https://twitter.com/jesuscasique1/status/1112874597576294402?s=12

The British Parliament is inching ever so closer to a “People’s Vote,” a second referendum on the UK leaving the European Union. We have never wavered and were way out in front of this issue,

BREXIT ain’ gonna happen. The political extremes on both ends have “woke” the sleepy and complacent middle, women, and the young.

…A second vote on BREXIT is an uphill battle, but if the Trump administration gets “bitch slapped” in the November midterms the momentum and pressure for a new BREXIT vote will build, in our opinion. — GMM, October 20th

Today’s Independent dishes on the prospects of a “People’s Vote,”

MPs have begun a fresh push to agree an alternative Brexit plan that would be put to a referendum in the autumn, despite throwing out all options last night.

Talks will begin to settle on a “composite motion”, combining soft Brexit proposals with a commitment to putting them to the people to confirm – with the alternative of staying in the EU.

Anna Soubry, who defected to The Independent Group from the Conservatives, insisted a compromise was still achievable and that supporters of a Final Say referendum were making “huge progress”.

“I believe we can now reach, in parliament, a majority based on progress we made last night for such a compromise, composite motion. That’s what we’ll be working on this morning,” she said.

Ms Soubry pointed out that the number of Tories backing a referendum was rising – from 7 to 15 on Monday night – and that, with 280 votes, a confirmatory ballot was the most popular option. – Independent, April 2nd

Not a trade without some risk but,

As always, we reserve the right to be long and wrong.

Artificial intelligence is already shaping the world, from driverless cars to dating. But according to Dr Eric Topol, a pioneer in digital medicine, perhaps its greatest impact will be on people’s health.

Click here to subscribe to The Economist on YouTube: https://econ.st/2xvTKdy

Grab your popcorn and strap yourself in, folks, for the coming political donnybrook over the full release of an unredacted version of the Mueller Report. Me thinks it will be kicked up to the Supremes to decide.

The above is exactly why we vote for full transparency with the exception of possibly some minor, but necessary, redactions to protect Agent Smith.

See our post, Newton’s Q1 Law Of Motion For The S&P, by clicking here

The past few weeks were a classic exercise in how markets tend to “retrofit” price action to their expectations of economic fundamentals and illustrates the risk of a self-fulfilling feedback loop. The 10-year bond yield fell more than 40 basis points from March 1 to March 27 and the 10-year less 3-month yield curve temporarily inverted, leading even the President’s top economic advisor and his nominee to the Federal Reserve to call for an emergency 50 bps interest rate cut by nation’s central bank.

Day trading the market and economic noise to set longer-term economic policy can be dangerous thang. That’s Chauncey Gardener-esque, folks, and puts the credibility of U.S. policymaking into question.

Why Did Rates Collapse In March?

Nobody really knows for certain but we suspect it was the collapse in the 10-year German bund yield, which crossed over into negative territory once again, falling from 18 bps on March 1 to -8 bps on March 27th. The German manufacturing sector is now in a “deep recession” and the shortage of German bunds due to ECB asset purchases has distorted the economic signal of interest rates.

Interest rates in the U.S. are affected and somewhat anchored by the German bund yield.

Interest rates in the U.S. are affected and somewhat anchored by the German bund yield.

Nevertheless, we were a bit perplexed by the sharp move down in U.S. yields as we didn’t see the U.S. economy collapsing. Au contraire,

Note the Atlanta’s Fed GDP now forecast for Q1 2019 has moved up from around 0.5 percent at the beginning of the month to around 1.2 percent, which is a big move lost on the markets. – GMM, March 22

Markets are way over their skis on the deflation and growth scare.

The Atlanta Fed’s GDP Now Q1 forecast has skyrocketed over the past few weeks, up from 0.3 percent to 1.7 percent. There is no deflation and it’s entirely possible the Cleveland Fed Median CPI prints 3 percent y/y in March with energy prices now skyrocketing. The daytraders in and out of the administration calling for a 50 bps rate cut are panicked and clueless unless they see something nobody else does. Could they be signaling the China trade deal is in trouble? Just askin’. – GMM, March 31

The GDP now Q1 forecast is currently at 2.1 percent.

