(COTD = Chart of the Day)

(COTD = Chart of the Day)

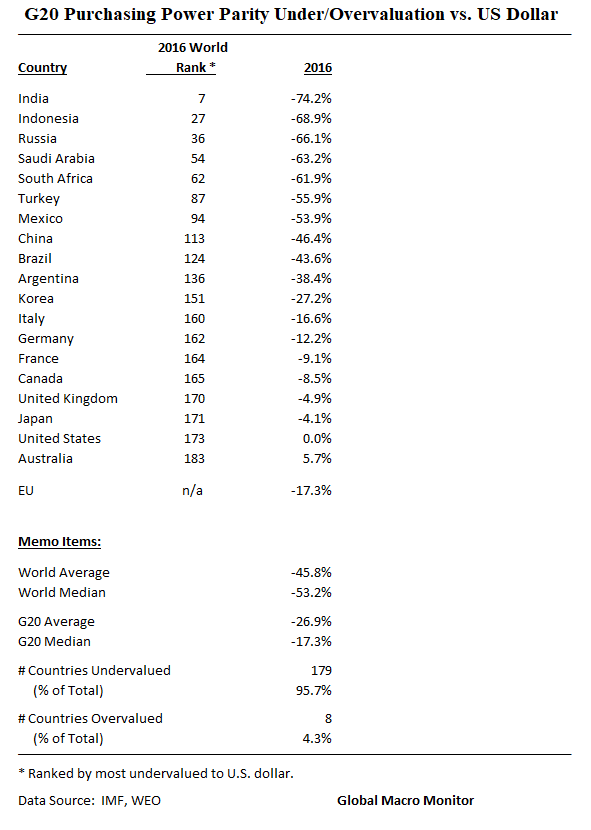

We’ve put together a couple of tables showing the undervaluation of the world’s currencies based on their 2016 purchasing power parity against the U.S. dollar.

The Purchasing-power-parity (PPP) between two countries is the rate at which the currency of one country needs to be converted into that of a second country to ensure that a given amount of the first country’s currency will purchase the same volume of goods and services in the second country as it does in the first. In the WEO online database, the implied PPP conversion rate is expressed as national currency per current international dollar. The advantages and disadvantages of using PPP-based exchange rates rather than market exchange rates are discussed in the Finance & Development article “PPP Versus the Market, Which Weight Matters?” (March 2007) and Box 1.2 of the September 2003 World Economic Outlook (WEO). For the latest PPP weights revision, please see the “Revised Purchasing Power Parity Weights” section in the July 2014 WEO Update. For the 2008 PPP weights revision, see figure 1.16 from Chapter 1 of the April 2008 WEO. For 2003 PPP weights revision, please see Box A2 from the April 2004 WEO. For the 2000 PPP weights revision, please see Box A1 from the May 2000 WEO.

The International Comparisons Program (ICP) is a global statistical initiative that produces internationally comparable Purchasing Power Parity (PPP) estimates. The PPP exchange rate estimates, maintained and published by the World Bank, the OECD, and other international organizations, are used by WEO to calculate its own PPP weight time series. Currently, WEO PPP exchange rates are based on the ICP’s 2011 report. For more information, you can go to the World Bank’s ICP page. – IMF

The data give only an approximation of undervaluation as spot exchange rates have moved since the rates were calculated. Also note the differences from our recent post on the Big Mac Index, especially in Brazil.

We calculated over/undervaluation by taking the IMF’s estimate of nominal dollar 2016 GDP and divided by the PPP nominal dollar 2016 GDP.

Not perfect, but the data give and an idea just how overvalued the dollar is across the world on a purchasing power basis; that only 8, or just 4 percent, of world currencies are overvalued (and just slightly) versus the dollar; that China is not alone; that Russia is extremely undervalued; Aussie is the only overvalued G20 currency; and the Swissie is expensive.

Still, we expect the dollar to get much stronger over the next few years due to President Trump’s fiscal policy and the Fed’s monetary tightening.

.

.

