My old stomping grounds just on left – 60 Broad. Goldie down the street on right at 90 handle Broad Street.

https://twitter.com/historyinpix/status/971303696566030339

My old stomping grounds just on left – 60 Broad. Goldie down the street on right at 90 handle Broad Street.

https://twitter.com/historyinpix/status/971303696566030339

Think “disarm” is the key, which is missing.

Thank goodness they’re talking, however, but not going to get lathered up just yet.

Didn’t the special envoy, Jimmy Carter, meet with the father in 2010?

And Half Baked.

Every little thing they do on trade is tragic

Everything they do is wrong

Even though the politics are more dramatic

Now I know trade diversion in steel is on

— paraphrasing Sting’s, Every Little Thing She Does Is Magic

Man, if you are going to rob a bank, rob the fricking bank!. Don’t do it half ass as your probability of going to prison and FUBAR go up exponentially.

Carving out countries exempt from the just proclaimed steel tariffs will do little to stop steel imports, in our opinion.

The reason? A form of trade diversion.

The steel tariff will shift trade from potentially lower cost producers, such as Korea and Brazil (a hypothetical, as we are not certain of relative prices) to Mexico and Canada, for example.

Think about it.

The relative price of steel imports from Korea and Brazil will go up 20 percent versus Canadian and Mexican steel. Importers will now import more steel from Mexico and Canada and less from Brazil and Korea. Of course, the volume may be restrained by the steel producing capacity of our good neighbors to the north and south.

Rather than importing 25 percent of our steel from Canada and Mexico the percentage likely could climb north of 50 percent. In order to provide incentives for local producers — the raison d’être of a tariff — the relative price of steel imports must increase across the board.

Injecting the term “short-term” on exemptions into the proclamation is probably enough to refrain Mexico and Canada from immediately expanding steel capacity and preventing China from moving their steel mills to Monterrey and Ontario.

Impact On Jobs?

Will the tariffs create new jobs in the United States? We suspect very little and not even close to what the president is touting. Even if they do, the steel jobs will be more than offset by losses in other sectors subject to higher prices and retaliation.

We are not sure if the president is getting good economic advice from those surrounding him. We even doubt they understand basic international trade theory.

Let’s see if the steel companies carry through with their announcements to reopen closed plants. Check back with us in one year.

Individual Tax Cut

The administration’s individual tax cuts were also half baked. Capping deductions for local property, income, and state taxes will have unintended consequences we have yet to discover and will be more clear on April 15, 2019.

If you are going to cut taxes, cut taxes and live with the consequences of higher debt. Find and dandy to find offsets, but don’t further distort an already distorted tax system.

We do give President Trump big kudos on the corporate tax cut.

It is All Politics

Note, today’s announcement on tariffs was a proclamation, not even a legal document. Only words, and we know, for certainty, with this president, words can mean whatever he wants them to, and can change day to day.

The timing of the announcement is hollow as it is political.

President Trumps plans to stump in Pennsylvania’s 18th congressional district this weekend, where the Democratic candidate, Conor and Republican, Rick Saccone, both support steel tariffs. The 18th is definitely steel country.

The special election in the Penn 18th is seen as a bellwether for the November midterms and an indicator of a potential major thumping of the Republicans.

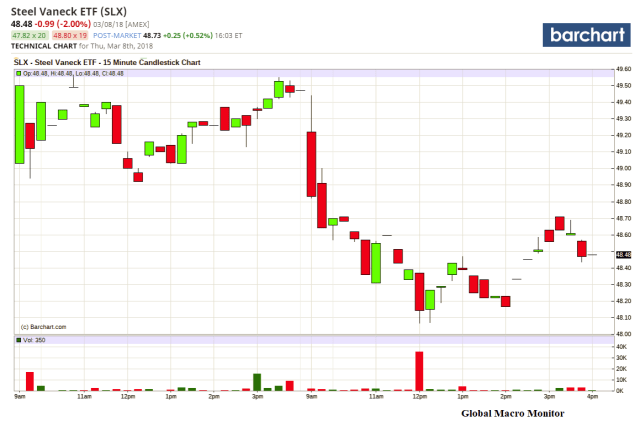

Steel Stocks

By the way, the steel stocks have been hammered since the exemptions were announced yesterday.

