We are still dazed and a bit livid over President Trump’s call for QE4, and increasingly perplexed how the market just takes such absurdities, including his latest nominees to the Fed, in stride. Is .999 percent the next target for the Fed’s IOER?

We feel as we have been transported to a parallel universe. Facts, words, data, logic, decency, truth, nothing matters anymore. Just make me some more Benjies!

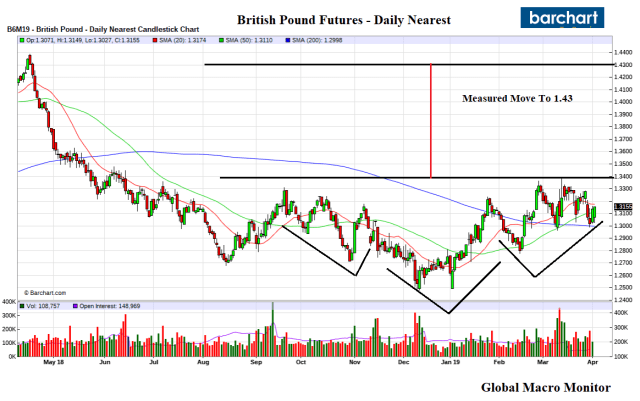

Our revulsion to the QE4 call motivated Global Macro Monitor’s last post, POTUS’ Morning Economic Briefing. Have a look.

Predictive Analytics Of Trump’s Decision Making

We have always thought if an AI predictive analytic algorithm was constructed to analyze and forecast the Trump administration’s decision-making process it would be dominated by the policy conditional,

If the Obama administration supported, proposed or implemented such a policy, then reverse and do the opposite.

Iran, the TPP, and Obamacare. Shall we go on?

There is zero doubt, in our mind, Russian and Chinese government engineers have already generated such an algo or a reasonable facsimile.

S&P500 Performance 26 Months After Inauguration

Using the above logic, the only justification we can conceive for calling for a QE4 unless Trump knows the China trade deal is toast is to further goose the stock market as Trump’s S&P is significantly lagging Obama’s market 557 trading days after the two governments came to power. President Trump is probably aware of and likely obsessed with these relative returns.

The following chart comparing the change in both presidents S&Ps since their respective inauguration date to early April into their third year will surprise many. We had to go back and check our calculation no less than three times. The power of gaslighting!

The data is especially shocking given the “the best economy ever, the greatest stock market ever” rhetoric coming from Trump and his so-called economic advisers. That shit is getting old, folks, and really starting to wear on us.

Why The Obama Outperformance?

Absolutely, there is logic in explaining the differential.

Such as Obama took office when the stock market and economy were collapsing and Trump inherited a bull market and strong economy, so Trump’s market hasn’t experienced the “trampoline effect” that Obama’s S&P did.

But, truth, logic, facts, and data don’t matter anymore, folks. Opinions and pronoucements are the new facts and data in the new Oceania AmeriKa.

The V bottom

Markets are now all about V bottom Fed bailouts. Market Socialism is Capitalism.

We expect the S&P500, driven by what we have tagged the Power of Zero, to close the year at around 3025, of which most of the rest of the year gains will take place in late Q3 and Q4. We then expect a Big Dipper sell-off, say, at least 35 percent, for the reasons we have posted earlier, to a level of around 1984 for the S&P.

Can you connect the cryptic dots here?

Of course, our speculation is only a calculated guess as nobody knows the future.

BFTP

BFTP = Blast From The Past

Reagan v Trump Macro Initial Conditions

Posted December 26, 2016

We hear lots of talk these days about, Why Donald Trump’s Market Rally Echoes Ronald Reagan’s.

We are big fans of Chaos Theory,

Chaos theory is a branch of mathematics focused on the behavior of dynamical systems that are highly sensitive to initial conditions—a response popularly referred to as the butterfly effect.[1] Small differences in initial conditions (such as those due to rounding errors in numerical computation) yield widely diverging outcomes for such dynamical systems, rendering long-term prediction of their behavior impossible in general.

So we thought we’d take a look at the macroeconomic initial conditions at the start of the Reagan Presidency versus the incoming Trump Presidency.

Check out the data:

In most macro categories that we have researched here, the initial conditions just aren’t there for a Reagan type bull market, in our opinion. First, and foremost, are the monetary headwinds.

