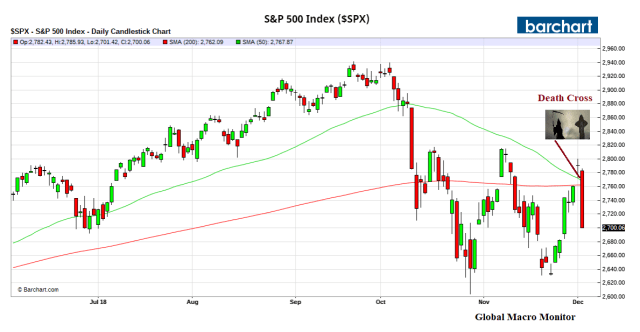

We had to post a response to the market punditry rationalization on why stocks accelerated downward today:

“the S&P500 broke its 200-day moving average.“

Are you fricking kidding me?

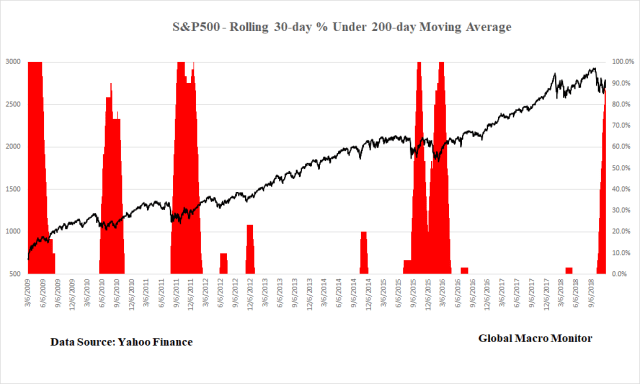

The S&P500 has been under its 200-day 87 percent of the past 30 trading days and 14 straight days prior to yesterday’s ramp.

Why then would a break of the 200-day moving average tank stocks?

Nice Chart

See the second chart below which illustrates the percentage of days over a 30-day rolling period the cash S&P500 has been below its 200-day moving average.

It is interesting that from March 16, 2016, to March 29, 2018, the S&P500 closed under its 200-day only once. That is 1 out of 514 trading days. Moreover, from June 28, 2016, to March 29, 2018, the S&P500 closed above its 200-day 442 consecutive days.

Didn’t Minsky say, something to the effect, the lack of volatility, leads to complacency, which sows the seeds of higher volatility?

Stop Losses?

We’ll concede it is possible that many, including the trading ‘bots, who got long yesterday’s ramp expecting a Christmas rally may have used the 200-day as their stop-loss. The pundits should have qualified their explanations instead of hanging it out there that today’s break of the 200-day was somehow unique. Come on, man!

Perverted Yield Curve And Self-Fulfilling Recessions

The noise around the “perverted” yield curve is also absurd, at least to us, and a bit dangerous as it could actually be self-fulfilling and cause the recession it is supposedly predicting. The policymakers, who have manipulated the markets for the past decade, just might be seeing the chickens finally coming home to roost.

Nevertheless, as we have said many times, the only way bond yields move lower is due to haven flows. That is other markets need to sell-off bigly.

We are working on a piece, crunching the numbers, on the yield curve. It should be posted in the next few days.

Interesting double-top, double bottom W forming in the S&P500. In honor of George H.W. and George W.? Hmmm……

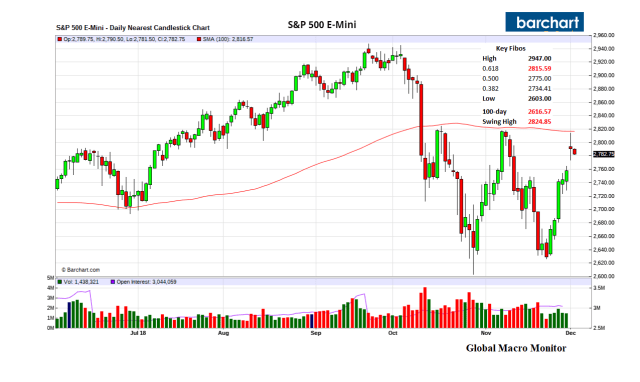

The futures were rejected right at key resistance in overnight trading, making a high at 2814.0 during in early morning pre-trading and it now down 31 handles in Asia trading. The cash market was repelled today right at 2800 (2800.18 if you’re counting)

