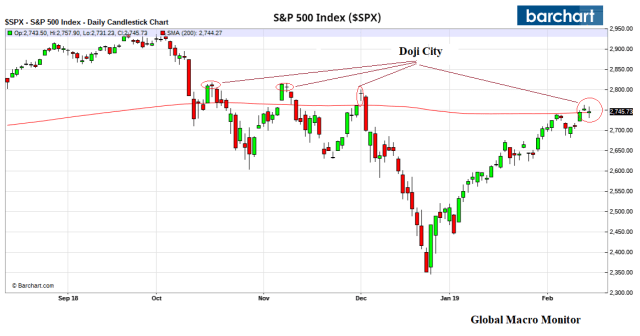

Total indecision in the S&P 500 price action at the 200-day moving average.

Very similar to past short-term peaks but if it were that easy, we’d all be eating caviar on our yachts.

Impressive that market doesn’t break. No sellers.

Nevertheless, better seller before everyone else starts selling.

Source: Using Japanese Slang

Check out today’s cover of the Economist.

It confirms our ongoing analysis and illustrates why you should read the Global Macro Monitor, folks.

It’s been almost exactly one year to the date since we posted, Karl, The Comeback Kid? We warned the 1-percenters to “Wake The F&*k Up” to what was coming — a move to Nordic Capitalism — especially if the millennials started to show up at the ballot box.

They did in November by increasing their turnout by more than 50 percent.

Just a few days before the midterms we posted,

We sense a political earthquake coming Tuesday. Female, young, and left. Brace yourself, folks. – GMM, October 31

Enter AOC & Co. A warning: she/they will take a big political hit — fair or not — on Amazon’s flight from NYC, and they really do need to learn and learn fast, that the private sector is the main engine of job growth and wealth creation.

Similar to using fire to cook your food and warm your house, use and harness market forces to accomplish your social and economic goals. Markets, like fire, are amoral. Corporate socialism, people’s socialism, socialism for the rich, socialism for the poor – hey, it’s hard to be pure.

Nevertheless, we were way out in front before others began jumping on the Karl Train.

Prairie Fire

The movement only gets stronger, in our opinion, as deep structural demographic, economic and political forces are driving the underlying social dynamics of the nation and many other countries in the West. Trump had his chance and deserves credit for reading what most pols missed, but he is increasingly viewed as a Trojan Horse for the elites — as he is or, at least, claims to be an elite — and is despised by the young. Not to mention his political and legal problems.

One political party believes they can win 2020 with a party of old white men scaring the middle by conflating Nordic Capitalism, which the millennials advocate, with “Venezuelan and Cuban socialism.”

Go ask a millennial if they prefer Caracas to Copenhagen? ‘Nough said.

The Rise Of Bernie

Think about it folks.

Bernie Sanders would be president today if Hillary and the Dems had not rigged the 2016 primaries in HRC’s favor. We believe almost one-third of Trump voters felt the Bern, especially in the mid-West, and Bernie would have brought out the younger voters en masse. Trump would not have had a chance.

Trump’s own pollster, Tony Fabrizio, stated flatly at a recent Harvard University Institute of Politics event that Sanders would have beaten Trump. He said Sanders would have run stronger than Clinton with lower-educated and lower-income white voters. I could not agree more, on both counts.

The real working-class hero candidate was always Sanders, not Trump, who has always been a crony capitalist pretending to be a populist. – The Hill, November 3, 2017

Now think five years back, and ask yourself if you ever, in your wildest imagination or fantasies, would have believed a no-name “socialist” independent from Vermont could become president? Or, for that matter, a 12 handicapper reality television star?

We are not advocating jack all here at GMM, as we are often accused, just making inferences from the economic, polling and demographic data, and trying to find our way along the foggy path into the future.