Monetary Conditions

Reagan began his Presidency with interest rates nowhere to go but south with a 22 percent Fed Funds rate and a 10-year Treasury yield of 12 1/2 percent. Though interest rates were not the policy target of the Fed at the time, just several months into the Reagan Presidency the 35-year bond bull market ignited and drove almost all asset prices from real estate to stocks, including the expansion of the price to earnings multiple.

The polar opposite monetary conditions exist at the advent of the Trump Presidency. Interest rates have nowhere to go but north, we believe, especially if Mr. Trump’s fiscal policy is implemented.

Unemployment

Mr. Trump will not have the labor slack and surplus to draw upon to drive economic growth. The country is pretty much at full employment although the level of tautness in the labor market can be debated. This risks much higher inflation than anticipated if his policies are passed and thus a more aggressive Fed. Also note the aging of the baby boom generation, which has driven much of the growth over the past 30 years.

Total Debt

President Reagan began his Presidency with a relatively small stock of debt. Mr. Trump will inherit a debt-to-GDP ratio almost three times that of President Reagan. This leaves less room for deficits as a result of his tax cuts and increased spending. The Trump plan is to increase economic growth and thus tax revenues through supply side and micro and regulatory policy. This is the second chance for this argument to succeed. Watch this space.

The high debt stock, coupled with expected large deficit spending, risks a spike in real interest rates and a sovereign credit downgrade.

Real Oil Price

President Reagan took office with a relatively high real oil price. Note this was in an era when high oil prices were considered “bad” for the economy. The real oil price dropped almost 75 percent in the first five years of the Reagan administration. President Trump will inherit a real oil price half that of Mr. Reagan, coupled with the ambiguity of not knowing if higher oil prices are good or bad for the economy. We don’t know where to go with this one.

Dollar

Mr. Trump inherits a real trade-weighted dollar a little over 10 percent stronger than President Reagan and, most likely, headed north given the world’s divergent growth and monetary policies. This could act as a headwind on corporate profits and export growth.

Individual Marginal Tax Rates

This is the pearl and central to the supply side argument. Cutting marginal tax rates to incentivize economic behavior and growth, which will increase tax revenues that offset the revenue loss from the tax cuts. Note, President Reagan, cut the top rate from 70 percent to 28 percent. That was Yuuuge! Mr. Trump just doesn’t have the room to do such large tax cuts as he starts at a lower base with the highest tax rate at around 40 percent.

Corporate Profit Margins

President Reagan took office with a lot of corporate inefficiency and room to expand corporate profits. It feels we are close to peak margins. Didn’t we just have an election to improve the wages of the average worker? Watch this space.

Stock Valuations

Much like the debt stock, Mr. Trump will inherit a stock market that is relatively highly valued. Note, one of Warren Buffet’s stock market valuation metrics, Stock Market Cap to GDP, is more than 160 percent higher now than it was when President Reagan took office. The U.S. will need lots of economic growth to “grow” into this metric.

Conclusion

There you have it. The macroeconomic initial conditions at the beginning of two Presidencies. This is just our first quick whack at this analysis.

President Trump is going to have to depend on “animal spirits” to do a lot of the heavy lifting and exquisite execution of supply side, microeconomic, and regulatory reform to increase potential GDP growth. Higher growth will increase the top line of companies and improve earnings. But we think, after looking at the data, the window is narrow.

Can we rally a lot? Absolutely. And probably will given the better business conditions initially created by regulatory reform and the fiscal stimulus.

A Reagan bull market? We don’t think so.

By the way, and contrary to the conventional wisdom, the Reagan bull market is only the 5th largest Presidential bull market since Teddy Roosevelt, just behind the Obama bull market.

We could be wrong and it surely hasn’t paid to short or underestimate Donald Trump. But, he just won’t, and probably, can’t, have the macro tailwinds that President Reagan had at his back given the initial conditions of the macro data.

Stay tuned.

Note To Our Readers

The Global Macro Monitor website will be under construction over the next several weeks as we search and construct a “fair path” to protect our contributors from the free riders. We have a few more posts in the pipeline but they will be few and far in between. If you are a contributor email us and we will send out our ongoing data analysis or the research you depend on. Cheers.

Interest rates in the U.S. are affected and somewhat anchored by the German bund yield.

Interest rates in the U.S. are affected and somewhat anchored by the German bund yield.