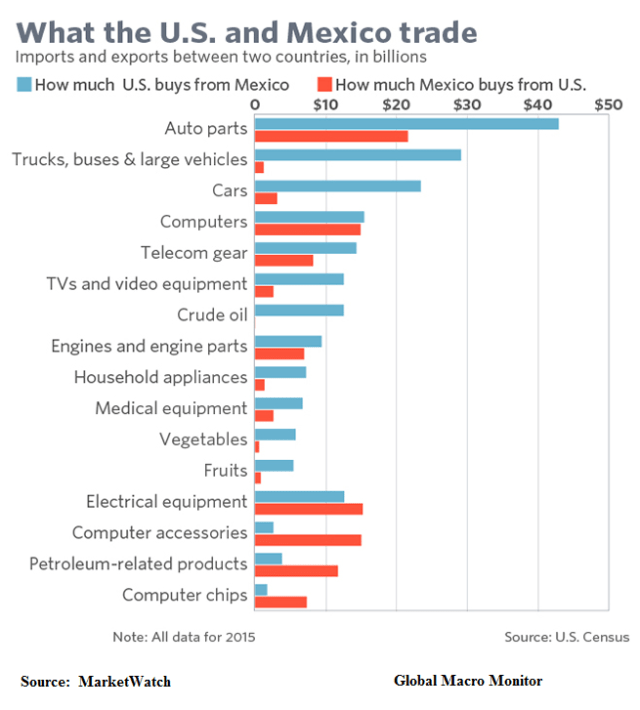

Which jobs do you think trade tariffs will destroy? Retail, no?

As tariffs and border taxes are implemented, the price of goods rise, real income falls, ergo demand falls and fewer WalMart shoppers buying higher priced goods equal layoffs. In the very states that voted for President Trump! And that’s not counting retaliation and result of a loss of jobs in the export sector.

Let’s think this thing through, policymakers. Even fotget the economics, just think of the politics.

Source: MarketWatch

Stratfor Latin America Analyst Reggie Thompson discusses the steps that would have to be taken before the construction of a wall along the U.S.-Mexico border could begin.

For more analysis, visit: http://www.Stratfor.com

Jan.22 — Now that Donald Trump is in the White House, the world’s biggest companies are trying to gauge the likelihood of a U.S. trade war with China. If the tension escalates, there could be losers on both sides. Bloomberg’s Jeanny Yu reports on “Bloomberg Markets.”

The Dow crossed 20k as the market perceives accelerated future profit growth from the “Good Trump” policies – deregulation, etc. – and traders surf the Keystone pipeline to higher prices. The momentum will continue until it doesn’t.

Not a lot of supply, a dearth of sellers and money will almost certainly move in and start chasing. Not cheap, but enjoy the ride.

We have deep concerns about the lurking “Bad Trump” policies, however.

The “buy American” rhetoric we heard yesterday around the pipeline plays well in Peoria but if it becomes law or is required in certain deals, it can be labeled a non-tariff barrier to free trade.

The Rules of Origin Agreement requires WTO members to ensure that their rules of origin are transparent; that they do not have restricting, distorting or disruptive effects on international trade; that they are administered in a consistent, uniform, impartial and reasonable manner; and that they are based on a positive standard (in other words, they should state what does confer origin rather than what does not).

– WTO

China does it but we would hate to see them expand it in retaliation, which they certainly will, if President Trump follows through with his tough trade and China policy rhetoric.

Imagine if Mr.Xi retaliates with a “buy China” cell phone policy, for example. That would take a big byte out of Apple. The company derived almost 2o percent of last quarter’s revenues from China and that was after a 3o percent year-on-year decline.

Then there is the real income impact on consumers of restricted trade. The jobs lost in retail, restaurants, etc. as Americans’ real incomes decline due to higher prices will almost certainly more than offset the jobs saved through restrictions on trade.

We have failed miserably as a government to assist those who have lost from the country’s free trade policies. Cheap prices at Costco and WalMart do have a cost in the form of a lost job for someone.

