Published on Jan 6, 2017CES is full of manufactures making Apple accessories. We went searching for the most interesting products! –Mac Rumors

Published on Jan 6, 2017CES is full of manufactures making Apple accessories. We went searching for the most interesting products! –Mac Rumors

If one morning I walked on top of the water across the Potomac River, the headline that afternoon would read: ‘President Can’t Swim.’ – President Lyndon B. Johnson

Hedge fund executive Robert Mercer and his family are poised to become major power brokers in Donald Trump’s Washington. WSJ’s Keach Hagey joins Lunch Break with Tanya Rivero and explains how the Mercers saw the appetite among voters for an outsider candidate as early as 2014. Photo: Sylvain Gaboury/Patrick McMullan Agency

Subscribe to the WSJ channel here:

http://bit.ly/14Q81Xy

Our money is on John Taylor as Trump has surrounded himself with the hard money crowd.

Jan.09 — Standish Chief Economist Vincent Reinhart discusses possible Federal Reserve appointments under a Trump administration. Reinhart speaks on “What’d You Miss?”

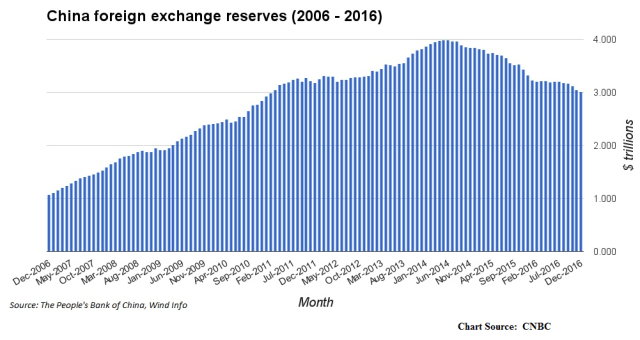

The FT reports,

China’s foreign exchange reserves continued to fall in December, albeit at a slower rate than previous months, as the central bank announced a lower than expected drop in foreign exchange reserves for the month.

Reserves fell by $41bn, to $3.01tn, less than the expected $51bn drop according to a Reuters poll of analysts. In November reserves fell $70bn.The lower than expected drop nonetheless showed that pressure on the renminbi continues, as many Chinese seek to get money out of the country.

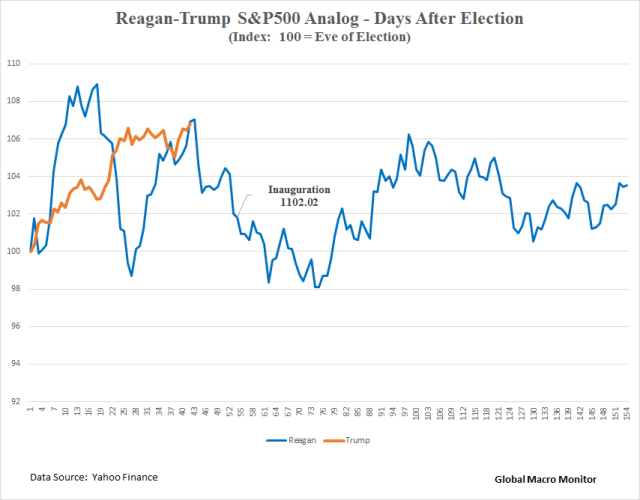

We’re still tracking the Reagan-Trump S&P500 analog. We’ve noted it’s a fun exercise and probably useless in predicting the future move in the index given the different macroeconomic initial conditions at the beginning of both Administrations. But, hold on! It is getting interesting here.

The chart below shows the Reagan S&P and the Trump S&P are trading right on top of each other after 42 days from the respective POTUS elections. In fact, the Trump S&P now trails Reagan by only .09 percent. If past is prologue, the S&P500 makes a new high on Monday and then succumbs to profit taking.

The Reagan S&P peaked on November 28, 1980, 18 days after the election, and entered a nasty bear market, which took the index down over 27 percent in 429 trading days, before the bull market began on August 11, 1982. The bull market was ignited by a precipitous drop in bond yields and U.S. economy exiting a very deep recession.

The macroeconomic conditions could not be more different as President Trump takes office.

