The S&P closed right at or just a smidgen above its 200-day moving average. The market rally based on a government shutdown deal? Come on, man!

Another government shutdown wasn’t priced, so why should stocks move on a deal?

We wrote this weekend,

China back online this week, Mnuchin and Lighthizer to China for negotiations, mo earnings, CPI, and government funding deadline on Friday.

Senate Appropriations Chairman Richard Shelby (R-Ala.) acknowledged on Sunday that negotiations had stalled, and he put the odds of getting a deal at 50-50. – Politico, Feb 10th

It will get done. They are not that foolish. – GMM, Feb. 10th

Seems to us, the noise traders and ‘bots were caught offside.

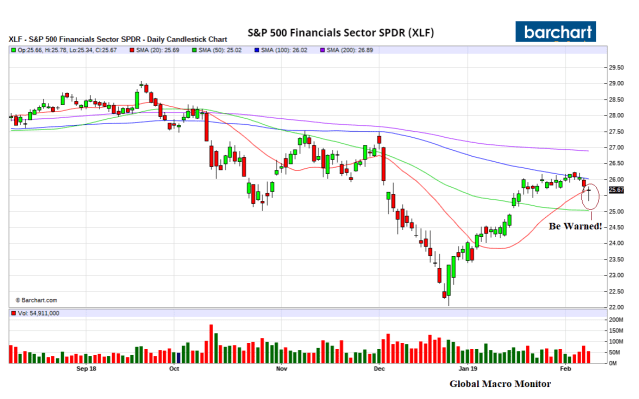

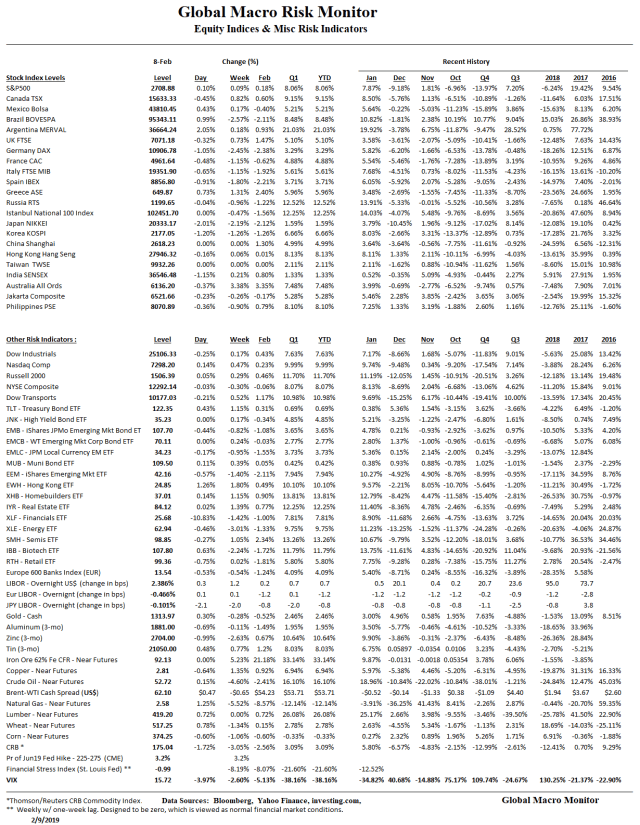

Three Green Candles

The price action over the next few days will be key.

As we posted earlier, three green candle closes above the 200-day sets the S&P500 up to challenge the yuuge level at 2800 (see table).

The announcement of some sort of convoluted China trade or extend and pretend will be one of the biggest sell the news events in recent history. Trump is going to take some big hits for caving on the big issues after causing mucho pain to the U.S. and global economy, and American farmers, in particular. All for the promise of a few soybeans and a “pig in a poke.”

Kudos for trying though but no strategy, no disciplined message, a divided team, and telegraphing fears of a stock market meltdown advantages the Chinese negotiators.

Seriously, folks, do you really think the Middle Kingdom, with all its history and past glory, after climbing back to global superpower status, is now going to cave and give up some of its sovereignty because Trump demands it?

President Xi already seems to be preparing his population for the worst case scenario, warning of “challenging times ahead” possibly in the event Trump goes ahead with the tariff hikes. Maybe we are reading too much into it and maybe not.

Selling strength higher prices.