Bonus

We highlighted the potential risk in our post yesterday,

Druckenmiller On Bonds

If you listened to the Druckenmiller interview we posted on New Year’s Day, he thrives in bear markets, not by shorting stocks but being long bonds. Shorting stocks in a bear market, though more profitable, he has learned is riskier due to the higher propensity for nutcracking short squeezes. Druck also worries about the level he is buying at.

Nevertheless, this confirms our suspicion the bond market has been hijacked by stock bears and short sellers. How far they push down yields is anyone’s guess. We just wonder who they are going to sell to when its time to get out. They couldn’t be betting on a central bank takeout in a new round of QE?

Unexpected bond market volatility could be the Black Swan of 2019. We will flesh out our thoughts in a later post. – GMM, Jan 3rd

Taking some ASHR, the Xtrackers Harvest CSI 300 China A ETF at $22.20 for a short-term trade going into next week’s trade negotiations. Our sense is Trump and Xi are under enormous pressure to generate a positive outcome, or at least some good news. Moreover, the monetary moves by the PBOC this morning relieves some of the near-term economic pressure. Stop at $21.50. Target $23.50.

The Apple bulls, if any still exist, now have their work cut out as the stock closed just a penny inside the red zone. The 200-week moving average also looms large as short-term support at $141.82.

The time for a bounce is now.

What a great story.

Taking cable right here at 1.2670 (March). Stop at 1.2470. Target 1.35.

Looking for positive BREXIT news: either Corbyn caves and supports a new referendum or soft BREXIT potential emerges. We do recognize the risk of big volatility to the downside if the politics go sideways.

Stocks were hit with a double punch with the Apple warning and this morning’s weak ISM data (see table). The S&P took out all its hard work since the Christmas Eve tank to close at its post-Christmas low.

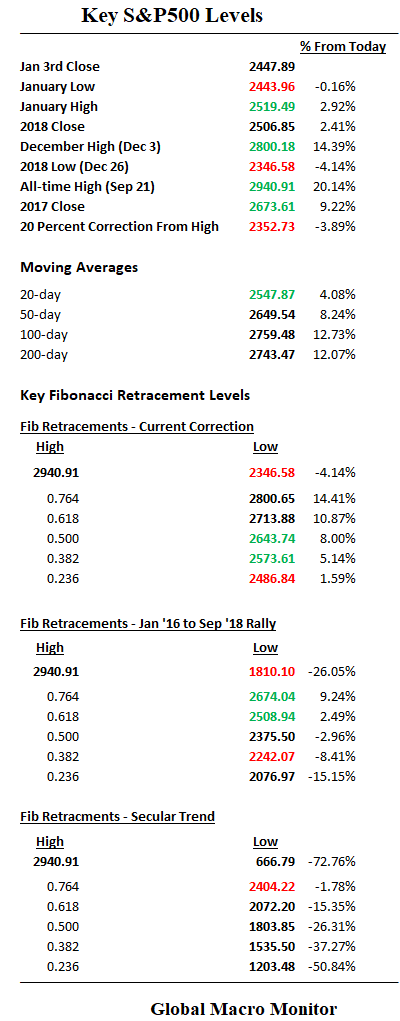

We’re not going to bore you with the key levels as they are evident in the table.

The logical short-term trade here is to bet on a test of the recent low at 2346.58, 4 percent down from today’s close. But as we quoted Stan Druckenmiller in our recent post,

“Logical doesn’t mean profitable.”

Eventually, and relatively soon, we think the test is a no-brainer, however, tomorrow’s employment data and Jerome Powell speech are events that could generate a bounce.

If the employment data comes in soft but not too soft, coupled with today’s weak ISM gives the Fed Chair the cover to strike an exceedingly dovish tone in his speech tomorrow. Ergo rally time and the shorts get their Friday facial and should further boost our gold trade.

Moreover, it’s now or never for a bounce. The chart below shows how rare it is that the S&P500 has closed this far below its 200-day moving average. In fact, only three times since August 2011.

If there is no or just a feeble bounce tomorrow, we get shorty the e-minis for the test of the recent low.

Brazil Equity Trade

How ’bout that Brazil trade, (EWZ), we identified on January 1st? It was up almost one percent in today’s extremely weak tape and now up almost 5 percent from our $39.00 entry point. We are moving the trailing stop up to $38.77. We like the country ETF as it also captures the currency move.

Druckenmiller On Bonds

If you listened to the Druckenmiller interview we posted on New Year’s Day, he thrives in bear markets, not by shorting stocks but being long bonds. Shorting stocks in a bear market, though more profitable, he has learned is riskier due to the higher propensity for nutcracking short squeezes. Druck also worries about the level he is buying at.

Nevertheless, this confirms our suspicion the bond market has been hijacked by stock bears and short sellers. How far they push down yields is anyone’s guess. We just wonder who they are going to sell to when its time to get out. They couldn’t be betting on a central bank takeout in a new round of QE?

Unexpected bond market volatility could be the Black Swan of 2019. We will flesh out our thoughts in a later post.

Source: Institute for Supply Management

The Palm Beach Daily News captures the global market and political zeitgeist at the start of the New Year in their hilarious ‘toon.

Hmmm…who does that Wall Street baby look like?

Hat Tip: David Wilson

Hmm… Wonder if the X Max price is hedonically adjusted to compensate for its superior technology to show there really has been no iPhone price inflation?

Hedonic quality adjustment is one of the techniques the CPI uses to account for changing product quality within some CPI item samples. Hedonic quality adjustment refers to a method of adjusting prices whenever the characteristics of the products included in the CPI change due to innovation or the introduction of completely new products.

The use of the word “hedonic” to describe this technique stems from the word’s Greek origin meaning “of or related to pleasure.” Economists approximate pleasure to the idea of utility – a measure of relative satisfaction from consumption of goods. In price index methodology, hedonic quality adjustment has come to mean the practice of decomposing an item into its constituent characteristics, obtaining estimates of the value of the utility derived from each characteristic, and using those value estimates to adjust prices when the quality of a good changes. – BLS

I wish they would hedonically adjust my income. Could be why we suspect the “real” – as in actual purchasing power – real wage is lower than what is being measured.

All this nonsense is starting to come home to roost.

Let us reiterate a thought from our last post, which is apropos to Apple.

The fundamental problem with

the housing marketApple is that [iPhone] prices are too high and need to come down. – GMM

And they will. Tesla gets its.