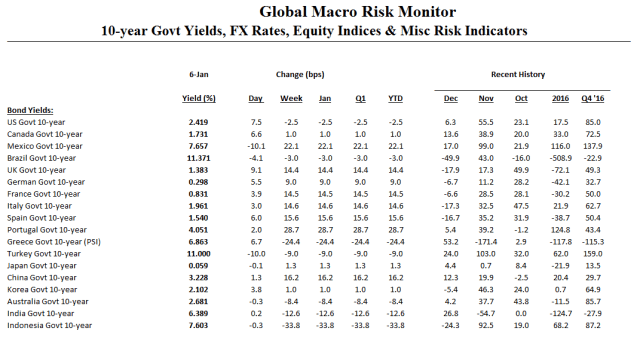

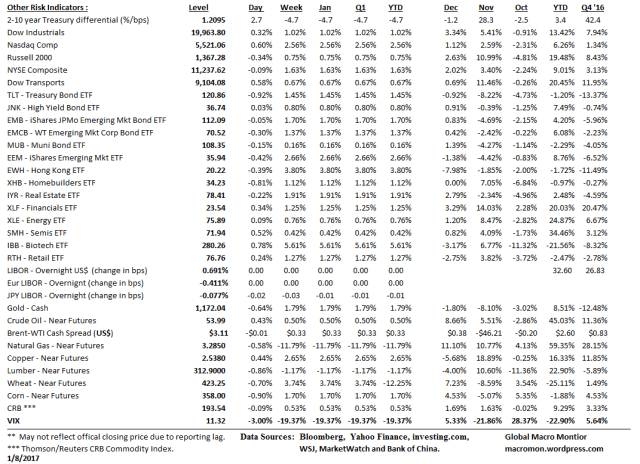

Click on table to enlarge and for better resolution

Grab one of these:

Careful what you wish for central bankers and fiscal policy makers. Though we don’t see signs of “rollover risk” in any of the G5 or G20, it’s all about confidence and you know what Joe said about confidence:

Confidence is a very fragile thing. – Joe Montana

.

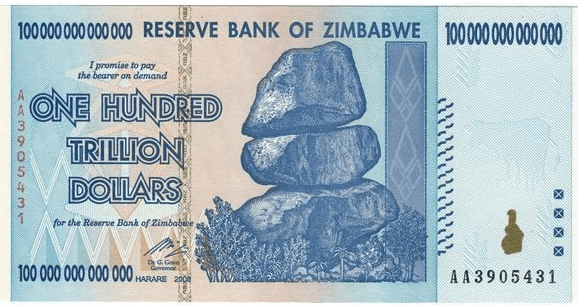

The World Economic Forum reports this about Zimbabwe’s ghost of hyperinflation past,

Zimbabwe was once so gripped by hyperinflation that the central bank could no longer afford paper on which to print practically worthless trillion-dollar notes.

The government reported in July 2008 that Zimbabwe was experiencing inflation of 231 million percent (231,000,000%). However, the Libertarian think tank, the Cato Institute, believes that the real inflation rate was 89.7 sextillion percent or 89,700,000,000,000,000,000,000%.

It is interesting to note that the country is now grappling with the opposite problem.

Like Britain, Japan, the US and other nations dealing with the consequences of weak demand and cheap oil, Zimbabwe is threatened more by the prospect of falling prices. But that doesn’t mean its people are ready to trust that hyperinflation won’t happen again.

This is what happens when you are not a reserve currency — i.e., there is global demand for and a financial incentive to hold your currency — and markets have lost confidence in your central bank and central government. That, in our opinion, is the next major systemic macro swan: the loss of confidence in a G5 central bank and government. Not a black swan as it is a known unknown rather than an unknowable unknown.

We still have ongoing debates with our good friends from the modern monetary theory (MMT) about whether a major sovereign government can default if they have an independent central bank. Yes, they can!

We had the same debate with our Argentine friends several years ago as to whether their government would or could devalue their currency when it was on an effective currency board. Yes, they did! And defaulted to boot.

Just as Russia chose to default on its GKOs (short-term ruble denominated treasury bills) in 1998 with an independent central bank, the same can happen to a G5 country as we approach the upper bound of debt limits and the lower for longer interest rate meme seems to be sunseting in a post-Trump world.

When a highly indebted sovereign crosses the tipping point — and nobody knows where the tipping point is — when the markets lose confidence in its ability to repay or rollover debt coming due and the window shuts on refinancing, they face three choices:

1) bailout – easy for a small country, such as Greece, but Italy or Japan are too big to bail; 2) hyperinflate – print money to pay maturing debt obligations and finance budget deficits. An aside: the Bulgarian central bank did this in 1996 resulting in hyperinflation, which peaked at a monthly inflation rate of 242% in February 1997. I was in the Bulgarian central bank in the fall of 1996, when a senior official looked me in the eye and said, [Gregor], we will not let the government default on its treasury securities.” I knew what was to come; and 3) default and restructure.

