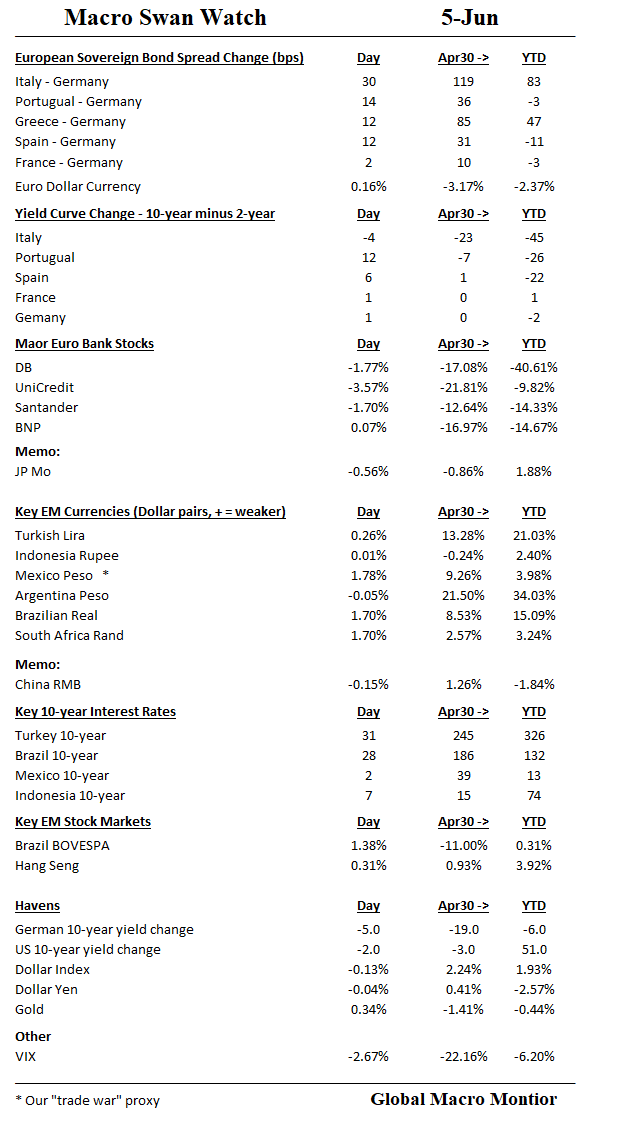

In a normal probability distribution…blue curve), the odds of risky outcomes (bad stuff happening) are thin at the extremes. In fat-tailed distributions, such outcomes have a greater chance of occurring (the [greenish] curve). Source

Non-normal distributions can be heavily skewed and unstable. – Decline of the Empire

Fat Tails In Real Life

If you have been following the Global Macro Monitor more than, say, a year, it should be clear by now we love living in the fat tails. That is we are natural contrarians, love to play devil’s advocate to and jackhammer the prevailing perma bullish narrative, and always looking for the next big move in the markets.

By fat tails, we mean more than a two standard deviation (sigma) move, which happens more often in the markets than they should in a normal distribution of returns. Ergo the “fat tails.”

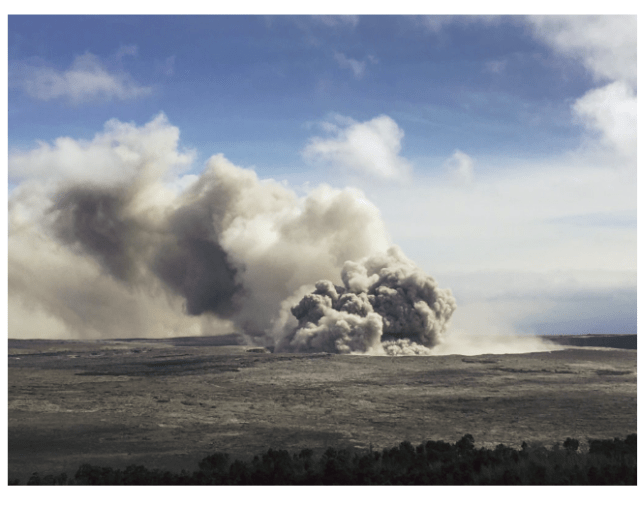

Hawaii

In the past year, we have experienced some very high sigma events in real life. If you recall in April, we went on a short-term spring break. To where, you may ask?

The rim of the Kilauea volcano on the big island of Hawaii!

This just a few weeks before it blew. As my 15-year daughter perused the landscape, which looked like a scene from the surface of Mars, we snapped the following picture of the rim with my iPhone. Again, this was just a few weeks before it blew as illustrated in the subsequent images.

I recall thinking at the time that the probability is very low of a volcanic eruption but what if while we were here? I have lived through some very terrifying earthquakes, one that destroyed our home. However, being stuck in the middle of the giant Pacific while the volcanic island is blowing its top would be scary, especially when you have your youngest child with you.