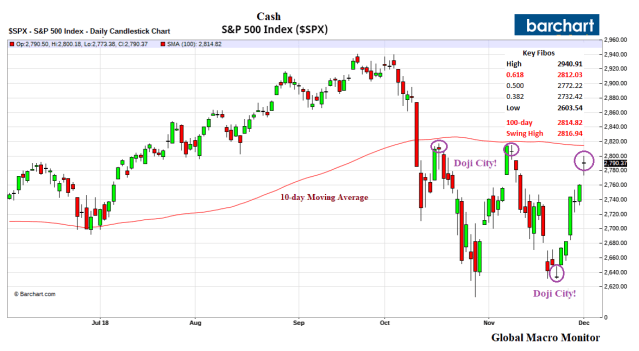

Doji City

The cash S&P made another well-formed Doji candlestick today. Notice during this Q4 correction, the Doji stick has signaled major reversals. It is important the cash S&P closes above 2817 in the next few days in order to set the stage for the Christmas rally.

The S&P had rallied 6.43 percent from the Black Friday/Thanksgiving low below succumbing to profit taking today. Calling short-term market moves is a mug’s game but we suspect they are gonna pull out all the stops to rally ‘em. Follow the indicators on your panel as it’s foggy and there is some significant event risk.

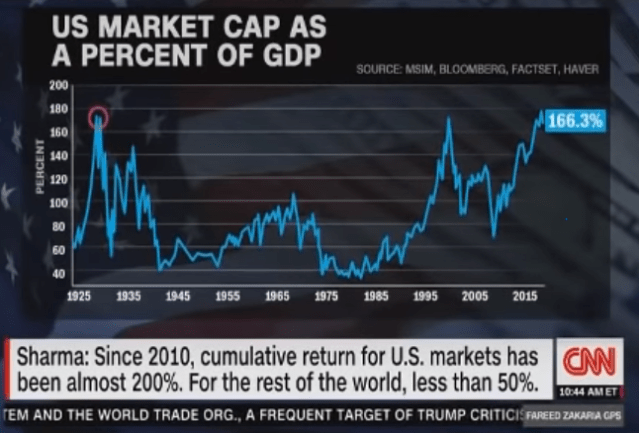

Stocks For The Medium-Term

You know our medium-term view on the U.S. stock market, which is reflected in the following chart.

If you read our Month In Review post last night, you would have noticed we are very skeptical of the fundamental factors which have driven the recent rocket ride in stocks. The Powell cave was a disgrace, in our opinion.

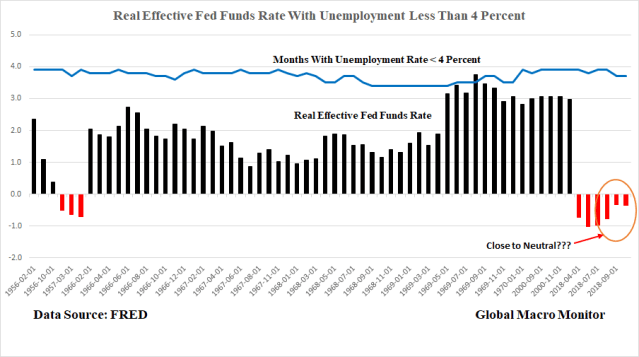

Take a look at the following chart, which graphs the 64 months where the civilian unemployment rate has been under 4 percent over the past 70 years with the real effective Fed Funds rate (using monthly yoy CPI inflation) in that particular month.

Now. try and convince us, or anyone, for that matter, the Fed Funds rate, which is currently negative in real terms, is “just below the broad range of estimates of the level that would be neutral” with an unemployment rate at less than 4 percent. He blinked to the president’s bullying.

Cow dung.