Moreover, the talk of deflation is just nonsense.

…the Fed began sucking dollars out of the economy. This combination of a reduced supply and heightened demand for dollars produced an entirely unnecessary deflation. – Stephen Moore, Wall Street Journal, March 13th

Actually, that sucking sound is not the Fed reducing bank reserves but it’s the U.S. Treasury increasing the size of its monthly note and bond auctions in order to maintain its balances (checking account) at the Fed as the central bank shrinks its balance sheet. That is coming to end in September, however.

Take a look at the Cleveland Fed’s Median CPI running at an annual rate of 2.7 percent, which may approach or breach 3 percent for March with the rise in energy prices.

What Now?

If you have been reading GMM, you know our thoughts on equities. The sheer momentum of such a strong first quarter carries over into the rest of the year, which is the justification of our year-end S&P target of 3025.

There has not been one year since 1950, not one, where the S&P has increased by more than 10 percent in Q1, after experiencing a negative prior year, which didn’t close the year up less than 20 percent. It’s Newton’s Q1 Law of S&P Momentum. Is this time different?

We don’t think the move will be sustainable, however, and are selling the strength in the final three quarters, which we suspect the bulk of the final move will take place in Q4.

Bonds

Bond yields are more interesting.

Clearly for yields to take off and move much higher, Euro yields will need to get off the mat. The German manufacturing sector may emerge and show some improvement if China has truly bottomed. We also expect pressure to build on German policymakers to introduce a significant fiscal stimulus.

We are now watching the key levels of 2.57, 2.63 (50-day), and 2.70 percent as the next hurdles for the 10-year to heal thyself. Stay tuned.

Newton’s three laws of motion may be stated as follows:

- Every object in a state of uniform motion will remain in that state of motion unless an external force acts on it.

- Force equals mass times acceleration.

- For every action, there is an equal and opposite reaction.

The first law, also called the law of inertia, was pioneered by Galileo. This was quite a conceptual leap because it was not possible in Galileo’s time to observe a moving object without at least some frictional forces dragging against the motion. In fact, for over a thousand years before Galileo, educated individuals believed Aristotle’s formulation that, wherever there is motion, there is an external force producing that motion. – Stanford University

Quite A Quarter!

The S&P500 was up 13.07 percent in the first quarter, the best since 1998 and the seventh best first quarter since 1950. Of all 276 quarters since 1950, Q1 2019 ranked 17th, in the 94 percentile and the best since Q3 2009. The index experienced a huge trampoline effect, bouncing off and reversing the 13.97 decline in Q4 2018, which ranked as the 10th worst performing quarter since 1950 placing it in the 3.6 percentile of S&P quarterly moves.

A Q1 S&P With Momentum Tends To Gain Momentum

Of the 10 first quarters where the S&P has increased over 10 percent, only one, 1987, has finished lower for the year. The data below also illustrate that the annual change for the S&P when the index was up more than 10 percent in Q1, averages 20.65 percent.

Using that average and extrapolating from Friday’s close would put the year-end S&P500 at 3025, or about 2.85 percent above the all-time high of 2940.91. We will use that as our target, which doesn’t violate our longer-term bearish view. Bear markets tend to climb back after a sharp sell-off to make a new nominal high before rolling over hard. This was certainly the case in 2007.

The underlying fundamentals just are there to have confidence the coming move as a sustainable one. The market certainly is not cheap.

In addition to our concerns about valuation, we don’t like the high levels of public and corporate debt, the changing structure of the U.S. Treasury market, the increasing market manipulation by governments (i.e., market socialism), the shifting geopolitical tectonic plates, including the recession of American global leadership and the end of Pax Americana, local domestic politics, and geopolitics, in general. We could go on.

Power Of Zero

We believe the Power of Zero, that is zero to negative bond yields, or the fear of, will be the main driver of equity markets until year-end. Walter Bagehot liked to quote the famous market aphorism as a powerful motivation for savers to chase risk,

JOHN BULL can stand many things but he cannot stand two per cent – Economist

Not without volatility, however.