U.S. Steel (X) was down around 3 percent today, and off 6.4 percent from yesterday’s intraday high, and the steel ETF (SLX) fell 2 percent today.

A Better Way To Help Steel Workers

Finally, rather than offering the steel workers false hope, motivated for political reasons, we believe the optimal policy is to compensate the losers of free trade by subsidizing their income and retraining to thrive in the 21st century economy.

Why not make sure their kids are learning to code so they can program the robots that will be making steel in the future?

In the future, the steel industry could be higher tech, with more robots and fewer workers.

Industry leaders see the steel business evolving over the coming decade. Change could come fast and it could be painful.

U.S. Steel Chief Executive Officer Mario Longhi chaired a panel discussion on Manufacturing the Future: The Next Era of Global Growth at the World Steel Association’s annual conference at the Fairmont Chicago Millennium Park Hotel Sunday. Panelists talked extensively about robots taking over manufacturing jobs, but said technological advances could also create new positions such as for digital mechanical engineers, data scientists and business operations data analysts. – NWI Times

Here is a personal story about a time when politicians really cared for those hurt from free trade yet understood trade benefited the majority.

The Reagan White House

After finishing up my Ph.D. comprehensive exams in economics and in between the dissertation, I interviewed at the White House, Council of Economic Advisors (CEA), as a junior economist. They had a program where the CEA would hire graduate students for one year who were in between their comp exams and the dissertation.

Ronald Reagan was President at the time and the day long interview took place in April 1986, just a few days after the U.S. bombed Muammar Gaddafi. That day, security on the White House grounds and in the Old Executive Office Building, where the Council is located, was intense. Secret Service, dressed in their black garb and flack jackets, everywhere.

Beryl Sprinkel was Chairman of the CEA and Michael Mussa was the real intellectual heavy weight of the CEA. The entire council was made up of “Chicago Boys,” not Chileans, but academics from the University of Chicago. Very free market thinking in everything.

Note, this was during a period in the economy when the trade sector was getting hammered by the strong dollar. The trade weighted U.S. dollar index had increased almost 30 percent since Reagan took office and was causing real hardship in the tradable goods sector.

So, the first question I was asked at the beginning of the interview was, “there is a bill in Congress to write the steelworkers, who have been displaced and lost their jobs through trade, a check for $100,000 [$221,000 in 2016 dollars]. What do you think of this bill?

I answered, “no, I think retraining and other polices may be more optimal”. They replied, “that’s what the Democrats think.” I didn’t get the job.

The Chicago boys think the individual can choose their future and retraining better than the government.

That $100,000 was real money and compensation back then, much more than what the government offers to the losers of free trade and globalization today. And, let’s get real, at the end of the day, it was an “effective bribe” to the steelworkers to allow the country to keep pursuing free trade policies.

The day long interview ended in Beryl Sprinkel’s office where he asked me, “[Gregor], can you make good charts? The President likes his charts.” Indeed, President Reagan did.

When I was leaving the Old Executive Office Building (OEOB) after the interview, I thought of taking a little tour of the White House grounds. I walked out of the east end of OEOB onto the White House grounds, probably no less than 100 feet from the Oval Office. I was met by a Secret Service officer in a black flack jacket carrying a high powered rifle, who asked what I was doing there. He booted me faster than a fighter jet. But, oh, so close to power!

So, concluding, I ask folks — whatever happened to that kind of thinking among the policymakers? That is, really compensating and taking care of the losers from free trade and globalization as we, the elites, enjoy the benefits of free trade and globalization in lower prices of goods and higher profit margins and stock prices? Tariffs and shrinking free trade and globalization are going to hurt all of us, including margins and stock prices.