Like the Russians, the decision to hyperinflate, default, or go begging to the IMF, is a political one. Russia saw that a high percentage of holders of its local currency debt was held by foreigners, hedge funds such as David Tepper.

Tepper says that losing 29% ($80 million) on Russia when Russia defaulted after an IMF deal “the biggest screw-up in his career”. – Ivanhoff Capital

The Russians made a political choice to default and inflict the pain on foreigners rather their domestic population through hyperinflation. What was interesting is Russia continued to pay their dollar-denominated euro bonds, which had a relatively low debt service burden compared to the maturing GKOs. The Russian government effectively carved out and gave implicit seniority to a specific component of their debt structure. Totally contrary to what MMT predicts will happen, i.e., print money to pay the local debt and default on the hard currency external debt.

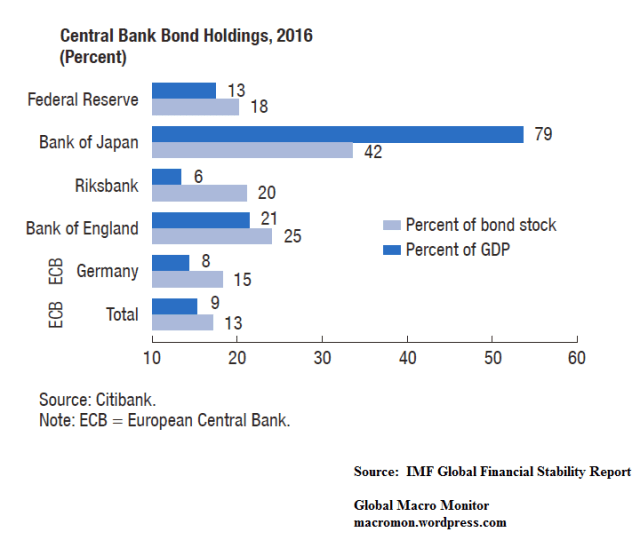

The major industrialized countries have gotten away with massive money printing and central bank financing not only of their sovereign governments but even some private corporations as well.

Good things don’t last forever.

As interest rates rise and are normalized, highly indebted countries could enter a vicious cycle on the fiscal side,

Our current debt may be manageable at a time of unprecedentedly low interest rates. But if we let our debt grow, and interest rates normalize, the interest burden alone would choke our budget and squeeze out other essential spending. There would be no room for the infrastructure programs and the defense rebuilding that today have wide support.

It’s not just federal spending that would be squeezed. The projected rise in federal deficits would compete for funds in our capital markets and far outrun the private sector’s capacity to save, to finance industry and home purchases, and to invest abroad.

Instead, we’d be dependent on foreign investors’ acquiring most of our debt — making the government dependent on the “kindness of strangers” who may not be so kind as the I.O.U.s mount up. –

We think foreigners will not be that “kind” to the U.S. in the new hardball world of Trumplandia as the risk of trade wars and deglobalization increases. Run, don’t walk, to read Martin Wolf’s latest, The long and painful journey to world disorder.

Furthermore, given the Trump fiscal policy, which will significantly reduce net public savings and is highly dependent on big increases in private investment and consumption for growth, further reducing net private savings, the U.S. current account balance, by definition, will deteriorate markedly over the next several years. Thus, there will be yuuuuge competition for the world’s foreign savings to finance the larger U.S. current account deficits. In this world, if realized, real interest rates will head north in a hurry.

Remember the National Accounting Identity,

(S-I) + (T-G) = (X-M)

(S-I) is the ‘private savings balance’ or the difference between private sector savings (S) and investment (I); (T-G) is the ‘government balance’ or the difference between tax receipts (T) and all government expenditure (G); (X-M) is the difference between exports (X) and imports (M) and is usually called the simple ‘current account balance’. –

As the tide of easy money recedes, we have a queasy feeling we’ll be seeing a lot of schlong over the next few years as the markets find out who has been swimming naked.

And, always, keep this in mind:

“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.” – Rudiger Dornbusch

Fasten your seatbelts, it’s going to be a bumpy night. Stay tuned!