Socialism is storming back because it has formed an incisive critique of what has gone wrong in Western societies. Whereas politicians on the right have all too often given up the battle of ideas and retreated towards chauvinism and nostalgia, the left has focused on inequality, the environment, and how to vest power in citizens rather than elites (see article). Yet, although the reborn left gets some things right, its pessimism about the modern world goes too far. Its policies suffer from naivety about budgets, bureaucracies and businesses. – Economist, Feb. 14

Look What QE Has Wrought?

Bernie and Co. (the MMT crowd) now think that much or let’s say, some, of the increased spending, can be financed by the Fed’s printing press. That reflects a total lack of understanding of monetary policy, monetization, and quantitative easing.

The Fed injected reserves into an impaired financial system to purchase Treasury and MBS bonds in order to inflate asset prices, mainly, but not totally, through hyping animal spirits, without increasing interest rates during a mass asset reallocation and explosion of fiscal deficits. The impact on demand was relatively inefficient and, at best, indirect.

Though a counterfactual can never be proven, nobody knows how much aggregate demand (AD) would have collapsed without QE. We maintain its better to be safe than sorry and it sure beats living under a freeway and eating bark for dinner — surely almost all of our fate if the system had collapsed. So kudos to Ben & Co. for saving the global financial and economic system.

The impact on AD came indirectly through the economic recovery plan’s fiscal spending and the wealth effect. and thus had little impact on goods and services inflation. This also happened during a period of household deleveraging, mainly in mortgage debt, and therefore, the massive reserve injection was not converted to endogenous money through bank credit expansion.

However, corporate and fiscal debt increased, mainly through bond issuance, and asset prices did hyperinflate.

People’s QE

The next big quantitative easing will be a “Peoples QE’ and we believe will go to finance consumption and investment directly. Money demand may not decline, especially at its genesis, but the People’s QE will definitely increase inflation. Its impact on real money demand will determine its length, efficacy, and ultimate fate.

We don’t worry so much about increases in the monetary base, especially when a financial system and credit is impaired, we worry more about the collapse in real money demand, which results from a loss of confidence in the central bank’s commitment to maintaining the purchasing power of the currency. That’s how hyperinflation begins and societies end.

This is our view of the end game, a ways off, however.

Difficult To Understand Monetary Policy

We now have a president who doesn’t understand free trade and certainly has no clue about monetary policy.

“Just run the presses — print money,” Trump said, according to Woodward, during a discussion on the national debt with Gary Cohn, former director of the White House National Economic Council.

“You don’t get to do it that way,” Cohn said, according to Woodward. “We have huge deficits and they matter. The government doesn’t keep a balance sheet like that.”

Cohn was “astounded at Trump’s lack of basic understanding,” Woodward writes. – CNBC

Scary clueless.

I read sometime, somewhere as an undergraduate that President Kennedy, a high IQ POTUS, had trouble remembering the difference between fiscal and monetary policy, and had to write cheat sheet notes on his hands during pressers. Fiscal policy on one hand and monetary policy on the other.

I am still trying to find the documentation for you, folks.

In his last presser Chairman Powell stated even the best and the brightest at the Fed does not know what is the right level of reserves to maintain a stable financial system. Alan Greenspan believed making monetary policy was a black box.

There is, regrettably, no simple model of the American economy that can effectively explain the levels of output, employment, and inflation. In principle, there may be some unbelievably complex set of equations that does that. But we have not been able to find them, and do not believe anyone else has either.

Consequently, we are led, of necessity, to employ ad hoc partial models and intensive informative analysis to aid in evaluating economic developments and implementing policy. There is no alternative to this, though we continuously seek to enhance our knowledge to match the ever growing complexity of the world economy. – Alan Greenspan, Decemeber 1996

Imagine the two candidates in the next presidential election debating the efficacy and risks of a “People’s QE.” Yikes!

We double down on our Soros quote posted late last night,

Most of us assume the future will more or less resemble the present, but this is not necessarily so. In a long and eventful life, I have witnessed many periods of what I call radical disequilibrium. We are living in such a period today. — George Soros, Feb. 12th

Radical disequilibrium, indeed. Not market friendly.