Better compensation for the losers and continue to pursue free trade. Tariffs help a small minority and hurt the majority — a Tyranny of the Minority, if you will.

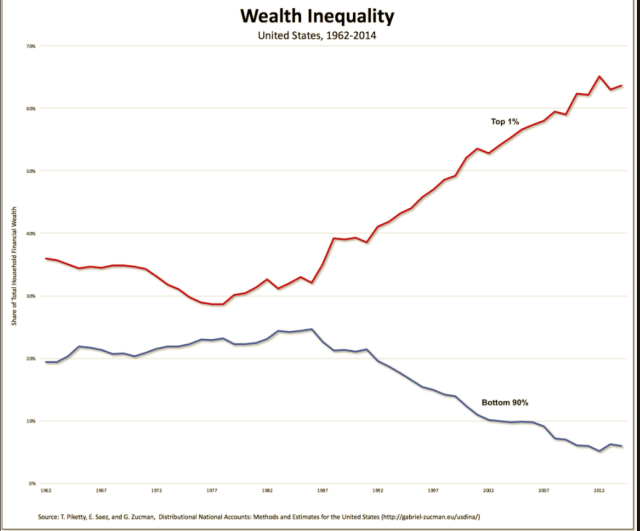

This is not a chart that generates confidence in future political and social stability. It looks like the jaws of a Great White ready to bite someone in the arse.

Clearly a contributing factor in the rise of populism and anti-elitism, and 2016’s political Black Swan. It will only get worse during the Trump administration and then we suspect the country will soon make a hard left turn. Stay tuned.

Hat Tip: Real-World Economics Review Blog

Bouncing around. Doesn’t seem like many real sellers out there. Traders and ‘bots push the indices down and then have to cover into the close. We wrote about this in our Week In Review post this past Sunday.

Risks are building in the markets but so is bearishness. Though markets are going to do what they are going to do in short-term, we have learned there are still not a lot of natural sellers, and if the market gets too offside, you can bet the other side for a trade.

The fast money is now so short-term focused, especially the growing number of HFTs that don’t hold overnight risk, they have no patience and must cover quickly especially if the market begins to move against them. We do believe investors are going to get a chance to buy stocks and much lower levels, however. – GMM, March 4

Market Commentary

The market rallied back from the Gary Cohn sell-off to finish slightly lower on the news that President Trump is softening up his tough trade talk. The White House indeed speaks hardly, and carries a small stick. Full of bluster and fake thunder, markets just are not buying it anymore.

Press secretary Sarah Huckabee Sanders told reporters the exemptions would be made on a “case by case” and “country by country” basis, a reversal from the policy articulated by the White House just days ago that there would be no exemptions from Trump’s plan. – U.S. News

Not surprised as we speculated yesterday but we are with the Paper Tiger on this one. Unfortunately, his reputation as a policy flake and Paper Tiger is growing and increases the risk of miscalculation by an adversary.

If leaders around the world take Trump seriously, it is because of the dangers such an unserious man with such enormous power represents. – WPR

S&P500

The S&P500 found support right at the 20-day moving average and the key 50 percent Fibonacci retracement level at 2,702 before rallying about one percent into the close.

Eye On Politics and Friday’s Employment Data

The president may reverse again and harden on tariffs as he campaigns in Pennsylvania’s 18th congressional district this weekend, which he won by 20 points 2016. The Democratic candidate, Coner Lamb, now leads Republican, Rick Saccone.

President Trump has specifically mentioned that the special election played a role in the administration’s trade policy. The special election is seen as a bellwether of what may be a potential lambasting of the Republicans in the November midterms.

Tariffs now take a back seat to the average hourly wage number in Friday’s employment data.

Great chart from the Visual Capitalist brought to of us from our favorite Polish crude and rude trader, the Skrypecker.