Incredible China Trade Deal

Then there is the China Trade Deal, supposedly cut in Buenos Aires. “It’s an incredible deal. It goes down, certainly, if it happens, it goes down as one of the largest deals ever made.” Note the “if” and a big if, to say the least.

Then this last night that got the S&P traders really, really lathered up.

China has agreed to reduce and remove tariffs on cars coming into China from the U.S. Currently the tariff is 40%.

But China’s readout of what happened in Argentina is different. China seems to believe that the only real movement was an agreement to halt additional tariffs and a mutual commitment to reduce the ones Trump and Xi put into effect this year.

In other words, Trump makes it sound like China is starting to cave to his demands. Top Chinese officials make it sound like the only thing that’s about to change is that U.S.-China trade relations would go back to where they were in January — before Trump unleashed his tariff war. – Washington Post

Cow dung!

The financial academics are going to have to develop a new theory and a “bullshit discount factor.”

Upshot

Today’s Doji stick makes it more tricky to call a Christmas rally.

Moreover, Mr. Mueller appears he is about to deliver to the White House his Christmas present. Will it be a shiny new bicycle and clean political bill of health or a Russian lump of coal? This will determine the mood of the tweets in the coming month, and, we know, tweets move markets in the short-run.

Yield Curve Inverts

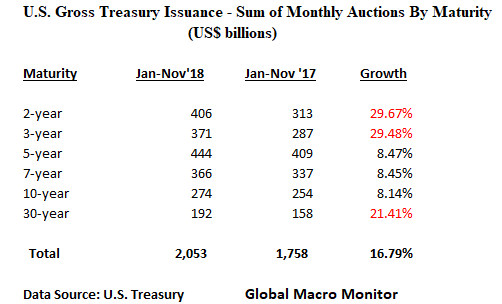

Have a look of this year’s Treasury auctions compared to last year.

With 2 and 3-year Treasury issuance growing at 30 percent and the belly and the 10-year growing at less than 10 percent, it doesn’t take a genius to understand why the yield curve is behaving the way it is. Are we wrong?

The Treasury seems to be running their own version of the Fed’s “Operation Twist.”

We think it was a mistake the Fed did not announce the unwind of Operation Twist, the manipulation of the yield curve pushing longer rates lower when it began to normalize interest rates and the balance sheet. Now market participants fret over distorted meaningless signals of Christmas past, which could, through reflexivity, have a real impact on the real economy.

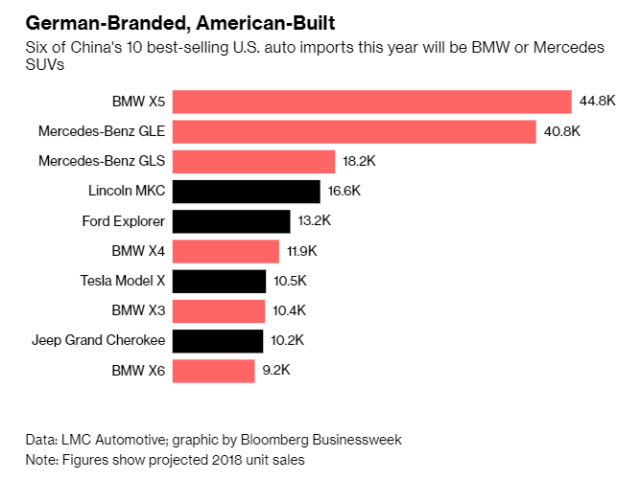

Of the ten best selling U.S. auto exports to China, six are German cars. The real world is not as simple and more complex than conventional impressions.

China’s tariff on car imports from all over the world was cut to 15 per cent from 25 per cent. But for US cars, China added a 25 per cent tariff over the summer, making the rate 40 per cent. – SCMP

So did China remove the 40 percent, of which 25 percent was in retaliation to the U.S. tariffs, on all U.S. cars, while the U.S. left its tariffs in place with the threat to escalate if negotiations go south? That interpretation should be highly discounted until more clarification.