What the federal government spent on Trade Adjustment Assitance in 2014 was absurd. Around $600 million or about one-half the cost of a B1 bomber! Can you spell B-A-C-K-L-A-S-H? Hillary certainly can.

Free trade, globalization, and significant, rather than trivial, adjustment assistance to those hurt by this policy is the way to go and the road to building real wealth for all nations, in our book.

Here is Stephen Roach on the President Trump’s hardline China policy,

This strategy will backfire. It is based on the mistaken belief that a newly muscular United States has all the leverage in dealing with its presumed adversary, and that any Chinese response is hardly worth considering. Nothing could be further from the truth.

…But the greatest tragedy for the US may well be the toll all of this takes on the American consumer. “America first” – whether it comes at the expense of China or via the so-called border-tax equalization that appears to be a central feature of proposed corporate tax reforms – will unwind many of the efficiencies of global supply chains that hold down consumer-goods prices in the US (think Wal-Mart).

With their incomes and jobs under long and sustained pressure, American consumers count on low prices for their economic survival. If Trump’s China policy causes those prices to rise, the middle class will be the biggest loser of all. – Project Syndicate

So enjoy the ride. Don’t fight the tape.

But keep in mind there are some very nasty policy proposals lurking out there and, if realized, will cause a world of hurt for the global markets and economy.

Stay tuned.

We posted last week the correlation of the bond and gold. Some argue gold has been rallying as a hedge against inflation or inversely with the dollar. Don’t think so and not yet on the inflation hedge.

Gold is moody and is currently in the mood to track interest rates, at least, for now. Check out how the 10-year note and gold are tracking in the chart below.

Remember gold is a “weird cat” with many lives and many reasons to move the way it does.

Gold is a weird cat with multiple personalities and more than nine lives. The yellow metal is up almost $100 since last Friday’s weak U.S. employment report.

At any given time period gold will assume any one of its multiple personalities based on a fundamental story and trade as: 1) a safe haven; 2) an inflation hedge; 3) a commodity; 4) a store of value against central bank balance sheet expansion; 5) an alternative currency; 6) central bank reserve currency; 7) a diversification asset; 8) an Armageddon hedge; and/or 9) all of the above.

– Global Macro Monitor

Note the dollar was down today as was gold. Rates are moving higher across the world. The 10-year German Bund yield has doubled since the new year, from 20 bps to close to 50 bps.

We believe the 35-year bond bull is over and expect interest rates to move up to the 5 percent level over the next few years. The tighter liquidity conditions should take gold into the triple digits this year. Inflation cometh, folks.

Stratfor Middle East Analyst Emily Hawthorne looks at the factors complicating Riyadh’s latest effort at reform.

For more analysis, visit: http://www.Stratfor.com

Our view that inflation in the U.S. is going to be the biggest market risk of 2017 is starting to take shape. Take a look at rents in the second chart below.

European political risks? Nah.

The March 15 elections in the Netherlands will probably result in Geert Wilders’ PVV far right party almost tripling his seats in the lower house from 12 to maybe 35, but far from a 75 seat majority and it will be hard for him to find coalition partners to form a government.

France? Betting markets have Fillon at 51 cents and LePenn at 34 cents. These guys have been wrong before, but, think about it, Fillon will take most votes to the left of LePenn. He is pretty conservative himself. A Fillon victory will spark a massive equity rally in Europe, in our opinion.

The German elections in September? Life is good in Germany, doubt they make big changes to their government.

China? Wild card. Opaque and hard to figure out. The financial sector is unlike other western economies. How does it fund itself? Interbank lines, deposits, borrowing from the PBOC? All of the above? At the end of the day, China is still a command economy. But, we are working hard on trying to get our hands around the Middle Kingdon. We do expect increased political tensions between China and the U.S. that could rattle markets.

So, as the U.S. closes its borders, implements border taxes, and restricts trade, inflation can only go north. Not priced. Stay tuned.

The FT’s Leo Lewis looks at how uncertainty over US President Donald Trump’s America First policy affects the dollar-yen currency trade.

► Subscribe to FT.com here: http://on.ft.com/2eZZoLI