Now you can see why the markets work themselves into a deflationary tizzy when China hits a speed bump.

Given all the noise around the Trump Tariffs, we have updated our ranking of the world’s 2018 Current Account Balances (CAB) by country from largest surplus to biggest deficit, both as a percentage of GDP and in US$ billions, in the ginormous table below. The data are estimates from the October 2017 IMF’s World Economic Outlook database.

However, first, check out the current account balances of the G20. We suspect Germany will be under increasing pressure from the Trump administration to reduce its surplus, which is mainly the result of the country’s high savings rate.

Let us begin with a little primer on how the current account balance is determined.

We posted this in January 2017, before President Trump was inaugurated.

Trump Fiscal Policy and the Current Account Deficit

If President Trump succeeds in implementing his proposed tax cuts and $1 trillion infrastructure spending plans, the U.S. current account deficit, by definition, will, once again, balloon as net public savings will decline and, we believe, will be complemented by a decline in net private savings as business investment and private consumption increases. This is the simple national income identity,

(S-I) + (T-G) = Current Account Balance (Foreign Savings)

(S-I) is the ‘private savings balance’ or the difference between private sector savings (S) and investment (I); (T-G) is the ‘government balance’ or the difference between tax receipts (T) and all government expenditure (G); (X-M) is the difference between exports (X) and imports (M) and is usually called the simple ‘current account balance’. –

President-elect Trump does not like trade deficits, and we suspect he will be perplexed by the continued deterioration of the current account deficit caused by his macro policies. This risks that his administration may implement even greater international trade distortions to try and reduce the trade deficit.

The U.S. current account deficit is indeed deteriorating, not because of unfair trade practices but because of domestic economic imbalances. Somebody call Peter and Wilbur.

Public Savings, Government Budget Deficits, And The Current Account

The following scatter plot attempts to illustrate the relationship between net public savings and the current account. It does not include net private savings, generally a larger factor in the relationship. We have omitted some extreme outliers (45 percent CA surplus, for example). The trend line does shows a clear positive relationship.

Current Account Surplus = Foreign Savings

Finally, the ginormous table on country current account balances.

We have also added the U.S. Treasury holdings of most of the top 20 surplus countries. A country’s current account surplus is simply excess savings shipped abroad, mainly recycled into U.S. Treasury securities, since the dollar is the main reserve currency, which helps to keep interest lows in the United States.

In fact, as of the end of 2017, 36 percent of all marketable Treasury notes and bonds, excluding the Fed’s holdings, were held by 16 of the top 20 current account surplus countries, of which China and Japan hold almost 25 percent.

Given the U.S. high dependence on foreign savings to finance everything from consumption, infrastructure and budget deficits, there will be much macro wrenching and shrinkage of foreign financing if policymakers resort to gimmicks and artificial measures to reduce the trade and current account deficit.

The policymakers should focus more on sustainable policies to increase private and public savings.

Amen.

.

Yes, we believe so.

https://twitter.com/HistoryInPix/status/967915137142280192

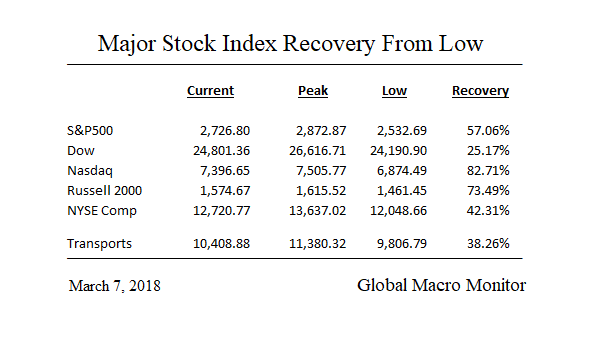

Maybe not tomorrow, maybe not next week, but sometime this year the S&P500 will break into bear market territory at 2,298.30, 20 percent off its January 26th high, and 15.76 percent down from today’s close.