Strap yourself in, it’s going to be an interesting rest of the year.

Traders and bears are going to be forced into this market. Stay tuned.

As the saying goes, “if you stare at the charts long enough, you can see any pattern you what to see.”

We weren’t even staring but spotted this cloud pattern last week.

It looks similar to only a pooh bear, however. So is it an omen of only a 30 percent bear market to come?

Summary

Commentary: The stock market usually bounces after a down year as back-to-back down years are very rare. The Dow’s probability of an up 2019 is close to 90 percent.

Markets are way over their skis on the deflation and growth scare.

The Atlanta Fed’s GDP Now Q1 forecast has skyrocketed over the past few weeks, up from 0.3 percent to 1.7 percent. There is no deflation and it’s entirely possible the Cleveland Fed Median CPI prints 3 percent y/y in March with energy prices now skyrocketing. The daytraders in and out of the administration calling for a 50 bps rate cut are panicked and clueless unless they see something nobody else does. Could they be signaling the China trade deal is in trouble? Just askin’.

Moreover, if Trump closes border with Mexico bad economic news to come.

If the bottom is in with the China growth scare, bonds are in for a big pasting in the next quarter. An uptick in China will also help sentiment in Germany and Europe.

We expect the Q1 momo to continue in stocks, with the S&P making a nominal new high by year-end at around 3025, 2.85 percent above the all-time high, before the continuation of the bear market, which began in Jan 2018, and the next Big Dipper hits. This is based on a simple extrapolation of the momentum that takes place after such a strong first quarter after a down year.

The S&P500 finished March close enough for government work to our February 4th expectation, so we are taking a victory lap.

If history is any guide, given the historical start to the year, the S&P should finish March at or around 2850-ish. – GMM, Feb 4th

Happy hunting next week and the quarter, folks!

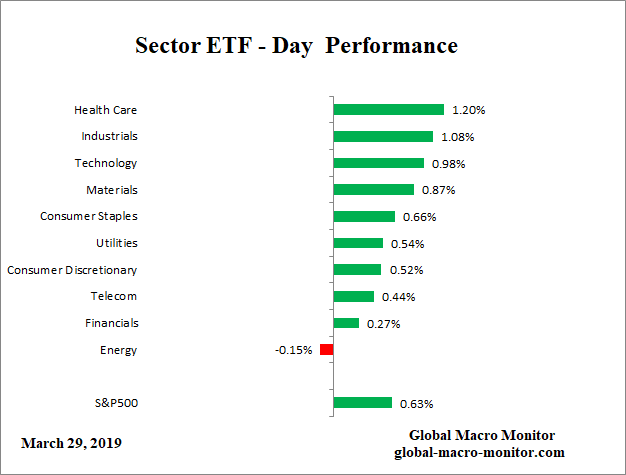

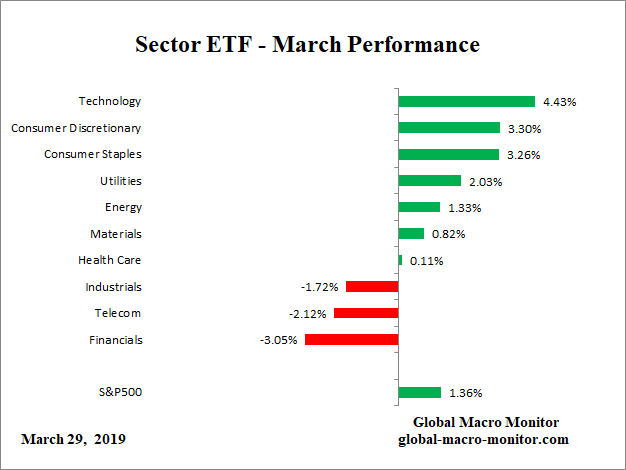

We will be phasing out free rider access to the Sector ETF Performance during our website overhaul to take place over the next month. Contribute by clicking on donate widget on the right-hand side of the website.

We will be phasing out free rider access to the Global Risk Monitor during our website overhaul scheduled to take place over the next month. Contribute by clicking on donate widget on the right-hand side of the website.