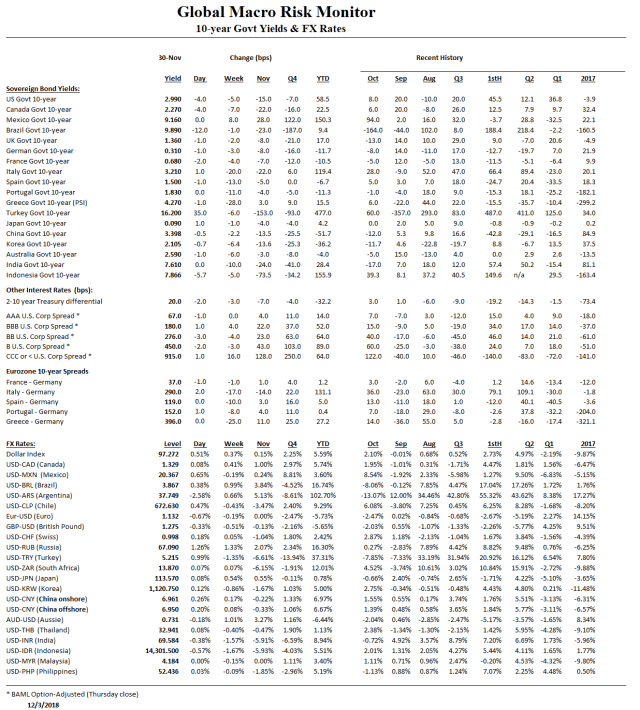

Most sovereign bond yields down on the month, led by hard-hit Turkey and Indonesian 10-years

The U.S. credit markets had a rough month

Argentina and Brazil currencies were lower with South Africa and Turkey recovering smartly. Nice EM bookends

Last week’s big stock rally allowed most stock indices to turn up for the month

Mexico’s Bolsa showing exceptional weakness as the new government takes over

Natural gas up yuge in November while crude oil down yuge

Commentary: Given that calling the short-term market is mug’s game, it is exceedingly more difficult when politicians and economic policymakers will not allow the markets to find their true or correct level. Everyone is now into market price manipulation: companies with their buybacks; central banks with their QE, and political leaders with their jawboning and selected, sometimes fake, news releases. This can’t be positive in the long-run. But, hey, we get our bonuses and reelected in the short-run, no?

Nevertheless, we believe, given all indicators point to, and the backdrop of a shrinking Fed balance sheet, coupled with bloating U.S. budget deficit and the crowding out effect, a high probability we have seen or are closer to the top than a new bull run.

The bullshit factor coming out of almost all governments is another factor traders must deal with. For example, the president just tweeted “China has agreed to reduce and remove tariffs on cars coming into China from the U.S. Currently the tariff is 40%.” It’s hard to unpack this.

China has agreed to reduce and remove tariffs on cars coming into China from the U.S. Currently the tariff is 40%.

China’s tariff on car imports from all over the world was cut to 15 per cent from 25 per cent. But for US cars, China added a 25 per cent tariff over the summer, making the rate 40 per cent. – SCMP

So did China remove the 40 percent, of which 25 percent was in retaliation to U.S. tariffs, on all U.S. cars, while the U.S. left its tariffs in place with the threat to escalate if negotiations go south? That interpretation should be highly discounted until more clarification.

We view the so-called “biggest trade deal ever” just a cease-fire with a still high risk of tanking.

Let the traders run with it, however.

The 2810-15 level on the S&P is critical, right about where futures are trading as we write. There is probably enough trader torque to take that out and rally this market into year-end.

Longer Term

The following charts were on Fareed Zakaria this morning, which capture our view of the U.S. market over the next few years. We will let you make your own inferences and investment decisions based on the charts

I was fortunate to work with the Bush #41 administration in developing and implementing their plan to resolve the 1980/90’s developing country (emerging markets in today’s parlance) debt crisis — The Brady Plan — named for his Treasury Secretary. Can you imagine today’s inhabitant of the White House allowing, say, Secretary Mnuchin to take credit for one of the administration’s signature policy triumphs?

President Bush always had a goal and a plan, which was always bathed in humility. No victory laps, no dancing on the Russians’ grave after communism fell.