In fact, I even thought of posting a piece about fat tails back then. While visiting the museum at the top of the rim, I came across a Richter scale that shows seismic activity usually significantly increases before an eruption. It was the inspiration for this quote,

Markets rarely fall out of the sky and usually signal something big is coming by a sharp rise in volatility. Think of a Richter scale before a volcano blows. – GMM, April 21

Pele is upset.

Pelehonuamea, to be exact. “She who shapes the sacred land.” In Hawaiian myth and culture, Pele is the goddess of fire and volcano and devours the Big Island when she is perturbed. She has a wicked temper and she made her home in the Halemaumau crater. – Washington Post

Kilauea is home to Pele, goddess of the volcano

Godspeed to our friends on the Big Island..

iPhone Shot On Spring Break (early April)

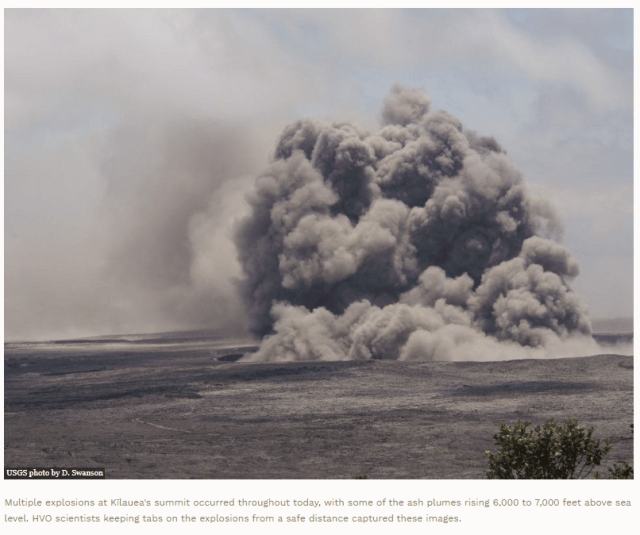

A Few Weeks Later

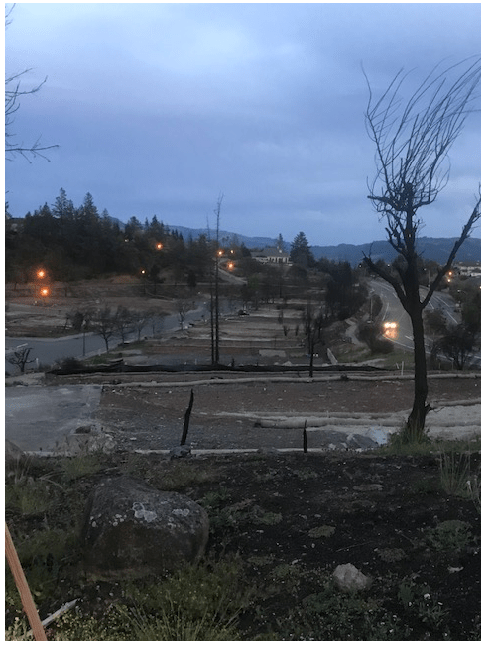

The October NorCal Fires

If you were tuned in to the Global Macro Monitor, you recall our experience fleeing from the flames of the October fires in Northern California. See here and here.

Those were some stressful daze. ‘

The lot just before the what looks like a Roman colonnade in the picture taken the morning after was our old home. Still stunned when I drive through the old neighborhood that something like that could have happened. Only one house is standing in the old track of about 600 homes.

I guess empirical probabilities become distorted relative to the logical probability when you wake up every morning and the sun still rises even though there were concerns and warnings that such a devastating fire could take place. I often thought of those warnings but dismissed them as a low probability “tail risk.”

We are now at ground zero of all that ills the housing market. The acute shortage of residential housing supply is driving rents sky high. The labor shortage coupled with increasing construction costs are making it difficult for contractors to build.

Regulatory red tape and the slow bureaucracy is adding to the difficult task of rebuilding. You can see in our old neighborhood not one lot is under construction more than eight months after the fire. The water was contaminated, and underground architecture was destroyed and needs rebuilding before residential construction can begin.

Many of the above problems in our local housing market are also reflected in the national housing market, which is fueling another price bubble. The current bubble is much different from the one experienced 2006-08, however, and driven not so much by leveraged buying but by the new supply-side economics. The price adjustment will therefore have much different dynamics.

Though devastating and one is too many lives lost the October fire was not even close to the devastation wreaked upon Puerto Rico and Houston from last year’s hurricane season.

Lessons Learned

What did we learn through all this?

Tail risk is real and more likely than a normal distribution foretells. Moreover, the real world and markets live in probability distributions with obese tails.

Finally, someday the quant driven trading algorithms are going to simultaneous short-circuit because they have their probability distributions wrong, causing a major market meltdown and significant damage to the global economy.

Stay tuned, HAL and Kurt.

Our Old Neighborhood The Morning After

Same Shot A Few Weeks Ago