All, severely lacking and a stark contrast to today’s political leaders.

The Fall Of Communism

I also was hired by the Polish government shortly after the communists fell as an economic and financial advisor to help the country restructure its debt and economy. My colleague and I had dinner one night with an administration official at a restaurant in Paris, which was once the childhood home/palace of Louis XIV.

The U.S. official conveyed to us the firm resolve of the Bush administration that it would not let Poland fail in their transition from communism to a market economy. They wanted to make Poland an example of a successful transition that the ex-Soviets/Russians could see and emulate. Poland became one of the superstar emerging economies over the next two decades.

Where Were The Europeans?

I was always perplexed where were the Europeans on the Poland issue? The German bankers, for example, were obsessed with one thing, getting their loans repaid with the smallest haircut possible, as they should have been. But why was the U.S. government the one leaning on the banks, including some of the largest in the U.S., to grant Poland a 50 percent debt haircut? Global leadership, that’s why.

The Europeans were not happy with the Bush administration over their hardball tactics in dealing with Poland’s private and Paris Club creditors.

Later, I found out the Poles, who were essentially broke, were being subsidized by the U.S. Treasury and my fees were effectively being paid by the American government, err the American taxpayer Japanese bondholders.

Kuwait

One of my best undergraduate college buddies, Malek, was from Kuwait. He told me that when Sadaam invaded in 1990, Sadaam’s brother, who led the invasion, set up headquarters in the house in front of his. Malek would rail against the Palestinians, many of whom were guest workers in Kuwait at the time because they sided with the Iraqis during the invasion. So much International Arab Brotherhood.

I called Malak a few years after the Gulf War who couldn’t talk as he was running out to celebrate the national holiday, “Festival of Gratitude,” in honor of George Herbert Walker Bush.

The celebration began as soon as a chartered blue and white Kuwaiti Airways jetliner landed, bringing the former President, his wife, Barbara, and other guests on his first visit to Kuwait.

The thousands lining the highway from the airport to the city included schoolchildren who were given a holiday for the occasion. Many waved small United States flags or balloons and others held signs. – NY Times

President Bush was also well connected to the golf world. He and #43 take a middle name from their maternal grandfather, George Herbert Walker, of the Walker Cup fame. His grandfather once had to suspend golfing legend, Bobby Jones, for throwing a club and wounding a female spectator, telling Jones, “You will never play in a USGA event unless you can control your temper.”

His golf pedigree can be found in his name. George Herbert Walker was his maternal grandfather, a former president of the United States Golf Association, who was instrumental in the founding of the biennial amateur competition that bears his name, the Walker Cup. Bush’s father, Prescott Bush, was also a former USGA president and a scratch golfer who impressed upon his son the importance of playing golf at a fast pace. – Golf World

President Bush proclaimed he was taught to play golf the proper way. He would often brag about his course record at Cape Arundel Golf Club in Kennebunkport, Maine. Was it a 63 or 64? “An hour and 20 minutes,” #41 would say.

Godspeed

R.I.P, President Bush. History will treat you well.

Sure, like all presidents, you made some mistakes. Nevertheless, we expect you’ll be among, or close to, the Top 10 before we see you on the other side.

A century ago, Argentina was one of the ten richest countries in the world. But crisis after crisis has earned it the dubious distinction of being the only nation ever to regress to developing country status. With hyperinflation, devaluations and IMF bailouts now facts of life, we meet the people who have lived through a major economic crisis roughly once every decade – including a taxi driver who lost everything in the 2001 crisis and now earns more money selling antiques. We also travel to some of the worst-hit places, where sermons from slum priest “Padre Toto” give people hope. But 2018 has once again tested Argentines’ patience. Inflation has topped 40% and the peso’s value has halved compared to the US dollar. Mauricio Macri’s government has tried to stem another crisis by signing up to the biggest bailout package in the IMF’s history. With the country’s future in limbo, the FT provides a glimpse into life in constant economic turmoil and asks: Can Argentina finally break the cycle of boom and bust?